- Biotechnology

- Taurine Market

Taurine Market Size, Share, and Growth Forecast 2026 - 2033

Taurine Market by Form (Powder Liquid), Source (Synthetic, Natural), Application (Energy Drinks, Dietary Supplements, Pharmaceuticals, Infant Formula, Animal Feed & Pet Food, Cosmetics), and Regional Analysis, 2026 - 2033

Taurine Market Share and Trends Analysis

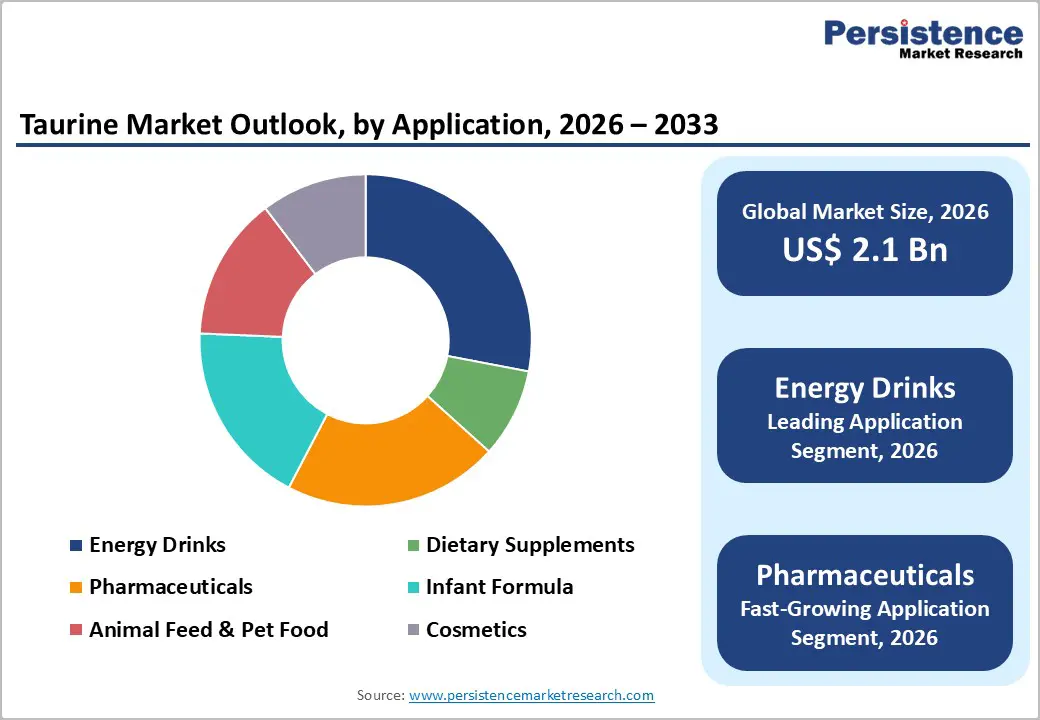

The global taurine market size is expected to be valued at US$ 2.1 billion in 2026 and projected to reach US$ 3.1 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033.

Strong demand from energy drinks, dietary supplements, infant formula, pharmaceuticals, and pet food is underpinning this growth, with taurine’s safety and functional benefits validated by authorities such as EFSA, FDA, and the Codex Alimentarius Commission, which allow its use in foods, beverages, and feeds within specified limits. Favorable toxicological evaluations confirming a wide safety margin for taurine intake, combined with rising consumer interest in performance, vitality, and pet health, are encouraging formulators to retain or increase taurine inclusion levels in existing products and extend it into next-generation functional beverages, clinical nutrition, and premium pet food offerings.

Key Industry Highlights:

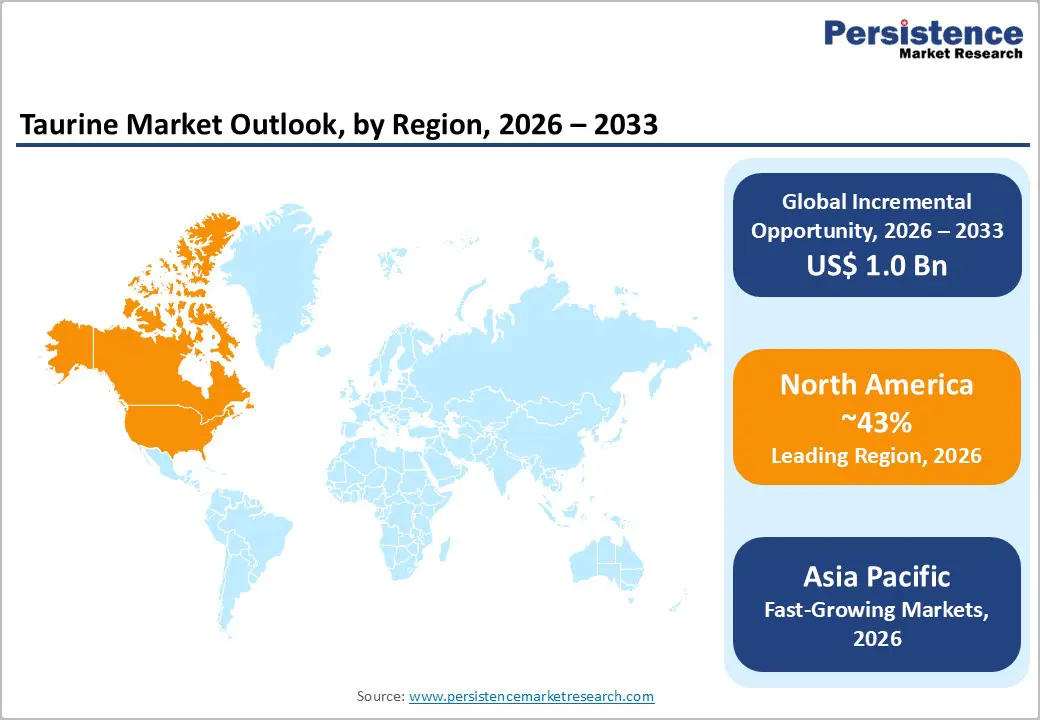

- North America leads the global taurine market, with an estimated 43% share in 2025, supported by a large energy drink and sports beverage base, established infant and clinical nutrition sectors, and a mature pet food industry that heavily relies on taurine fortification for feline health.

- Asia Pacific is projected to be the fastest-growing taurine region between 2025 and 2032, benefiting from its status as the primary manufacturing hub, competitive synthetic production costs in China, and rising consumption of functional beverages, infant formula, and premium pet food across China, India, and ASEAN markets.

- Among applications, energy drinks dominate the taurine market with about 28% share in 2025, driven by taurine’s entrenched role as a core functional ingredient in performance-oriented beverages and by regulatory opinions affirming its safety at current exposure levels in key markets.

- The pharmaceuticals segment is expected to be the fastest-growing taurine application through 2032, as research continues on its potential cardiovascular, metabolic, and neurological benefits and as several Asian markets maintain long-standing use of taurine in liver tonics, ophthalmic preparations, and parenteral nutrition solutions.

- A key market opportunity lies in premium nutraceuticals and pet nutrition, where taurine’s recognized safety, essential role in feline diets, and versatile functionality support launches of condition-specific products ranging from cardiac-support cat foods to performance-focused functional beverages and sports nutrition products.

| Key Insighst | Details |

|---|---|

| Taurine Market Size (2026E) | US$ 2.1 billion |

| Market Value Forecast (2033F) | US$ 3.1 billion |

| Projected Growth CAGR (2026 - 2033) | 5.4% |

| Historical Market Growth (2020 - 2025) | 4.8% |

Market Dynamics

Drivers - Rising consumption of energy drinks and functional beverages

The first major demand driver for the taurine market is the sustained expansion of energy drinks and functional beverages, where taurine remains a core functional ingredient alongside caffeine and vitamins. UNESDA, representing the European soft drinks industry, reports that energy drinks account for around 2.5% of the total non-alcoholic beverages market in Europe, and highlights taurine as one of the main ingredients in these products. Scientific opinions by EFSA have concluded that typical taurine exposure from energy drinks at current use levels does not pose a safety concern, confirming a taurine NOAEL of 1,000 mg/kg body weight/day, which is far above normal consumer intakes. This combination of growing category penetration and a clear regulatory safety margin provides beverage players with confidence to continue formulating taurine-containing energy drinks, sports beverages, and ready-to-drink performance products across major markets.

Expanding use in infant nutrition, clinical nutrition, and pet food

A second robust growth driver for the taurine market is its expanding role in infant nutrition, specialized medical nutrition, and pet food, where its physiological importance is well documented. The FAO/WHO Codex Standard for Infant Formula (CODEX STAN 72-1981) permits optional taurine addition up to 12 mg/100 kcal, establishing an international benchmark that many national regulators and manufacturers follow when designing infant and follow-on formulas. A petition to the USDA National Organic Program notes that taurine has been added to conventional and organic infant formulas in the United States since the 1980s to compensate for lower taurine content in bovine-milk-based products, aligning fortification levels with those found in human milk. In pet nutrition, taurine is recognized as an essential nutrient for cats, and the EFSA FEEDAP Panel concluded that feed supplementation up to 0.2% taurine is well tolerated by all animal species, further supporting its significant and rising inclusion in complete pet foods.

Restraints - Regulatory scrutiny and public health concerns surrounding energy drinks

One important restraint is the wider regulatory and public health scrutiny directed at energy drinks as a category, which can indirectly influence taurine demand. Authorities and scientific panels have raised concerns about high consumption of energy drinks, particularly among adolescents, due to combined intake of caffeine, sugar, and other stimulants. While EFSA has concluded that taurine itself is safe at current exposure levels, several countries have implemented stricter labeling rules, marketing restrictions, or voluntary codes of practice for energy drinks, and discussions about age-based sales limitations and caffeine caps remain active. Any tightening of energy drink regulations may dampen volume growth in this application segment, constraining taurine use even if the ingredient’s toxicological profile remains favorable.

Supply-side concentration and exposure to petrochemical input costs

Another restraint arises from the high concentration of taurine production capacity in China and the dependence on synthetic manufacturing routes based on petrochemical intermediates such as ethylene oxide. Industry analyses indicate that most taurine is produced via the ethylene oxide process because of its relatively low cost, high yield, and energy efficiency, but this binds producers to the pricing and availability of upstream petrochemical feedstocks. Chinese manufacturers also face increasingly stringent environmental and safety regulations around handling ethylene oxide and waste streams, which can raise compliance costs and limit the ability to rapidly scale capacity. For downstream users in beverages, nutrition, and pet food, this geographic and process concentration heightens supply risk during periods of energy price volatility, regulatory crackdowns, or logistics disruptions.

Opportunity - Premium nutraceuticals and sports nutrition formulations

A major opportunity for taurine suppliers lies in the premium nutraceutical and sports nutrition segments, where consumers seek science-backed ingredients that support endurance, recovery, and cognitive performance. FDA evaluation of a GRAS notice for taurine in non-carbonated flavored water-based beverages concluded that the proposed use level of 0.0045% and estimated mean daily intakes from beverages, supplements, and diet remain substantially below doses associated with adverse effects, underscoring its favorable safety profile in functional beverages. Scientific literature also links taurine to roles in bile acid conjugation, antioxidant defense, osmoregulation, and membrane stabilization, which sports nutrition brands leverage by incorporating taurine into energy shots, pre-workout blends, and hydration drinks. As the global sports nutrition market shifts toward cleaner labels, reduced sugar, and multifunctional performance benefits, taurine-containing formulations in ready-to-drink beverages, powders, and gels present a strong growth avenue for ingredient manufacturers.

Rapid growth in organized pet food and condition-specific animal nutrition

Another compelling opportunity is the rapid expansion of organized pet food and condition-specific animal nutrition, particularly in emerging markets. Pet ownership has been rising across China, India, and Latin America, and premiumization trends are driving demand for formulated cat and dog foods enriched with functional ingredients. Regulatory and scientific recognition that taurine is essential for cats and beneficial for dogs, with safe supplementation levels identified by the EFSA FEEDAP Panel, underpins its widespread inclusion in complete and balanced pet foods. As brand owners introduce lines targeting cardiac health, senior pets, and indoor cats, taurine is often highlighted on packaging as a key functional nutrient, creating opportunities for taurine suppliers to partner with major pet food manufacturers, develop tailored feed-grade specifications, and secure long-term supply contracts in this fast-growing application area.

Category-wise Analysis

Form Insights - Powder form as the dominant delivery format

Within the taurine market, the powder form is the leading segment, estimated to have a roughly 78% share of global volume in 2025. Taurine powder offers high stability, long shelf life, and excellent compatibility with dry blending processes used in energy drink premixes, dietary supplement tablets and capsules, infant formula bases, and compound feeds. Major Chinese producers such as Qianjiang Yongan Pharmaceutical Co., Ltd. emphasize large-scale production of crystalline taurine powder, with capacities reported at around 58,000 tons per year and exports to the food, health products, feed, and pet food industries worldwide. Powdered taurine can be precisely metered into formulation lines and is easier to store and transport than liquid solutions, making it the preferred choice for multinational beverage and nutrition brands operating complex, multi-plant supply chains. The liquid segment is expected to grow faster from a smaller base, driven by its use in certain beverage manufacturing systems and integrated dosing solutions.

Source Insights - Synthetic taurine as the primary and most scalable source

By source, synthetic taurine overwhelmingly dominates the market, likely contributing more than 85-90% of global supply in 2025, due to its cost-effectiveness, scalability, and consistent purity. Industry reports on the taurine sector in China indicate that the ethylene oxide process is the mainstream manufacturing route, chosen for its relatively low unit production cost, high yields, and manageable energy requirements. Leading producers such as Qianjiang Yongan Pharmaceutical operate integrated plants that have achieved certifications including GMP, ISO9001, ISO22000, BRC, HALAL, and KOSHER, enabling them to supply food-, feed-, and pharma-grade synthetic taurine to international customers. Natural taurine, previously sourced from animal tissues, has largely fallen out of favor due to ethical concerns, complexity of extraction, and higher costs, and is now mainly confined to niche or research applications. As global demand rises from beverages, infant formula, and pet nutrition, synthetic taurine is expected to retain its dominant position while incremental interest in “naturally positioned” solutions may spur limited innovation in alternative pathways.

Application Insights - Energy drinks leading, pharmaceuticals emerging as fastest-growing segment

Among applications energy drinks constitute the leading segment, accounting for 28% of taurine demand in 2025, driven by taurine’s established role as a hallmark ingredient in many global and regional energy drink brands. UNESDA characterizes energy drinks as functional beverages that typically contain caffeine, taurine, vitamins, and other substances with nutritional or physiological effects, and notes that these products represent roughly 2.5% of the non-alcoholic beverages market in Europe. EFSA’s scientific opinion on caffeine and taurine, combined with national regulatory decisions, has effectively endorsed taurine’s continued use in energy drinks at current concentrations, helping maintain its central role in product positioning around alertness and performance. The pharmaceuticals segment is projected to be the fastest-growing application, supported by taurine’s incorporation into liver health tonics, cardioprotective formulations, ophthalmic solutions, and parenteral nutrition products in several Asian markets with emerging research suggesting potential benefits in cardiovascular, metabolic, and neurological health.

Regional Insights

North America Taurine Market Trends and Insights

North America represents a leading region in the taurine market, driven by strong demand from the energy drinks, dietary supplements, and functional food industries. The region benefits from a well-established beverage sector, where taurine is widely used in energy drinks and performance-enhancing formulations. High consumer awareness regarding fitness, mental alertness, and preventive healthcare continues to support taurine-based supplement sales. The growing sports nutrition culture, particularly in the U.S., has further strengthened product innovation and premium formulations containing amino acids like taurine. Additionally, the expansion of clean-label and fortified food trends is encouraging manufacturers to incorporate taurine into functional snacks and ready-to-drink beverages. The pharmaceutical sector also contributes steadily, with taurine being explored for cardiovascular and metabolic health applications. Strong distribution networks, advanced manufacturing capabilities, and regulatory clarity regarding food additives provide a favorable business environment. Rising pet humanization trends in the U.S. and Canada are also increasing taurine demand in premium pet food products, reinforcing North America’s dominant position in the global taurine market.

Asia Pacific Taurine Market Trends and Insights

Asia Pacific is emerging as a high-growth region in the taurine market, supported by expanding food processing, pharmaceutical manufacturing, and rising health awareness across developing economies. Countries such as China, Japan, India, and South Korea are witnessing increasing consumption of energy drinks, fortified beverages, and dietary supplements containing taurine. Rapid urbanization, growing disposable incomes, and a younger population base are fueling demand for functional drinks and sports nutrition products. The region also benefits from strong domestic production capabilities, particularly in China, which acts as a major global exporter of synthetic taurine. In addition, rising infant nutrition awareness is driving taurine inclusion in infant formula products across Southeast Asia. Pharmaceutical research and generic drug manufacturing expansion further contribute to regional demand. The growing pet ownership trend, especially in urban China and Japan, is increasing taurine use in premium pet food formulations. Overall, improving healthcare access, manufacturing cost advantages, and expanding retail distribution networks position Asia Pacific as a fast-growing and strategically important taurine market.

Competitive Landscape

The taurine market competition landscape is characterized by intense rivalry among ingredient suppliers, driven by product quality, cost efficiency, and formulation expertise. Key players compete based on production capacity, spectrum of product grades (food, pharmaceutical, and feed), and geographic reach. Market differentiation increasingly comes from compliance with stringent regulatory standards and the ability to supply consistent, high-purity taurine for diverse end uses such as beverages, supplements, and pet nutrition. Strategic partnerships with beverage and nutraceutical manufacturers, along with expanded distribution networks, further shape competitive positioning. Price fluctuations in raw materials and economies of scale also influence competitive advantage, making innovation and operational efficiency critical for sustained leadership in the global taurine market.

Key Developments:

- In September 2025, LG Chem announced that it had launched the UK Taurokit 2% solution for injection in South Korea, marking a strategic entry into the surgical antimicrobial segment. The product, developed in collaboration with UK Chemiphar and recently approved for clinical use, was positioned as an advanced antimicrobial drug to help prevent surgical site infections, particularly in complex procedures.

Companies Covered in Taurine Market

- Yongan Pharmaceutical Co., Ltd.

- Grand Pharma (China)

- Jiangyin Huachang Food Additive Co., Ltd.

- Taisho Pharmaceutical Co., Ltd.

- Huanggang Fuchi Pharmaceutical

- Jiangsu Yuanyang Pharmaceutical Co., Ltd.

- Zhangjiagang Duling Food Co.

- Hubei Xinxin Pharmaceutical

- Evonik Industries AG, Kemin Industries Inc.

- Lonza Group, Sigma-Aldrich / Merck Group

- Zhejiang NHU Co., Ltd.

- Kyowa Hakko Bio Co., Ltd.

- AlzChem Group AG

- Henan Eastar Chem. & Tech. Co., Ltd.

- Shandong WorldSun Biological Technology Co., Ltd.