- Metals & Minerals

- Titanium Sponge Market

Titanium Sponge Market Size, Share, and Growth Forecast, 2026 - 2033

Titanium Sponge Market by Product Type (High Purity Sponge Titanium, Commercial Grade Sponge Titanium), End-user (Aerospace & Defense, Chemical, Industrial, Medical, Marine), and Regional Analysis for 2026 - 2033

Titanium Sponge Market Size and Trends Analysis

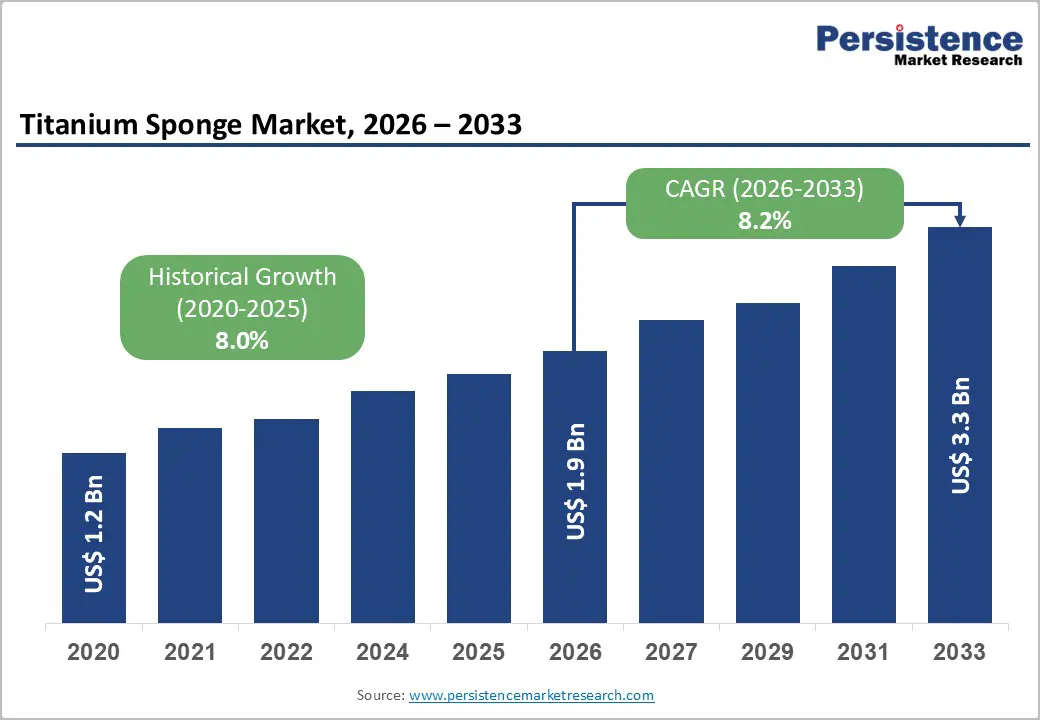

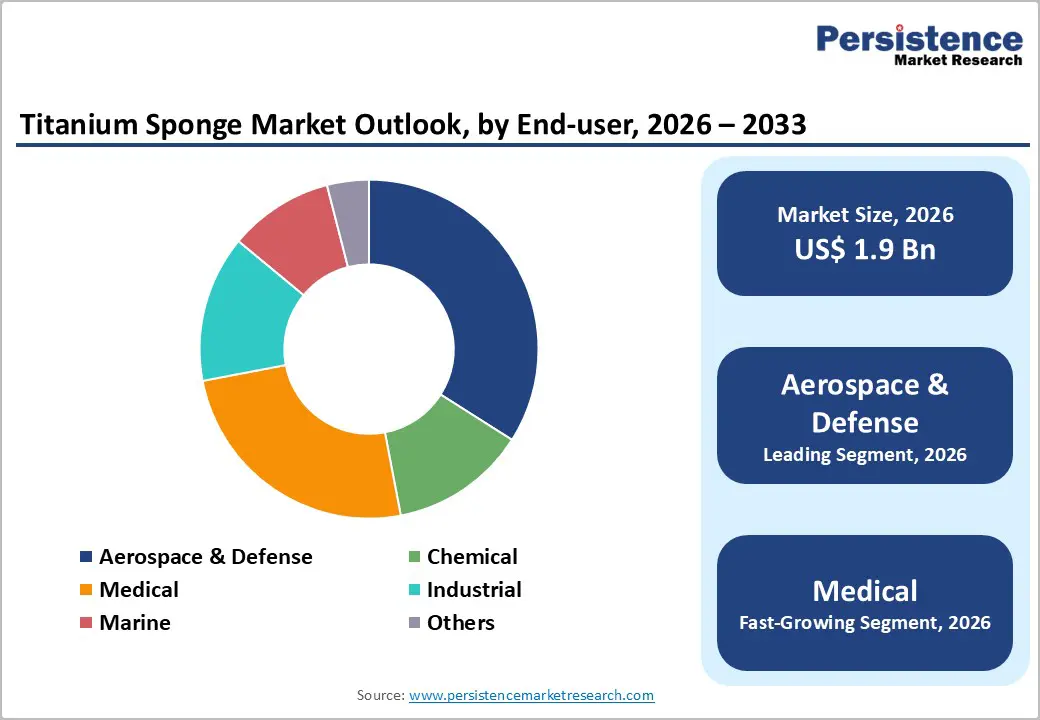

The global titanium sponge market size is likely to be valued at US$1.9 billion in 2026 and is expected to reach US$3.3 billion by 2033, growing at a CAGR of 8.2% during the forecast period from 2026 to 2033, driven by rising demand in the aerospace sector for lightweight, high-strength materials, which enhance fuel efficiency and performance in aircraft and defense applications.

The medical industry is driving demand for titanium through its expanding use in implants, surgical instruments, and biomedical devices, supported by its superior biocompatibility and corrosion resistance. Industrial sectors such as chemical processing, power generation, and marine applications are increasingly adopting titanium sponge for equipment that requires high durability and resistance to harsh environments. The post-pandemic recovery of commercial aviation, rising global defense expenditures, and growing investments in additive manufacturing and high-purity titanium applications are further strengthening market demand.

Key Industry Highlights:

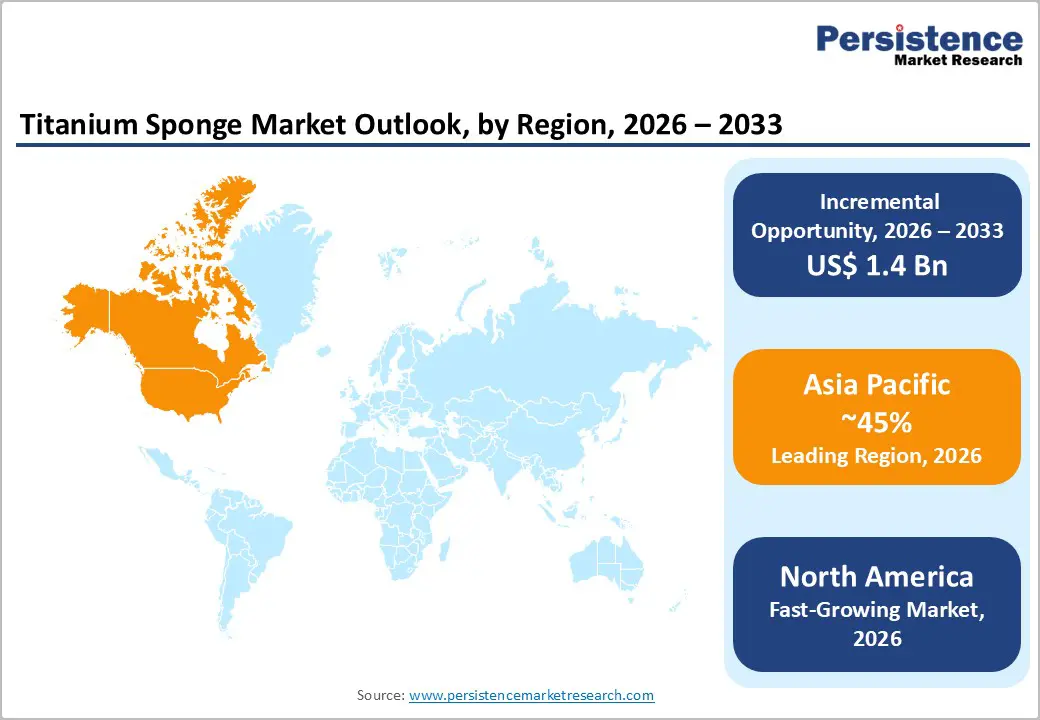

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for 45% market share in 2026, driven by rising aerospace demand, industrial growth, and expanding domestic titanium production.

- Fastest-growing Region: North America is likely to be the fastest-growing region in the titanium sponge market in 2026, supported by rising aerospace and defense demand, medical applications, and investments in domestic production and advanced manufacturing.

- Leading Product Type: The high-purity sponge titanium segment is projected to be the leading product type in 2026, accounting for 40% of revenue, driven by rising aerospace demand and medical applications requiring ultra-pure titanium.

- Leading End-user: The aerospace & defense segment is anticipated to be the leading end-user, accounting for over 50% of revenue in 2026, supported by rising aircraft production, defense modernization programs, and the growing use of lightweight, high-strength titanium materials.

| Key Insights | Details |

|---|---|

| Titanium Sponge Market Size (2026E) | US$1.9 Bn |

| Market Value Forecast (2033F) | US$3.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand from the Aerospace & Defense Sector

Titanium sponge is the primary feedstock for producing titanium alloys, which are extensively used in aircraft structures, jet engines, landing gear, fasteners, and other critical components. As commercial aviation continues to recover and aircraft manufacturers ramp up production to address substantial order backlogs, demand for high-purity titanium sponge is increasing steadily. Airlines are placing greater emphasis on fuel efficiency and emission reduction, accelerating the adoption of lightweight materials such as titanium. The transition toward next-generation aircraft designs, including wide-body and fuel-efficient narrow-body platforms, further reinforces the need for advanced titanium materials. Defense forces place a strong emphasis on performance, durability, and weight reduction, positioning titanium sponge as a strategic material and supporting sustained growth momentum across the aerospace and defense sectors.

The expansion of the defense sector further strengthens titanium sponge demand, driven by rising military expenditures and ongoing modernization programs across major economies. Titanium alloys produced from sponge titanium are widely used in fighter aircraft, helicopters, naval vessels, armored vehicles, and missile systems due to their exceptional strength, corrosion resistance, and ability to withstand extreme operating conditions. Heightened geopolitical tensions and increased emphasis on domestic defense manufacturing have accelerated procurement of advanced military platforms, directly boosting titanium consumption. Emerging applications, such as hypersonic vehicles, unmanned aerial systems, and additive manufacturing of defense components, rely heavily on high-purity titanium feedstock, reinforcing long-term demand growth.

Supply Chain Vulnerabilities and Geopolitical Risks

Titanium sponge production is concentrated in a limited number of regions, primarily Asia Pacific and Eastern Europe, making global supply chains highly vulnerable to geopolitical tensions, trade restrictions, and export controls. Disruptions in major producing countries can quickly result in supply shortages, price fluctuations, and extended lead times for downstream industries such as aerospace, defense, and medical manufacturing. Titanium sponge production is energy-intensive and relies on the consistent availability of key raw materials, including titanium tetrachloride, magnesium, and high-purity chlorine. Volatility in energy costs or raw material supply further pressures production stability and cost structures.

Geopolitical conflicts, sanctions, and evolving trade policies have heightened the risk of supply disruptions, particularly for countries dependent on imports of high-purity titanium sponge. Limitations on cross-border technology transfer and defense-related material trade can restrict access to critical grades required for aerospace and military applications. Manufacturers face challenges in maintaining stable production schedules and meeting stringent quality requirements. Although initiatives such as supply chain diversification, reshoring, and increased recycling are being pursued, addressing these structural vulnerabilities remains a significant challenge, potentially constraining short-term market growth and elevating operational risks across the titanium sponge industry.

Advancements in Additive Manufacturing and Recycling

Additive manufacturing technologies increasingly rely on titanium powders derived from high-purity sponge titanium due to their superior mechanical strength, design flexibility, and weight reduction capabilities. Aerospace and defense manufacturers are adopting AM to produce complex components with reduced material waste, shorter lead times, and improved performance. The medical sector is expanding the use of 3D-printed titanium implants and prosthetics, driven by customization needs and titanium’s excellent biocompatibility. Growing investments in aerospace-grade powder production facilities are strengthening the linkage between sponge titanium suppliers and additive manufacturing value chains.

Recycling innovations enhance market opportunities by improving supply security and sustainability. Titanium scrap recycling helps reduce dependency on primary sponge production, lowers energy consumption, and mitigates supply chain risks associated with geopolitical uncertainties. Advanced recycling techniques now enable the recovery of high-purity titanium suitable for aerospace-grade applications, supporting circular economy initiatives. These developments are particularly important in regions with limited domestic sponge capacity, helping stabilize supply and pricing. Increased investments in closed-loop recycling systems also improve cost-efficiency and long-term availability of titanium sponge for critical end-use industries.

Category-wise Analysis

Product Type Insights

High-purity titanium sponge is expected to dominate the titanium sponge market, accounting for approximately 40% of total revenue in 2026, driven by its indispensable role in high-performance applications. This segment leads the market due to stringent requirements for quality, strength, and reliability, particularly in aerospace and advanced engineering sectors. High-purity sponge titanium is critical for producing titanium alloys used in aircraft engines, structural airframes, and other high-stress components, where material failure is unacceptable. Its exceptional fatigue resistance, thermal stability, and corrosion resistance make it essential for mission-critical applications. For instance, Toho Titanium Co., Ltd. specializes in supplying high-purity titanium sponge to aerospace and industrial customers, delivering materials that comply with rigorous international quality standards.

High-purity sponge titanium is also expected to be the fastest-growing segment in 2026, driven by rising demand from next-generation aerospace, medical, and additive manufacturing applications. Growth in this segment is supported by the increasing use of advanced titanium alloys that require ultra-clean and highly consistent feedstock to meet stringent performance and safety requirements. Medical device manufacturers are expanding their use of high-purity titanium in implants and surgical instruments, benefiting from its superior biocompatibility and long service life. For example, Osaka Titanium Technologies Co., Ltd. continues to invest in advanced purification technologies to address the growing demand for premium-grade sponge titanium.

End-user Insights

The aerospace and defense segment is expected to remain the leading end-use segment, accounting for approximately 50% of total market revenue in 2026, supported by the sector’s strong dependence on lightweight, high-strength materials. Titanium sponge serves as the primary feedstock for titanium alloys that are extensively used in aircraft structures, jet engines, landing gear, and a wide range of defense platforms. The industry’s focus on fuel efficiency, durability, and high performance makes titanium an essential material for both commercial and military aircraft. For example, VSMPO-AVISMA Corporation is a major supplier of titanium materials to global aerospace manufacturers, supporting large commercial aircraft programs and defense applications. The dominance of this segment is further reinforced by substantial aircraft order backlogs, ongoing fleet modernization initiatives, and rising defense procurement across major economies.

The medical sector is expected to be the fastest-growing end-use segment in 2026, driven by increasing demand for biocompatible, durable, and corrosion-resistant materials. Titanium produced from sponge titanium is widely used in orthopedic implants, dental fixtures, cardiovascular devices, and surgical instruments due to its high strength, non-toxicity, and long-term biocompatibility. For instance, Zimmer Biomet, a leading medical device manufacturer, extensively utilizes titanium alloys in orthopedic implants to improve performance and patient outcomes. The growing adoption of 3D printing in healthcare is enabling the production of patient-specific implants with complex geometries, enhanced osseointegration, and reduced recovery times, all of which depend on high-quality titanium materials.

Regional Insights

North America Titanium Sponge Market Trends

North America is expected to be the fastest-growing region in the titanium sponge market in 2026, driven by advanced manufacturing capabilities and stringent quality standards. The region benefits from a well-established aerospace ecosystem, where titanium sponge is a critical input for producing high-performance alloys used in aircraft structures, engines, and defense platforms. Increasing emphasis on lightweight materials to enhance fuel efficiency and reduce emissions continues to support steady demand. The medical sector is contributing to market growth through rising use of titanium in orthopedic implants, dental applications, and surgical instruments, supported by an aging population and higher healthcare spending. Strict regulatory oversight and certification requirements further sustain demand for high-purity titanium sponge, reinforcing premium pricing and long-term supplier relationships.

Investment activity in North America is increasingly centered on strengthening supply chain resilience, expanding recycling capabilities, and adopting advanced processing technologies. Manufacturers are prioritizing domestic sourcing and circular economy initiatives to reduce reliance on imports and mitigate geopolitical risks. For example, ATI Metals plays a significant role in supplying titanium materials to aerospace and defense customers while expanding recycling operations to enhance sustainability and cost-efficiency. The growing adoption of additive manufacturing in aerospace and medical applications is generating new demand for high-quality sponge-derived titanium powders. Closer collaboration between material producers and end-use manufacturers is also improving process efficiency, quality control, and material traceability.

Europe Titanium Sponge Market Trends

Europe is expected to be a key market for titanium sponge in 2026, driven by strong demand from the aerospace, medical, and industrial sectors, underpinned by advanced engineering capabilities and stringent regulatory standards. The region hosts a mature aerospace manufacturing base, where titanium sponge is critical for producing high-performance alloys used in aircraft structures, engines, and space applications. Rising focus on lightweight materials and fuel-efficient aircraft continues to support steady titanium sponge consumption. The medical sector also fuels growth, with increasing use of titanium-based implants and surgical instruments, driven by aging populations and expanding healthcare infrastructure.

Sustainability and technological innovation are major trends influencing the European titanium sponge market. Manufacturers are prioritizing recycling, energy-efficient production processes, and compliance with strict environmental regulations. For instance, Advanced Metallurgical Group N.V. (AMG) plays a prominent role in supplying titanium materials to European aerospace and industrial customers while investing in recycling initiatives and low-carbon production technologies. The expanding adoption of additive manufacturing in aerospace and medical applications is further boosting demand for high-purity sponge-derived titanium powders. Closer collaborations between aerospace OEMs and material suppliers are accelerating the development of advanced titanium grades to meet evolving performance requirements.

Asia Pacific Titanium Sponge Market Trends

The Asia Pacific region is expected to dominate the titanium sponge market in 2026, accounting for approximately 45% of the total share, driven by robust manufacturing capabilities, expanding aerospace programs, and rising industrial demand. Key countries such as China, Japan, and India lead the region due to their well-established metallurgical infrastructure and cost-efficient production ecosystems. Growing aircraft manufacturing, defense modernization efforts, and space exploration initiatives are driving demand for high-purity titanium sponge, while rapid industrialization and the expansion of chemical processing, power generation, and marine industries sustain steady demand for commercial-grade titanium sponge.

Capacity expansion and technological advancement are major trends shaping the Asia Pacific market. Manufacturers are investing in advanced refining techniques, automation, and energy-efficient processes to meet stricter quality standards and environmental regulations. For example, Pangang Group Vanadium Titanium & Resources Co., Ltd. plays a key role in China’s titanium sponge production, supporting both aerospace and industrial customers through integrated manufacturing capabilities. The increasing adoption of additive manufacturing and medical implants in the region is driving demand for high-purity titanium sponge, reinforcing growth prospects across multiple sectors.

Competitive Landscape

The global titanium sponge market is moderately fragmented, characterized by a mix of established global producers and emerging regional players competing on quality, capacity, and technological innovation. While the market is moderately concentrated, the leading producers control a substantial share of production through integrated supply chains encompassing raw material sourcing, sponge manufacturing, and downstream titanium products. Competition is heavily influenced by stringent aerospace and defense qualification standards, high entry barriers due to capital-intensive processes, and the requirement for advanced refining technologies to produce high-purity titanium.

Key players such as VSMPO-AVISMA Corporation, TIMET (Titanium Metals Corporation), and Toho Titanium Co., Ltd. leverage production scale, technical expertise, and strategic partnerships with aerospace OEMs to maintain and grow market share. These companies focus on capacity expansion, certification upgrades, and sustainability initiatives to meet evolving industry demands and differentiate their offerings. Innovations in sponge refining, energy-efficient production processes, and recycling capabilities are becoming increasingly critical competitive factors, helping manufacturers enhance cost efficiency while minimizing environmental impact.

Key Industry Developments:

- In January 2026, PTC Industries Limited secured a major contract from the Vikram Sarabhai Space Centre (VSSC), a key division of the Indian Space Research Organisation (ISRO), to supply aerospace-grade titanium alloy ingots for India’s space missions. Under the agreement, PTC Industries will convert 40 tonnes of Grade 1 titanium sponge into Ti-6Al-4V alloy ingots using the advanced Double Vacuum Arc Remelting (Double VAR) process over one year. This process ensures high metallurgical cleanliness, uniform composition, and superior mechanical strength, which are essential for aerospace and space applications.

- In February 2025, aerospace-grade titanium sponge producers in Japan, Kazakhstan, and Saudi Arabia implemented capacity-optimization and production-scaling strategies to strengthen their market positions. Higher utilization at Kazakhstan’s Ust-Kamenogorsk Titanium and Magnesium Plant (UKTMP) and Saudi Arabia’s AMIC Toho Titanium Metal offset reduced Japanese output due to inventory adjustments and softer domestic demand. This coordinated approach reflects a deliberate effort to rebalance the global supply of aerospace-grade titanium sponge, expanding the role of newer producers and reducing reliance on U.S.-exposed supply chains.

Companies Covered in Titanium Sponge Market

- Titanium Metals Corporation (TIMET)

- VSMPO-AVISMA Corporation

- Toho Titanium Co., Ltd.

- Kobe Steel, Ltd.

- ATI Metals

- OSAKA Titanium Technologies Co., Ltd.

- Zaporozhye Titanium & Magnesium Combine (ZTMC)

- China National Aero-Technology Import & Export Corporation (CATIC)

- Pangang Group Vanadium Titanium & Resources Co., Ltd.

- Advanced Metallurgical Group N.V. (AMG)

- Sumitomo Corporation

- RTI International Metals, Inc.

- Tronox Limited

Frequently Asked Questions

The global titanium sponge market is projected to reach US$1.9 billion in 2026.

The titanium sponge market is propelled by growing demand from aerospace, defense, medical, and industrial sectors that require materials combining light weight, high strength, and exceptional corrosion resistance.

The titanium sponge market is expected to grow at a CAGR of 8.2% from 2026 to 2033.

Key market opportunities include the rising adoption of additive manufacturing, the growth of aerospace and defense initiatives, the expanding application in medical implants, and progress in recycling and sustainable production technologies.

Titanium Metals Corporation (TIMET), VSMPO-AVISMA Corporation, and Toho Titanium Co. are the leading players.