- Specialty & Fine Chemicals

- Triethylene Glycol Market

Triethylene Glycol Market Size, Share, and Growth Forecast, 2026 - 2033

Triethylene Glycol Market By Application (Natural Gas Dehydration, Solvents, Plasticizers, Humectants, Polyester Resins, Others), End-user (Oil & Gas, Automotive, Textile, Construction, Others), and Regional Analysis for 2026 - 2033

Triethylene Glycol Market Size and Trends Analysis

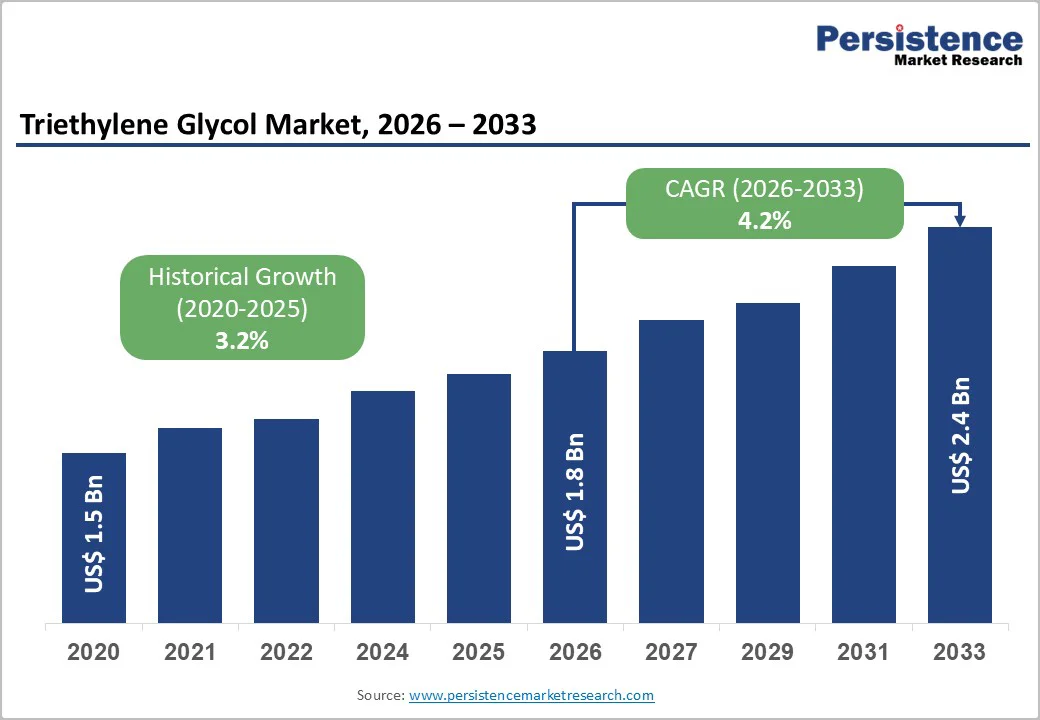

The global triethylene glycol market size is likely to be valued at US$1.8 billion in 2026, and is expected to reach US$2.4 billion by 2033, growing at a CAGR of 4.2% during the forecast period from 2026 to 2033, driven by the increasing prevalence of natural gas processing demands, rising need for moisture-absorbing solvents in oil & gas, and advancements in polyester resin formulations. Rising demand for non-toxic triethylene glycol in automotive and textiles, coupled with improved humectant and plasticizer grades and its role in energy-efficient processes, is driving market growth.

Key Industry Highlights:

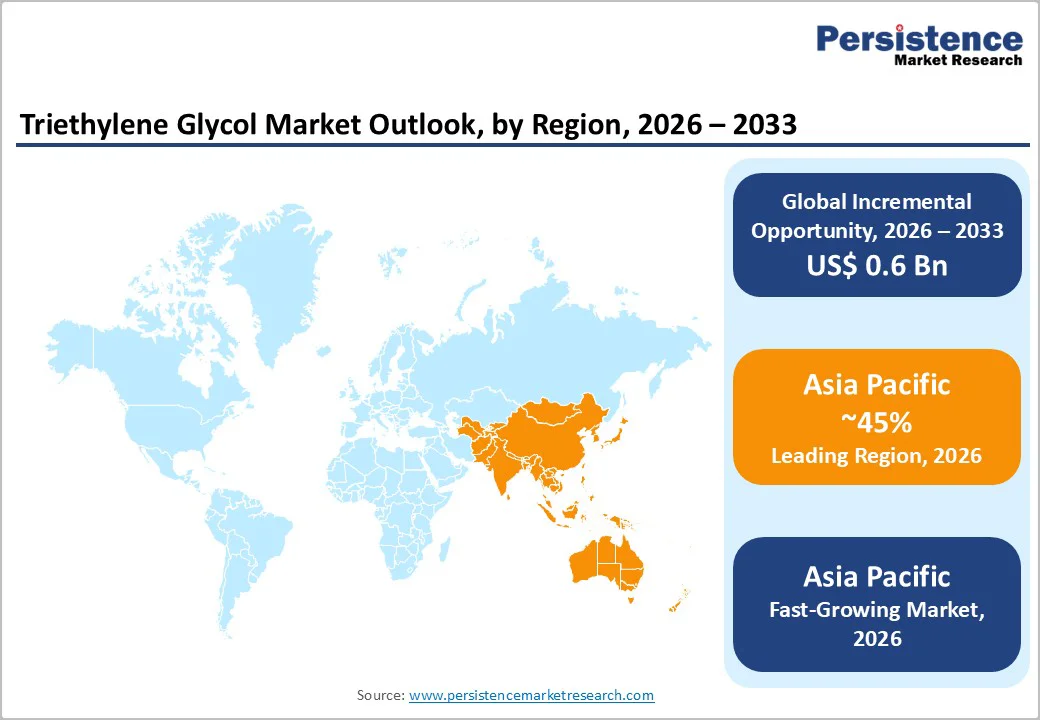

- Leading Region: Asia Pacific, anticipated to lead, account for a 45% market share in 2026, driven by booming shale gas projects, high textile output, and strong chemical manufacturing in China and India.

- Fastest-growing Region: Asia Pacific, fueled by LNG expansions, rising awareness of glycol-based dehumidification, and growing investments in automotive coatings in Southeast Asia.

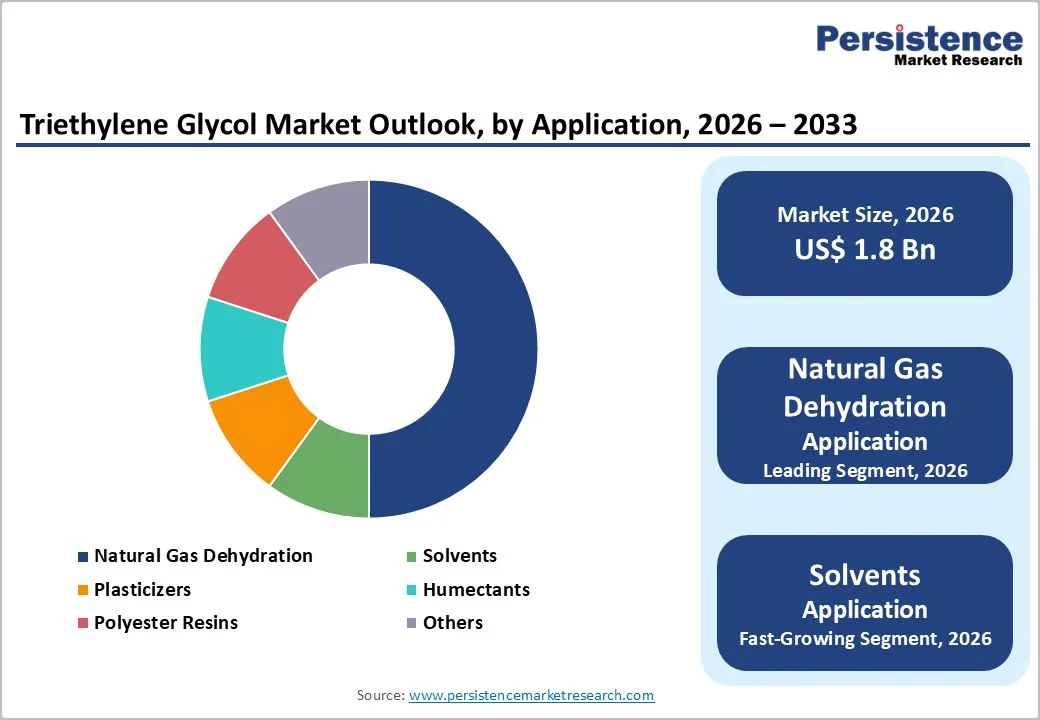

- Dominant Application: Natural gas dehydration, to hold approximately 50% of the market share, as it generates strong, efficient moisture removal by closely mimicking absorption processes.

- Leading End-user: Oil & gas to account for over 55% of the market revenue, due to pipeline integrity needs, extraction surges, and widespread use in gas sweetening.

| Key Insights | Details |

|---|---|

|

Triethylene Glycol Market Size (2026E) |

US$1.8 Bn |

|

Market Value Forecast (2033F) |

US$2.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Natural Gas Processing Demands and Demand for Moisture-Absorbing Solvents

The growing demand for natural gas processing presents a significant opportunity for glycol suppliers, driven by the industry’s need for dry, contaminant-free feeds and optimized pipeline flow. Traditional absorbents often cause hydrate blockages, particularly in offshore pipelines, resulting in shutdowns and efficiency losses. Advanced solvent technologies, including triethylene glycol dehydration units, plasticizer blends, humectant formulations, resin catalysts, and purified grades, provide a hygroscopic, low-volatility solution. These systems simplify regeneration, reduce the need for multiple cycles, and perform effectively during peak production or LNG liquefaction, where rapid drying is essential.

Triethylene glycol also mitigates corrosion, lowers freezing points, and minimizes impurity carryover, addressing critical concerns in energy operations. Its improved recyclability and ease of handling make it suitable for high-pressure and remote applications, including natural gas and polyester production. With global energy organizations emphasizing higher throughput and user-friendly chemicals, demand continues to grow across oil & gas, automotive, and construction sectors.

High Development and Purification Costs

High development and purification costs pose a major challenge for companies advancing next-generation triethylene glycol and innovative solvent systems. Creating specialized grades, such as ultra-pure dehydration fluids, plasticizer-enhanced resins, or humectant concentrates, demands extensive research, advanced distillation, and hydrogenation processes, which are significantly more expensive than diethylene glycol alternatives. Achieving high purity is particularly difficult, as many refined variants, oxygen-reduced batches, and stabilizer-blended products are highly sensitive to oxidation, temperature, and moisture, requiring careful optimization to maintain performance during storage and application.

Meeting industry specifications often involves costly fractionation trials, sophisticated GC testing, and the use of high-grade inhibitors, all of which increase R&D expenditures. Compliance with stringent regulatory requirements, covering VOC limits, flash points, and batch consistency, necessitates multiple stability studies across diverse conditions and production batches, adding both time and cost. Scaling up production further requires controlled reactors, specialized columns, and robust quality-assurance systems, driving overall costs higher. For smaller refiners, these complexities can restrict product portfolio expansion or delay market entry.

Advancements in Bio-Based and High-Purity Delivery Platforms

Advances in bio-derived and high-purity triethylene glycol delivery systems are reshaping the global energy sector by tackling two critical challenges: fossil fuel dependence and contamination risks. Bio-based triethylene glycol, designed with up to 50% renewable content, reduces reliance on petroleum and enables carbon-neutral dehydration in gas processing plants. Innovations such as enzymatic synthesis, catalytic upgrading, oligomer separation, and hybrid blending improve yields, minimize impurities, and lower lifecycle costs for operators and sustainability initiatives.

High-purity platforms, including solvent-grade liquids, resin precursors, humectant gels, and catalyst supports, enhance absorption efficiency by increasing molecular hygroscopicity, the process’s first line of defense against hydrates and corrosion. These advanced formats prevent off-spec products, boost throughput, and enable automated dosing without the need for specialized chemists, making them ideal for large-scale field operations. Emerging technologies such as nano-filtered glycols, mucoadhesive polymers, and VLP-based absorbers further improve capture efficiency and regeneration performance.

Category-wise Analysis

Application Insights

Natural gas dehydration is expected to lead the market, capturing around 50% of the market share in 2026. Its prominence is driven by strong absorption efficiency, cost-effectiveness, and scalability, making it the preferred choice for LNG preprocessing. Glycol-based dehydration provides hydrate inhibition, ensures gas dryness, and supports flow assurance, making it ideal for large-scale extraction operations. For instance, at Shell’s Gbaran/Ubie gas processing facility in Nigeria, TEG dehydration is used in the absorption/regeneration loop to meet sales-gas specifications and prevent hydrate formation on export and processing lines. This approach is favored for its high-throughput cost-effectiveness, ability to achieve the required dry-gas dew point for liquefaction and sales, and its role in maintaining flow assurance over long export pipelines.

The solvents segment is the fastest-growing, driven by versatility and increasing use in polyester resins. Their solvency properties enable targeted dissolution and reduced residue formation. Advances in high-purity solvents are further enhancing performance and accelerating adoption, particularly in North America and Europe, where demand for clean, reactive fluids is rising. For example, solvent-based polyester resins account for approximately 30% of resin usage in automotive coatings due to their superior adhesion and finish quality.

End-user Insights

The oil & gas sector is expected to lead the market, accounting for roughly 55% of the share in 2026, driven by pipeline requirements, large-scale field operations, and strong global demand for dehydration agents. Its dominance continues as operators increasingly use glycols for gas sweetening and storage. The rising adoption of humectant aids and expanded construction projects underscores the growing focus on comprehensive protection. For instance, EPA guidelines on glycol dehydrators indicate that most oil and gas operations employ TEG to dry gas before it enters sales pipelines, preventing hydrate formation and ensuring uninterrupted flow.

The textile segment is projected to be the fastest-growing, fueled by robust fiber production and the expanding use of plasticizers in yarns. The shift toward flexible, dye-stable platforms with improved moisture retention is accelerating adoption. Innovations in resin-integrated glycols and pilot trials of solvent-based solutions are driving growth. For example, companies such as BASF provide intermediates and additives for the textile industry, including PolyTHF®, a key chemical for producing elastic spandex/elastane fibers used in apparel like swimwear, activewear, underwear, and stretch denim. While PolyTHF enhances fiber elasticity and durability, it is distinct from triethylene glycol.

Regional Insights

North America Triethylene Glycol Market Trends

North America is expected to account for nearly 30% of the triethylene glycol market in 2026, supported by the region’s advanced energy infrastructure, strong R&D capabilities, and high awareness of efficiency benefits. Dehydration systems across the U.S. and Canada ensure broad availability of triethylene glycol for oil & gas, automotive, and textile applications. Rising demand for convenient, easily regenerated solvent forms is further driving adoption by enhancing throughput and reducing challenges associated with batch processing.

Technological advancements in triethylene glycol, such as stable purities, optimized absorption delivery, and targeted impurity removal, are attracting significant investment from both public and private sectors. Government initiatives and clean energy programs continue to encourage its use to mitigate hydrate formation, corrosion, and emerging biofuel risks, sustaining market demand. Increasing adoption of plasticizer hybrids and construction resins, particularly in automotive and related applications, is expanding the scope of triethylene glycol’s end-use markets.

Europe Triethylene Glycol Market Trends

Europe’s triethylene glycol market is driven by rising awareness of dehydration benefits, robust processing infrastructure, and government-led sustainability initiatives. Countries such as Germany, France, and the U.K. have well-established chemical frameworks that support regular solvent use and encourage the adoption of innovative glycol delivery systems. These efficient formulations are especially attractive to oil & gas operators, cost-conscious industries, and construction users, enhancing yield and coverage rates.

Advances in triethylene glycol technology, such as improved recyclability, resin-targeted delivery, and enhanced bio-based grades, are further expanding market potential. European authorities are actively supporting research and trials to address both routine and specialized applications, reinforcing market confidence. The increasing focus on convenient, closed-loop solutions aligns with the region’s preventive chemistry and emissions-reduction goals. Public awareness campaigns and efficiency initiatives are extending reach across urban and rural areas, while suppliers continue investing in catalysts and high-purity formulations to boost performance.

Asia Pacific Triethylene Glycol Market Trends

Asia Pacific is projected to be both the largest and fastest-growing market, capturing a 45% share in 2026, driven by increasing processing awareness, government initiatives, and expanding application programs across the region. Countries such as India, China, Japan, and Southeast Asian nations are actively promoting chemical strategies to meet rising gas demands and emerging textile requirements. Triethylene glycol is particularly favored for its scalable application, ease of blending, and suitability for large-scale production in both urban and rural areas.

Technological advancements are enabling the development of stable, efficient, and easy-to-handle triethylene glycol, capable of withstanding challenging operational conditions while minimizing waste. These innovations are essential for servicing remote refineries and improving overall process efficiency. Growing demand from the natural gas, automotive, and construction sectors is further driving market expansion. Public-private partnerships, increased investment in chemical R&D, and enhanced manufacturing capacity are accelerating growth, while the convenience, improved absorption, and reduced inefficiency risks of triethylene glycol make it a preferred choice across the region.

Competitive Landscape

The global triethylene glycol market is dominated by large, vertically integrated chemical companies with strong feedstock access, advanced manufacturing capabilities, and extensive distribution networks. Dow and Exxon Mobil Corporation capitalize on their expansive petrochemical operations to deliver high-purity TEG for high-volume applications like natural gas dehydration and industrial solvents. BASF and Huntsman International LLC emphasize technical expertise and application-focused solutions, providing tailored grades and process efficiency enhancements for end users.

LyondellBasell Industries Holdings B.V. and SABIC enhance competitiveness through integrated production models that combine cost efficiency with wide geographic coverage, serving diverse energy and industrial markets. Eastman Chemical Company stands out through innovation and specialty chemical expertise, supplying TEG for performance-driven and value-added applications..

Key Industry Developments

- In August 2025, Dow and Huntsman launched a funded initiative to develop bio-based triethylene glycol with 40% renewable content, enhancing flexibility and sustainability for polyester textile applications.

- In May 2025, LyondellBasell reported that its humectant-grade triethylene glycol completed 500-ton pilot trials in India, showing comparable moisture retention to diethylene glycol and strong stability.

Companies Covered in Triethylene Glycol Market

- Dow

- Exxon Mobil Corporation.

- BASF

- Huntsman International LLC.

- LyondellBasell Industries Holdings B.V.

- SABIC

- Eastman Chemical Company

- India Glycols Limited

- LOTTE Chemical Corporation

- PTT Global Chemical Public Company Limited

- Muby Chem Private Limited

Frequently Asked Questions

The global triethylene glycol market is projected to reach US$1.8 billion in 2026.

The rising prevalence of natural gas processing demands and the demand for moisture-absorbing solvents are key drivers.

The triethylene glycol market is poised to witness a CAGR of 4.2% from 2026 to 2033.

Advancements in bio-based and high-purity delivery platforms are the key opportunities.

Dow, Exxon Mobil Corporation, BASF, Huntsman International LLC., and LyondellBasell Industries Holdings B.V. are the key players.