- Plastics, Polymers & Resins

- Thermoformed Plastic Products Market

Thermoformed Plastic Products Market Size, Share, and Growth Forecast 2025 - 2032

Thermoformed Plastic Products Market by Product Type (PET / PETG, PP, HIPS / PS, PVC, ABS, Polycarbonate, Recycled & Bio-based Plastics, Others), Product Form (Trays, Blister packs, Clamshells, Lids & Containers, Heavy-Gauge Thermoformed Parts, Twin-Sheet Thermoformed Parts, Displays & Signage), Process Type, Application, Regional Analysis, 2025 - 2032

Thermoformed Plastic Products Market Size and Trend Analysis

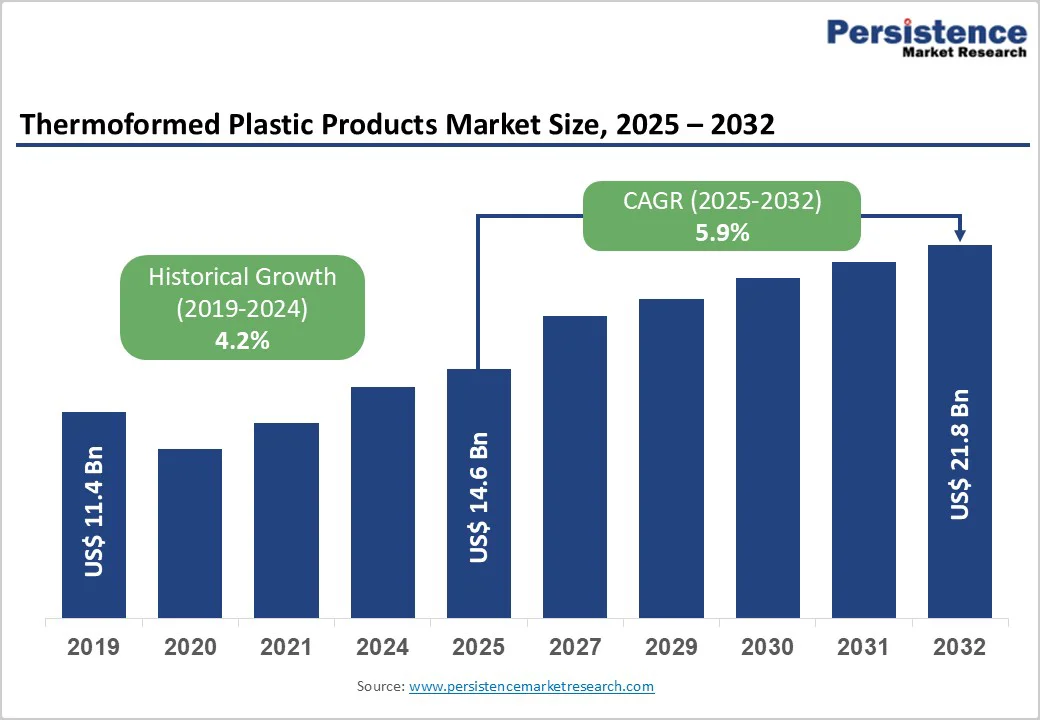

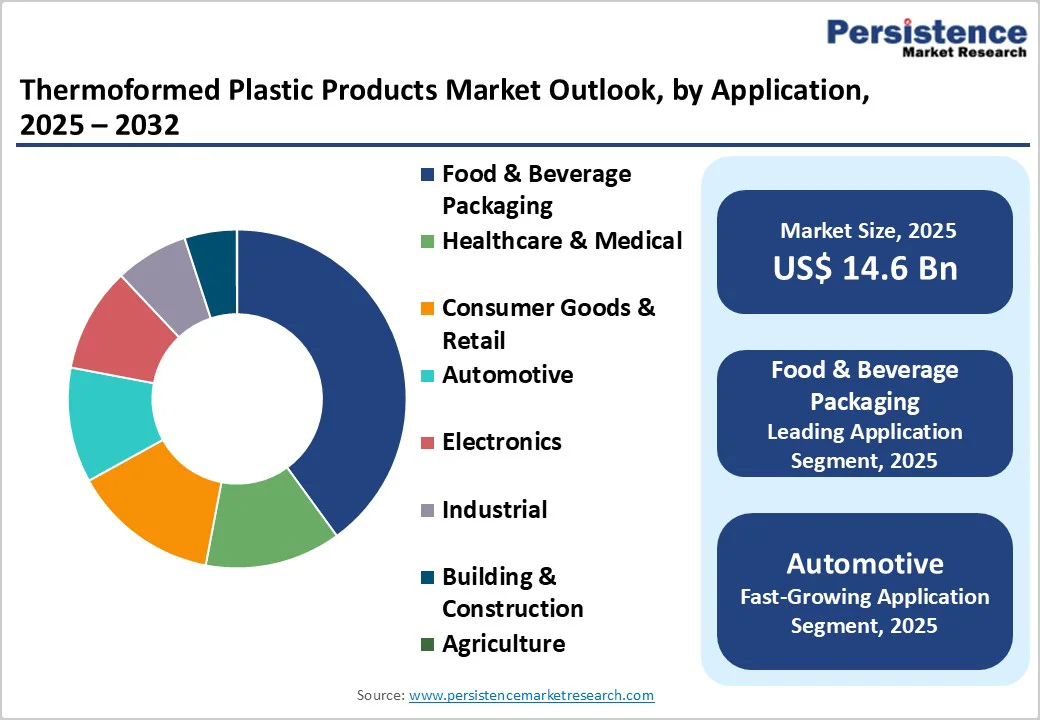

The Global Thermoformed Plastic Products Market size is likely to be valued at US$ 14.6 Bn in 2025 and is projected to reach US$ 21.8 Bn by 2032, growing at a CAGR of 5.9% between 2025 and 2032. The market's expansion is primarily driven by rising demand for lightweight, cost-effective packaging solutions across food & beverage, healthcare, and automotive industries, along with increasing adoption of recyclable and sustainable thermoformed materials supporting regulatory compliance.

Key Market Highlights

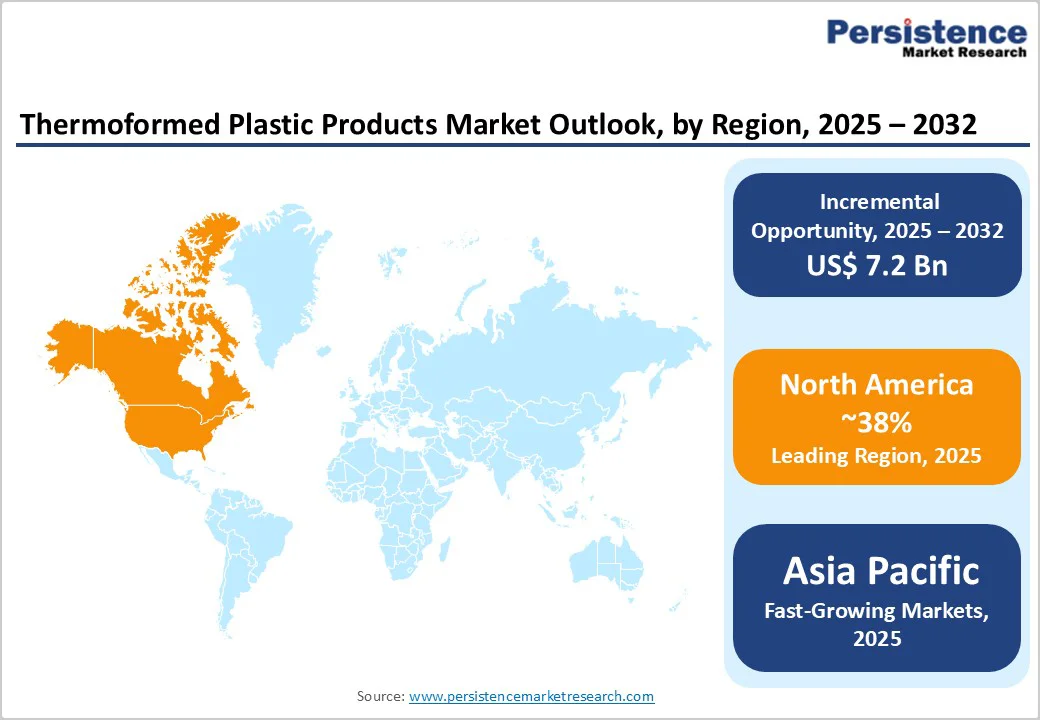

- Leading Region: North America dominates the global thermoformed plastic products market with 38% share, driven by advanced infrastructure and regulatory support for sustainable packaging innovations.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with 7% CAGR, fueled by manufacturing hubs in China and India catering to rising e-commerce and food demands.

- Leading Application: Food & Beverage Packaging remains the dominant application segment with 40% share, offering lightweight solutions that extend shelf life and reduce waste.

- Fastest-Growing Product Type: Recycled & Bio-based Plastics is the fastest-growing product type with 6.4% CAGR, supported by global sustainability policies and consumer eco-preferences.

- Key Opportunity: Adoption of sustainable materials presents a key opportunity, enabling companies to access premium markets through recyclable thermoformed innovations.

| Key Insights | Details |

|---|---|

|

Market Size (2025E) |

US$ 14.6 Bn |

|

Market Value Forecast (2032F) |

US$ 21.8 Bn |

|

Projected Growth CAGR(2025-2032) |

5.9% |

|

Historical Market Growth (2019-2024) |

4.2% |

Market Dynamics

Drivers - Growing Reliance on Convenient and Safe Food Packaging is Driving Strong Demand for Thermoformed Plastic Products

Growing reliance on convenient and safe food packaging is a major driver accelerating the global Thermoformed Plastic Products Market. As consumer lifestyles become increasingly fast-paced, the demand for ready-to-eat meals, on-the-go snacks, fresh produce packs, and portion-controlled food items continues to rise. Thermoformed plastics, such as PET, PP, and polystyrene, offer lightweight, durable, and hygienic packaging solutions that extend shelf life, maintain product freshness, and provide excellent barrier protection against contaminants. Retailers and food processors prefer thermoformed trays, clamshells, and containers due to their versatility, cost-effectiveness, and compatibility with automated filling and sealing systems.

The growing emphasis on food safety, strict regulatory standards, and the need for tamper-evident packaging further boost adoption. The expansion of quick-service restaurants, online food delivery, and supermarket fresh food sections reinforces this trend, making thermoformed plastic packaging indispensable for efficient and safe food handling across global supply chains.

Rising Healthcare Needs and Sterile Medical Packaging Requirements are accelerating the Adoption of Thermoformed Plastics

Rising healthcare needs and the growing emphasis on sterile, reliable medical packaging are significantly accelerating the adoption of thermoformed plastics. As global healthcare expenditure increases and hospitals, diagnostic centers, and pharmaceutical companies expand their operations, the demand for safe, contamination-free packaging for medical devices, surgical instruments, vials, and diagnostic kits is rising rapidly. Thermoformed plastics, such as medical-grade PET, PVC, and PP, offer excellent clarity, durability, and superior barrier properties, making them ideal for sterile blister packs, trays, and clamshells used in medical applications.

Their ability to maintain product integrity throughout transportation and storage, while supporting gamma and E-beam sterilization, enhances their suitability in critical healthcare environments. The rapid growth of single-use medical products, along with strict regulatory requirements for infection control and patient safety, further strengthens their market adoption. The surge in point-of-care testing, home healthcare, and chronic disease management fuels sustained demand for high-precision thermoformed medical packaging solutions globally.

Restraint - Volatile Resin and Oil Prices Continue to Challenge Cost Stability in Thermoformed Plastic Manufacturing

One of the major restraints affecting the global thermoformed plastic products market is the frequent fluctuation in raw material costs, especially for petroleum-based resins such as PET and PP. These materials experience price volatility that can increase production costs by as much as 20% during peak periods. When oil prices fluctuate, resin prices rise sharply, reducing profit margins for manufacturers and discouraging capacity expansions.

The situation is more challenging in developing markets where supply chain disruptions, such as those observed in 2024 due to geopolitical tensions, create inconsistent material availability. This makes it difficult for smaller companies to compete with larger players that possess stronger procurement networks. As a result, market stability is affected, and innovation slows as companies become cautious about investing in new technologies when raw material costs are unpredictable.

Increasing Global Restrictions on Single-Use Plastics Limiting Traditional Thermoformed Packaging Applications

Environmental regulations represent another major challenge for the thermoformed plastic products market, especially in regions implementing strict policies to reduce plastic waste. Several governments have introduced bans or limitations on single-use plastics, which restricts the use of thermoformed products in disposable packaging. The EU’s Single-Use Plastics Directive alone has contributed to a 30% reduction in plastic consumption across member states since 2021, pushing manufacturers to adopt alternative materials.

Switching to sustainable or paper-based packaging often involves higher production costs and extensive redesign efforts. This increases compliance expenses and slows down adoption in industries like retail and food service. Consequently, market growth weakens in heavily regulated areas, forcing companies to rethink their material strategies and invest in greener technologies that may not provide immediate financial returns.

Opportunity - Growing Interest in Recycled and Bio-Based Plastics is Creating New Opportunities for Sustainable Thermoformed Packaging

A significant opportunity in the thermoformed plastic products market lies in the rising demand for eco-friendly materials, including recycled and bio-based plastics. Consumers and regulators increasingly prefer sustainable packaging, aligning with policies such as the EPA’s goal to achieve 50% plastic recycling by 2030. Bio-based PET and similar materials are becoming more popular because they offer the same strength and performance as traditional plastics while reducing environmental impact.

The bio-based PET could account for around 25% of the market by 2032, particularly within food packaging due to its compatibility with sustainability certifications. Companies collaborating with renewable material suppliers can gain competitive advantages, higher margins, and broader acceptance in environmentally focused regions such as Europe. This shift also supports circular economy models, creating additional revenue streams through recycling and reuse programs.

Rapid Industrial Growth in the Asia Pacific is Unlocking Major Expansion Opportunities for Thermoformed Plastic Manufacturers

Thermoformed plastic product manufacturers have substantial opportunities for expansion in emerging markets, particularly in the Asia Pacific. According to ADB projections, demand in the region is expected to grow by nearly 7% annually due to rapid industrialization and a growing middle-class population. Countries like India and China offer significant cost advantages in manufacturing, enabling efficient production of components for automotive, electronics, and consumer goods sectors.

Infrastructure improvements under initiatives such as China’s Belt and Road are strengthening supply chains and boosting demand for thermoformed parts. Additionally, expanding retail markets, increasing food consumption, and growing agricultural activities in these regions support broader product adoption. Companies that localize production and establish regional partnerships are well-positioned to benefit from these trends and achieve long-term, sustainable growth.

Category-wise Analysis

Product Type Insights

In the product type category, PET/PETG stands out as the leading segment with nearly 25% market share because of its clarity, strong barrier properties, and high recyclability. These qualities make it highly suitable for food, beverages, and pharmaceutical packaging. The PET’s lightweight nature helps reduce shipping costs by 15–20% compared to glass. Growing global recycling capacity, now around 20 million tons annually, further strengthens supply reliability and supports PET/PETG’s market leadership.

Product Form Insights

The Trays segment leads the product form category with about 30% market share due to its versatility and usefulness in retail, food service, and industrial packaging. The trays help reduce food waste by improving portion control and enabling better stacking during transport. Their fast production capacity, reaching up to 500 units per minute, makes them cost-effective for large-scale operations. These advantages drive strong adoption across consumer goods, healthcare, and e-commerce sectors.

Process Type Insights

Thin-gauge thermoforming dominates the process type segment with nearly 35% market share because it supports high-speed production of disposable packaging. This process reduces material use by about 25%, helping manufacturers control costs. Its compatibility with both radiant and contact heating methods allows quick scaling for large production runs. These benefits make thin-gauge thermoforming the preferred option for blister packs, food containers, and other lightweight packaging needs.

Application Insights

Food and beverage packaging is the top application area, accounting for around 40% of market demand due to the need for hygienic, durable, and lightweight solutions. The thermoformed packaging can reduce spoilage by about 15% in supply chains, which is essential as global population levels rise. Its tamper-evident features also strengthen consumer trust, making it widely used in ready-to-eat meals and packaged foods. These functional and safety benefits support its leading position in the market.

Regional Insights

North America Global Thermoformed Plastic Products Market Trends

North America remains a dominant market for thermoformed plastic products, with the U.S. leading due to its strong manufacturing base and high demand from food, healthcare, and consumer industries. Strict FDA regulations ensure high safety and quality standards, encouraging continuous innovation in recyclable PET trays and medical-grade packaging.

Sustainability initiatives driven by the EPA are accelerating the adoption of bio-based and recycled materials. In the automotive sector, NHTSA reports show that thermoformed components can improve fuel efficiency by around 10% due to lightweight construction. These factors collectively reinforce North America’s position as a trendsetter in advanced thermoforming applications.

Europe Global Thermoformed Plastic Products Market Trends

Europe’s market for thermoformed plastic products remains strong, led by countries such as Germany, the U.K., France, and Spain. The region’s growth is heavily influenced by its commitment to circular economy practices and strict environmental regulations. The European Commission’s Green Deal and related directives have accelerated the shift toward recycled plastics, with 25% of all packaging now incorporates post-consumer recycled content.

Germany’s expertise in engineering and its adherence to DIN standards support highly precise thermoforming, especially in medical and industrial sectors. The U.K. and France also drive sustainability through measures like the Plastic Packaging Tax, which has reduced the use of virgin plastics by 15% since 2022. Spain’s agricultural sector continues to adopt thermoformed packaging to support crop protection and distribution. Together, these developments create a coordinated and innovation-driven market landscape.

Asia Pacific Thermoformed Plastic Products Market Trends

Asia Pacific remains one of the most dynamic and fast-growing regions in the thermoformed plastic products market. China, Japan, India, and ASEAN nations continue to lead due to their manufacturing strength and expanding consumer markets. China, the world’s largest producer of plastics, reported a 12% rise in export volumes for thermoformed trays and packaging materials in 2024.

India’s rapid urbanization, expected to reach 600 million urban residents by 2030 according to NITI Aayog, has significantly increased demand for food and retail packaging. Japan remains a key player in high-precision automotive and electronics-related thermoforming. Meanwhile, ASEAN sees strong growth supported by regional trade agreements and rising manufacturing activity, with annual output increasing by 6% as reported by the ASEAN Secretariat. These combined factors ensure sustained expansion for thermoformed plastic products across the region.

Competitive Landscape

The global thermoformed plastic products market is moderately fragmented, with a mix of large multinational firms and regional players competing through innovation and sustainability focus. Market concentration stands at around 40% held by top players, who employ strategies such as R&D investments in bio-based materials and strategic acquisitions to expand capacity. Key differentiators include advanced automation for precision forming and eco-certifications, while emerging models emphasize circular supply chains and digital twins for efficient design. This structure encourages collaboration on green technologies, driving overall competitiveness.

Key Market Developments

- In February, 2025: Plastic Ingenuity introduced a sustainable thermoform-ready pharmaceutical tub made from recyclable polyester to support improved circularity in medical packaging. This solution directly addresses rising EU waste management concerns and aligns with sustainability priorities.

- In April, 2025, the PET Recycling Coalition granted funding to multiple North American recycling facilities to upgrade equipment for better PET thermoform recovery. These improvements strengthen regional recycling efficiency and increase the high-quality recycled PET supply.

- In September 2025: Cosmo Plastech unveiled its latest thermoformed sustainable rigid packaging solutions at the World of Ice Cream Expo, emphasizing eco-friendly materials designed for modern food applications and improved product safety.

Companies Covered in Thermoformed Plastic Products Market

- Pactiv, LLC.

- Anchor Packaging, Inc.

- Associated Packaging, Ltd.

- Peninsula Packaging Company, LLC.

- Placon Group

- Berry Plastics

- CM Packaging

- Clear Lam Packaging

- Graham Packaging

- D&W Fine Pack

- Huhtamaki Group

- Silgan Plastics

- Sonoco Products Company

- Winpak Ltd.

Frequently Asked Questions

The market is expected to reach US$ 21.8 Bn by 2032, growing from US$ 14.6 Bn in 2025 at a 5.9% CAGR.

Key drivers include rising food packaging needs for convenience and healthcare demands for sterile solutions, supported by lightweight material benefits.

Food & Beverage Packaging leads with 40% share, due to its role in extending shelf life and meeting e-commerce growth.

North America leads, driven by U.S. manufacturing strength and regulatory frameworks promoting innovation.

Sustainable materials like bio-based plastics offer growth through eco-compliance and emerging market expansion.