- Semiconductor Materials & Components

- Thermoelectric Modules Market

Thermoelectric Modules Market Size, Share, and Growth Forecast 2025 - 2032

Thermoelectric Modules Market by Product Type (Bulk, Micro, Thin Film), Technology (Single Stage, Multi Stage), End-user (Consumer Electronics, Manufacturing and Industrial, IT and Telecom, Automotive, Healthcare), and Regional Analysis for 2025 - 2032

Thermoelectric Modules Market Size and Trend Analysis

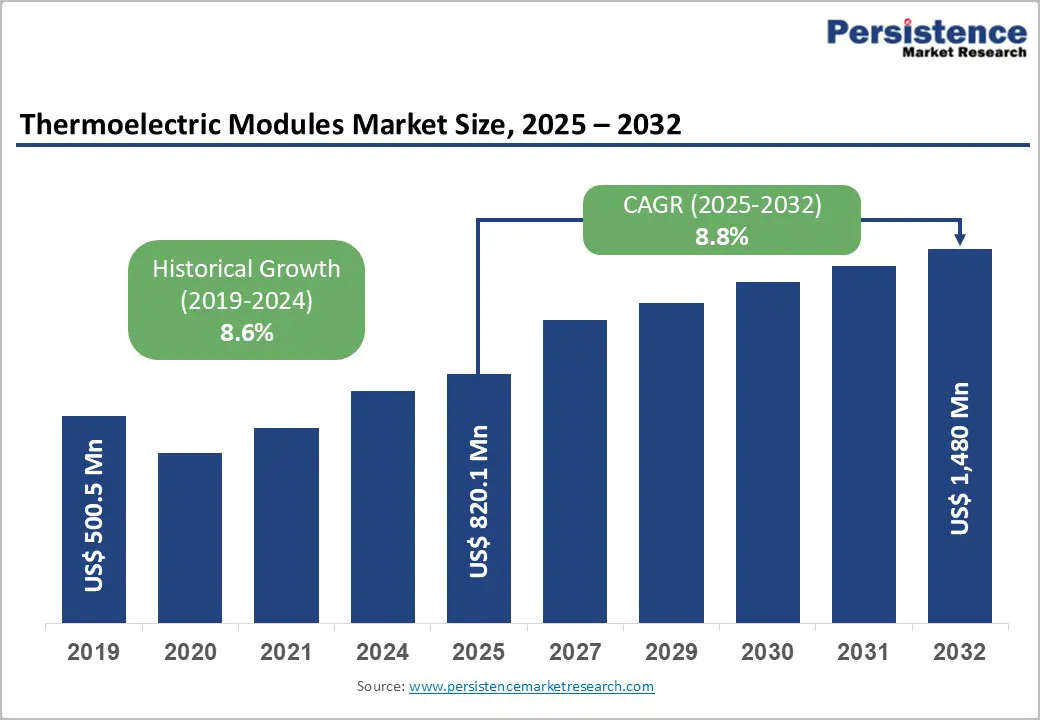

The global thermoelectric modules market size is likely to be valued at US$820.1 million in 2025 and is expected to reach US$1,480 million by 2032, growing at a CAGR of 8.8% during the forecast period from 2025 to 2032, driven by rising demand for energy-efficient, solid-state cooling solutions and increasing adoption of waste-heat recovery technologies across automotive, manufacturing, and consumer electronics industries.

The growth is driven by the rapid adoption of electric vehicles (EVs), industrial automation, and miniaturized electronic devices, where thermoelectric modules provide precise temperature control, high reliability, and maintenance-free operation without refrigerants.

Key Industry Highlights:

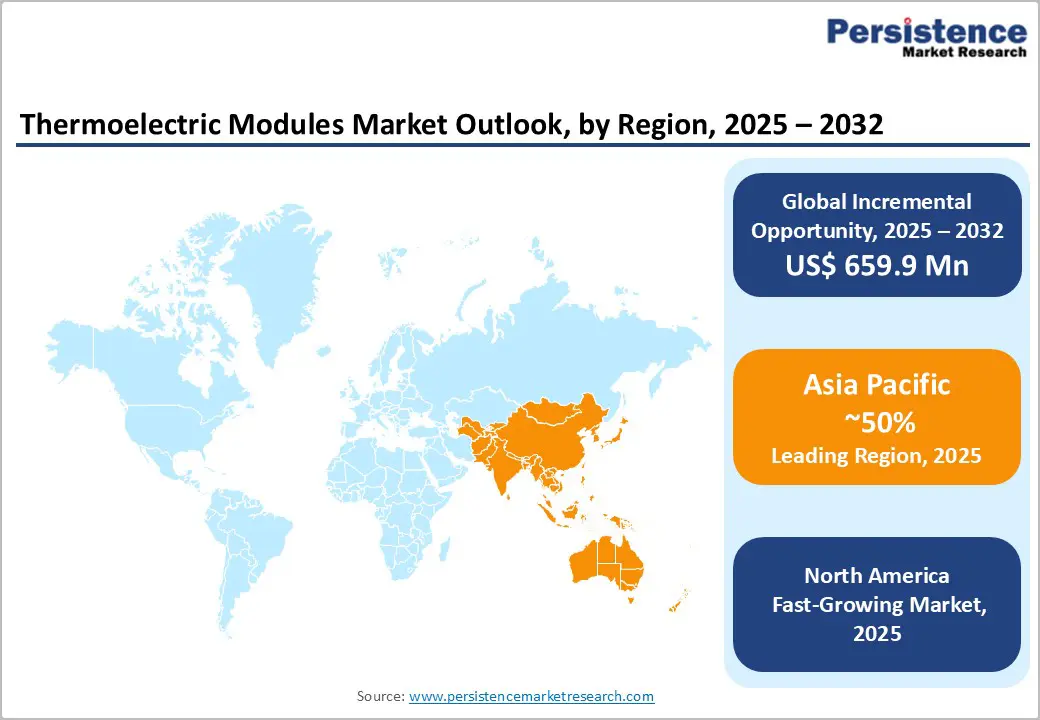

- Leading Region: Asia Pacific leads the market with around 50% share in 2025, driven by rapid industrial growth, state-funded clean-tech investments, and favorable export-oriented policies.

- Fastest-growing Region: North America is the fastest-growing region, driven by innovation hubs, strict energy-efficiency regulations, and government-backed projects in waste heat recovery and automotive applications.

- Leading Product Type: Bulk modules lead the product type segment with 50% revenue share in 2025, due to their broad applicability and ease of customization for industrial and automotive sectors.

- Leading Technology: Single-Stage technology leads the market with over 42% revenue share, preferred for its simplicity and cost-effectiveness in standard applications.

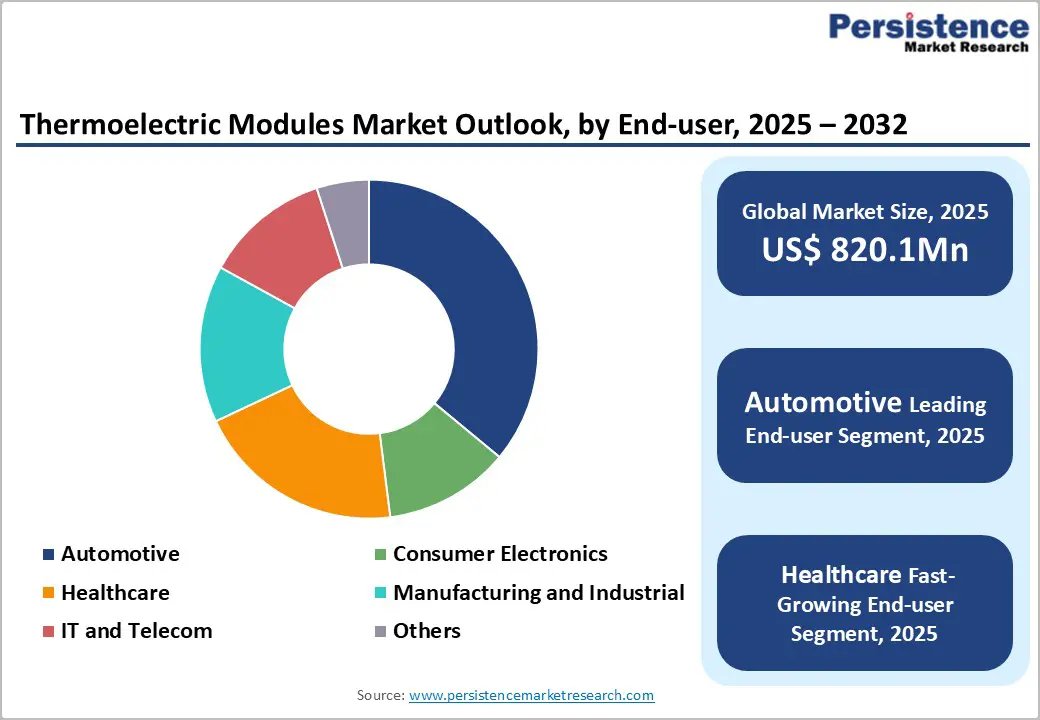

- Leading End-user Type: Automotive is the leading segment in the market with about 40% revenue share, due to thermoelectric module integration in vehicle climate systems and industrial processes.

| Key Insights | Details |

|---|---|

| Thermoelectric Modules Market Size (2025E) | US$820.1 Mn |

| Market Value Forecast (2032F) | US$1,480 Mn |

| Projected Growth CAGR (2025 - 2032) | 8.8% |

| Historical Market Growth (2019 - 2024) | 8.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Energy-Efficient Solutions

Thermoelectric modules operate without moving parts or refrigerants, enabling precise cooling and heating with minimal energy loss, which makes them highly attractive for automotive, consumer electronics, and industrial applications. In EVs, these modules are gaining traction for battery thermal management, seat climate control, and cabin comfort, helping manufacturers improve overall energy efficiency and driving range. In consumer electronics and IT & telecom equipment, the growing need to manage heat in smaller, high-performance devices is also accelerating the adoption of solid-state cooling solutions.

Emphasis on sustainability and reduced carbon emissions is increasing the use of thermoelectric modules in waste-heat recovery systems. Manufacturing plants and industrial processes generate significant unused heat, and thermoelectric technology enables partial conversion of this heat into usable electrical energy, improving overall system efficiency. Governments and regulatory bodies are also promoting energy-efficient technologies through stricter efficiency standards and clean-energy initiatives, supporting market growth. As industries focus on lowering operating costs, reducing energy consumption, and meeting environmental goals, thermoelectric modules are increasingly viewed as a practical and scalable solution, reinforcing their long-term demand across multiple end-user sectors.

High Initial Cost and Complexity

High initial costs and system complexity are key challenges limiting adoption, especially in cost-sensitive applications. Thermoelectric modules rely on specialized semiconductor materials such as bismuth telluride and advanced alloys, which are expensive to source and manufacture. Fabrication processes require precise material engineering and quality control, increasing production costs compared to conventional cooling technologies. As a result, thermoelectric solutions often carry higher upfront prices, limiting their penetration in price-driven markets and small-scale industrial users despite their long-term efficiency benefits.

The complexity of system integration further limits widespread adoption. Thermoelectric modules require carefully designed heat sinks, thermal interfaces, and power control systems to achieve optimal performance. Improper integration can significantly reduce efficiency, making system design more demanding and engineering-intensive. For automotive, healthcare, and industrial applications, this complexity increases development time and raises total system costs. Smaller manufacturers and end-users may lack the technical expertise needed to implement thermoelectric solutions effectively, slowing adoption. Although ongoing R&D and economies of scale are gradually reducing these barriers, high initial investments and design complexity continue to pose challenges to rapid market expansion in the short term.

Emerging Markets and Industrial Automation

Expanding manufacturing capacity and increased investment in energy-efficient technologies are driving automation across the Asia Pacific, Latin America, and parts of the Middle East. As factories, logistics centers, and process industries modernize, demand is rising for compact, reliable, and low-maintenance thermal management solutions to support automated equipment, sensors, and control systems. Thermoelectric modules, with their solid-state construction and precise temperature control, are particularly well-suited for space-constrained or complex environments where conventional cooling is impractical.

These modules are increasingly deployed on automated production lines, in industrial electronics, and in monitoring systems to improve reliability and minimize downtime. Growing emphasis on energy efficiency and sustainability in emerging markets is further supporting adoption, as thermoelectric technologies enable lower power consumption and waste-heat recovery. In smart factories, thermoelectric modules help maintain stable operating temperatures for sensors, power electronics, and control units, ensuring consistent performance even in harsh industrial conditions.

Category-wise Analysis

Product Type Insights

Bulk modules lead the thermoelectric modules market, capturing around 50% of total revenue share in 2025, driven by their broad usability and ease of customization for demanding industrial and automotive applications. Their robustness, high power density, and established manufacturing base make them the go-to choice for traditional cooling and power-generation systems. For example, bulk thermoelectric modules are widely used in automotive seat climate control, EV battery thermal management, and industrial process cooling due to their durability, high load-handling capacity, and long operational life, reinforcing their adoption in large-scale applications.

Thin-film thermoelectric modules represent the fastest-growing product type, driven by rising demand for compact, high-efficiency systems. Their ultra-slim form factor makes them ideal for space-constrained applications such as smartphones, wearable electronics, and portable medical devices, where traditional cooling solutions are impractical. For example, they are increasingly used in telecom base stations and IoT-enabled sensors, where thin-film modules enable precise temperature control and energy harvesting. Ongoing advancements in nanomaterials and thin-film fabrication techniques are further improving efficiency while lowering production costs, accelerating adoption across next-generation electronics and smart technologies.

Technology Type Insights

Single-stage thermoelectric technology leads the market, accounting for over 42% revenue share in 2025, as these modules are widely preferred for their simplicity, reliability, and cost-effectiveness. They deliver moderate temperature differentials without complex design requirements, making them attractive for high-volume applications. For example, single-stage modules are commonly used in consumer electronics cooling, such as portable refrigerators and electronic enclosures, where stable and efficient thermal control is required. The use of mature materials such as bismuth-telluride balances performance and cost, allowing OEMs to integrate these modules into existing systems with minimal redesign.

Multi-stage thermoelectric modules represent the fastest-growing technology segment, driven by their enhanced cooling capacity and ability to maintain high temperature differentials across multiple stages. These modules are increasingly used in medical and laboratory equipment, such as DNA analyzers and vaccine storage systems, where precise and deep cooling is essential. As industries demand more advanced thermal solutions, multi-stage thermoelectric technology continues to gain traction in critical, high-performance environments.

End-user Type Insights

Automotive stands as the leading end-user segment, accounting for 40% revenue share in 2025. Automotive applications such as seat climate control, battery thermal management in EVs, and cabin comfort systems remain strong contributors as OEMs shift toward compact, energy-efficient thermal solutions. The manufacturing and industrial sectors increasingly rely on thermoelectric modules for process cooling, precision temperature regulation, and waste-heat recovery systems that boost operational efficiency. For example, thermoelectric modules are increasingly used in power electronics cooling, where reliable temperature regulation enhances system performance and longevity. Beyond automotive, the manufacturing and industrial sectors rely on thermoelectric modules for process cooling, precision temperature regulation, and waste-heat recovery in equipment such as industrial control panels and automated production lines, improving operational efficiency and reducing energy losses.

The healthcare segment is the fastest-growing end-user category, driven by the increasing use of thermoelectric modules in medical devices that require precise and stable temperature control. These modules are widely used in portable vaccine and blood storage units, diagnostic analyzers, and other applications where temperature accuracy is critical. Adoption is also rising in point-of-care testing (POCT) devices and lab-on-chip systems, as thermoelectric technology supports compact, energy-efficient designs. Growing demand for reliable cooling solutions across clinical, laboratory, and home-care settings continues to accelerate uptake in the healthcare sector.

Regional Insights

North America Thermoelectric Modules Market Trends

North America is the fastest-growing region in the thermoelectric modules market, driven by strong technological advancement, rising adoption of solid-state thermal solutions, and increasing investments in energy-efficient systems. The U.S. leads the region due to its robust innovation ecosystem, where major manufacturers, research labs, and semiconductor companies are advancing high-performance thermoelectric materials such as bismuth-telluride and silicon-germanium. For example, Laird Thermal Systems, headquartered in the U.S., has expanded its portfolio of advanced thermoelectric coolers for electronics and medical applications, strengthening regional adoption of high-efficiency thermal solutions.

The region is also witnessing strong uptake across aerospace, defense, medical devices, and EV thermal management systems. Growing electrification in transportation and the need for waste-heat recovery have increased interest in thermoelectric modules for EV battery cooling plate, power electronics, and energy optimization. In healthcare, rising demand for precision diagnostics, portable medical coolers, and temperature-sensitive devices is accelerating the adoption of advanced thermoelectric technologies across hospitals, laboratories, and point-of-care settings.

Europe Thermoelectric Modules Market Trends

Europe remains a significant market for thermoelectric modules, driven by strong regulatory support for energy efficiency under the European Green Deal and related clean-technology mandates. The region’s well-established industrial base, particularly in Germany, France, and the U.K., is increasingly integrating thermoelectric modules into industrial automation systems and manufacturing processes to enhance waste-heat recovery and reduce overall energy consumption. Growing emphasis on carbon neutrality and electrification across automotive and industrial sectors is further supporting the adoption of solid-state thermal solutions that operate without refrigerants.

Research and innovation are also flourishing across Europe, supported by EU-funded programs such as Horizon Europe, which promote the development of advanced and sustainable thermoelectric materials, including lead-free alternatives. Strong public-private collaboration between research institutes and industry players is accelerating the commercialization of next-generation modules. European manufacturers are increasingly focusing on multi-stage and high-power thermoelectric modules designed for precision cooling in medical equipment, scientific instruments, renewable-energy systems, and laboratory applications, reinforcing Europe’s role as a hub for advanced thermoelectric technology development.

Asia Pacific Thermoelectric Modules Market Trends

Asia Pacific leads the thermoelectric modules market with over 50% share, supported by its vast manufacturing base, rapid industrialization, and rising demand for energy-efficient technologies. The region’s strength is anchored by manufacturing hubs such as China and reinforced by its dual role as a major producer and consumer of consumer electronics and electric vehicles, two key end-use segments for thermoelectric modules. For instance, Kyocera Corporation of Japan has expanded its thermoelectric module offerings for automotive and industrial uses, addressing thermal management requirements in EVs and high-performance electronics across the region.

Government support further strengthens the Asia Pacific’s market leadership. China’s sustainability and industrial efficiency policies promote the adoption of thermoelectric modules in automotive systems, factory automation, and power electronics, particularly for waste-heat recovery. Japan and South Korea continue to lead in advanced R&D on thermoelectric materials, focusing on higher efficiency for cooling and energy-harvesting applications, which further consolidates the region’s dominant position in the global market.

Competitive Landscape

The global thermoelectric modules market exhibits a moderately fragmented structure, driven by the presence of established multinational corporations alongside specialized and emerging regional players competing for share across key application segments. Ferrotec, II-VI Marlow (Coherent Corp), and Laird Thermal Systems dominate high-volume sectors such as consumer electronics, automotive thermal management, and industrial cooling, while smaller innovators and regional firms, particularly in Asia Pacific, increasingly gain traction with cost-competitive offerings.

With key leaders including Ferrotec, II-VI Marlow, Laird Thermal Systems, KELK Ltd., TE Technology, and several regional specialists, players differentiate themselves through innovation, application focus, and geographic reach. These players compete through sustained investment in advanced thermoelectric materials and module designs, strategic partnerships with OEMs, and expansion into new end-use markets such as EV battery thermal control and medical diagnostics.

Key Industry Developments:

- In November 2025, Clearwater Wellness introduced the “SnowCap,” a world-first thermoelectric ice bath requiring no ice or plumbing, using patented technology for advanced recovery solutions.

- In May 2025, a Nature study reported the first practical solid-state refrigeration breakthrough using nano-engineered thin-film thermoelectric materials, delivering a much higher cooling performance than traditional bulk devices.

Companies Covered in Thermoelectric Modules Market

- Crystal Ltd.

- TEC Microsystems GmbH

- Ferrotec Corporation

- Thermonamic Electronics (Jiangxi) Corp. Ltd.

- KELK Ltd.

- KRYOTHERM

- Laird Technologies

- RMT Ltd.

- TE Technology Inc.

- II-VI Incorporated

Frequently Asked Questions

The global thermoelectric modules market is valued at US$820.1 million in 2025 and expected to reach US$1,480 million by 2032, reflecting robust growth.

The thermoelectric modules market is primarily driven by growing demand for energy-efficient solutions, continuous advancements in thermoelectric materials, and expanding adoption across automotive, consumer electronics, and healthcare applications.

The bulk product type segment currently leads in market share with wide applicability.

Asia Pacific leads with over 50% market share, driven by manufacturing and industrial growth.

Emerging markets in Asia and expansion into healthcare applications represent significant growth opportunities.