- Advanced Materials

- Rockwool Market

Rockwool Market Size, Share, and Growth Forecast 2026 - 2033

Rockwool Market by Product Form (Blanket (Mat) Rock Wool, Board/Rigid Rock Wool, Loose-Fill Rock Wool, Pipe Section Rock Wool, Sprayed Rock Wool), by Application (Building & Construction, Industrial Insulation, HVAC Systems, Fire Protection, Horticulture), by Regional Analysis, 2026 - 2033

Rockwool Market Size and Trend Analysis

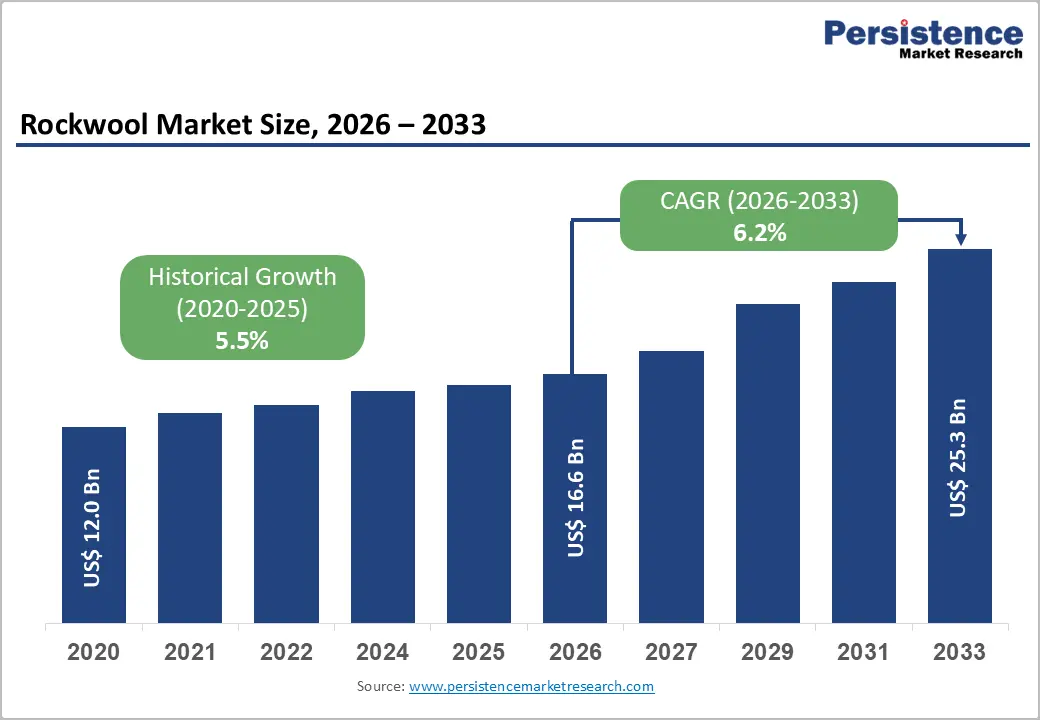

The global rockwool market size is expected to be valued at US$ 16.6 billion in 2026 and projected to reach US$ 25.3 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033. This sustained expansion is driven by tightening global building energy efficiency regulations, rapid urbanization across Asia Pacific and the Middle East, and the growing demand for non-combustible, high-performance insulation materials in both new construction and retrofit applications.

Rockwool's superior fire resistance, maintaining structural integrity at temperatures exceeding 1,000°C, combined with excellent acoustic and thermal insulation properties, is cementing its position as the material of choice under increasingly stringent building codes including the European Energy Performance of Buildings Directive (EPBD) and comparable regulations across North America and Asia.

Key Industry Highlights

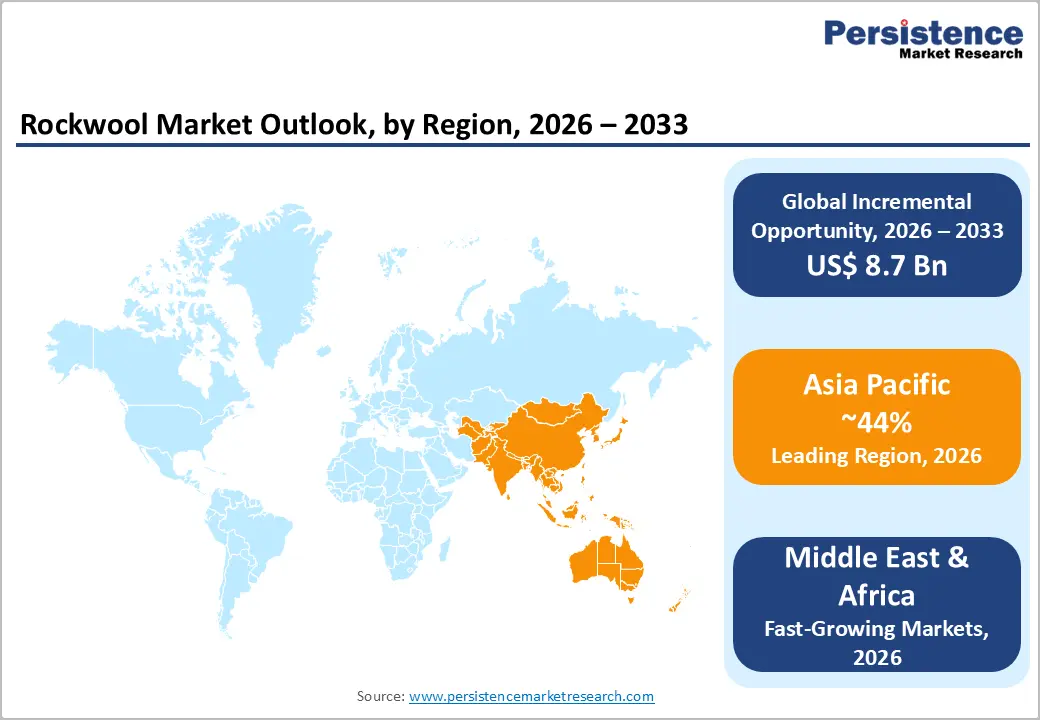

- Leading Region: Asia Pacific dominates the global rockwool market with a 44% revenue share in 2026, led by massive construction activity in China, policy-driven green building adoption, and rapid industrialization across India, South Korea, and ASEAN nations driving sustained high-volume demand.

- Fastest Growing Region: Middle East & Africa is the fastest-growing regional market for rockwool, fueled by large-scale infrastructure and urban development programs including Saudi Vision 2030, rising fire safety code enforcement in commercial construction, and expanding industrial insulation demand in the oil & gas sector.

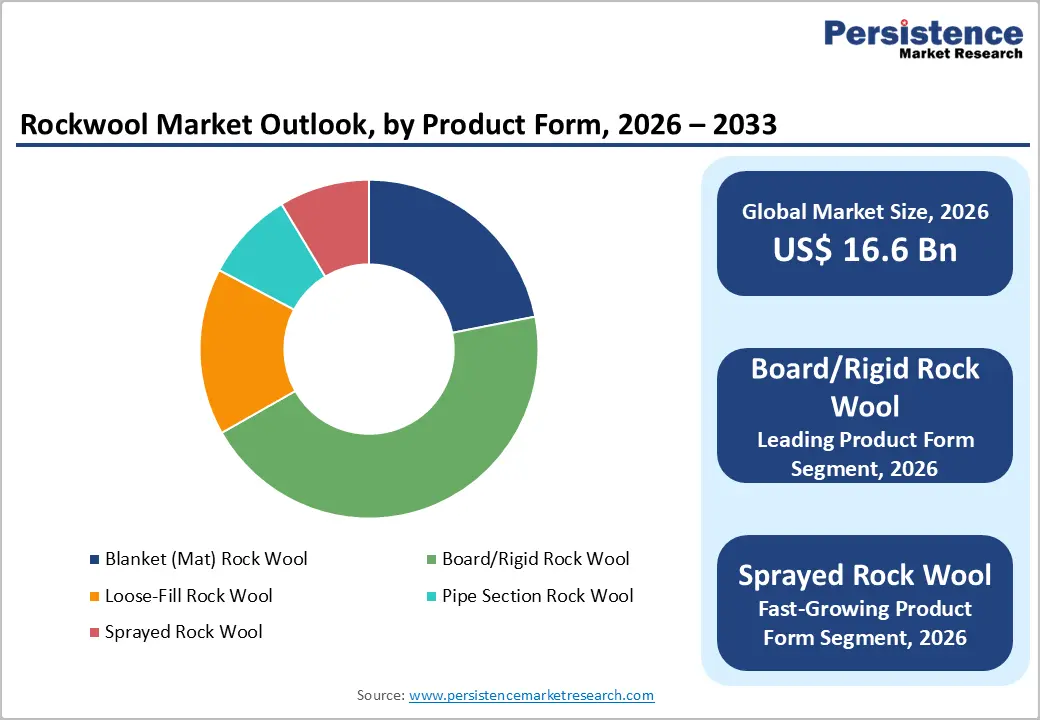

- Dominant Product Type: Board/Rigid Rock Wool dominates the product form landscape with a 43% share in 2026, anchored by its dimensional stability, compatibility with ETICS and ventilated facade systems, and alignment with Passive House and LEED green building standards globally.

- Fast-Growing Segment: Sprayed rock wool is the fast-growing product segment at a projected 7% CAGR by 2033, driven by expanding structural steel fire protection requirements in data centers, petrochemical plants, and high-rise commercial construction under NFPA and IBC standards.

- Key Market Opportunity: Rockwool-based horticulture growing media, led by ROCKWOOL's Grodan brand, represent a high-growth diversification opportunity, with the global vertical farming and hydroponics sector expanding rapidly and food security priorities intensifying global investment in controlled environment agriculture.

DRO Analysis

Drivers - Stringent Building Energy Efficiency Regulations and Green Building Standards

Increasingly stringent energy efficiency mandates are the most powerful structural driver of rockwool demand globally. The European Union's Energy Performance of Buildings Directive (EPBD), recast in 2024, requires all new buildings in EU member states to be zero-emission by 2030 and mandates large-scale renovation of the existing building stock to nearly zero-energy standards. The U.S. Department of Energy (DOE) estimates that buildings account for approximately 40% of total U.S. energy consumption, driving federal and state-level support for deep insulation retrofits.

Similarly, China's 14th Five-Year Plan includes binding targets for green building standards across 50% of new urban construction. These regulatory frameworks are creating sustained, policy-backed demand for high-performance thermal insulation solutions including rockwool boards, blankets, and pipe sections across both residential and commercial construction segments.

Rapid Urbanization and Construction Activity in Emerging Economies

Accelerating urbanization across Asia Pacific, the Middle East, and Africa is generating a huge demand for rockwool insulation products in new residential, commercial, and industrial construction. The United Nations (UN) projects that 68% of the world's population will live in urban areas by 2050, with the largest growth concentrated in India, China, Nigeria, and Indonesia.

According to the Global Construction Perspectives and Oxford Economics, the global construction output is forecast to grow by 85% to US$ 15.5 trillion by 2030, with emerging markets driving most of the new volume. High-rise residential and commercial buildings, where fire safety requirements mandate the use of non-combustible insulation, are a particularly high-value end market for rockwool, as stone wool's Euroclass A1 non-combustibility certification meets the most demanding fire safety specifications globally.

Restraints - High Manufacturing Energy Intensity and Raw Material Cost Volatility

Rockwool production is an energy-intensive process requiring melting of basalt rock and recycled slag at temperatures exceeding 1,500°C, making manufacturing costs highly sensitive to energy price fluctuations. The European energy crisis of 2022-2023, which saw natural gas prices spike by over 300% at peak, significantly elevated production costs for European rockwool manufacturers.

Raw material costs, particularly recycled slag availability tied to the steel industry's output cycles, introduce further margin unpredictability. These cost pressures constrain manufacturers' ability to offer competitive pricing against alternative insulation materials in price-sensitive markets, particularly in Latin America and parts of Southeast Asia.

Competition from Alternative Insulation Materials

Rockwool faces persistent competitive pressure from alternative insulation products, most notably glass wool (fiberglass), expanded polystyrene (EPS), and spray polyurethane foam (SPF), across various application segments. Glass wool, produced by manufacturers including Owens Corning and Knauf Insulation, offers comparable thermal performance at lower per-unit weight and often lower costs in residential applications.

EPS dominates in certain external wall insulation composite systems (ETICS) due to cost advantages. Where fire resistance is not a regulatory requirement, substitution by these materials limits rockwool's addressable volume, particularly in low-rise residential construction across price-sensitive geographies.

Opportunities - Sprayed Rock Wool Applications in Industrial and Commercial Fire Protection

Sprayed rockwool, the fast-growing product form segment at a projected CAGR of 7%, presents compelling growth opportunities in structural steel fire protection for commercial construction, oil & gas facilities, and petrochemical plants. The National Fire Protection Association (NFPA) standards and the International Building Code (IBC) mandate specific fire resistance ratings for structural steel elements in commercial and industrial buildings, and sprayed mineral fiber systems are a cost-effective compliance solution.

The rapid growth of data center construction globally, with the International Energy Agency (IEA) reporting that data centers consumed approximately 200-250 TWh of electricity in 2022, is creating significant incremental demand for sprayed rockwool in fire compartmentalization and thermal management applications. Companies offering spray application services alongside product supply are capturing higher margins, value-added revenue streams within this segment.

Horticulture and Hydroponic Growing Media in Controlled Environment Agriculture

Rockwool's application as a growing substrate in hydroponics and controlled environment agriculture (CEA) is an emerging high-growth opportunity distinct from the traditional construction sector. Rockwool growing slabs and cubes provide excellent water retention, aeration, and sterile growing conditions ideal for commercial hydroponic production of vegetables, herbs, and fruits. The global vertical farming and hydroponic market is experiencing significant momentum, with the Association for Vertical Farming (AVF) reporting consistent double-digit growth in controlled environment agricultural installations across North America, Europe, and Asia.

Major rockwool producers including ROCKWOOL International A/S have dedicated horticulture product lines, marketed under the Grodan brand, specifically engineered for precision irrigation systems. As food security concerns and sustainable agriculture investments intensify globally, demand for rockwool-based growing media is projected to grow significantly faster than the core construction segment.

Category-wise Analysis

Product Form Insights

Board/Rigid Rock Wool is the dominant product form segment, likely to account for approximately 43% of the global rockwool market in 2026. Rigid boards are preferred in a wide range of high-value construction applications, including external wall insulation, flat roof systems, and raised-access flooring, due to their dimensional stability, compressive strength, and the ability to maintain insulation performance under mechanical load without compression settlement. Their compatibility with ventilated facade systems and External Thermal Insulation Composite Systems (ETICS) used extensively across European green building retrofits underpins consistent demand.

ROCKWOOL International A/S and Saint-Gobain S.A. report that rigid board formats represent their largest revenue-generating product lines in European markets. The growing adoption of Passive House (Passivhaus) construction standards, which mandate very high insulation thicknesses, further elevates rigid board volumes in premium residential construction.

Application Insights

Building & construction is the leading application segment, poised to capture approximately 58% of the global rockwool market revenue in 2026. The segment's dominance is rooted in rockwool's unmatched combination of thermal, acoustic, and fire-safety properties demanded by modern construction codes globally. Residential and commercial building insulation, walls, roofs, floors, and facades, represent the highest-volume-end markets.

The European Commission estimates that over 35% of the EU's buildings are more than 50 years old and require energy renovation, creating a massive retrofit opportunity estimated at 35 million buildings needing upgrade by 2030. In new construction, LEED, BREEAM, and WELL green building certification standards increasingly specify non-combustible, low-embodied-carbon insulation materials, with rockwool's recyclability and mineral content supporting its sustainability credentials in green building rating systems.

Regional Analysis

North America Rockwool Market Trends and Insights

North America holds a stable share of the global rockwool market, driven by tightening building energy codes across U.S. states and Canadian provinces, growing institutional demand for fire-rated insulation in commercial and industrial construction, and the accelerating deep energy retrofit market supported by the U.S. Inflation Reduction Act (IRA), which allocated over US$ 369 billion in clean energy and building efficiency incentives.

U.S. Rockwool Market Size

The United States accounts for approximately 80% of North America's rockwool market revenue, anchored by robust commercial construction activity, federal and state energy efficiency incentives under the IRA, and growing awareness of rockwool's fire and acoustic advantages in multi-family residential construction. The U.S. Green Building Council (USGBC) reports over 105,000 LEED-certified projects globally, with the U.S. representing the largest share of certified floor area.

Europe Rockwool Market Trends and Insights

Europe is the second-largest rockwool market and the region with the highest per-capita consumption, driven by decades of robust building energy efficiency regulations, mandatory renovation programs under the EPBD, and the presence of the world's leading rockwool manufacturers headquartered in Denmark, Germany, and France. The EU Green Deal's renovation wave strategy is targeting the renovation of 3% of total building floor area annually across member states.

Germany Rockwool Market Size

Germany is likely to register approximately 22% of European rockwool market revenue in 2026, supported by the country's Gebäudeenergiegesetz (GEG), the Buildings Energy Act mandating near-zero energy standards for new construction, and substantial federal funding for building renovations under the Bundesförderung für effiziente Gebäude (BEG) program. Germany's large industrial sector also drives significant demand for high-temperature industrial insulation.

U.K. Rockwool Market Size

The U.K. accounts for approximately 17% of the European rockwool market, with demand significantly shaped by post-Grenfell Tower fire safety reforms that have effectively mandated non-combustible insulation for external wall systems on buildings above 11 meters under Building Regulations Approved Document B. This regulatory shift has structurally redirected market demand toward mineral wool, directly benefiting rockwool producers.

France Rockwool Market Size

France represents approximately 14% of the European rockwool market, driven by the RE2020 energy and carbon regulation for new buildings, one of Europe's most ambitious, which came into force in January 2022 and sets strict thermal performance and carbon footprint limits. The MaPrimeRénov's government renovation subsidy scheme has also stimulated demand for insulation in the residential retrofit segment.

Asia Pacific Rockwool Market Trends and Insights

Asia Pacific leads the global rockwool market with a 44% revenue share in 2026, driven by massive construction activity in China, which alone accounts for approximately 60% of the region's rockwool consumption, alongside rapid growth in India, South Korea, Japan, and ASEAN nations. China's push for green building standards, including its Three-Star Green Building rating system and energy efficiency codes for public buildings, is a primary demand engine.

India Rockwool Market Size

India accounts for approximately 9% of the Asia Pacific's rockwool market and is among the fastest-growing individual markets, driven by the National Mission for Enhanced Energy Efficiency (NMEEE), rapid industrial expansion, and the government's Smart Cities Mission encouraging green building certifications. Rising awareness of fire safety in high-rise commercial construction further supports premium rockwool adoption.

Japan Rockwool Market Size

Japan holds approximately 12% of the Asia Pacific's rockwool market revenue, supported by high construction quality standards, aging building stock renovation requirements, and stringent seismic and fire safety codes. Japan's ZEB (Zero Energy Building) policy framework and the country's advanced industrial sector, requiring high-temperature pipe and equipment insulation, sustain consistent premium product demand from domestic and international manufacturers.

Southeast Asia Rockwool Market Size

Southeast Asia contributes approximately 11% of the Asia Pacific's rockwool market revenue in 2026 and is experiencing accelerating growth driven by rapid commercial and industrial construction in Vietnam, Thailand, Indonesia, and Malaysia. Rising adoption of international building standards, the growth of export-oriented manufacturing facilities requiring fire-rated industrial insulation and expanding data center infrastructure are key demand drivers for the region.

Competitive Landscape

The global rockwool market is moderately consolidated, with ROCKWOOL International A/S commanding a clear market leadership position globally, supported by its vertically integrated production, the Grodan horticulture subsidiary, and manufacturing presence across 40+ countries. Key competitors including Knauf Insulation, Saint-Gobain S.A. (via Isover), Johns Manville, and Owens Corning, compete across overlapping mineral wool and glass wool product portfolios.

Regional players, including TechnoNICOL, Izocam, and Paroc Group hold significant shares in Eastern Europe, Turkey, and the Nordic markets, respectively. Competitive differentiation centers on fire certification breadth, thermal performance data, sustainability credentials (EPDs), and application engineering support. Investment in low-carbon manufacturing, including electric melting furnace technology, is emerging as a key long-term differentiator.

Key Developments:

- In March 2025: ROCKWOOL International A/S announced an investment of approximately EUR 100 million to expand production capacity at its Cigacice, Poland facility, targeting growing demand across Central and Eastern European construction markets.

- In October 2024: Knauf Insulation launched its next-generation ECOSE Technology mineral wool boards with a 20% reduction in embodied carbon compared to previous formulations, reinforcing its position in the European green building specification market.

- In June 2024, Saint-Gobain S.A. completed the acquisition of a majority stake in a Southeast Asian insulation manufacturer, expanding its Isover mineral wool distribution network into high-growth ASEAN construction markets, including Vietnam and Indonesia.

Companies Covered in Rockwool Market

- ROCKWOOL International A/S

- Johns Manville Corporation

- Knauf Insulation

- Owens Corning

- Saint-Gobain S.A.

- TechnoNICOL Corporation

- Kingspan Group plc

- Izocam Ticaret ve Sanayi A.S.

- CertainTeed Corporation

- Uralita Group

- Sai Insulation India

- Nanjing Zhongrunda New Material Technology Co., Ltd

- Paroc Group

- Ursa Insulation S.A.

- Arabian Fiberglass Insulation Company Ltd.

Frequently Asked Questions

The global rockwool market is projected to reach US$ 16.6 billion in 2026, growing from US$ 12.0 billion in 2020 to a historical CAGR of 5.5%. The market is forecast to expand further to US$ 25.3 billion by 2033, representing an absolute dollar opportunity of US$ 8.7 billion, driven by regulatory mandates for energy-efficient buildings and rapid construction activity in emerging economies.

The primary drivers include stringent global building energy efficiency regulations, notably the EU's EPBD mandating zero-emission buildings by 2030 and the U.S. Inflation Reduction Act's building efficiency incentives, combined with rapid urbanization in Asia Pacific and the Middle East. Rockwool's superior fire resistance (Euroclass A1 non-combustibility), thermal and acoustic performance, and growing adoption in horticulture and industrial applications further sustain diverse demand growth globally.

Asia Pacific leads the global rockwool market with approximately 44% revenue share in 2025, driven by China's massive construction output and green building code implementation, rapid industrialization in India and ASEAN nations, and high construction quality standards in Japan and South Korea. The region benefits from large domestic manufacturing capacity and consistently high construction investment volumes across both residential and commercial sectors.

Two compelling growth opportunities are: (1) Sprayed rockwool in structural fire protection for data centers, petrochemical facilities, and commercial high-rises, the fastest-growing product segment at 7% CAGR, supported by NFPA and IBC compliance mandates; and (2) Rockwool horticulture growing media for the rapidly expanding hydroponics and vertical farming sector, led by ROCKWOOL's Grodan brand, benefiting from global food security investments and controlled environment agriculture growth.

The global rockwool market is led by ROCKWOOL International A/S (Denmark), the world's largest mineral wool producer, followed by Saint-Gobain S.A. (Isover brand, France), Knauf Insulation (Germany), Johns Manville Corporation (U.S.), Owens Corning (U.S.), TechnoNICOL Corporation (Russia), and Kingspan Group plc (Ireland). Regional leaders include Paroc Group (Nordics), Izocam (Turkey), Arabian Fiberglass Insulation Company (Middle East), and Sai Insulation India.