- Clothing, Footwear, & Accessories

- Global Wool Yarn Market

Global Wool Yarn Market Size, Share, and Growth Forecast 2026 – 2033

Wool Yarn Market by Yarn Type (Worsted and Woolen), Wool Type (Merino Wool, Peruvian Highland Wool, Teeswater Wool, Shetland Wool, Cashmere Wool, and Others), Application (E Apparel, Upholstery Fabrics, Blankets, Flooring, and Others), and Regional Analysis

Wool Yarn Market Size and Share Analysis

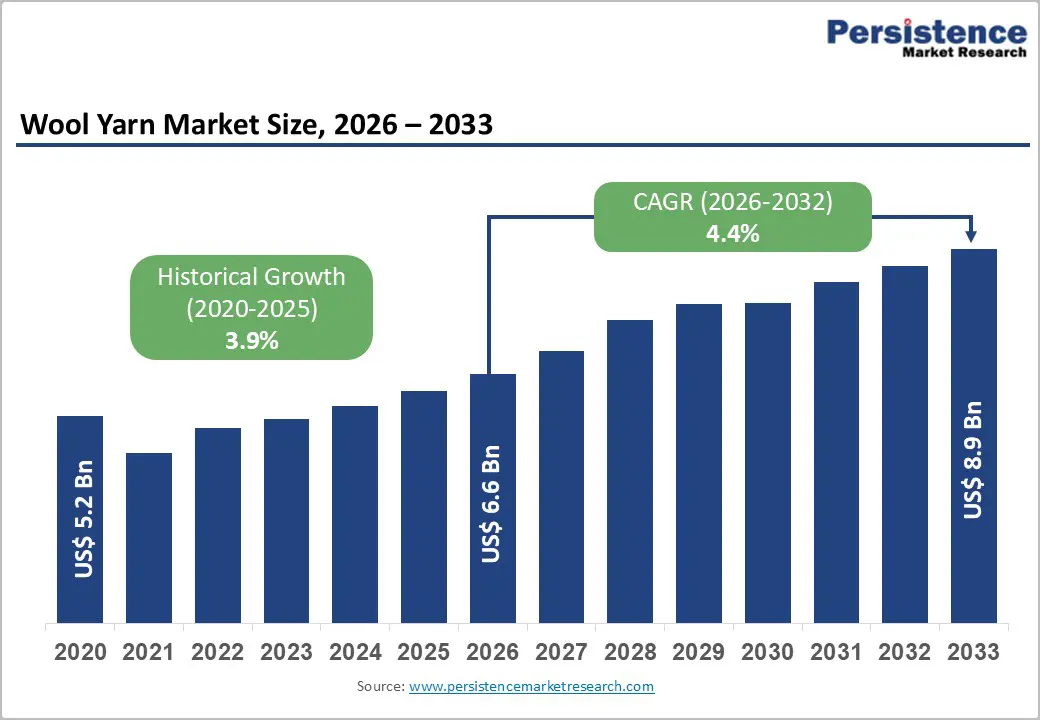

The global Wool Yarn Market size was valued at US$ 6.6 Billion in 2026 and is projected to reach US$ 8.9 Billion by 2033, growing at a CAGR of 4.4% between 2026 and 2033. The market is experiencing steady growth driven by rising consumer demand for sustainable and natural fibers, premiumization trends in the apparel sector, expanding fashion industry investments, and growing adoption of high-quality wool products across diverse applications including luxury garments, sportswear, upholstery, and home furnishing segments.

Key Market Highlights

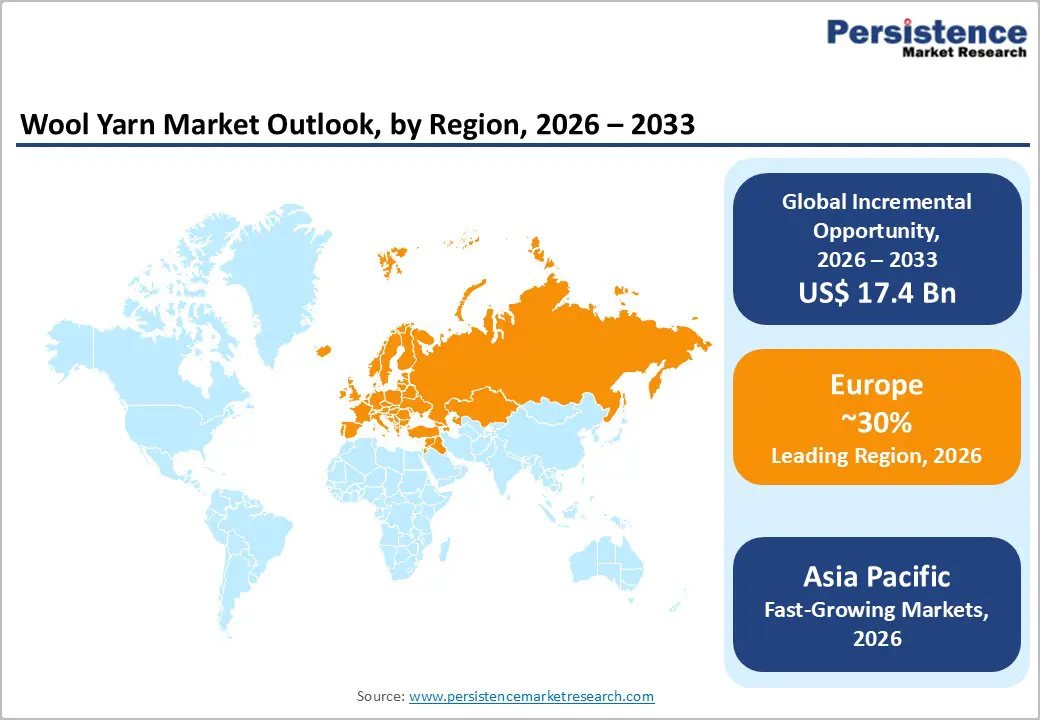

- Leading Country: Europe commands approximately 30% of global Wool Yarn Market revenue, with Germany maintaining regional dominance through advanced textile technology, precision manufacturing, heritage brands, and strong emphasis on sustainable, premium wool yarn applications across diverse segments.

- Fastest Growing Region: Asia-Pacific exhibits fastest market growth at 5.6% CAGR through 2033, propelled by rapid economic development, expanding textile manufacturing capabilities, government wool development initiatives, and emerging consumer demand for premium products in China, India, and ASEAN nations.

- Dominant Yarn Type: Worsted yarn commands approximately 65% of market revenue, driven by premium apparel applications, luxury fashion investments, and superior aesthetic characteristics supporting premium positioning in formal wear, blazers, and professional attire manufacturing globally.

- Growing Wool Type: Specialty wool types including Cashmere and premium heritage varieties expand fastest at 7.8% CAGR, reflecting premiumization trends and consumer willingness to invest in ultra-premium, distinctive natural fiber products commanding exceptional price points.

- Key Market Opportunity: Technical textile and performance sportswear applications represent the highest-potential market opportunity, leveraging wool's superior moisture-wicking, temperature-regulating, and antimicrobial properties supporting emerging consumer demands for high-performance, sustainable athletic and outdoor apparel.

| Key Insights | Details |

|---|---|

| Global Wool Yarn Market Size (2026E) | US$ 6.6 Bn |

| Market Value Forecast (2033F) | US$ 8.9 Bn |

| Projected Growth CAGR (2026-2033) | 4.4% |

| Historical Market Growth (2020-2025) | 3.9% |

Market Dynamics

Market Growth Drivers

Accelerating Sustainability Consciousness and Consumer Preference for Natural, Eco-Friendly Fibers

Global consumer demand for sustainable, biodegradable textile products is driving exceptional growth in wool yarn consumption, with environmental consciousness reshaping purchasing decisions across developed and emerging markets. The International Wool Textile Organization (IWTO) reports that wool production reached approximately 1,949 million kilograms of raw wool globally in 2021, supporting stable supply foundations for downstream yarn manufacturers. Wool's inherent biodegradability, renewable characteristics, and minimal environmental footprint compared to synthetic alternatives are attracting sustainability-focused consumers, with Merino wool consumption reaching 304 KMT in 2024 and tracking consistent growth through 2034.

Regulatory frameworks including European Union sustainability mandates, GDPR compliance requirements, and emerging Asia-Pacific environmental standards are compelling textile manufacturers to incorporate natural fibers like wool supporting premium positioning and consumer confidence. Consumer awareness regarding microplastic shedding from synthetic textiles, combined with rising health consciousness regarding hypoallergenic and breathable natural fibers, is accelerating wool yarn adoption in athleisure, technical sportswear, and wellness-focused apparel segments. The convergence of environmental activism, regulatory pressure, and informed consumer preferences is creating structural demand tailwinds supporting sustained wool yarn market expansion across geographic markets.

Premium Fashion Investments and Luxury Textile Expansion Driving Worsted Yarn Demand Growth

Premium and luxury fashion segments are experiencing exceptional growth in worsted wool yarn adoption, driven by consumer aspirations for high-quality, durable garments that command premium positioning and superior aesthetic characteristics. Suits applications represent approximately 52% of worsted wool yarn demand in 2025, underscoring the critical role of premium formal wear in driving high-quality wool material consumption across global fashion markets.

Fashion brands and textile manufacturers increasingly prioritize incorporating worsted wool yarns to enhance product quality, durability, and aesthetic appeal while satisfying conscious consumer demand for natural fiber content and premium positioning. The growing influence of luxury lifestyle brands, premiumization trends in developed markets, and increasing willingness of affluent consumers to invest in high-quality natural fiber clothing are creating sustained growth opportunities for premium wool yarn suppliers across global markets.

Market Restraints

Price Volatility of Raw Wool Materials and Elevated Production Costs Creating Margin Pressures

Fluctuating raw wool pricing and escalating production costs present substantial challenges constraining profit margins and limiting market expansion, particularly for smaller manufacturers lacking economies of scale. British Wool auction prices averaged 81.9 pence per kilogram in 2023, falling significantly below the £1.20 per kilogram threshold required to cover shearing expenses, directly impacting producer profitability and supply chain stability.

Rising labor costs, energy expenses, equipment investments, and sophisticated technology requirements for wool processing and yarn manufacturing are creating structural cost pressures that smaller manufacturers struggle to absorb while maintaining competitive positioning. Commodity price volatility driven by geopolitical factors, currency fluctuations, and global supply chain disruptions creates unpredictable cost structures complicating pricing strategies and long-term business planning for wool yarn manufacturers.

Supply-Side Constraints and Declining Greasy Wool Output Limiting Production Capacity Expansion

Declining greasy wool production trends, adverse weather conditions, and variability in clean wool yields across major producing regions constrain supply growth and create structural bottlenecks limiting market expansion potential. Global greasy wool production has demonstrated declining trends since 2015, with major producers including New Zealand experiencing 2.4% production declines and China recording 0.4% drops in recent years, compressing global supply foundations. Clean wool yield variability, ranging from 76% in Australia to approximately 40% in China, complicates supply forecasting and cost management across diverse geographic sourcing regions.

Drought conditions causing lighter fleeces, reduced shearing volumes, and labor shortages in wool-producing regions are creating supply instability that constrains manufacturers' ability to fulfill growing demand at consistent quality and pricing levels.

Market Opportunities

Emerging Integration of Wool in Technical Textiles and Performance Sportswear Creating Expanded Market Applications

Next-generation applications of wool yarn in technical textiles, performance sportswear, and athleisure categories represent substantial growth opportunities as manufacturers recognize wool's superior moisture-wicking, temperature-regulating, and antimicrobial properties supporting emerging consumer demands. Advanced wool blends combining natural fibers with synthetic components enable manufacturers to develop innovative products addressing specific performance requirements in outdoor apparel, cycling wear, hiking equipment, and extreme-weather protection garments. Merino wool-based technical textiles are gaining momentum in specialized applications where natural fiber characteristics provide competitive advantages, with manufacturers investing in advanced processing technologies enabling customization and enhanced functionality.

The convergence of active lifestyle trends, growing consumer willingness to invest in performance-oriented apparel, and technological advances enabling innovative wool processing are creating high-potential market segments where wool yarn integration generates premium valuations. Emerging sports and wellness markets, particularly in Asia-Pacific developing economies, are creating substantial opportunities for manufacturers introducing premium wool-based sportswear adapted to regional preferences and climate requirements.

Expansion of Government Support Programs and Integrated Wool Development Initiatives in Emerging Markets

Government-backed wool development initiatives and strategic investments in emerging markets are creating substantial growth opportunities for wool yarn manufacturers and producers targeting developing economies with expanding textile sectors. India's Ministry of Textiles has allocated US$ 1.66 million through the Integrated Wool Development Programme (IWDP) extending through 2026, focusing on quality enhancement, supply chain harmonization, and skill development supporting enhanced competitiveness. India's wool sector supports approximately 1.2 million jobs in the organized sector and delivered exports valued at US$ 1.74 billion in FY24, reflecting substantial industry scale and growth potential in emerging markets. Turkey's wool sector, employing over 8,000 workers across 110 companies focused on wool yarn manufacturing, leverages domestic raw wool imports to produce high-value textiles including carpets and apparel, with export volumes exceeding $700 million annually.

China's government initiatives supporting textile sector modernization, coupled with expanding apparel production and sustainability drives, are creating substantial demand for blended textiles incorporating high-quality wool materials. These structural government support programs, combined with emerging market economic development and expanding middle-class consumer bases, establish favorable conditions for sustained wool yarn market expansion across developing economies throughout the forecast period.

Category-wise Insights

Yarn Type Analysis

Worsted yarn commands approximately 65% of the Wool Yarn Market revenue, driven by widespread adoption in premium apparel, luxury fashion, and professional wear applications where superior aesthetic characteristics and durability justify premium pricing. Worsted yarn, characterized by smooth, strong, and lustrous fibers undergoing comprehensive combing processes, creates parallel fiber alignment essential for producing high-quality fabrics supporting formal wear, luxury garments, and professional attire manufacturing. Suits applications account for approximately 52% of worsted wool yarn demand, underscoring the critical role of premium formal wear in driving high-quality wool material consumption.

Worsted yarn is projected to maintain dominant market share through 2033 with sustained growth supported by premiumization trends, expanding luxury fashion investments, and increasing consumer preference for high-quality natural fiber products. The superior processing characteristics and aesthetic appeal of worsted yarns continue establishing market dominance in premium apparel categories and formal wear segments.

Wool Type Analysis

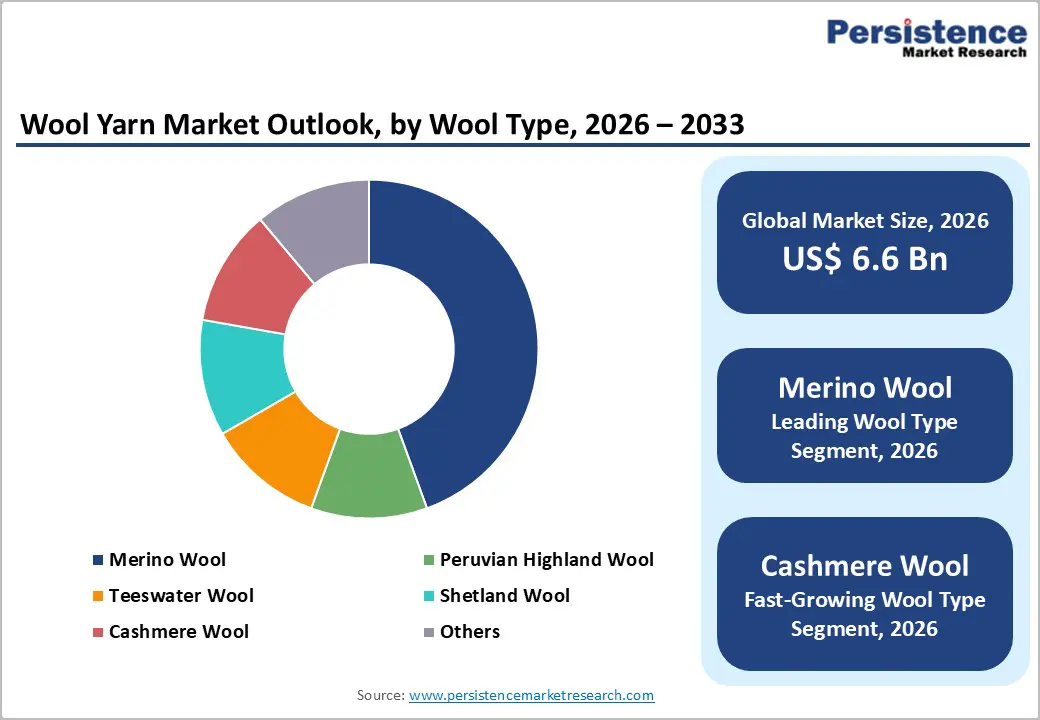

Merino wool commands approximately 47% of the Wool Yarn Market, driven by exceptional softness, breathability, moisture-wicking properties, and premium positioning supporting premium apparel and technical textile applications. Merino wool consumption reached 304 KMT in 2024 and is tracking consistent growth through 2034, reflecting strong industry momentum and expanding applications across fashion and technical textile segments. Merino wool's hypoallergenic characteristics, temperature-regulating properties, and natural antimicrobial features support adoption in performance sportswear, athleisure, outdoor apparel, and wellness-focused clothing categories.

The Merino wool segment is projected to expand at 5.6% CAGR through 2032, outpacing overall market growth and maintaining dominant market share driven by premiumization trends and expanding technical textile applications. Merino's exceptional versatility across diverse application categories, combined with strong brand positioning and consumer recognition, establishes the segment as the clear market leader through the forecast period .

Application Analysis

Apparel applications encompassing sportswear, blazers, jackets, and general clothing segments dominate approximately 48-52% of Wool Yarn Market revenue, driven by fashion industry expansion, luxury brand investments, and consumer preference for natural fiber clothing. Sportswear represents the fastest-growing apparel subsegment at 6.8% CAGR, reflecting consumer demand for performance-oriented, breathable, moisture-wicking garments in athletic and outdoor activities. Blazers and Jacketing applications maintain strong demand at 5.9% CAGR, supported by premium fashion brands' continued reliance on high-quality wool materials for formal wear and professional attire.

Apparel applications are expected to maintain market dominance through 2033, supported by continuing luxury fashion investments, premium brand positioning, and sustainable fashion trends emphasizing high-quality, durable natural fiber clothing. The apparel sector's dominance reflects fundamental consumer preferences for clothing comfort, durability, and environmental sustainability characteristics inherent to wool yarn products.

Regional Insights

North America Wool Yarn Trends

North America commands approximately 26% of global Wool Yarn Market revenue, driven by premium consumer base, strong apparel manufacturing sector, and luxury brand concentration supporting high-value wool yarn consumption. The United States represents the dominant regional market, supported by robust luxury fashion industry, established wool apparel manufacturers, and affluent consumer demographics sustaining premium product demand.

North American manufacturers are increasingly investing in premium wool yarn applications, sustainable production practices, and traceability mechanisms aligned with consumer demands for ethical sourcing and environmental responsibility. The region's regulatory frameworks emphasizing sustainability compliance and consumer preference for natural fiber products continue supporting robust demand for high-quality wool yarn across diverse applications and market segments.

Europe Wool Yarn Trends

Europe represents approximately 30% of global Wool Yarn Market revenue, with Germany maintaining regional leadership commanding approximately 29.6% of European wool yarn market share, supported by advanced textile technology, precision fashion manufacturing, and comprehensive innovation capabilities. The Worsted Wool Yarn Market in Europe is projected to grow from USD 437.2 million in 2025 to USD 678.4 million by 2035, expanding at 4.5% CAGR, reflecting robust demand for premium textiles and luxury apparel throughout the region. Germany's advanced textile technology sector, United Kingdom's heritage fashion brands, France's luxury positioning, and Spain's emerging fashion manufacturing capabilities are collectively driving regional market growth through premium product innovation and sustainable manufacturing practices.

European Union regulatory frameworks including GDPR, EU Green Deal requirements, and mandatory sustainability reporting are compelling manufacturers to adopt traceable, sustainable wool yarn sourcing supporting premium positioning and regulatory compliance. The region's emphasis on responsible production, combined with heritage textile manufacturing expertise and consumer preference for sustainable, premium products, continues establishing Europe as a high-value wool yarn market sustaining growth through the forecast period.

Asia Pacific Wool Yarn Trends

Asia-Pacific represents the fastest-growing regional market, commanding approximately 28% of global Wool Yarn Market revenue with exceptional growth at 5.6% CAGR through 2033, driven by rapid economic development, expanding textile manufacturing capabilities, and emerging consumer demand for premium products. China leads regional production with 367.5 thousand tonnes of wool produced in 2023, with government initiatives supporting textile sector modernization, expanding apparel production, and sustainability drives encouraging blended textile incorporation. India is expanding rapidly at 6.4% CAGR within the Worsted Wool Yarn Market, supported by the Integrated Wool Development Programme allocating US$ 1.66 million through 2026, focusing on quality enhancement, supply chain development, and skill advancement.

Japan contributes at 3.8% CAGR, while ASEAN nations including Vietnam, Thailand, and Indonesia are emerging as growing wool yarn consumption centers reflecting economic development and expanding middle-class consumer bases. Asia-Pacific's exceptional growth reflects the region's manufacturing advantages, rapidly expanding textile sectors, emerging consumer demand for premium products, and government support for industry development driving structural growth opportunities throughout the forecast period.

Competitive Landscape for the Wool Yarn Market

The Wool Yarn Market exhibits highly fragmented competitive structure with numerous small and medium-sized companies operating alongside regional leaders, with no single company commanding dominant global market share. Competition is primarily driven by product quality, brand reputation, sustainability credentials, and specialized wool yarn capabilities supporting diverse applications across premium to value segments. Key market players including The Woolmark Company, Indorama Ventures Public Company Limited, Ortovox, Wool Yarns of New Zealand, American Woolen Company, Sudwolle Group, and emerging specialists are pursuing differentiation strategies emphasizing sustainable practices, traceability mechanisms, and innovation in yarn development.

Companies are increasingly investing in supply chain transparency, implementing third-party assurance schemes, and developing heritage brand positioning supporting premium product positioning. Regional manufacturers like HTX-Shanghai Huaxiang Woolen Co. Ltd. in China, Shandong Hengtai Textile Co. Ltd., and Indian manufacturers including Rosy Woollen Mills Pvt. Ltd. and Sharman Woolen Mills Ltd. are expanding through localized production and regional brand development strategies.

Key Market Developments

- In October 2025, British Wool announced implementation of traceability premiums applied to over 700 tonnes of wool, demonstrating market acceptance of verified sustainable sourcing, enhancing product differentiation, and supporting supply chain transparency throughout the distribution network.

- In September 2024, Indorama Ventures Public Company Limited expanded wool yarn production capacity in India through investment in advanced processing technology and sustainable manufacturing infrastructure, targeting emerging market demand and supporting regional textile development initiatives.

- In June 2024, The Woolmark Company announced advanced traceability initiatives through Woolmark+ roadmap, emphasizing sustainability verification, supply chain transparency, and premium brand positioning supporting consumer confidence in wool product authenticity and ethical sourcing practices.

Companies Covered in Global Wool Yarn Market

- The Woolmark Company

- Indorama Ventures Public Company Limited

- Ortovox

- HTX- Shanghai Huaxiang Woolen Co.,Ltd.

- Wool Yarns of New Zealand

- American Woolen Company

- Sudwolle Group

- John Marshall & Company (Joma)

- Shandong Hengtai Textile Co. Ltd

- Henan First Textile & Apparel (Group) Co. Ltd.

- Shanghai Charmkey Textile Co.,Ltd

- Ferney Spinning Mills Limited

- Rosy Woollen Mills Pvt. Ltd.

- Sharman Woolen Mills Ltd

- KentWool

Frequently Asked Questions

The Global Wool Yarn Market is projected to reach US$ 8.9 Billion by 2033, expanding from US$ 6.6 Billion in 2026 to a CAGR of 4.4%, driven by increasing consumer demand for sustainable natural fibers, premiumization trends in fashion, expanding technical textile applications, and government support for wool development initiatives globally.

The market is primarily driven by accelerating sustainability consciousness and consumer preference for eco-friendly, biodegradable natural fibers; premium fashion investments and luxury brand expansion; expanding technical textile applications in sportswear; growing consumer health awareness regarding hypoallergenic products; and government-backed wool development programs supporting emerging market industry expansion.

Merino wool dominates approximately 42-47% of market revenue, driven by exceptional softness, breathability, and moisture-wicking properties supporting premium apparel, athleisure, and technical textile applications with Merino consumption reaching 304 KMT in 2024 and tracking consistent growth through 2033.

Europe commands approximately 25-30% of global Wool Yarn Market revenue as leading region, with Germany maintaining dominance through advanced textile technology, precision manufacturing, heritage brands, and emphasis on sustainable premium wool yarn applications across diverse market segments.

Technical textile and performance sportswear applications represent the highest-potential market opportunity, leveraging wool's superior moisture-wicking, temperature-regulating, and antimicrobial properties supporting emerging consumer demands for high-performance sustainable athletic apparel and outdoor textiles.

The Woolmark Company leads through advanced traceability and sustainability certification; Indorama Ventures expands through emerging market production capacity and technology investment; American Woolen Company maintains heritage leadership in premium North American manufacturing; regional specialists including Ortovox and Wool Yarns of New Zealand differentiate through sustainable positioning and specialized applications.