- Biotechnology

- Whole Exome Sequencing Market

Whole Exome Sequencing Market Size, Share, and Growth Forecast 2026 - 2033

Whole Exome Sequencing Market by Product (Instruments, Consumables, Software and Services), Application (Drug Discovery & Development, Clinical Diagnostics, Personalized Medicines, Others), Technology (ION Semiconductor Sequencing, Sequencing by Synthesis, Others), End User, by Regional Analysis, 2026 - 2033

Whole Exome Sequencing Market Size and Trend Analysis

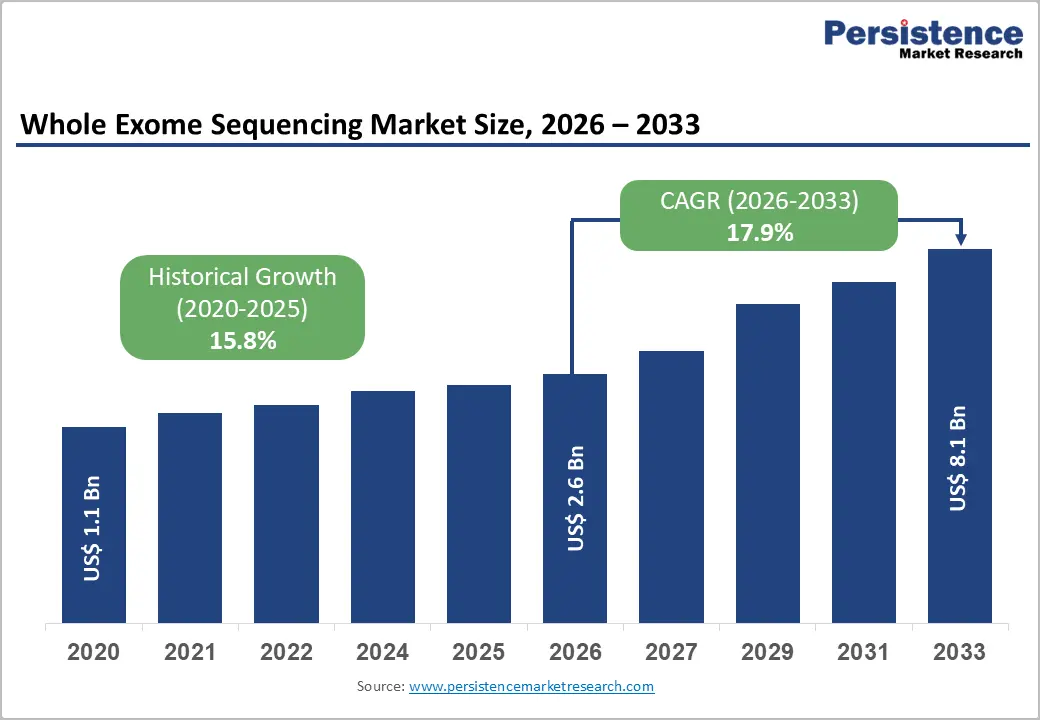

The global whole exome sequencing market size is expected to be valued at US$ 2.6 billion in 2026 and projected to reach US$ 8.1 billion by 2033, growing at a CAGR of 17.9% between 2026 and 2033. It is witnessing a strong growth due to the rising adoption of precision medicine, increasing use in clinical diagnostics, and expanding applications in rare disease detection and oncology. WES enables comprehensive analysis of protein-coding regions, making it highly valuable for identifying disease-causing genetic mutations.

Decline in sequencing costs, from over US$ 1,000 per genome a decade ago to below US$ 200, has improved affordability and accessibility. Growing insurance coverage for diagnostic applications, the rise of domestic manufacturers, and strategic collaborations between genomics companies and healthcare providers further support market expansion. Government initiatives such as NHGRI funding and the European Union’s 1+ Million Genomes project are also driving institutional demand globally.

Key Industry Highlights:

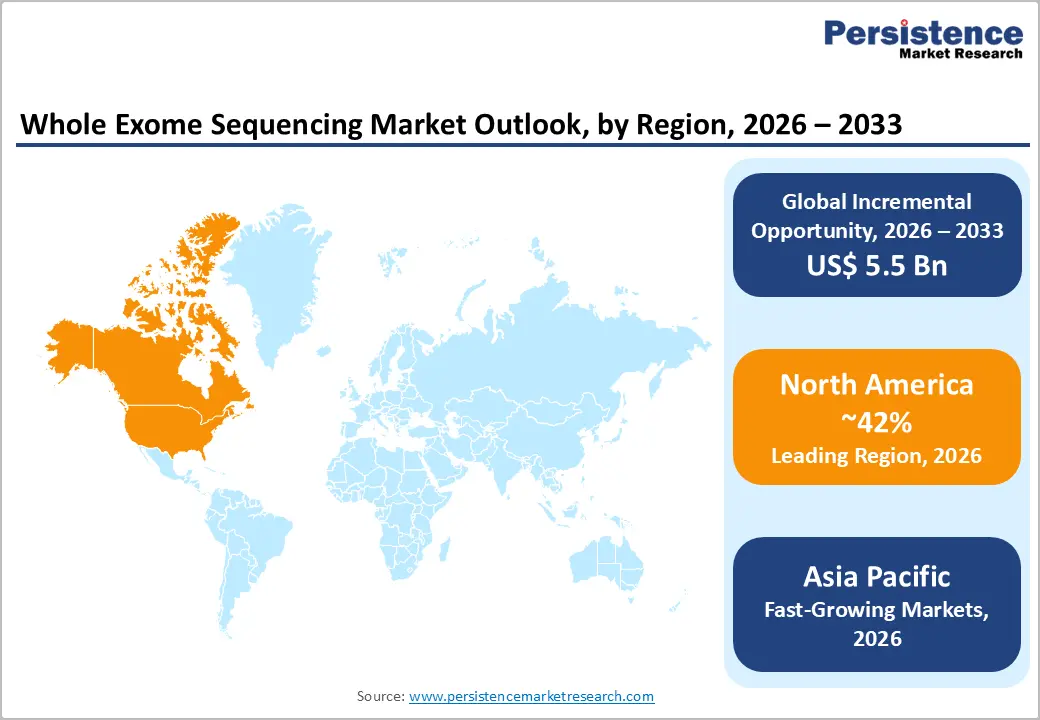

- Leading Region: North America dominated the market in 2026 with ~42% revenue share, driven by mature reimbursement frameworks, high clinical adoption, and leading genomics companies including Illumina and Caris Life Sciences.

- Fast-Growing Market: Asia Pacific is projected to register the highest CAGR during the forecast period, propelled by government-funded population genomics programs in China, India, and Japan, alongside rapidly expanding clinical WES infrastructure and a large underdiagnosed rare disease burden.

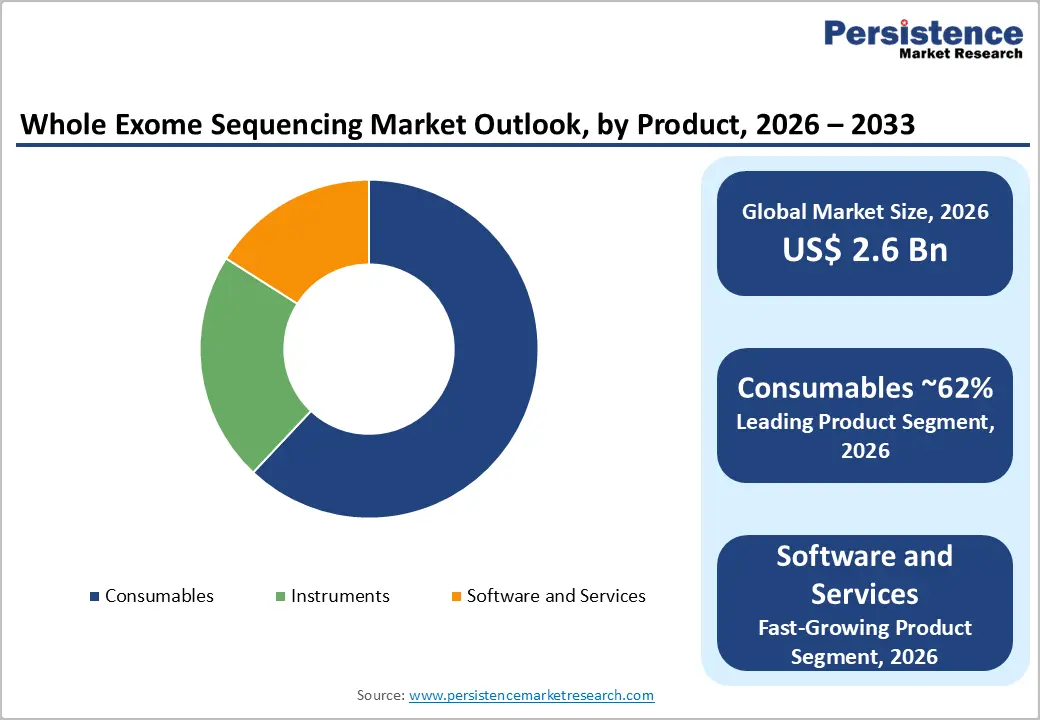

- Dominant Product Segment: Consumables lead the product category with ~62% market share in 2025, driven by recurring demand for capture kits and library preparation reagents across clinical and research applications, with leading products from Illumina and Integrated DNA Technologies.

- Fast-Growing Product Segment: The Software and Services segment is projected to fastest growing segment, fuelled by AI-enabled variant interpretation platforms, cloud-based bioinformatics solutions, and growing outsourcing of WES data analysis by clinical laboratories and CROs.

- Key Opportunity: Large-scale population genomics initiatives across the Asia Pacific, including India's Genome India Project and China's Precision Medicine Initiative, offer significant revenue opportunities for WES service providers and software vendors during the forecast window.

Market Dynamics

Drivers - Surging Demand for Rare Disease Diagnosis and Genomic Medicine

Whole exome sequencing has emerged as the gold standard for identifying the genetic basis of rare and undiagnosed diseases, which collectively affect ~1 in 17 people globally according to the Rare Diseases International coalition. Traditional diagnostic odysseys often span 5-7 years and involve numerous inconclusive tests; WES dramatically shortens this trajectory by interrogating all protein-coding regions of the genome in a single assay.

The Undiagnosed Diseases Network (UDN), supported by the U.S. National Institutes of Health (NIH), reported diagnostic success rates exceeding 35% using exome sequencing for previously unresolved cases. As rare disease registries expand globally, and reimbursement pathways improve particularly in France, Japan, and Australia clinical demand for WES is accelerating meaningfully across both pediatric and adult patient populations.

Restraints - Regulatory Complexity and Data Privacy Concerns

The clinical deployment of WES is increasingly subject to evolving and heterogeneous regulatory frameworks across jurisdictions. In the European Union, the General Data Protection Regulation (GDPR) and the EU In Vitro Diagnostic Regulation (IVDR 2017/746) impose stringent requirements on genomic data handling, consent, and cross-border transfer, increasing compliance costs. Similarly, in the United States, the interplay between HIPAA, the Genetic Information Nondiscrimination Act (GINA), and state-level laws creates a complex compliance landscape.

Patient concerns regarding genetic data privacy and potential misuse particularly for insurance discrimination can reduce uptake and complicate large-scale population genomics programs.

Opportunities - Growing collaboration between genomics companies and healthcare providers

The growing collaboration between genomic companies and healthcare providers presents a significant opportunity in the global whole exome sequencing market. Genome Medical collaborated with Nest Genomics in January 2025 to expand access to genetic services, offering timely test ordering, medical consultations, genetic counselling, and personalized treatment.

In April 2024, SOPHiA GENETICS joined forces with Strand Life Sciences to advance precision medicine initiatives and improve the use of genomic data to enhance patient care. Flatiron Health collaborated with Caris Life Sciences in January 2024 to integrate clinical data from Flatiron’s EHR information with genomic insights from Caris’ DNA, RNA, and imaging data, advancing oncology research.

These partnerships facilitate seamless integration of WES into clinical practice, improving diagnosis and treatment plans, particularly for oncology and rare diseases. As healthcare systems embrace precision medicine, such collaborations are poised to drive the widespread adoption and growth of WES in clinical settings.

Category-wise Analysis

Product Insights

The consumables segment dominates the whole exome sequencing market, accounting for ~62% of total market revenue in 2026. This dominance is underpinned by the recurring nature of consumable purchases, including capture kits, library preparation reagents, flow cells, and sequencing chips, relative to one-time instrument investments.

As WES throughput scales in clinical and research settings, consumable spend compounds accordingly. Illumina, Inc. and Integrated DNA Technologies (IDT) are leading providers of WES-specific enrichment kits such as the IDT xGen Exome Research Panel and Illumina's TruSeq Exome, which together account for a substantial share of consumable procurement globally. The continued reduction in per-sample sequencing costs, driven by increased competition among kit manufacturers and economies of scale, further supports high consumable uptake across all end-user segments.

Application Insights

The clinical diagnostics leads the application landscape of the whole exome sequencing market, commanding ~38% of overall application revenue in 2025. Clinical diagnostics serves as the primary gateway through which WES transitions from research settings to routine patient care. The segment's leadership is reinforced by the growing integration of WES into standard-of-care pathways for rare inherited disorders, pediatric neurology, and hereditary cancer syndromes.

The American College of Medical Genetics and Genomics (ACMG) has issued guidelines recommending WES as a first- or second-tier diagnostic tool for patients with suspected genetic conditions. Payer coverage expansion in the U.S., Germany, and France is further accelerating clinical test volumes, supported by robust reimbursement codes under CPT code 81415 and comparable frameworks in Europe.

End-user Insights

The Academic and Research Institutes segment holds the leading share among end users in the Whole Exome Sequencing market, representing ~34% of demand in 2026. This leadership is driven by the pivotal role of universities, national genome centers, and government-funded research organizations in generating foundational exome datasets that underpin translational genomics. Institutions such as the Wellcome Sanger Institute, the Broad Institute of MIT and Harvard, and the Beijing Genomics Institute (BGI) conduct large-scale WES studies that directly consume instruments, consumables, and sequencing services.

Sustained government research funding, including NIH's National Human Genome Research Institute (NHGRI) budget of over US$ 600 million annually, ensures continued institutional investment in WES capabilities throughout the forecast period.

Regional Insights

North America Whole Exome Sequencing Market Trends and Insights

North America is anticipated to hold 42% of the global market share in 2025, driven by growing insurance coverage for WES, large-scale genomics programs, and FDA-backed diagnostic integration driving the clinical adoption. Whole genome sequencing (WGS) and exome sequencing are widely used to diagnose suspected genetic disorders. The U.S. has been a frontrunner in integrating WES into insurance coverage, particularly for oncology, rare genetic disorders in children, and neurodevelopmental conditions.

A recent study revealed an increase in the payer coverage for both WGS and WES across the region. Currently, half of the insurance population has coverage for only WES, 12% have coverage for both WGS & WES, while 37% have no coverage for either. This growing insurance coverage is expected to boost WES adoption in clinical settings, further expanding the U.S. whole exome sequencing market.

U.S. Whole Exome Sequencing Market Size

The U.S. accounts for ~85% of North America's WES market revenue, underpinned by the concentration of leading WES providers, including Illumina, Caris Life Sciences, and GENEWIZ (Azenta Life Sciences). CMS reimbursement under CPT codes for exome sequencing and the FDA's expanding companion diagnostic approvals create a favorable commercial environment for continued U.S. market growth.

Europe Whole Exome Sequencing Market Trends and Insights

Europe represents the second-largest regional market, driven by coordinated genomics initiatives such as the EU 1+Million Genomes Initiative and national programs in the UK, Germany, and France. The region's strong public health infrastructure and the integration of WES into rare disease diagnostic pathways through the European Reference Networks (ERNs) support consistent market expansion across both Western and Eastern European healthcare systems.

Germany Whole Exome Sequencing Market Size

Germany holds ~22% of Europe's WES market, bolstered by a robust network of university hospitals and the German Center for Genomic Research. Germany's early adoption of WES under statutory health insurance (GKV) coverage for hereditary conditions and active participation in pan-European genomics consortia distinguish it as Europe's leading national WES market.

UK Whole Exome Sequencing Market Size

The UK accounts for ~20% of the European WES market revenue. The NHS Genomic Medicine Service (GMS), which expanded clinical whole genome and exome testing capacity from 2021 onwards, alongside the legacy of Genomics England's 100,000 Genomes Project, positions the UK as a global benchmark for health system-integrated genomics, driving sustained clinical WES volumes.

France Whole Exome Sequencing Market Size

France contributes ~16% of the European market, supported by the France Médecine Génomique 2025 (PFMG 2025) national sequencing plan. This initiative established 12 clinical sequencing sites (SeqOIA and AURAGEN) across the country, providing reimbursed WES and WGS for oncology and rare disease indications, creating a structured and growing clinical demand pipeline.

Asia Pacific Whole Exome Sequencing Market Trends and Insights

Asia Pacific is the fast-growing regional market for whole exome sequencing and is expected to register the highest CAGR during the forecast period. China dominates regional demand through BGI's extensive sequencing infrastructure and government-backed population genomics programs, while Japan, India, South Korea, and Australia are ramping up clinical and research WES deployments. Rapidly expanding healthcare digitization budgets and growing awareness of genomic medicine are accelerating adoption across diverse healthcare systems.

India Whole Exome Sequencing Market Size

India is among the fast-growing individual country markets in the region, supported by the Genome India Project and a rapidly growing network of private diagnostic chains such as MedGenome and Mapmygenome. India's large genetically diverse population, coupled with a growing middle class seeking precision diagnostics, positions it to capture an estimated 18-20% of the Asia Pacific's WES market by 2033.

Japan Whole Exome Sequencing Market Size

Japan represents a mature but steadily growing WES market within Asia Pacific, holding ~14% of regional revenue. Japan's Agency for Medical Research and Development (AMED) funds large-scale genomic medicine implementation programs, and the integration of WES into cancer board workflows under the Japan Cancer Genomic Medicine Promotion Plan ensures sustained clinical demand from hospital-based sequencing centers.

Competitive Landscape

The global market is moderately consolidated, with Illumina, Inc. commanding a dominant position through its SBS platform ecosystem and broad consumable portfolio. The competitive landscape is defined by platform innovation, service expansion, and strategic partnerships. Market leaders are investing in AI-powered interpretation software, direct-to-laboratory sequencing services, and emerging market presence as key differentiators. BGI Genomics and Eurofins Genomics compete aggressively on cost and throughput, particularly in price-sensitive markets.

Emerging players such as 3billion, Inc. are leveraging rare disease specialty positioning and AI-driven diagnostics to carve out defensible niches within the broader market ecosystem.

Key Developments:

- In February 2026, Illumina, Inc. unveiled an 18-month NovaSeq X innovation roadmap featuring Q70 quality scores, 30% faster performance, and output reaching 35 billion reads with new flow cells and staggered starts.

- In February 2025, Roche introduced its sequencing by expansion (SBX) technology, a new category of next-generation sequencing offering ultra-rapid, high-throughput sequencing for a broad range of applications, including WGS, WES, and RNA sequencing.

- In October 2024, Illumina Inc., collaborated with National Taiwan University (NTU) Hospital for a “Whole Genome Sequencing (WGS) Project.”

- September 2024: GENEWIZ (Azenta Life Sciences) expanded its WES service portfolio with a new clinical-grade exome sequencing offering targeting rare disease diagnostics for hospital and CRO clients across North America and Europe.

- March 2024: BGI Genomics announced a partnership with Mapmygenome to expand affordable WES services across South Asia, targeting underserved rare disease patient populations in India and neighboring markets.

Companies Covered in Whole Exome Sequencing Market

- CD Genomics

- Eurofins Genomics

- GENEWIZ (Azenta Life Sciences)

- Illumina, Inc.

- Integrated DNA Technologies, Inc.

- Blueprint Genetics Oy

- Caris Life Sciences

- MedGenome

- Psomagen

- 3billion, Inc.

- BGI

- Mapmygenome

- Almac Group

- CeGaT GmbH

- Others

Frequently Asked Questions

The global whole exome sequencing market is estimated to be valued at US$ 2.6 billion in 2026.

The increasing prevalence of rare genetic disorders and the growing demand for affordable diagnostic solution is expected to drive the global market.

North America is the leading regional market, commanding ~42% of global revenue in 2025.

Growth opportunities include expanding cancer diagnostics, rare disease detection, precision medicine adoption, AI-driven analysis, and emerging market healthcare investments.

CD Genomics, Eurofins Genomics, Illumina, Inc., Integrated DNA Technologies, Inc., Caris Life Sciences, Thermo Fisher Scientific Inc., and Laboratory Corporation of America® Holdings are a few leading players.