- Automotive Components & Materials

- CRATE Engines Market

CRATE Engines Market Size, Share, and Growth Forecast, 2025 - 2032

CRATE Engines Market By Engine Type (New Engines, Rebuilt Engines, Remanufactured Engines, Used Engines), Capacity (600-1000cc, 1000-3000 cc, 3000-5000cc), Fuel Type (Gasoline, Diesel), Regional Analysis 2025 - 2032

CRATE Engines Market Share and Trends Analysis

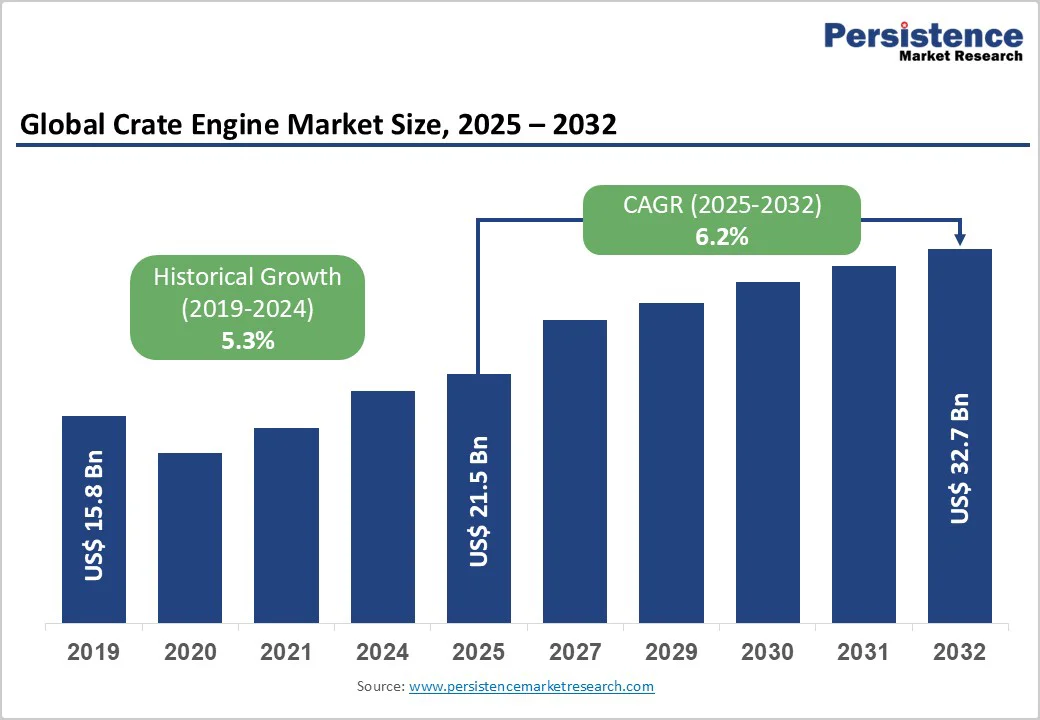

The global CRATE engines market size is likely to value at US$ 21.5 billion in 2025 and is projected to reach US$ 32.7 billion, growing at a CAGR of 6.2% between 2025 and 2032. This robust expansion reflects the increasing demand for cost-effective, high-performance engine replacement solutions across automotive restoration, motorsports, and industrial applications. The market's growth trajectory is primarily driven by the rising popularity of classic car restoration, surging motorsports participation, and the expanding global vehicle fleet requiring engine replacements as vehicles age beyond traditional service lifespans.

Key Industry Highlights:

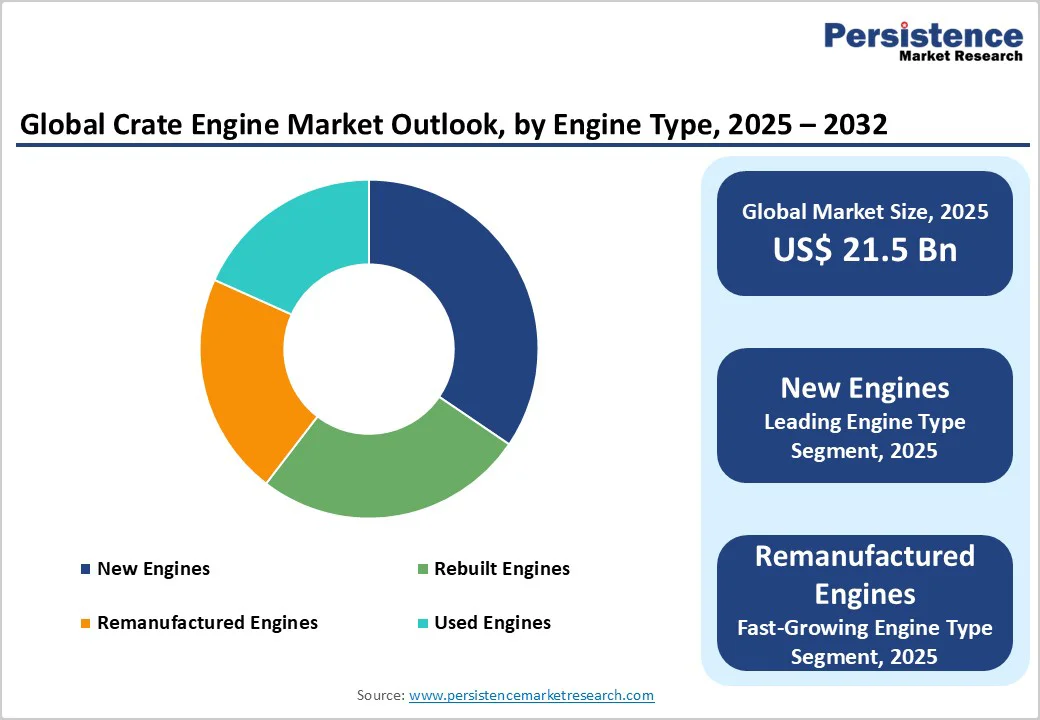

- Leading Engine Type: New Engines dominate with 34% market share, while Remanufactured Engines emerge as the fastest-growing segment at 7.3% CAGR, driven by cost advantages and sustainability benefits.

- Capacity Segmentation: The 1000-3000 CC category holds 39% market share as the leading segment, while 3000-5000 CC registers fastest growth at 6.9% CAGR, propelled by commercial vehicle and construction equipment demand.

- Fuel Type Dominance: Gasoline engines command 73% market share, supported by widespread passenger vehicle applications, while Diesel engines grow fastest at 5.7% CAGR driven by superior fuel efficiency and commercial sector adoption.

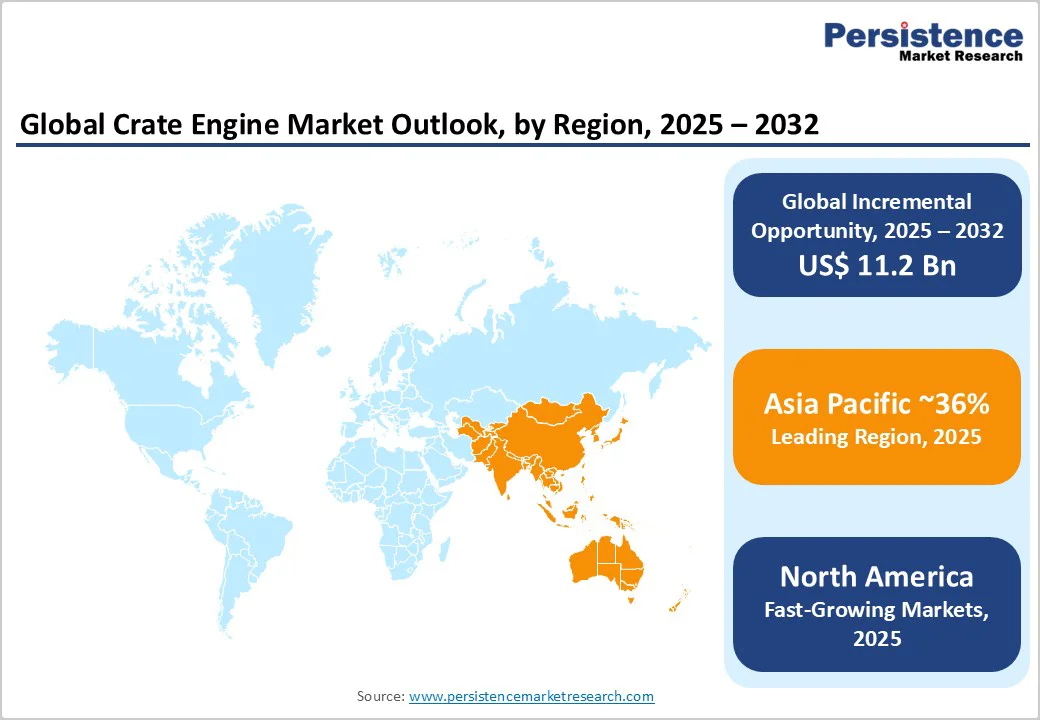

- Regional Leadership: Asia Pacific dominates with 37% global share and fastest trajectory. Europe maintains 26% share with stringent quality standards. In comparison, North America exhibits a prominent 5.9% CAGR supported by strong restoration culture.

- Vehicle Age Dynamics: U.S. average vehicle age reached 12.8 years in 2025 with over 110 million vehicles in prime aftermarket service range (6-14 years), creating sustained replacement engine demand as scrappage rates hold at 4.5%.

- Motorsports Catalyst: Global motorsports market expanded to US$ 9.5 billion in 2024 with projected 8.1% CAGR through 2034, while Formula 1 attendance surged 36% and revenues increased 20%, driving high-performance crate engine demand.

| Key Insights | Details |

|---|---|

|

Crate Engines Market Size (2025E) |

US$ 21.5 Billion |

|

Market Value Forecast (2032F) |

US$ 32.7 Billion |

|

Projected Growth CAGR (2025-2032) |

6.2% |

|

Historical Market Growth (2019-2024) |

5.3% |

Market Dynamics

Drivers - Increasing Average Vehicle Age and Growing Replacement Demand

The escalating average age of vehicles globally represents a fundamental driver propelling CRATE engines market expansion. In the United States, the average vehicle age reached 12.8 years in 2025, marking the second consecutive year of two-month increases. This aging fleet creates substantial opportunities for engine replacement services, particularly as vehicles between 6 to 14 years represent the prime aftermarket service range, currently encompassing over 110 million vehicles or approximately 38% of the U.S. fleet. Similarly, Europe's vehicle fleet averages 12.3 years for passenger cars, with countries like Greece and Estonia maintaining fleets around 17 years old, substantially elevating engine replacement requirements.

The Bureau of Transportation Statistics projects passenger car average age will reach 14.5 years by 2029, while light trucks will average 12.4 years, creating sustained demand for replacement engines as more vehicles require major powertrain overhauls rather than complete vehicle replacement. This demographic shift is amplified by scrappage rates holding steady at 4.5-4.6%, indicating that older vehicles remain operational longer, directly increasing the addressable market for CRATE engine solutions.

Surging Motorsports Participation and Performance Enhancement Culture

The explosive growth in motorsports racing activities worldwide constitutes a critical market catalyst. Formula 1 spectator attendance surged around 5.7 million in 2023, representing a 36% increase over 2019 levels, while F1 revenues climbed 20% from 2021 to 2022, according to Motorsport Network. This burgeoning motorsports ecosystem drives substantial demand for high-performance crate engines that deliver enhanced horsepower, improved torque, and racing-level reliability. The motorsport transmission market itself is forecasted at around 9.6% CAGR, reflecting the broader performance components demand trajectory. Additionally, the thriving car tuning and customization culture, particularly across North America, Europe, and the Asia Pacific, propels demand for crate engines offering adaptability to unique specifications and performance requirements. According to the Specialty Equipment Market Association (SEMA), 79% of vehicle owners express interest in personalizing their vehicles, creating robust demand for high-performance crate engines that facilitate cost-effective modifications.

Restraints - Stringent Emission Regulations and Compliance Complexities

Increasingly rigorous emission standards globally present significant operational challenges for CRATE engine manufacturers and distributors. The European Union's Euro 7 regulations, effective from mid-2025, impose substantially stricter limits on nitrogen oxides (NOx) and particulate matter emissions, targeting 56% and 39% reductions, respectively by 2035 compared to Euro 6 standards. These regulations extend beyond exhaust emissions to encompass brake systems and tire particles, while introducing extended lifetime requirements with durability multipliers of 1.2 for gaseous emissions during additional lifetime periods.

Similarly, the U.S. Environmental Protection Agency's Clean Trucks Plan implements tightened standards for NOx and greenhouse gases from heavy-duty trucks, while California's Advanced Clean Trucks and Advanced Clean Fleets regulations mandate specific percentages of zero-emission vehicle purchases starting in 2025. India's transition to CEV Stage V emission norms effective January 2025 represents a leap from Stage III to Stage V for equipment powered by engines below 37kW, requiring diesel particulate filters and sophisticated aftertreatment systems.

Supply Chain Disruptions and Component Availability Constraints

Persistent supply chain challenges continue to restrain market growth potential. The automotive remanufacturing sector faces ongoing difficulties sourcing critical components including semiconductors, specialized alloys, and precision-machined parts essential for engine assembly. Lead times for geared motors and precision components have extended significantly due to chip shortages and labor scarcities impacting manufacturing operations globally.

The U.S. Department of Transportation reports around 5,300 required permits for restoration activities, highlighting regulatory complexities that compound supply constraints. Additionally, the limited availability of rare or discontinued parts for vintage engines creates bottlenecks in restoration projects, with the National Highway Traffic Safety Administration noting that high costs for rare parts and skilled labor deter many potential buyers from engine upgrades. Tariff fluctuations between the U.S. and trading partners directly affect costs for complete engine assemblies, turbochargers, and fuel injection systems imported from Mexico and Germany, increasing expenses for performance upgrades and replacement engines. These supply chain vulnerabilities necessitate diversified sourcing strategies and inventory buffers, elevating operational costs and potentially constraining market expansion velocity.

Opportunities - Electrification and Hybrid Crate Engine Development

The transition toward electrification presents transformative opportunities for CRATE engine manufacturers. Electric crate engines are gaining traction as environmental regulations tighten and electric vehicle adoption accelerates, with projections indicating electric vehicles will account for 15-18% of global car sales by 2025. The electric vehicle market's rapid expansion creates demand for electric crate engine conversion kits enabling enthusiasts to retrofit classic vehicles with zero-emission powertrains while preserving vintage aesthetics. Hybrid crate engine systems combining internal combustion with electric motors represent another growth frontier, offering enhanced fuel economy and reduced emissions while maintaining performance characteristics valued by motorsports participants and commercial fleet operators. Manufacturers investing in fuel-agnostic engine platforms capable of operating on traditional diesel, natural gas, hydrogen, and renewable fuels position themselves advantageously for future regulatory environments while expanding addressable markets across multiple fuel infrastructure scenarios.

Advanced Remanufacturing Technologies and Sustainability Positioning

Technological innovations in remanufacturing processes unlock substantial value creation opportunities. Advanced restoration techniques, including brush electroplating, arc spraying, and laser cladding, enable the restoration of severely damaged components, reducing environmental impacts by lowering raw material demands and manufacturing processes for replacement parts. Life cycle assessments demonstrate that remanufactured engines utilizing advanced restoration technologies achieve significant ecological benefits, reducing CO2 emissions by approximately 253kg compared to new engine manufacturing.

Economic advantages are equally compelling, with remanufactured engines costing 30-50% less than new counterparts while meeting or exceeding OEM performance specifications. The automotive parts remanufacturing market is projected to reach US$107.6 billion by 2032 at a 6.4% CAGR, reflecting the accelerating adoption of circular economy principles and sustainability mandates.

Manufacturers emphasizing certified remanufacturing processes with comprehensive quality assurance, backed by warranties comparable to new engines, can differentiate offerings and capture environmentally-conscious customer segments. Integration of AI-driven core inspections, predictive analytics for component lifecycle management, and digital twins for process optimization further enhances remanufacturing efficiency and quality consistency, creating competitive advantages in increasingly sophisticated markets.

Category-wise Analysis

Engine Type Analysis

New engines dominate the CRATE engines market, commanding 34% market share as the leading segment. This dominance reflects consumer preference for factory-fresh powertrains with full manufacturer warranties, latest technological enhancements, and guaranteed OEM specifications. New engines appeal particularly to premium automotive restoration projects, competitive motorsports applications requiring maximum reliability, and commercial fleet operators prioritizing long-term performance assurance. Major OEMs, including General Motors' Chevrolet Performance division, Ford Motor Company, and Stellantis' Mopar brand, leverage extensive dealer networks and brand equity to maintain strong positioning in this premium segment.

Remanufactured engines emerge as the fastest-growing segment, registering 7.3% CAGR through the forecast period. This accelerated growth stems from compelling cost advantages, environmental sustainability benefits, and technological improvements elevating remanufactured engine quality to match or exceed new engine standards. The remanufactured engine market benefits from stringent emission regulations, compelling cost-effective compliance solutions, and increasing awareness of circular economy principles. Remanufacturing processes incorporating advanced restoration technologies enable recovery of approximately 62% by quantity, 80.1% by weight, and 77.8% by value of engine components, delivering significant resource conservation and cost efficiencies.

Capacity Analysis

1000-3000 CC segment holds the dominant market position with 39% market share, reflecting its broad applicability across passenger cars, light commercial vehicles, compact SUVs, and performance motorcycles. This displacement range balances power output, fuel efficiency, and installation versatility, making it the preferred choice for mainstream automotive applications. The segment benefits from extensive OEM support, with manufacturers including Honda, Toyota, Ford, and General Motors offering comprehensive crate engine portfolios within this capacity bracket.

3000-5000 CC segment registers the fastest growth at 6.9% CAGR, driven by robust demand from commercial vehicle operators, construction equipment applications, and performance truck enthusiasts. This displacement category delivers superior torque characteristics essential for heavy-duty towing, hauling, and industrial operations. The diesel engine market within this range is projected to grow significantly, reflecting strong commercial vehicle adoption and infrastructure development requirements. Heavy-duty applications, including excavators, wheel loaders, and commercial trucks increasingly specify engines within this displacement range for optimal power-to-weight ratios and operational durability.

Fuel Type Analysis

Gasoline engines maintain market leadership with 73% share, driven by their widespread adoption in passenger vehicles, light-duty trucks, and recreational applications. Gasoline engines offer advantages, including lower initial purchase costs, quieter operation, reduced maintenance requirements, and established fueling infrastructure availability. The global gasoline engine market growth supported by hybrid technology integration and continued dominance in cost-sensitive markets. Performance enthusiasts favor gasoline crate engines for their high-RPM capabilities, responsive throttle characteristics, and extensive aftermarket support ecosystems.

Diesel engines represent the fastest-growing fuel type segment at a positive CAGR, propelled by superior fuel efficiency, enhanced torque output, and extended engine longevity advantages. Diesel engines deliver approximately 20% greater thermal efficiency compared to gasoline counterparts, translating directly to fuel economy improvements and lower operating costs over vehicle lifespans. Diesel's high torque generation at lower RPMs makes these engines ideal for heavy-duty applications including commercial transportation, construction machinery, and industrial power generation, where reliability and power output under sustained load conditions prove critical.

Regional Insights

North America CRATE Engine Market Trends

North America commands significant market presence with prominent 5.9% CAGR through 2032, establishing the region as a critical growth driver. The United States dominates regional dynamics, accounting for approximately 79.3% of North American market share in 2024. This leadership position stems from deeply embedded automotive culture, particularly surrounding muscle cars, classic vehicle restoration, and motorsports participation. The region benefits from robust infrastructure including 1,640 licensed restoration workshops and extensive dealer networks supporting both OEM and aftermarket crate engine distribution. General Motors and Ford Motor Company maintain strong market positions through their Chevrolet Performance and Ford Racing divisions respectively, offering factory-engineered crate engines with comprehensive warranties that appeal to performance enthusiasts and restoration professionals.

The regulatory environment significantly influences market dynamics, with EPA Phase 3 Greenhouse Gas standards and various state-level emissions requirements driving technological advancement. California's Advanced Clean Trucks regulations mandate increasing zero-emission vehicle percentages, creating opportunities for electric crate engine development. Investment trends reflect strong private and corporate funding for classic car events, with over 890,000 classic cars currently undergoing or awaiting restoration, generating substantial parts and engine demand. The competitive landscape features established players including Blueprint Engines, ATK High Performance Engines, JEGS High Performance, and Pace Performance alongside OEM offerings, fostering innovation and competitive pricing dynamics.

Europe CRATE Engines Market Trends

Europe holds substantial 26% global market share, characterized by stringent regulatory frameworks, rich automotive heritage, and sophisticated consumer preferences. Germany, the United Kingdom, France, and Spain drive regional performance, with Germany alone generating USD 1.1 billion in motorsports-related revenue in 2024. The European Union's average vehicle fleet age of 12.3 years, with countries like Greece maintaining 17-year-old fleets, creates substantial replacement engine demand. Europe's leadership in automotive engineering excellence, exemplified by manufacturers including BMW, Mercedes-Benz, and Volkswagen Group, establishes high quality standards influencing global market expectations.

Euro 7 emission standards implementation beginning mid-2025 represents the most significant regulatory development, imposing 56% NOx and 39% particulate matter reduction requirements compared to Euro 6 standards. These regulations drive substantial R&D investments in clean engine technologies, particulate filters, and advanced aftertreatment systems. The regulatory harmonization across EU member states facilitates market standardization while creating compliance complexities for smaller manufacturers. Investment trends emphasize sustainability and circular economy principles, with remanufacturing activities receiving policy support as resource-efficient alternatives to new production. The competitive landscape features both established OEMs and specialized remanufacturers including Perkins Engines (Caterpillar subsidiary), with distribution networks spanning automotive dealerships, independent workshops, and online retail channels.

Asia Pacific CRATE Engines Market Trends

Asia Pacific emerges as the dominant region, commanding 37% global market share and representing the fastest-growing geography with projected 7.3% CAGR through 2032. China leads regional dynamics with 59.4% market share within Asia-Pacific, followed by significant contributions from Japan, India, and ASEAN nations. The region's explosive growth stems from rapid industrialization, expanding middle-class populations with rising disposable incomes, and surging vehicle production rates. China's motor vehicle production reached 26.0 million units in 2021, while India's production expanded from 3.3 million units in 2020 to 4.3 million units in 2021, according to OICA statistics.

Manufacturing advantages including lower labor costs, established supply chain ecosystems, and government initiatives such as India's Make In India program attract substantial investment in engine production and remanufacturing capabilities. ASEAN growth dynamics reflect increasing vehicle ownership rates, expanding automotive aftermarket services, and growing motorsports interest, particularly in Thailand, Malaysia, and Indonesia markets. Regulatory environments vary significantly across the region, with India implementing CEV Stage V emission norms effective January 2025, while China enforces China VI-b standards targeting stricter NOx and particulate matter limits. Investment trends emphasize capacity expansion for both new engine manufacturing and remanufacturing facilities, supported by government incentives promoting industrial development and employment generation.

Competitive Landscape

The global CRATE engines market exhibits a moderately consolidated structure with established OEMs controlling approximately 45-50% combined market share, while specialized independent manufacturers and remanufacturers account for the remaining share. Leading players with estimated market positions include General Motors, Ford Motor Company, and Stellantis. The market demonstrates moderate barriers to entry given capital requirements for manufacturing infrastructure, quality certification standards, and distribution network establishment, favoring established players with brand recognition and dealer relationships. However, opportunities exist for niche specialists focusing on specific displacement ranges, fuel types, or application segments including motorsports, marine, or industrial power generation.

Strategic Developments:

- New Product Launch - Chevrolet Performance Hellephant Series (May 2025): Stellantis' Direct Connection division introduced the advanced supercharged Hellephant series of crate engines, targeting high-performance enthusiast markets. This launch demonstrates strategic focus on premium performance segments, offering factory-engineered solutions with comprehensive warranties that compete directly with custom engine builds.

- Manufacturing Investment - Stellantis Kokomo Facility Expansion (January 2025): Stellantis announced investments exceeding $100 million in Kokomo, Indiana facilities to produce the all-new GMET4 EVO four-cylinder engine beginning in 2026, adding more than 100 jobs. This strategic investment emphasizes commitment to U.S. powertrain manufacturing and positions the company to meet evolving fuel efficiency and emission requirements.

- Distribution Network Enhancement - Mopar Parts Distribution Center Georgia (August 2025): Stellantis invested more than $41 million establishing a 422,000-square-foot Mopar Parts Distribution Center in Forsyth, Georgia, featuring advanced AutoStore automated storage and retrieval systems. This facility strengthens southeastern U.S. distribution capabilities, reducing order wait times and improving inventory turnover efficiency.

Companies Covered in CRATE Engines Market

- General Motors (Chevrolet Performance)

- Ford Motor Company

- Stellantis (Mopar)

- Cummins Inc.

- Caterpillar Inc.

- Blueprint Engines

- JASPER Engines & Transmissions

- ATK High Performance Engines

- Honda Performance Development

- Toyota Motor Corporation

- Nissan Motor Corporation

- BMW Group

- Volkswagen Group

- Perkins Engines (Caterpillar)

- Edelbrock LLC

Frequently Asked Questions

The global CRATE Engines Market reached US$ 21.5 billion in 2025, driven by strong demand across automotive restoration, motorsports, and commercial vehicle applications worldwide.

The CRATE engines market is propelled by increasing global vehicle fleet age in developed markets, surging motorsports participation and attendance growth, classic car restoration boom in the U.S. alone, and cost-effective remanufactured engines offering 30-50% savings versus new alternatives.

The CRATE engines market is anticipated to expand at a compound annual growth rate (CAGR) of 6.2% between the forecast period.

Significant opportunities include electric and hybrid crate engine development targeting prominent EV adoption by 2025, Asia-Pacific expansion with China commanding regional share of ~60%, advanced remanufacturing technologies reducing CO2 emissions by 253kg, and classic car market growth.

Leading manufacturers include General Motors (Chevrolet Performance), Ford Motor Company, Stellantis (Mopar), Cummins Inc., Caterpillar Inc., Blueprint Engines, JASPER Engines & Transmissions and other players.