- Medical Devices

- Arthroscopic Shaver Market

Arthroscopic Shaver Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Arthroscopic Shaver Market by Product Type (Control System, Shaver Handpieces, Accessories), by Application (Knee Repair, Shoulder Repair, Hip Repair, Others), by End User, and Regional Analysis from 2026 to 2033

Arthroscopic Shaver Market Share and Trends Analysis

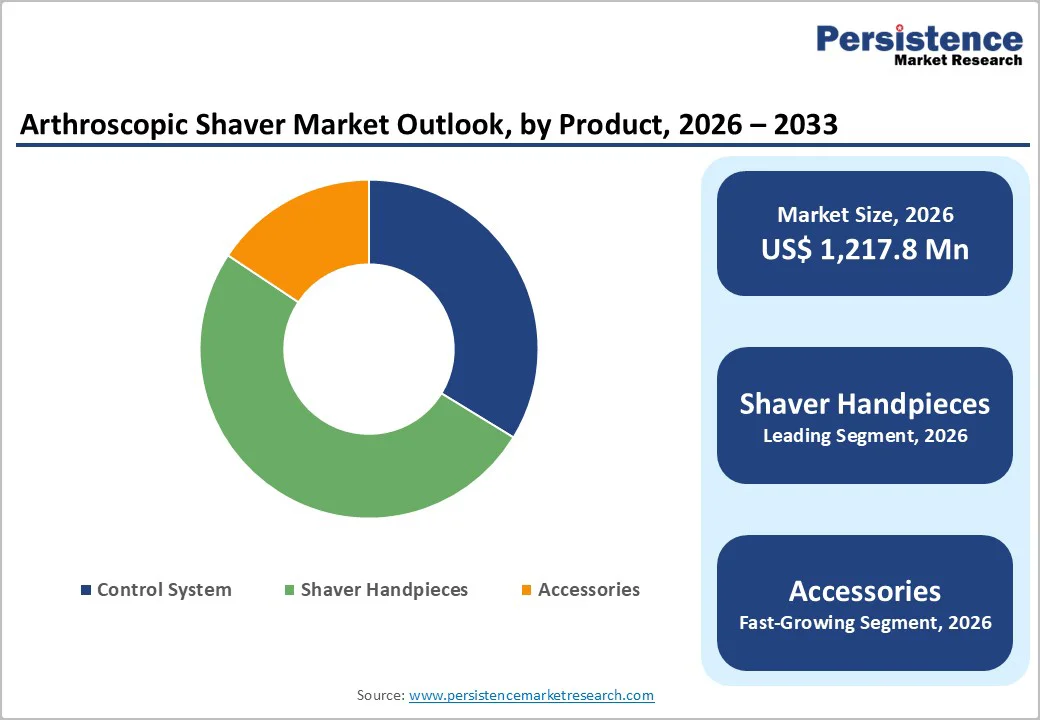

The global arthroscopic shaver market size is likely to grow from US$1,217.8 million in 2026 to US$1,856.3 million by 2033. The market is projected to record a CAGR of 6.2% during the forecast period from 2026 to 2033. The growing preference for minimally invasive joint surgeries and the rise in prevalence of musculoskeletal disorders have triggered the need for arthroscopic shavers.

Hospitals dominate usage, while ambulatory surgical centers are rapidly adopting these devices due to efficiency and infection control benefits. Knee arthroscopy remains the most common application, followed by procedures on the shoulder and hip.

Technological innovations, such as improved shaver systems, disposable blades, and advanced suction mechanisms, are enhancing surgical precision and reducing recovery time. Growing awareness, aging population, and expanding healthcare infrastructure in the Asia Pacific are creating new growth opportunities.

Key Industry Highlights:

- The arthroscopic shaver market is growing steadily due to increasing preference for minimally invasive orthopedic surgeries.

- Knee arthroscopy is the largest application segment, driven by the high prevalence of knee osteoarthritis and ligament injuries. Shoulder, hip, and foot & ankle arthroscopies are also significant contributors.

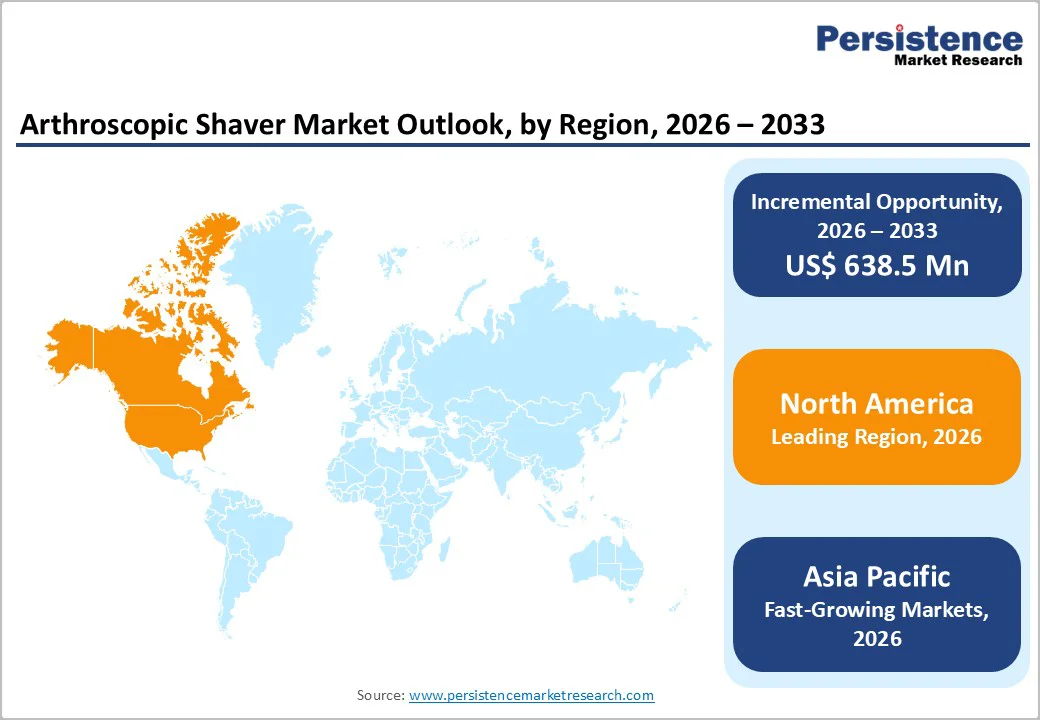

- North America leads the market, supported by advanced healthcare infrastructure and high awareness. Europe follows closely, while Asia Pacific is the fastest-growing region due to rising healthcare investment, increasing orthopedic surgeries, and growing awareness of minimally invasive treatments in countries such as India, China, and Japan.

- Hospitals account for the largest share due to high procedure volumes and advanced infrastructure. Ambulatory Surgical Centers (ASCs) are the fastest-growing end-users, owing to cost-efficiency, shorter hospital stays, and increasing preference for outpatient minimally invasive surgeries.

| Key Insights | Details |

|---|---|

| Arthroscopic Shaver Market Size (2026E) | US$1,217.8 Mn |

| Market Value Forecast (2033F) | US$1,856.3 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.2% |

| Historical Market Growth (CAGR 2020 to 2024) | 5.9% |

Market Dynamics

Driver - Increasing Adoption of Disposable Shaver Blades

The increasing adoption of disposable shaver blades is becoming a major growth driver in the Arthroscopic Shaver Market, as healthcare facilities shift toward cost-efficient and infection-controlled surgical workflows. Disposable blades eliminate the need for complex sterilization cycles, reducing downtime and operational burden on CSSD teams.

Their consistent sharpness, single-use safety, and compatibility with modern shaver systems enhance surgical precision while minimizing cross-contamination risks. Ambulatory Surgical Centers, which prioritize rapid turnover, particularly benefit from disposables due to predictable performance and reduced maintenance requirements.

This shift aligns with global trends favoring hygienic, ready-to-use instruments that support high procedure volumes and better patient outcomes.

Restraints - Slow Adoption in Rural and Tier-2 Healthcare Settings

Slow adoption in rural and tier-2 healthcare settings remains a significant restraint for the Arthroscopic Shaver Market. Many smaller hospitals lack the advanced surgical infrastructure required to support minimally invasive arthroscopic procedures, including high-quality imaging systems, sterile processing units, and trained surgical staff.

Budget limitations further restrict their ability to invest in costly shaver consoles, disposable blades, and maintenance services. Additionally, orthopedic surgeons in these regions often rely on traditional open surgeries due to limited hands-on training in arthroscopy and insufficient exposure to modern surgical technologies.

The absence of dedicated arthroscopy centers, inconsistent power supply, and supply-chain challenges for spare parts and consumables further hinder adoption, slowing market expansion outside metropolitan clusters.

Opportunity - Customizable Blades & Modular Systems

Customizable blades and modular arthroscopic shaver systems present a strong market opportunity as surgeons increasingly demand tools tailored to specific joint procedures. Different blade geometries-such as fluted, serrated, hooked, or aggressive cutting profiles-allow precise tissue removal based on anatomy and pathology.

Modular consoles with adjustable speed, torque, and suction settings enable surgeons to fine-tune performance during complex arthroscopies. This flexibility enhances surgical precision, reduces operative time, and improves patient outcomes.

Additionally, modular platforms lower long-term costs for hospitals by allowing upgrades or component replacements without purchasing an entirely new system, making them highly attractive for both high-volume centers and emerging markets.

Category-wise Analysis

By Application Insights

Knee repair accounts for the highest share because knee injuries are the most frequent among all joint-related conditions, driven by sports activities, age-related degeneration, and lifestyle changes. Procedures such as meniscectomy, ACL reconstruction, cartilage debridement, and synovectomy are performed in very high volumes globally.

Knee arthroscopy is also preferred due to its quick recovery time and strong clinical success rates. As a result, hospitals and ASCs consistently use arthroscopic shavers for routine knee procedures, creating sustained, high-volume demand. The combination of a large patient population, increasing incidence of knee disorders, and high procedural frequency makes knee repair the dominant application segment.

By End User Insights

Hospitals account for the highest share because they handle the largest volume of arthroscopic surgeries and have the advanced infrastructure required for complex orthopedic procedures. They invest in full arthroscopy towers, high-end shaver systems, and a wider range of disposable blades, driving higher equipment consumption.

Hospitals also treat trauma, sports injuries, and emergency joint conditions that cannot be managed in smaller centers. Their ability to offer multidisciplinary care, post-operative rehabilitation, and round-the-clock surgical services makes them the primary destination for arthroscopic procedures. As a result, hospitals consistently generate the highest demand for arthroscopic shaver systems and accessories.

Regional Insights

North America Arthroscopic Shaver Trends

North America leads the Arthroscopic Shaver Market due to its advanced orthopedic infrastructure, high adoption of minimally invasive surgeries, and strong presence of specialized sports medicine centers. The region benefits from well-established reimbursement systems and rapid uptake of technologically advanced shaver systems and disposable blades.

The U.S. drives the majority of the regional demand, supported by high rates of ACL injuries, meniscal tears, and arthroscopic outpatient procedures performed in hospitals and ASCs. Strong R&D activity, surgeon training programs, and continuous product innovation from domestic manufacturers further strengthen North America’s dominant position in the global arthroscopic shaver landscape.

Asia Pacific Arthroscopic Shaver Market Trends

Asia Pacific is emerging as a high-growth region in the Arthroscopic Shaver Market due to the rapid expansion of healthcare infrastructure, rising sports injuries, and increasing awareness of minimally invasive orthopedic procedures. Countries such as India, China, and Japan are witnessing higher arthroscopy volumes supported by improving insurance coverage and growing orthopedic specialties.

Demand for cost-effective shaver systems and disposable blades is rising as hospitals and ambulatory centers upgrade equipment. Increasing medical tourism, surgeon training programs, and government investments in advanced surgical technologies are accelerating adoption. The region’s large patient population and unmet orthopedic care needs make the Asia Pacific a key future growth engine.

Competitive Landscape

The Arthroscopic Shaver Market is moderately competitive, with companies focusing on innovation, ergonomic designs, and improved cutting efficiency to strengthen their market presence.

Manufacturers are expanding portfolios with advanced handpieces, variable-speed consoles, and a wide range of disposable blades to meet surgeon-specific needs. Strategic partnerships with hospitals, sports medicine centers, and distributors enhance market reach. Companies are also investing in R&D to integrate smarter control systems, better suction mechanisms, and modular platforms.

Key Industry Developments:

- In December 2022, Marshall University launched the clinical trial evaluating a new meniscus repair technology. The study compared nanoscopic arthroscopy with standard arthroscopy for treating meniscus tears, aiming to assess differences in visualization, precision, and patient recovery outcomes.

Companies Covered in Arthroscopic Shaver Market

- Arthrex Inc

- Stryker Corporation

- CONMED Corporation

- Smith & Nephew Plc.

- Zimmer Biomet Holdings, Inc.

- Medtronic Plc.

- Johnson & Johnson

- Richard Wolf GmbH

- De Soutter Medical Limited

- Karl Storz GmbH & Co. Kg

- Others

Frequently Asked Questions

The global arthroscopic shaver market is projected to be valued at US$1,217.8 Mn in 2026.

Increasing cases of osteoarthritis, meniscal tears, ligament injuries, and degenerative joint conditions elevate the need for arthroscopic procedures.

The global market is poised to witness a CAGR of 6.2% between 2026 and 2033.

Expansion of outpatient arthroscopy drives demand for compact, affordable, and efficient shaver systems.

Arthrex Inc, Stryker Corporation, CONMED Corporation, Smith & Nephew Plc., and others.