- Biotechnology

- Whole Genome Sequencing Market

Whole Genome Sequencing Market Size, Share, and Growth Forecast 2026 - 2033

Whole Genome Sequencing Market by Product (Instruments, Consumables, Services), by Sequencing Type (Large Whole Genome Sequencing, Small Whole Genome Sequencing), by End User (Pre-sequencing, Sequencing, Data Analysis), by Regional Analysis, from 2026 to 2033

Whole Genome Sequencing Market Share and Trends Analysis

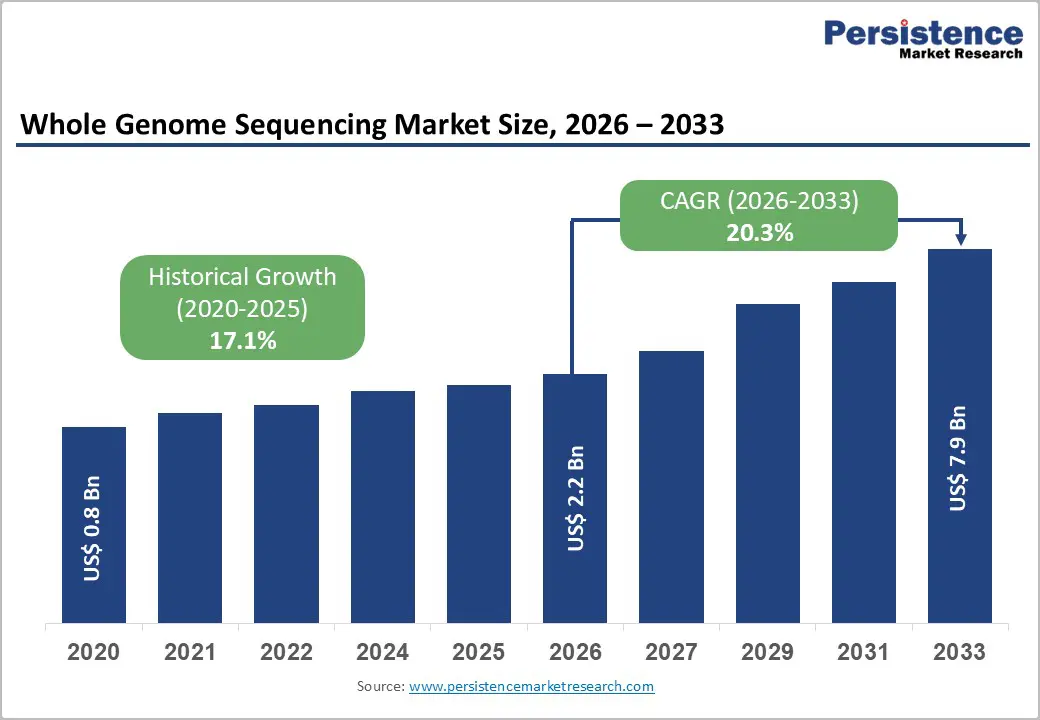

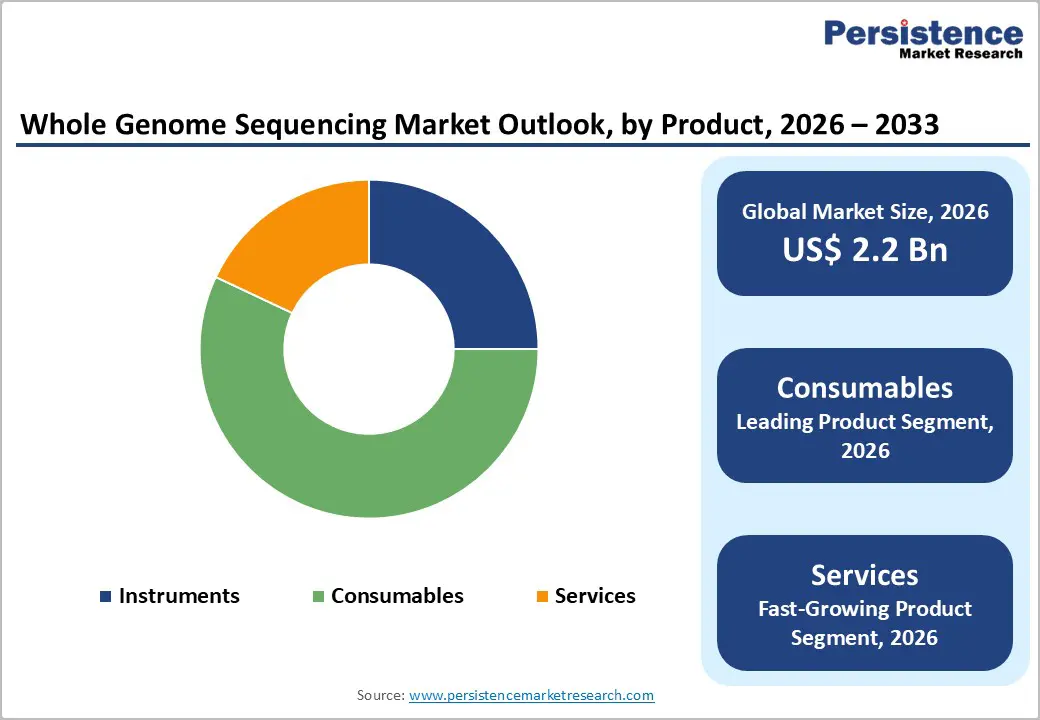

The whole genome sequencing market size is expected to be valued at US$ 2.2 billion in 2026 and projected to reach US$ 7.9 billion by 2033, growing at a CAGR of 20.3% between 2026 and 2033.

Whole Genome Sequencing (WGS) is a cutting-edge genomic technology that determines the complete DNA sequence of an organism's genome, encompassing all ~3 billion base pairs in the human genome, including both protein-coding genes (exons) and non-coding regions (introns and regulatory elements). Unlike targeted sequencing or whole-exome sequencing (which focus only on specific genes or coding regions), WGS provides the most comprehensive and unbiased view of an individual's genetic makeup.

In healthcare, WGS drives precision medicine, rare disease diagnosis, oncology, pharmacogenomics, and population health initiatives. It also supports research in infectious disease surveillance, agriculture, and evolutionary biology. The global whole genome sequencing market is experiencing robust growth, fueled by technological advancements, declining costs, rising adoption in clinical diagnostics, and expanding applications in personalized medicine. WGS represents a transformative tool unlocking deeper insights into human health, disease mechanisms, and tailored therapeutic strategies.

Key Industry Highlights:

- The increasing prevalence of genetic disorders and cancer mutations is one of the prime driving elements for the market.

- Improvements in early detection and treatment are crucial to the market’s growth.

- The increasing adoption of whole-genome sequencing in precision medicine is driving market revenue.

- WGS is finding broader applications in clinical diagnostics, including the detection of rare genetic disorders, congenital diseases, and prenatal screening.

- The large whole-genome sequencing segment held the largest market share by sequencing type.

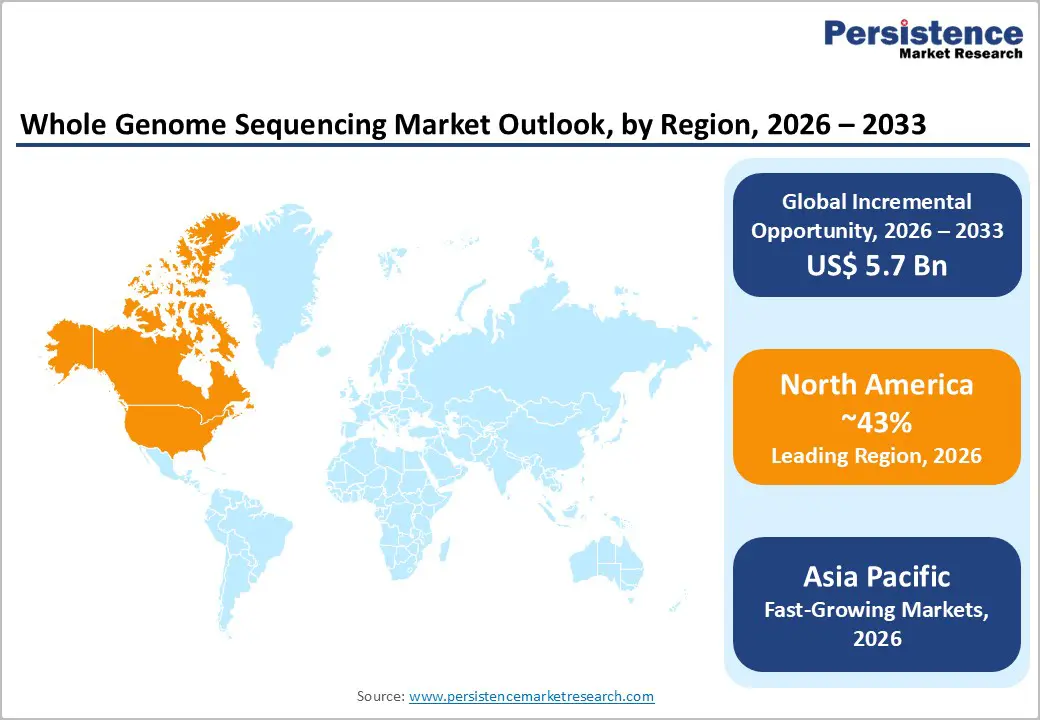

- North America accounts for the largest share of the whole-genome sequencing market.

- There is a growing trend toward integrating WGS data with other omics data to gain a more comprehensive understanding of complex biological systems and diseases.

| Key Insights | Details |

|---|---|

| Whole Genome Sequencing Market Size (2026E) | US$ 2.2 billion |

| Market Value Forecast (2033F) | US$ 7.9 billion |

| Projected Growth CAGR (2026 - 2033) | 20.3% |

| Historical Market Growth (2020 - 2025) | 17.1% |

Market Dynamics

Driver - Expanding Applications in Precision Medicine

Expanding applications of WGS in precision medicine significantly contribute to its market growth. Precision medicine tailors treatment plans to individual genetic profiles, offering more effective and personalized healthcare solutions. WGS enables the identification of genetic mutations and variants associated with various diseases guiding the selection of targeted therapies. In oncology, for instance, WGS helps identify specific genetic alterations in tumors allowing for personalized treatment strategies that improve patient outcomes. WGS is increasingly used in diagnosing rare genetic disorders such as prenatal screening, and pharmacogenomics where understanding an individual's genetic makeup can predict their response to drugs. As the medical community and regulatory bodies increasingly recognize the value of genomic data in improving healthcare outcomes, the adoption of WGS in clinical practice is set to rise propelling market growth.

Technological Advancements

Technological advancements are a primary driver of growth in the whole genome sequencing (WGS) market. Innovations in next-generation sequencing (NGS) technologies have drastically reduced the cost and time required for sequencing a human genome. For instance, the cost of sequencing a genome has dropped from nearly $100 million in the early 2000s to below $1,000 by 2023, making WGS accessible to a broad range of researchers and clinical applications.

Advancements in bioinformatics tools have improved the accuracy and efficiency of data analysis, allowing for more comprehensive and meaningful interpretations of genomic data. As sequencing technology continues to evolve with new platforms offering higher throughput and better accuracy, the barriers to entry lower further, driving market growth.

Government and Private Sector Investment

Substantial investments from governments and the private sector are key drivers of growth in the WGS market. Governments worldwide are funding large-scale genomic projects aimed at advancing medical research and public health. For example, initiatives like the UK Biobank and the U.S. National Institutes of Health's All of Us Research Program aim to sequence large populations to understand the genetic basis of diseases better and develop new treatments. Private sector investments are fuelling innovation and commercialization of WGS technologies. Companies like Illumina, Thermo Fisher Scientific, and others are investing heavily in research and development to enhance their sequencing platforms and expand their applications.

Venture capital funding in genomics startups is on the rise supporting the development of novel technologies and services. This influx of capital is accelerating technological advancements, expanding market reach and fostering collaborations that drive the growth of the WGS market.

Restraints - High Costs and Accessibility Issues

Whole genome sequencing (WGS) remains expensive compared to other diagnostic methods despite significant cost reductions over the years. The upfront costs of sequencing equipment, coupled with the need for advanced bioinformatics tools and skilled personnel to analyse and interpret the data present financial barriers. Small research institutions and healthcare providers, especially in low- and middle-income countries often find it challenging to afford these expenses.

The ongoing costs of maintaining and updating sequencing technologies and databases can strain budgets. Accessibility issues also arise in terms of infrastructure and training, as many regions lack the necessary resources to implement and utilize WGS effectively. These financial and logistical challenges can hinder the widespread adoption of WGS, particularly in resource-limited settings, restraining market growth.

Data Privacy and Ethical Concerns

The use of WGS raises significant data privacy and ethical concerns that can impede market growth. Sequencing an individual's entire genome generates vast amounts of sensitive genetic information, which, if mishandled, could lead to privacy breaches and potential misuse. There is a growing apprehension among the public regarding the storage, sharing, and potential exploitation of their genetic data by third parties including insurers and employers. Moreover, ethical dilemmas arise regarding informed consent, particularly when sequencing is performed on vulnerable populations such as minors or individuals unable to provide informed consent.

The fear of genetic discrimination and the potential misuse of genetic information can lead to resistance from patients and slow the adoption of WGS in clinical settings. Addressing these privacy and ethical issues requires robust regulatory frameworks and clear guidelines, which are still evolving, thereby posing a restraint on the market's growth.

Opportunity - Integration with Artificial Intelligence and Machine Learning

The integration of artificial intelligence (AI) and machine learning (ML) with whole genome sequencing (WGS) presents a significant growth opportunity for the market. AI and ML can vastly enhance the capabilities of WGS by automating and refining the analysis of complex genomic data. These technologies can help in identifying patterns and correlations that may not be apparent through traditional methods leading to new insights into genetic variations and their associations with diseases. For instance, AI algorithms can rapidly process and analyse large datasets, identifying genetic mutations and predicting their potential impact on health. This capability is particularly valuable in personalized medicine, where understanding the genetic basis of an individual's disease can lead to more targeted and effective treatment strategies.

AI-driven analytics can also improve the accuracy of variant calling, reducing false positives and false negatives, which are critical for clinical applications where precision is paramount. Also, AI and ML can facilitate the development of predictive models for disease risk assessment and drug response enabling proactive healthcare management. AI can provide comprehensive insights into an individual's health trajectory by integrating genomic data with other health data (e.g., electronic health records, lifestyle information). This holistic approach can significantly enhance patient outcomes and reduce healthcare costs, making WGS a more attractive option for healthcare providers.

The synergy between AI and WGS can accelerate research in genomics by enabling high-throughput analysis of genetic data, thus expediting the discovery of novel biomarkers and therapeutic targets. This can drive innovation in drug development and precision therapies, opening new avenues for treatment and prevention of complex diseases. As AI and ML technologies continue to advance, their integration with WGS will likely lead to more efficient, accurate, and scalable genomic analyses propelling the market forward. This confluence of cutting-edge technologies holds the promise of transforming healthcare and unlocking new potentials in genomics positioning the WGS market for significant growth.

Category-wise Analysis

By Product Insights

The whole genome sequencing market is classified into instruments, consumables and services based on product where the consumables segment dominates the market. Consumables such as reagents and assay kits are used repeatedly in sequencing procedures, leading to continuous demand.

As sequencing technologies evolve, they require specialized consumables compatible with new processes consequently drives the need for customized products. Also, the growing emphasis on genomics research and personalized medicine increases the demand for sequencing consumables. The increasing prevalence of genetic diseases necessitates more genetic testing and profiling further boosting the demand for consumables.

By Sequencing Type Insights

The whole genome sequencing market is further sub-segmented into large whole genome sequencing and small whole genome sequencing based on type. Among these segments, large-scale whole genome sequencing dominated the market in 2023 with a significant share of 77% due to its advantages. These advantages include a detailed examination of the genome at the individual base level and the capability to detect disease-causing alleles in extensive genomes that may go unnoticed with other approaches.

The method is typically used to detect prevalent genetic differences in the population, analyse tumours, determine the source of disorders, and choose animals and plants for agricultural breeding. The Okinawa Institute of Science and Technology (OIST) in Japan uses the NovaSeq 6000 device, a high-capacity whole genome sequencing device to explore the evolutionary genomics of different ocean species and chordates.

Region-wise Insights

North America Whole Genome Sequencing Market Trends

North America plays a central role in advancing the whole genome sequencing market, accounting for roughly 43% of global revenue in 2025. The region benefits from a highly developed research ecosystem supported by leading universities, genomic institutes, biotechnology firms, and pharmaceutical companies. Continuous innovation in sequencing platforms, bioinformatics tools, and automation systems has accelerated clinical and research adoption. Strong government backing through public funding programs further stimulates large-scale genomic studies, rare-disease research, and national precision-medicine initiatives.

The prevalence of inherited disorders also reinforces demand for comprehensive sequencing approaches. In the United States, the Down syndrome affects approximately one in every 707 newborns, translating to more than five thousand cases annually. Such statistics emphasize the importance of genome-wide screening for early diagnosis, carrier detection, and individualized treatment planning. Hospitals and diagnostic laboratories increasingly integrate whole genome sequencing into clinical workflows, sustaining regional market leadership.

Asia Pacific Whole Genome Sequencing Market Trends

Asia Pacific is projected to register the fastest growth in the whole genome sequencing market, driven by rising healthcare investment, expanding biotechnology sectors, and supportive government policies. Countries across the region are strengthening genomic research infrastructure through funding programs, public-private partnerships, and national precision-medicine initiatives. Growing demand for infectious-disease surveillance, oncology research, and rare-disease diagnostics is further accelerating adoption of large-scale sequencing platforms.

Government involvement has played a direct role in expanding sequencing capacity. In India, authorities approved multiple laboratories including Eurofins Genomics India, Genotypic Technologies, Strand Life Sciences, Neuberg Supratech Reference Labs, and CARINGdx to conduct genome sequencing for SARS-CoV-2 surveillance. Such initiatives highlight regional commitment to genomic preparedness and diagnostics. As laboratory networks expand and sequencing costs gradually decline, Asia Pacific is expected to become a major contributor to global whole genome sequencing revenues over the forecast period.

Competitive Landscape

The whole genome sequencing market features a competitive environment dominated by global life-science companies and specialized genomics technology providers. Firms are commonly assessed on the breadth of their sequencing platforms, consumables, software capabilities, financial performance, recent product launches, and geographic presence. Market position is further influenced by regulatory approvals, service networks, and adoption across clinical and research laboratories.

Leading players actively pursue strategic collaborations with hospitals, academic centers, and pharmaceutical companies to expand customer bases and accelerate technology deployment. Mergers and acquisitions are frequently used to gain access to novel chemistries, automation systems, and bioinformatics tools. Geographic expansion through new facilities and distribution partnerships also remains a core strategy for strengthening competitive advantage.

Key Industry Developments:

- In September 2025, Oxford Nanopore Technologies, known for its nanopore-based molecular sensing platforms introduced a 24-hour whole genome sequencing workflow from blood samples, delivering rapid, information-dense results and enabling true end-to-end sample-to-answer analysis within a single day.

- In September 2023, Illumina NovaSeq X, launched a high-throughput sequencing system that has been highly successful, with 390 orders received in 2023.

- In July 2022, QIAGEN N.V. and Sysmex Corporation formed a partnership to develop jointly and market cancer companion diagnostics worldwide, utilizing next-generation sequencing (NGS) and genomic technologies.

Companies Covered in Whole Genome Sequencing Market

- Thermo Fisher Scientific, Inc

- Danaher Corporation

- Illumina, Inc

- QIAGEN N.V.

- Merck KGaA

- Eurofins Scientific

- Siemens Healthineers

- Macrogens, Inc

- Bio-Rad Laboratories, Inc

- Agilent Technologies, Inc

- F. Hoffmann-La Roche Ltd.

- Others

Frequently Asked Questions

The global whole genome sequencing market is projected to be valued at US$ 2.2 Bn in 2026.

The expanding applications in precision medicine are one of the key drivers for market growth.

The global market is expected to witness a CAGR of 20.3% between 2026 and 2033.

Key opportunities include clinical diagnostics expansion, oncology applications growth, newborn screening adoption, declining sequencing costs, and population-genomics programs worldwide.

North America is the leading region in the global whole genome sequencing market.