- Biotechnology

- Adult Hemoglobinopathy Testing Market

Adult Hemoglobinopathy Testing Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Adult Hemoglobinopathy Testing Market by Test Type (Hemoglobin Electrophoresis, High-Performance Liquid Chromatography (HPLC), Genetic Testing, and Others), Indication (Sickle Cell Disease, Beta Thalassemia, and Alpha Thalassemia), End-user (Hospitals, Diagnostics Laboratories, and Specialty Clinics), and Regional Analysis from 2026 to 2033

Adult Hemoglobinopathy Testing Market Share and Trends Analysis

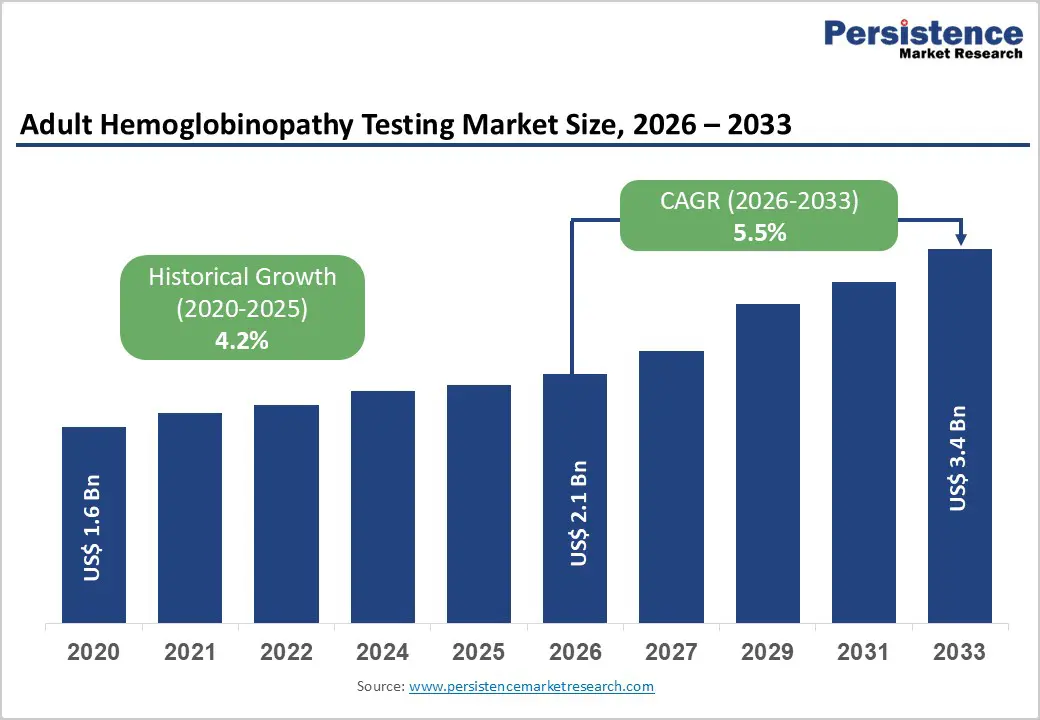

The global adult hemoglobinopathy testing market size is estimated to grow from US$ 2.1 billion in 2026 to US$ 3.4 billion by 2033, growing at a CAGR of 5.5% during the forecast period from 2026 to 2033.

Global demand for adult hemoglobinopathy testing is rising rapidly, driven by increasing prevalence of inherited hemoglobin disorders, improved survival of pediatric patients transitioning into adulthood, and growing clinical emphasis on early and accurate diagnosis to prevent long-term complications. Hospitals and specialty hematology centers are increasingly utilizing hemoglobin electrophoresis, HPLC, and genetic testing to support routine screening, confirmatory diagnosis, and disease monitoring.

Rising investments in diagnostic infrastructure, expansion of laboratory networks, and the growth of integrated screening and referral programs are accelerating global adoption. Continuous advancements in automated electrophoresis systems, high-throughput HPLC platforms, next-generation sequencing, and AI-enabled laboratory analytics are significantly improving diagnostic accuracy, workflow efficiency, and turnaround times. Additionally, growing adoption of guideline-based screening protocols, rising disease awareness linked to public health initiatives, and expanding clinical evidence supporting early detection are further propelling global market growth.

Key Industry Highlights:

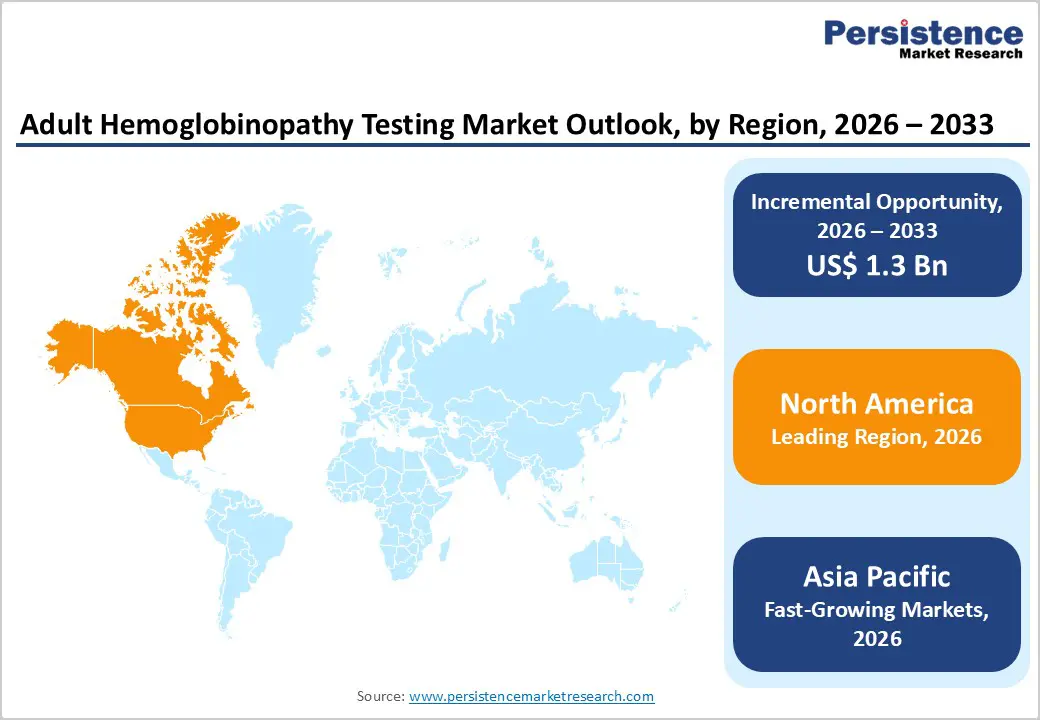

- Leading Region: North America holds the largest share at 47.8%, supported by advanced diagnostic infrastructure, high adoption of standardized screening protocols, strong healthcare expenditure, and early access to FDA-approved adult hemoglobinopathy testing technologies.

- Fastest-Growing Region: Asia Pacific is expanding the fastest due to a large affected population, rapid modernization of diagnostic laboratories, increasing medical tourism, and growing investments in laboratory and screening capacity.

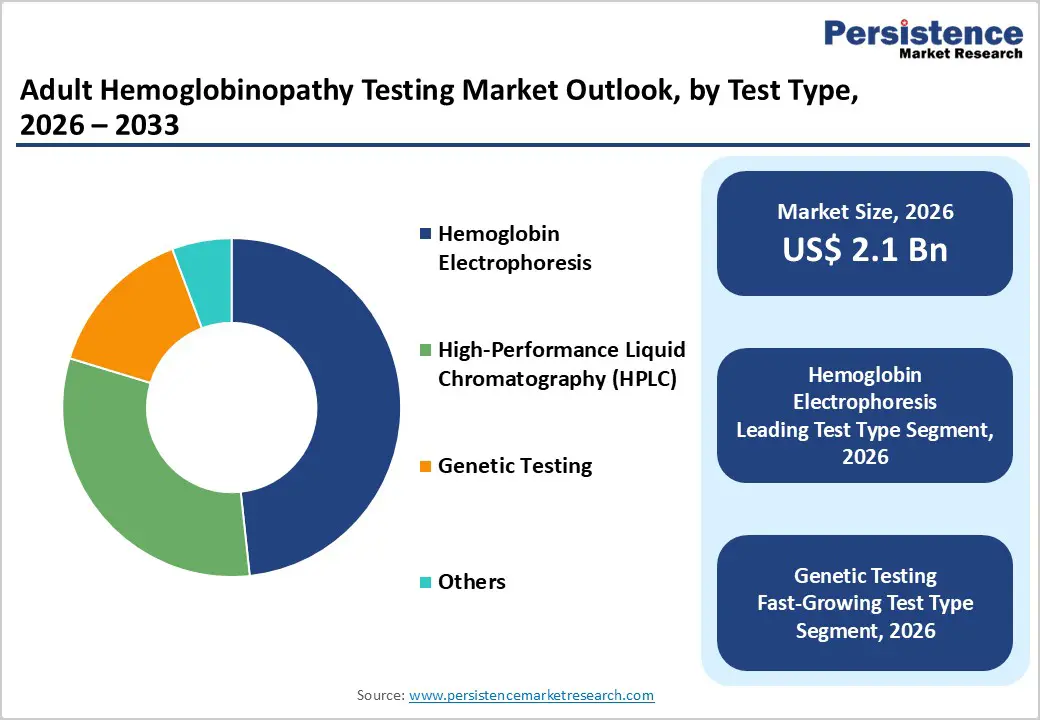

- Leading Test Type Segment: Hemoglobin electrophoresis dominates the market due to its extensive use in screening and confirmatory algorithms, offering high specificity and long-term diagnostic reliability.

- Fastest-Growing Test Type Segment: Genetic testing is growing rapidly, driven by increased awareness, declining sequencing costs, and the expanding use of molecular diagnostics, which support broader adoption for carrier detection and complex case resolution.

- Leading Indication Segment: Sickle cell disease remains the top application, driven by high adult disease burden, routine monitoring requirements, and strong integration of diagnostic testing into long-term disease management pathways.

- Fastest-Growing Indication Segment: Beta thalassemia testing is scaling quickly as demand increases for precise variant identification, carrier screening, and advanced diagnostics to support moderate-to-severe disease management.

| Key Insights | Details |

|---|---|

| Adult Hemoglobinopathy Testing Market Size (2026E) | US$ 2.1 Bn |

| Market Value Forecast (2033F) | US$ 3.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Dynamics

Driver - Rising Adult Disease Burden Supported by Expanded Screening and Awareness Initiatives

The global adult hemoglobinopathy testing market is witnessing sustained growth due to the rising adult prevalence of inherited blood disorders such as sickle cell disease and thalassemias. For instance, in 2024, data from the Centers for Disease Control and Prevention (CDC) indicate that sickle cell disease (SCD) affects approximately 100,000 individuals in the U.S., with over 90% of patients being non-Hispanic Black or African American and an estimated 3%-9% belonging to Hispanic or Latino populations. Despite advances in clinical management, the disease continues to impose a significant long-term health burden, as individuals with SCD in the U.S. experience an average life expectancy more than 20 years shorter than the general population, highlighting the critical need for sustained diagnostic monitoring and early adult-stage disease management.

Advances in pediatric diagnosis, early intervention, and long-term disease management have significantly improved survival rates, resulting in a larger cohort of patients transitioning into adulthood and requiring lifelong clinical monitoring. In parallel, population growth in high-prevalence regions across the Asia Pacific, the Middle East, and Africa is further increasing the absolute number of affected adults. This expanding patient base is driving consistent demand for routine screening, confirmatory diagnostics, and disease surveillance across hospital and reference laboratory settings.

Increasing public-health screening initiatives and heightened clinician awareness are driving higher testing volumes globally. Government-led programs focusing on carrier screening, premarital testing, and adult disease identification are being implemented across multiple regions to reduce disease burden and improve early detection. Medical education efforts, guideline-driven diagnostic pathways, and advocacy initiatives led by patient organizations are improving clinician adherence to standardized testing protocols. Together, these initiatives are expanding access to diagnostic services, increasing referral rates, and strengthening the role of hemoglobinopathy testing as a core component of adult hematology care pathways.

Restraints - Infrastructure and Interpretation Challenges Limiting Diagnostic Adoption

In many low- and middle-income regions, inadequate laboratory infrastructure and shortages of skilled diagnostic professionals remain significant barriers to the widespread adoption of adult hemoglobinopathy testing. Limited availability of automated electrophoresis systems, HPLC platforms, and molecular diagnostic technologies restricts testing capacity, particularly outside major urban centers. Additionally, insufficient training in hematology diagnostics and laboratory quality management affects test accuracy, turnaround times, and clinical confidence. These constraints reduce access to reliable screening and confirmatory testing, delaying diagnosis and limiting effective disease monitoring among adult patient populations in high-burden geographies.

Moreover, the complexity of interpreting hemoglobin variants and the lack of standardized reporting frameworks further restrain market growth. Adult hemoglobinopathies often present with overlapping or rare variants that require specialized expertise to interpret accurately, particularly when using advanced molecular or hybrid testing approaches. Variability in result formats, reference ranges, and nomenclature across laboratories can lead to inconsistent clinical interpretation and hesitation among physicians to rely on test outcomes for decision-making. The absence of universally harmonized diagnostic guidelines and reporting standards increases the risk of misclassification, reducing clinician confidence and slowing adoption, especially in non-specialist healthcare settings.

Opportunity - Advancement of Integrated Molecular and Point-of-Care Diagnostic Solutions

The adult hemoglobinopathy testing market is witnessing a strong opportunity through the bundling of hemoglobinopathy assays into broader hereditary, carrier, and newborn screening NGS panels. Integrating hemoglobin variant detection with multi-disease genetic panels enhances clinical value, improves diagnostic efficiency, and supports higher average selling prices for laboratories. This approach enables clinicians to identify carriers, confirm complex genotypes, and assess coexisting inherited conditions within a single workflow. As sequencing costs decline and reimbursement pathways gradually improve, bundled NGS offerings are gaining traction across reference laboratories and tertiary hospitals, driving higher test volumes and broader market uptake.

Furthermore, expanded adoption of molecular diagnostics, including next-generation sequencing and targeted gene panels, is improving diagnostic yield for complex, atypical, or rare hemoglobin variants that are difficult to resolve using conventional methods alone. These advances are complemented by the development and commercialization of rapid, point-of-care hemoglobin variant assays designed for outpatient clinics, community health centers, and remote settings. Portable and rapid testing solutions reduce turnaround time, expand access in underserved regions, and support decentralized care delivery. Together, molecular innovation and point-of-care deployment are reshaping diagnostic pathways, improving case detection, and creating significant growth opportunities across both developed and emerging markets.

Category-wise Analysis

By Test Type Insights

The hemoglobin electrophoresis segment is projected to dominate the global adult hemoglobinopathy testing market in 2026, accounting for 48.3% of revenue. This dominance is driven by its long-standing role as a frontline diagnostic method for identifying abnormal hemoglobin variants such as HbS, HbC, and HbE. Hemoglobin electrophoresis remains widely adopted across hospitals and diagnostic laboratories due to its cost-effectiveness, ease of interpretation, and strong clinical validation. Its routine use in initial screening, confirmatory diagnosis, and disease monitoring supports sustained demand. Continued integration with automated platforms, compatibility with high-throughput laboratory workflows, and strong endorsement within clinical diagnostic guidelines further drive its leading position globally.

By Indication Insights

The sickle cell disease segment is projected to dominate the global adult hemoglobinopathy testing market in 2026, accounting for 54.7% of revenue. This is attributed to the high prevalence of sickle cell disease among adults, particularly in regions with high newborn survival rates and improved long-term disease management. Adults with sickle cell disease require regular diagnostic testing to confirm disease, differentiate variants, and monitor clinical status. Established screening programs, increased clinician awareness, and the need for lifelong disease surveillance contribute to sustained testing volumes. Expanding access to diagnostic services and growing emphasis on early identification of disease-related complications further support this segment’s strong market position.

By End-user Insights

The hospitals segment is projected to dominate the global adult hemoglobinopathy testing market in 2026, capturing a 44.6% revenue share. Hospitals, particularly tertiary-care centers and academic medical institutions, serve as primary hubs for diagnosing adult hemoglobinopathies due to their ability to manage complex cases, perform confirmatory testing, and support multidisciplinary care. High patient inflow, the availability of specialized hematologists, and access to advanced diagnostic technologies, such as automated electrophoresis and HPLC systems, drive hospital-based demand. Additionally, hospitals play a critical role in referral-based testing, emergency diagnosis, and long-term disease monitoring, reinforcing their dominance within the end-user landscape.

Regional Insights

North America Adult Hemoglobinopathy Testing Market Trends

North America is expected to maintain global dominance in the adult hemoglobinopathy testing market, with a market share of 47.8%, supported by advanced healthcare infrastructure, robust diagnostic coverage, and well-established screening programs. The U.S. leads the region due to high awareness of sickle cell disease, widespread availability of diagnostic laboratories, and strong presence of leading diagnostic manufacturers. Routine testing in hospitals and reference laboratories, combined with continued FDA approvals for advanced diagnostic platforms, supports sustained adoption. Increasing focus on early disease identification, adult disease monitoring, and decentralized diagnostic services continues to drive investment from major healthcare systems.

The region also benefits from favorable reimbursement policies for diagnostic testing, high clinician reliance on confirmatory assays such as electrophoresis and HPLC, and growing adoption of molecular testing in specialized cases. Investments in laboratory automation, digital diagnostic workflows, and population-level screening initiatives further enhance testing efficiency. Rising advocacy efforts and public awareness programs related to hemoglobin disorders continue to strengthen North America’s long-term leadership in the global adult hemoglobinopathy testing market.

Europe Adult Hemoglobinopathy Testing Market Trends

Europe shows steady and mature adoption of adult hemoglobinopathy testing, supported by strong public health policies, centralized laboratory networks, and standardized diagnostic guidelines across key markets such as Germany, the U.K., France, Italy, Switzerland, and the Nordic countries. Robust epidemiological surveillance systems and consistent clinical validation support widespread use of hemoglobin electrophoresis, HPLC, and complementary diagnostic methods. The region shows high integration of automated laboratory systems and standardized testing protocols to improve diagnostic accuracy and reduce turnaround time.

Europe’s favorable regulatory environment, emphasis on quality assurance, and strong contributions from academic research centers support the evaluation and adoption of advanced diagnostic technologies. Growing demand for cost-effective testing solutions, improved laboratory efficiency, and expanded adult screening initiatives continues to drive market growth. Government-supported programs focused on genetic disorder management and early diagnosis further reinforce Europe’s stable market expansion.

Asia Pacific Adult Hemoglobinopathy Testing Market Trends

Asia Pacific is projected to be the fastest-growing region, with a CAGR of 7.5%, driven by rising disease prevalence, expanding healthcare infrastructure, and increased diagnostic awareness. Countries such as China, India, Japan, South Korea, and Southeast Asian nations are witnessing growing adoption of hemoglobinopathy testing across hospitals, diagnostic laboratories, and government healthcare programs. The availability of cost-effective diagnostic platforms and strong participation from regional diagnostic manufacturers are improving accessibility, particularly in mid-sized hospitals and urban diagnostic centers. For instance, in July 2025, the Council of Scientific and Industrial Research (CSIR) announced plans to launch an affordable screening test kit for sickle cell anemia within six months. The PCR-based diagnostic kit, developed by the Centre for Cellular and Molecular Biology (CCMB), a CSIR laboratory, is expected to be priced below INR 100, significantly improving access to low-cost screening in India.

Government-led screening initiatives, investments in laboratory capacity, and collaborations with global diagnostic companies are accelerating market adoption. Increasing emphasis on early diagnosis, improved disease surveillance, and integration of genetic testing in select patient populations is supporting strong growth momentum. Expanding private healthcare networks, rising medical tourism, and the development of specialized hematology centers continue to underpin robust market expansion across the Asia Pacific.

Competitive Landscape

The global adult hemoglobinopathy testing market is moderately to highly competitive, with key participants including Bio-Rad Laboratories, Inc., Revvity, Siemens Healthineers, Thermo Fisher Scientific Inc., and Trinity Biotech. These companies leverage broad diagnostic portfolios, established laboratory instrumentation, and strong global distribution networks to strengthen their presence across hospitals, reference laboratories, and specialty diagnostic centers. Rising prevalence of sickle cell disease and thalassemia among adult populations continues to drive demand for routine screening and confirmatory testing.

Manufacturers are focusing on advancing HPLC systems, automated electrophoresis platforms, and molecular diagnostic solutions, while emphasizing regulatory approvals, assay standardization, and strategic collaborations with public health programs and laboratory networks to expand access to testing and accelerate market growth.

Key Industry Developments:

- In June 2025, the Government of India announced the launch of affordable sickle cell anemia test kits for nationwide screening, aiming to expand early detection and improve access to hemoglobinopathy testing across high-burden and underserved populations.

- In October 2023, Sanguina received U.S. Food and Drug Administration (FDA) clearance for its AnemoCheck Home hemoglobin test kit, enabling at-home monitoring of hemoglobin levels for individuals with anemia related to nutritional deficiencies, thalassemia, and sickle cell disease.

Companies Covered in Adult Hemoglobinopathy Testing Market

- Bio-Rad Laboratories, Inc.

- Revvity

- Siemens Healthineers

- Thermo Fisher Scientific Inc.

- Trinity Biotech

- BIOMEDOMICS INC.

- Cepheid

- F. Hoffmann-La Roche Ltd

- Quest Diagnostics Incorporated.

- ARUP Laboratories.

- Danaher Corporation

- Sysmex Corporation

- QuidelOrtho Corporation.

- Randox Health London Ltd

- Others

Frequently Asked Questions

The global adult hemoglobinopathy testing market is projected to be valued at US$ 2.1 Bn in 2026.

Rising prevalence of sickle cell disease and thalassemia among adults, expanded newborn survivors transitioning to adult care, wider access to diagnostic laboratories, and increasing physician awareness drive demand for adult hemoglobinopathy testing market.

The global adult hemoglobinopathy testing market is poised to witness a CAGR of 5.5% between 2026 and 2033.

Growth in molecular and genetic testing, expansion of routine carrier screening programs in emerging markets, and integration of advanced diagnostics into hospital and reference laboratory workflows create key market opportunities.

Bio-Rad Laboratories, Inc., Revvity, Siemens Healthineers, Thermo Fisher Scientific Inc., and Trinity Biotechare some of the key players in the adult hemoglobinopathy testing market.