- Food Packaging

- Western Europe Premade Pouch Packaging Market

Western Europe Premade Pouch Packaging Market

Western Europe Premade Pouch Packaging Market by Material Type (Plastic, Paper, Others), Closure Type (Tear Notch, Spout, Others), End-use Industry, and Analysis for 2026 - 2033

Western Europe Premade Pouch Packaging Market Trends and Analysis

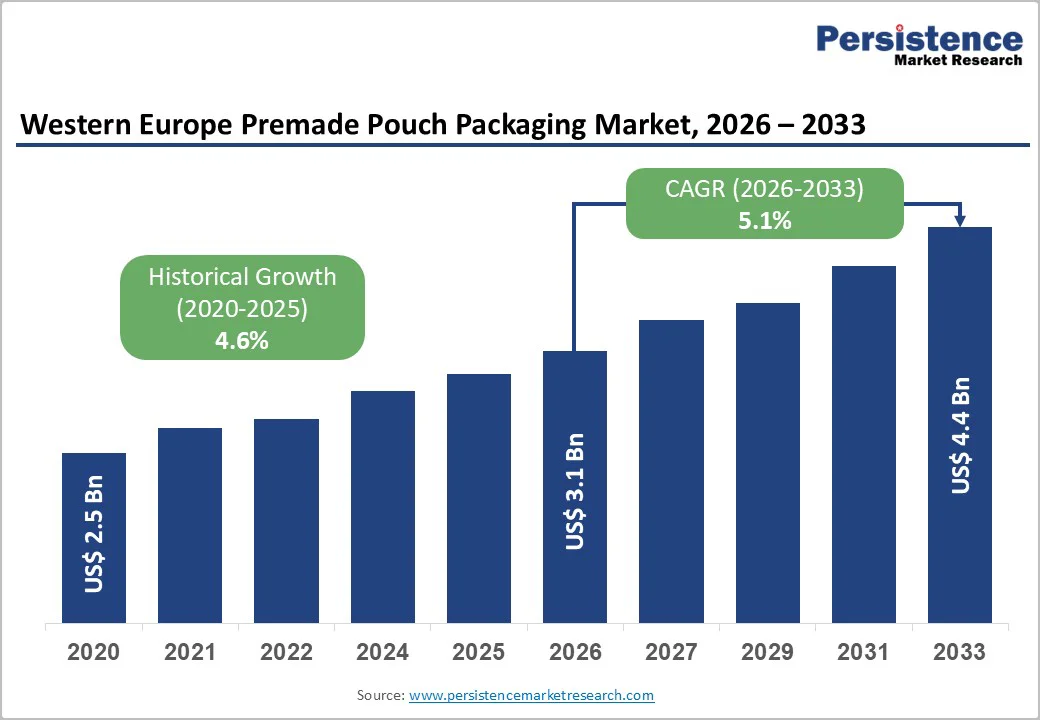

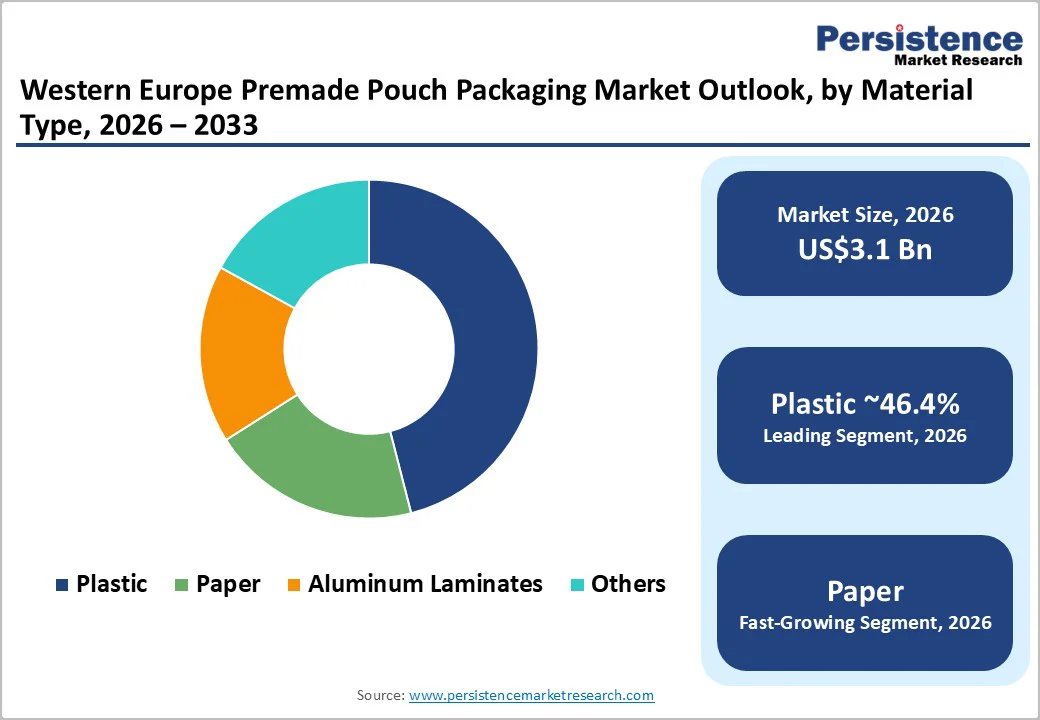

The Western Europe premade pouch packaging market size is likely to be valued at US$3.1 billion in 2026 and is expected to reach US$4.4 billion by 2033, growing at a CAGR of 5.1% during the forecast period from 2026 to 2033, driven by strong demand from food, beverage, pet food, and personal care applications.

Premade pouches are gaining widespread adoption due to their convenience, strong shelf appeal, material efficiency, and compatibility with high-speed filling lines. Demand is shaped by consumer preferences for portion control, resealability, and visually distinctive packaging, while regulatory pressure to reduce waste and improve recyclability is driving material and structural innovation. Continued growth in packaged and ready-to-consume foods, especially in urban households, remains a key driver supporting demand for flexible, lightweight packaging solutions.

Key Industry Highlights

- Investment Plans: Packaging converters across Western Europe are increasingly investing in recyclable mono-material films, digital printing lines, and spouted pouch technologies, with sustainability-focused capital expenditure accounting for more than 35% of recent packaging innovation investments.

- Dominant Material Type: Plastic premade pouches are anticipated to dominate with a 46.4% revenue share in 2026, supported by superior barrier properties, lightweight structure, and compatibility with high-speed filling and printing technologies.

- Leading Closure Type: Tear-notch closures are estimated to lead the market with a 43.6% revenue share in 2026, driven by their low complexity, ease of opening, and widespread use in snacks, dry foods, and single-serve applications.

| Key Insights | Details |

|---|---|

| Western Europe Premade Pouch Packaging Market Size (2026E) | US$3.1 Bn |

| Market Value Forecast (2033F) | US$4.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory-Driven Sustainable Packaging Adoption & Mono-Material Film Integration

A core driver in Western Europe is the regulatory push toward recyclable, mono-material flexible packaging formats, which has accelerated the adoption of premade pouches that meet evolving EU circular economy mandates. Under frameworks such as the EU Packaging and Packaging Waste Directive and Single-Use Plastics Directive, brands are compelled to shift from traditional multi-layer laminates to recyclable mono-material films, driving demand for advanced premade pouches that reduce complexity in recycling streams. This regulatory alignment enhances both compliance and brand sustainability credentials, particularly for food and personal care producers seeking to demonstrate eco-conscious packaging commitments while simplifying end-of-life processing.

Premium On-the-Go Food & E-commerce-Optimized Flexible Packaging Demand

Another critical driver is the escalating demand for convenience-centric premade pouch formats optimized for on-the-go lifestyles and ecommerce distribution. Urban European consumers increasingly prioritize resealable, lightweight pouches with high barrier properties that support longer shelf life, portability, and minimal transit damage, a trend amplified by the growth of DTC (direct-to-consumer) food and personal care brands.

For example, several Western European snack and functional beverage producers have introduced high-barrier transparent premade pouches with tear notches and spouts to appeal to quality-seeking, health-focused buyers, reinforcing packaging differentiation in a crowded market. In Germany and France, major food brands have transitioned to recyclable premade pouches with advanced barrier films and resealable closures, enabling compliance with stricter packaging waste targets while boosting shelf-life performance for snacks and ready-to-eat meals. These drivers go beyond generic packaging growth themes by focusing on regulatory compliance with EU sustainability frameworks and functional, consumer-led pouch design trends that uniquely propel the premade pouch segment in Western Europe.

Barrier Analysis - Recyclability Challenges of Multi-Layer Laminate Structures

Despite steady growth, the Western Europe premade pouch packaging market confronts multi-layer laminate recyclability constraints that limit adoption beyond core food categories. Many premade pouches rely on complex film structures that combine PET, PE, PA, and aluminum to achieve high-barrier performance. Still, this material complexity makes them difficult to process through existing recycling systems and reduces closed-loop recovery rates. This limited recyclability of multi-material flexible films can suppress demand from sustainability-sensitive brands and conscious consumers who increasingly prefer chemically recyclable or mono-material packaging formats, even when performance trade-offs exist.

Supply Chain and Technological Barriers for High-Performance Premade Pouches

Restraint stems from specialized supply chain dependencies for high-performance barrier films and niche printing technologies required for premium premade pouch formats. The availability and lead times of barrier films and custom digital printing materials remain inconsistent across Western Europe, pressuring manufacturers to maintain larger inventories and complicating production scheduling. Smaller converters and regional producers often struggle with access to equipment and technical expertise for advanced sealing and high-resolution digital pouch printing, limiting their ability to compete with larger, vertically integrated firms and slowing the diffusion of innovation across the broader market.

Opportunity Analysis - Recyclable Mono-Material & High-Barrier Bio-Based Premium Pouch Innovations

Western Europe’s premade pouch packaging market presents a strong opportunity in recyclable mono-material flexible pouch formats and high-barrier bio-based films tailored for premium food and beverage lines. As converters innovate with recyclable PP/PE mono-structures and biodegradable lamination alternatives, brands can differentiate through packaging that meets both sustainability and performance demands without compromising barrier functions for sensitive goods. This trend creates high-value niches in organic snacks, artisanal beverages, and clean-label consumer goods that leverage advanced material science to boost shelf life and brand sustainability credentials. For example, Südpack’s certified recyclable and compostable high-barrier pouch optimized for hot-fill food applications exemplifies how niche material innovation can unlock new premium segments in Western Europe’s food packaging space.

E-Commerce Optimized & Customized Digital Print Premade Pouch Solutions

Rapid growth in e-commerce, optimized premade pouch formats with digital print customization and interactive branding features, presents a unique growth frontier in Western Europe. As online retail and DTC food, cosmetic, and health-supplement brands seek lightweight, tamper-proof, and visually distinctive pouch packaging scalable for small batch runs, demand for digitally printed, bespoke premade pouches is rising. Enhanced packaging, including QR code integration, high-resolution graphics, and on-package storytelling, boosts shelf appeal in both online and retail environments. This opportunity is particularly strong for converters offering short-run digital printing and tailored pouch formats that align with rapid product launches and seasonal promotions.

Category-wise Analysis

Material Type Insights

Plastic materials hold a leadership position, anticipated to account for approximately 46.4% of revenue share in 2026. This dominance stems from plastic’s versatile performance profile, providing robust barrier protection against moisture, oxygen, and contaminants, essential for preserving shelf life and quality across food, beverage, and personal care applications. Plastic films, particularly polyethylene (PE) and polypropylene (PP), are readily heat-sealable and compatible with high-speed automated production, reducing unit costs and supporting large-scale operations.

Their lightweight nature lowers transportation and logistics costs, a significant advantage in cost-sensitive European supply chains. Furthermore, plastics are highly adaptable to advanced printing and pouch design innovations, enabling striking brand visuals and functional enhancements such as resealability and ergonomic shaping, which boost consumer appeal across retail and online channels.

Paper-based premade pouch materials are emerging as the fastest-growing segment, driven by intensifying consumer demand for sustainable packaging and circular design preferences. As brands respond to environmental expectations, paper substrates, especially those with innovative barrier coatings or recyclable paper composites, are gaining traction where conventional multi-layer plastics face scrutiny.

Although paper alone historically offered weaker moisture and oxygen barriers, coated paper systems now deliver competitive protective performance while enabling easier recyclability and lower environmental impact at end-of-life, crucial for meeting evolving sustainability goals. The growth of paper pouches is particularly strong in organic foods, craft snacks, and specialty consumer goods, where eco-friendly positioning increases shelf differentiation and resonates with eco-conscious buyers. This transition is supported by advancements in fiber-based packaging that align with circular economy trends without significantly compromising barrier functionality. European artisanal coffee roasters are increasingly using paper pouches with high-barrier inner linings to maintain freshness while appealing to sustainability-focused consumers, illustrating how niche material innovation can unlock premium market segments.

Closure Type Insights

The tear-notch closure type is expected to account for the largest share of approximately 43.6% in Western Europe’s premade pouch packaging market. Its popularity lies in exceptional consumer convenience: a tear notch clearly indicates where to open the package without scissors or tools, which enhances everyday usability, especially in single-serve and on-the-go categories. This closure is widely adopted across snack foods, dried fruit, powdered supplements, pet treats, and other fast-moving consumer goods where quick, intuitive access to the product is a priority.

The tear notch’s simple design also integrates seamlessly with flexible pouch structures, maintains barrier integrity until opening, and keeps manufacturing complexity low relative to reclosable systems. Manufacturers increasingly deploy tear notches alongside resealable features such as zippers, balancing ease of first access with long-term freshness retention, which further reinforces its prominence across diverse product lines.

Spout closures are likely to be the fastest-growing segment in the closure type category, propelled by rising demand for liquid and semi-liquid packaging formats in Western Europe. The spout feature enables controlled pouring and dispensing, reducing spillages and waste while enhancing user experience for products such as juices, functional drinks, sauces, baby foods, and liquid detergents. These closures are well-aligned with growth in on-the-go beverage consumption and refillable packaging trends, where precision and convenience outweigh the cost premium of more complex closure systems.

Spouts also support brand differentiation through ergonomic designs and cap customization, which appeals to performance-oriented buyers and premium product segments. As beverage and liquid food brands expand their flexible packaging portfolios to meet changing consumption occasions, spout closures are expected to sustain strong adoption and elevate the overall value of premade pouch offerings in the region. Functional beverage brands in Western Europe are increasingly launching products in spout-enabled premade pouches, allowing consumers to pour directly into reusable bottles or drink straight from the pack. This innovation boosts both convenience and sustainability credentials.

Competitive Landscape

The Western Europe premade pouch packaging market is moderately competitive, characterized by the presence of a few large multinational packaging converters alongside a broad base of regional and niche manufacturers. Leading players benefit from scale, advanced material capabilities, and long-standing relationships with major food and consumer goods brands, enabling them to secure high-volume contracts and maintain consistent quality standards across the region.

Mid-sized and specialized firms remain active by focusing on customization, shorter production runs, and application-specific pouch solutions. These players compete effectively in premium, organic, and specialty product segments where flexibility, speed, and tailored packaging designs are valued. As a result, competition is driven by innovation, sustainability alignment, and service differentiation rather than price alone, keeping the market dynamic and balanced.

Key Industry Developments

- In April 2025, Mondi Group collaborated with Evonik Industries to launch a lightweight recyclable paper pouch innovation for fumed silica applications, reducing packaging weight by ~30% and advancing circular economy packaging solutions in Europe’s flexible packaging sector.

- In February 2025, Mondi Group signed a partnership with Proquimia to introduce paper-based stand-up pouches for dishwashing products in Iberia, reflecting rising demand for sustainable, high-performance pouch formats in Western European household goods markets.

Companies Covered in Western Europe Premade Pouch Packaging Market

- Amcor plc

- Mondi Group

- Berry Global Inc.

- Sonoco Products Company

- Sealed Air Corporation

- Constantia Flexibles Group

- Huhtamaki Oyj

- Smurfit Kappa Group

- ProAmpac LLC

- Glenroy Inc.

- Coveris Holdings S.A.

- Clondalkin Group

- Swiss Pack

- ePac Flexible Packaging

- Omag-Pack

- FFP Packaging Solutions

- Tyler Packaging

- Pouches.co.uk

Frequently Asked Questions

The Western Europe premade pouch packaging market is estimated to be valued at US$3.1 billion in 2026.

By 2033, the Western Europe premade pouch packaging market is projected to reach US$4.4 billion.

Key trends include rising adoption of recyclable mono-material pouches, growth of spouted pouches for liquid and functional beverages, increased use of digital printing for customization, and demand for lightweight, shelf-ready flexible packaging.

By material type, plastic premade pouches lead the market with about 46.4% share, while tear notch closures dominate the closure segment with nearly 43.6% share, driven by ease of use and wide applicability.

The Western Europe premade pouch packaging market is expected to grow at a CAGR of 5.1% from 2026 to 2033.

Major players include Amcor plc, Mondi Group, Huhtamaki Oyj, Constantia Flexibles, and ProAmpac.