- Clothing, Footwear, & Accessories

- U.S. Wool Market

U.S. Wool Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

U.S. Wool Market by Wool Type (Sheep’s Wool, Merino Wool, Cashmere Wool, Alpaca Wool, Mohair Wool, Angora Wool, Others), Form (Woven, Non-woven, Others), Application (Apparel, Home Textiles, Industrial Textiles, Technical Textiles, Automotive Textiles, Others), and Regional Analysis for 2026 - 2033

U.S. Wool Market Trends & Analysis

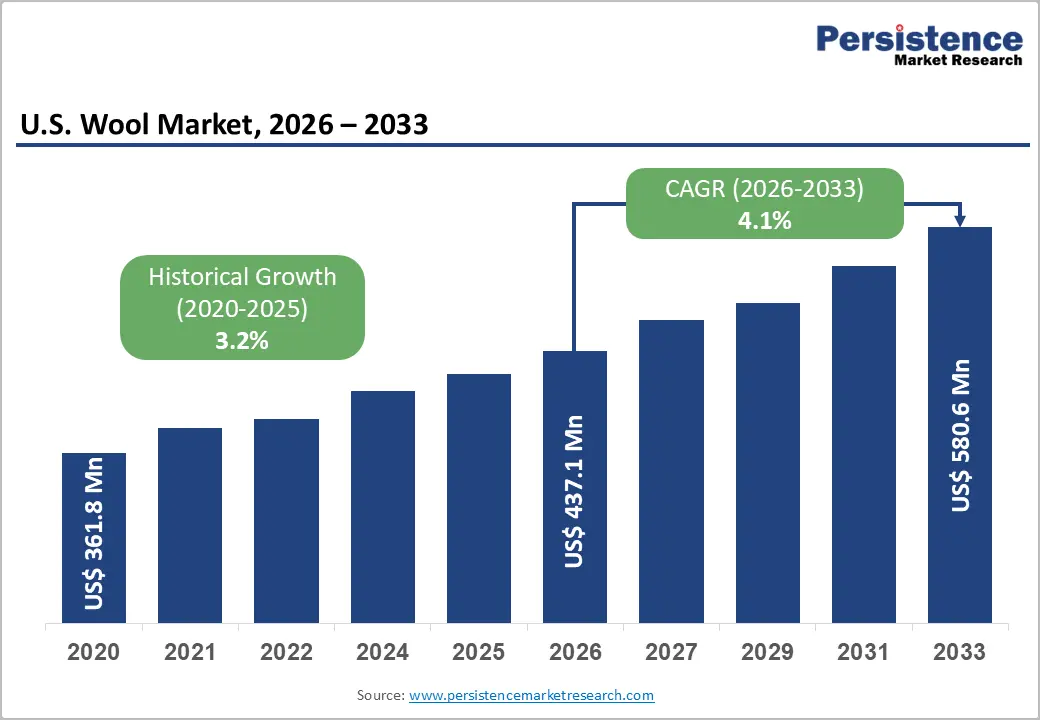

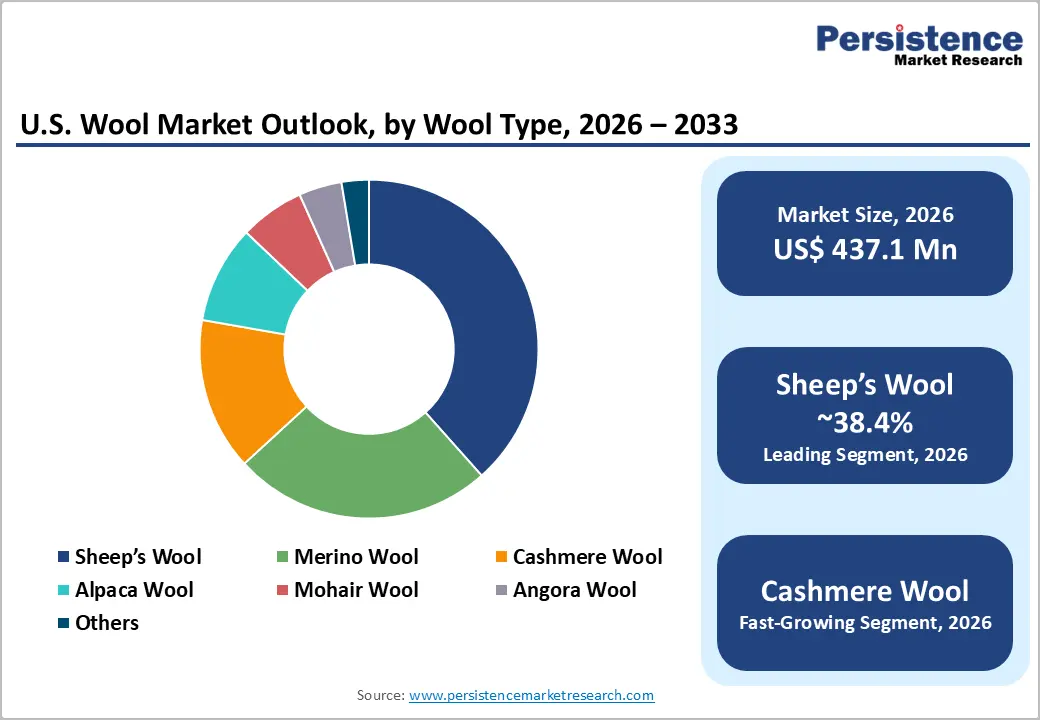

The U.S. wool market size is projected at US$ 437.1 million in 2026 and is projected to reach US$ 580.6 million by 2033, growing at a CAGR of 4.1% between 2026 and 2033. Growth is underpinned by rising demand for sustainable, biodegradable fibers, as global wool markets expand from about US$ 44 Bn in the mid-2020s to the mid-US$ 60 Bn range by 2033, supported by 3.5-5% annual growth in natural fiber consumption. U.S. greasy wool production was roughly 22.5 million pounds in 2024, and farm-gate value reached US$ 35.3 million in 2023, forming the upstream basis for higher-value apparel, home, and technical textiles.

At the same time, wool’s environmental profile biodegradability, recyclability and long lifespan-aligns with emerging regulations and brand commitments on circularity and microplastic reduction. Premium and performance brands are expanding Merino-rich product lines and circular initiatives, while regenerative agriculture and traceability programs such as Nativa Regen strengthen the value proposition for U.S.-sourced wool in both domestic and export-oriented value chains.

Key Industry Highlights:

- Segment Leadership: Apparel holds around 41.7% share, supported by premium and performance Merino knitwear, tailored garments, and outerwear, while Sheep’s Wool remains the leading fiber type with 38.4% share across apparel, home, and industrial uses.

- Fast-Growing Wool Type: Cashmere wool grows at roughly 10% CAGR, and Automotive Textiles expand near 6.4% CAGR, reflecting rising demand for luxury knitwear and sustainable interior insulation and padding in vehicles, particularly EVs and premium models.

- Form Dynamics: Woven wool accounts for about 63.8% of value, anchored by suiting, coats and blankets, whereas Non-woven wool grows around 5.1% CAGR as felts, insulation and technical composites gain traction in industrial and building applications.

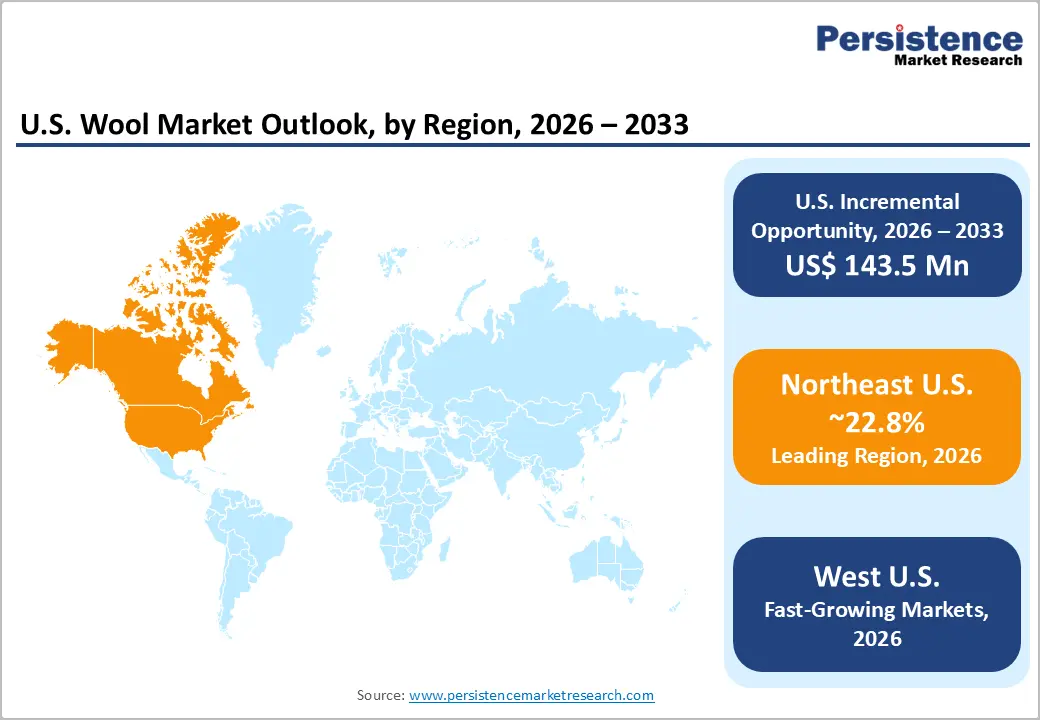

- Regional Leaders: Northeast U.S. leads with 22.8% share, supported by fashion and home-textile demand, while West U.S. records the fastest growth at about 4.8% CAGR and Southeast U.S. combines 22.3% share with roughly 7.7% CAGR, driven by automotive and interior applications.

- Strategic Shifts: Regenerative wool programs, circular initiatives like Smartwool’s Second Cut™, and the Nativa Regen traceability platform are reshaping sourcing and branding, while IWTO’s Green Book improves environmental accounting and supports premium positioning for verified U.S. wool.

- Value-Chain Evolution: Infrastructure proposals such as the Pacific Northwest wool pool and scouring facility aim to rebuild domestic processing capacity, helping U.S. stakeholders capture more value between raw wool and high-margin textiles and apparel.

Market Dynamics Analysis

Drivers - Sustainability, biodegradability, and regulatory alignment

Wool’s credentials as a renewable, biodegradable and recyclable fiber are increasingly quantified by the International Wool Textile Organisation (IWTO), which highlights that roughly 50% of wool’s weight is organic carbon, that wool products have long lifespans, and that around 6% of the total wool market is already recycled-far higher than most fibers. Wool also biodegrades readily on land and in water and does not contribute to microplastic pollution, which aligns with tightening regulations on synthetic fiber shedding.

In parallel, global wool demand is projected to rise from about US$ 42-45 Bn in 2024-2026 to around US$ 56-65 Bn by the early 2030s, supported by 3.6-4.9% CAGR as brands and regulators prefer low-impact, traceable inputs. For U.S. stakeholders, this sustainability advantage enables premium positioning in apparel, home and technical segments, helps satisfy retailer due-diligence requirements, and supports access to eco-label and carbon-label programs that can defend margins even as domestic wool production volumes trend downward.

Premium and Performance Apparel Demand

Global wool-based apparel is benefiting from a pivot by outdoor, lifestyle and luxury brands toward performance Merino and fine wool blends that offer moisture management, thermoregulation and odor resistance without synthetics. Brands active in the U.S. market including Smartwool, Icebreaker, Patagonia and others have expanded Merino-rich collections and marketing campaigns that reposition wool as a lightweight, high-performance fiber rather than a heavy, niche winter fabric. A 2024 consumer survey cited by industry sources shows rising preference for natural fibers in next-to-skin garments, particularly among younger, sustainability-focused demographics.

This demand shift supports the dominance of apparel applications, which account for an estimated 41.7% of U.S. wool end-use value, and drives above-average growth in Merino and Cashmere segments as brands seek differentiated, soft-hand fabrics for knitwear, base layers and tailored garments. U.S. mills such as Pendleton Woolen Mills emphasize domestic sourcing relationships and American-made fabrics, while niche spinners like Harrisville Designs use 100% U.S.-sourced wool to target premium craft and heritage markets. Together, these trends support value growth even in the face of relatively flat or declining domestic clip volumes.

Restraints - Declining domestic production and supply chain constraints

USDA data show U.S. shorn wool production declined from about 38.8 million pounds in 2020 to 22.5 million pounds in 2024, reflecting lower sheep inventories and structural contraction in the sheep industry. Texas producers, for example, cut wool output by 19% in 2023 as flock numbers fell. In addition, the U.S. now has only two commercial-scale scourers, with Chargeurs Wool USA highlighted as a key facility, resulting in logistical bottlenecks and higher dependence on export or offshore processing.

Recent analysis of the wool yarn market notes supply chain limitations in securing high-quality domestic wool, with USDA-reported disruptions reducing available stocks in 2024 due to transport challenges from rural areas and complexities in grading and sorting. These constraints limit the ability of U.S. mills to respond quickly to demand spikes, raise working-capital needs for processors and can shift part of value creation to overseas scouring and spinning hubs, dampening domestic market scalability despite healthy downstream demand.

Competition from synthetics and price volatility

Although wool benefits from strong eco-credentials, it competes directly with cheaper synthetic fibers whose global production continues to grow faster than that of natural fibers. Market intelligence indicates that while the global wool market is expanding at roughly 5% CAGR, overall apparel fiber output is rising slightly faster, driven mainly by polyester. Fluctuating wool prices linked to global clip volumes, currency movements, and fashion cycles create uncertainty for U.S. buyers and can incentivize fiber substitution when cost pressures intensify.

For mass-market apparel and home textiles, retailers often prioritize cost and consistency, which can limit wool’s penetration outside premium segments when synthetic blends offer acceptable performance at lower prices. In industrial and automotive applications, engineering specifications sometimes favor synthetic or mineral fibers based on legacy standards, further constraining adoption. Together, these factors cap wool’s addressable share in price-sensitive segments, tempering the growth outlook relative to its sustainability-driven potential.

Opportunities - Regenerative, traceable and certified wool

The launch of regenerative agriculture programs such as Nativa Regen in the United States-developed by Chargeurs Luxury Fibers with Oregon-based Shaniko Wool Company-creates a platform for dual Nativa/Responsible Wool Standard (RWS) certification, backed by blockchain traceability from farm to finished garment. Shaniko oversees nine farms across four states and was the first U.S. wool producer to receive RWS certification, positioning it at the forefront of verified regenerative wool supply. IWTO’s Green Book initiative, aligned with ISO 14067, further strengthens wool’s biogenic carbon accounting, facilitating robust environmental claims for certified fibers.

As global wool markets head toward US$ 65 billion by the early 2030s, even modest penetration of regenerative and fully traceable wool into premium apparel and home textiles could represent a multi-hundred-million-dollar opportunity globally, with the U.S. capturing a share through domestic growers and brand programs. For the U.S. market sized at US$ 0.4371 Bn in 2026, a 15-20% share of value coming from certified regenerative or traceable wool by 2033 would translate into tens of millions of dollars in incremental premium revenue, particularly in Merino, Cashmere, and high-end woven segments.

Regional clustering and domestic processing capacity

A 2024 pre-feasibility study for the Pacific Northwest sheep’s wool sector highlights substantial surplus coarse to medium wool in Washington, Oregon and Idaho and proposes a tri-state wool pool and regional scour facility to rebuild the local industry. The study argues that aggregating sufficient volume would justify investment in scouring, storage and logistics infrastructure, along with a “Pacific Northwest Wool” brand identity for mid-scale markets. This vision aligns with the fact that Chargeurs Wool USA and one other scourer are currently the only commercial-sized scouring plants in the country, underscoring capacity gaps.

By expanding domestic processing and branding, such initiatives could capture more of the value added between greasy wool and finished textile, supporting rural economies and reducing transport emissions. For the U.S. wool market, incremental domestic scouring and early-stage processing capacity, coupled with regional brands, could conservatively unlock additional revenue in the low tens of millions of dollars by 2033 through higher-margin yarns, fabrics, and branded products targeting both domestic and export buyers.

Category-wise Analysis

Wool Type Insights

Sheep’s wool is the leading wool type, accounting for roughly 38.4% of the U.S. wool market value, as it forms the bulk of domestic greasy wool production and underpins mainstream apparel, home textiles and felts. USDA data show U.S. shorn wool output at 22.5 million pounds in 2024, dominated by traditional sheep breeds in states such as California, Wyoming, Utah, Colorado, and Idaho. Compared with Merino, Cashmere, Alpaca, Mohair, and Angora, sheep’s wool offers broader availability and more competitive pricing, which should preserve its leadership despite growing interest in fine and specialty fibers.

Cashmere is the fast-growing wool type, projected at around 10% CAGR, driven by luxury knitwear, premium accessories, and high-margin blended fabrics that command substantial price premiums over conventional wool. U.S. brands increasingly source certified and traceable Cashmere aligned with animal-welfare and land-stewardship standards, allowing them to differentiate within the broader natural fiber portfolio while complementing Merino and other fine wools.

Form Insights

By form, woven wool textiles lead with an estimated 63.8% share, reflecting the continued importance of wool suiting, overcoats, blankets, and high-end upholstery fabrics in U.S. consumption. Heritage mills such as Pendleton Woolen Mills, which weaves blankets and apparel fabrics in Oregon and Washington using long-standing relationships with sheep ranchers, exemplify this dominant woven segment and help sustain domestic spinning and weaving capabilities. Compared with non-wovens and other forms, woven products capture higher per-unit value and sit at the core of fashion, outdoor and home textile demand.

Non-woven wool is the fast-growing form, increasing at about 5.1% CAGR, supported by applications in felts, insulation, filtration media and technical composites where wool’s loft, resilience and fire resistance are advantageous. As building codes and industrial buyers seek sustainable materials and improved acoustic and thermal performance, demand for non-woven wool mats and blends in construction, industrial equipment and automotive interiors is expected to outpace traditional woven categories from a smaller base.

Application Insights

Apparel (sweaters, suits, coats, knitwear) is the leading application, with around 41.7% share of U.S. wool market value, anchored by premium knitwear, tailored garments and performance base layers. The global shift toward natural and luxury fibers, combined with expanded Merino collections by outdoor and athleisure brands, sustains wool’s relevance in both winter and trans-seasonal wardrobes. Compared with home, industrial, technical and automotive uses, apparel captures higher brand margins and benefits most directly from storytelling around animal welfare, traceability and circularity.

Automotive textiles are the fast-growing application is Automotive Textiles (interior insulation & padding), which is forecast to reach 6.4% CAGR, supported by increased focus on cabin comfort, noise attenuation and sustainable materials in electric and premium vehicles. Wool-based felts and blends are being evaluated for headliners, door panels, seat padding and acoustic insulation, where they can replace petrochemical foams and synthetic fiber mats, supporting OEM sustainability targets and offering incremental demand for mid-micron wool types.

Regional Insights

Northeast U.S. Wool Market Trends

The Northeast U.S. commands a leading share due to high concentrations of fashion, outdoor and lifestyle brands, dense urban retail markets and strong demand for premium wool apparel and home textiles in states such as New York, Massachusetts and Pennsylvania. In 2026, the Northeast’s wool market is estimated in the low-hundreds-of-millions-of-dollars range, reflecting both direct sourcing from U.S. growers and imports of fine wool, yarns and finished products, with steady growth expected through 2033 supported by premium apparel, blankets and interior textiles.

Beyond New York and Massachusetts, Pennsylvania home to the historic Woolrich brand along with New Jersey and New England states, underpin demand in outerwear, heritage sportswear and home furnishings. The region’s regulatory environment emphasizes product safety and sustainability disclosures, while competition features a mix of global brands, specialty retailers and e-commerce players investing in traceable and environmentally certified wool lines.

West U.S. Wool Market Trends

The West U.S. is the fast-growing region, with projected 4.8% CAGR, underpinned by significant wool production in states such as California, Wyoming, Utah, Colorado and Idaho and by strong regional brands and mills that emphasize U.S.-grown wool and local manufacturing. By 2026, the Western wool market is expected to account for a substantial portion of U.S. clip value and downstream processing, including scouring by Chargeurs Wool USA and fabric production by mills like Pendleton, supporting regional revenues in the high tens of millions to low hundreds of millions of dollars.

States such as Oregon, Washington, Colorado and Utah are central to regenerative and traceable wool initiatives, including the Nativa Regen program and proposed Pacific Northwest wool pool, which aim to rebuild infrastructure and capture more value locally. The regional ecosystem combines sheep producers, scouring, mills and outdoor brands, and leverages innovation in sustainability, branding and circularity to differentiate West-sourced wool in domestic and export markets.

Southeast U.S. Wool Market Trends

The Southeast U.S. holds a prominent 22.3% share and grows at around 7.7% CAGR, driven by population growth, strong retail presence and increasing use of wool in apparel, home and automotive textiles in states such as Texas, Georgia and the Carolinas. In value terms, Southeast U.S. wool consumption is expected to reach the mid-tens of millions of dollars by 2026, supported by downstream processing, distribution hubs and automotive manufacturing clusters that source wool-blend interior materials and carpets, with continued expansion through 2033.

Texas remains a notable wool-producing state despite recent volume declines, while broader Southeast states host textile and automotive supply chains that integrate wool into upholstery, insulation and technical felts. The region benefits from pro-manufacturing policies and investment incentives, with competition among global and domestic suppliers focusing on cost-competitive, sustainable wool solutions aligned with OEM and retailer environmental targets.

Competitive Landscape

The U.S. wool market is fragmented upstream but more consolidated downstream, with numerous sheep producers and a limited number of large scourers and mills, complemented by powerful apparel and outdoor brands. Key differentiators include traceability, regenerative and RWS certifications, design capabilities, and brand storytelling around sustainability, durability and American-made production.

Dominant strategic themes are innovation in circular and regenerative programs, cost leadership in commodity wool processing, and market expansion through deeper integration between growers, processors and brands, supported by data-rich transparency platforms and partnerships that link U.S. fiber to global premium apparel and technical textile demand.

Strategic Developments

- In April 2024, Smartwool launched its Second Cut™ Hike Sock in the U.S. and abroad, using yarn from its sock take-back program and ZQ Merino, highlighting closed-loop circularity and driving demand for recycled wool in performance socks and accessories.

- In April 2025, Smartwool and Icebreaker expanded collaborative circular-fashion initiatives under VF Corporation, combining resale and recycling programs to extend Merino wool product lifecycles, reduce waste and position U.S. merino brands as leaders in climate-positive and regenerative wool strategies.

- In December 2024, a Pacific Northwest pre-feasibility study proposed a tri-state wool pool and regional scour facility, outlining infrastructure and branding investments needed to aggregate surplus coarse and medium wool and rebuild a competitive mid-scale wool industry in Washington, Oregon and Idaho.

- In January 2026, IWTO introduced its Green Book biogenic carbon accounting methodology, aligning with ISO 14067 to more accurately reflect wool’s natural carbon cycles and providing U.S. brands and growers with robust data for environmental product declarations and sustainability marketing claims.

U.S. Wool Market Report - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 361.8 Mn |

| Current Market Value (2026) | US$ 437.1 Mn |

| Projected Market Value (2033) | US$ 580.6 Mn |

| CAGR (2026 - 2033) | 4.1% CAGR |

| Leading Region | Northeast U.S - 22.8% |

| Dominant Application | Apparel - 41.7% |

| Top-ranking Wool Type | Sheep’s Wool - 38.4% |

| Incremental Opportunity | US$ 143.5 Mn |

Companies Covered in U.S. Wool Market

- VF Corporation (Smartwool, Icebreaker)

- Patagonia Inc.

- Pendleton Woolen Mills

- Woolrich

- Chargeurs Wool USA / Nativa

- Shaniko Wool Company

- Smartwool

- Harrisville Designs

- The North Face

- Minus33

- The Woolmark Company

- Regional wool pools and cooperatives

Frequently Asked Questions

The U.S. Wool Market is expected to reach about US$ 437.1 Mn in 2026 and approach US$ 580.6 Mn by 2033, reflecting steady value growth across apparel, home and technical applications.

Growth is driven by rising demand for sustainable, biodegradable fibers, premium and performance apparel expansion, and increasing use of wool in technical, home and automotive textiles supported by regenerative, traceable and circular initiatives.

Between 2026 and 2033, the U.S. Wool Market is projected to grow at approximately 4.1% CAGR, broadly in line with global wool sector growth in natural and eco-friendly textile fibers.

Key opportunities lie in regenerative and traceable wool programs, circular and recycled wool products, and expanded domestic processing and regional branding, which can unlock premium pricing and new revenue pools in apparel, home and technical segments.

Key players include VF Corporation (Smartwool, Icebreaker), Patagonia, Pendleton Woolen Mills, Woolrich, Chargeurs Wool USA / Nativa, Shaniko Wool Company, Harrisville Designs, The North Face, Minus33 and The Woolmark Company, alongside regional wool pools and cooperatives.