- Food Ingredients & Additives

- Taste Modulators Market

Taste Modulators Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Taste Modulators Market by Product Type (Sweet Modulators, Salt Modulators, Fat Modulators), Source (Natural, Synthetic), Application (Food, Beverages), and Regional Analysis from 2026 - 2033

Taste Modulators Market Share and Trends Analysis

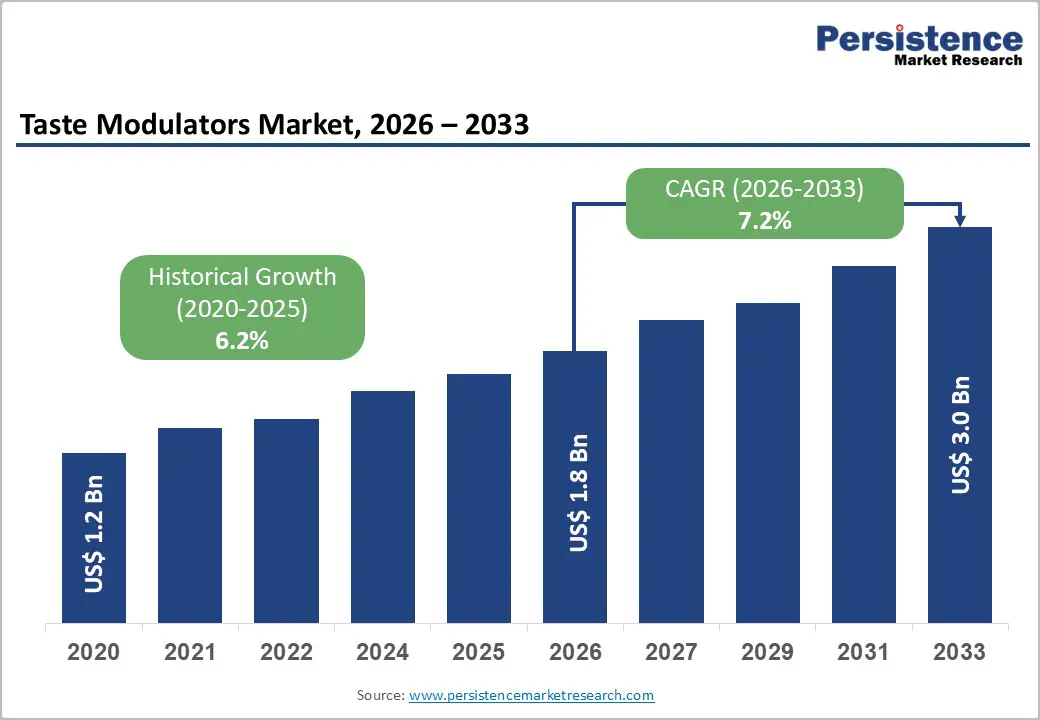

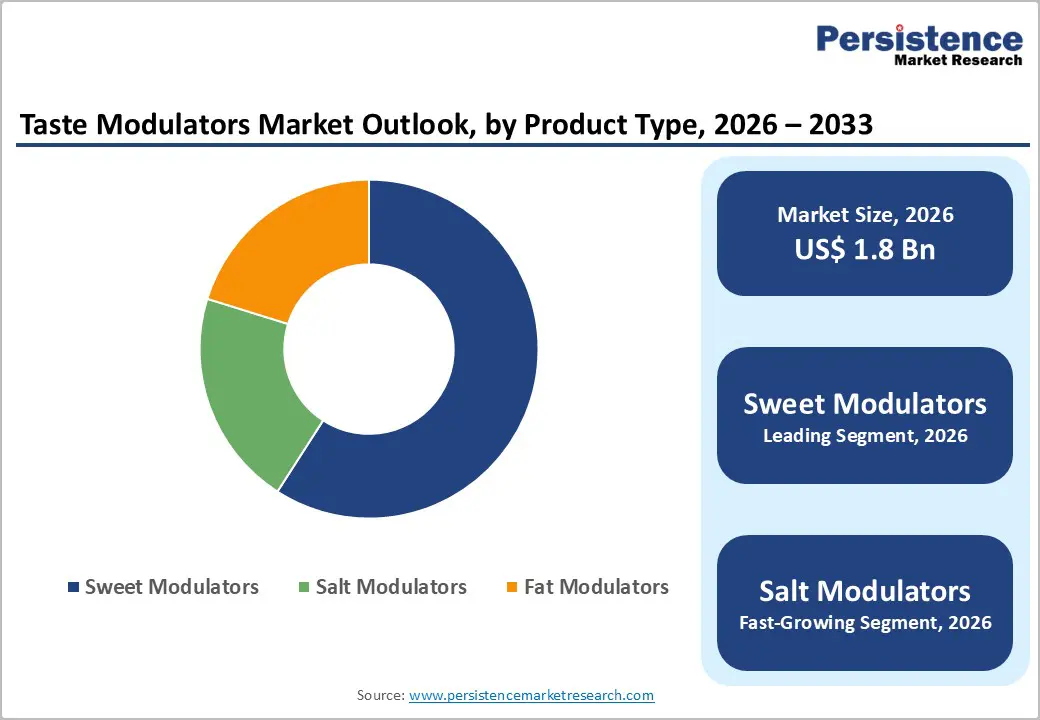

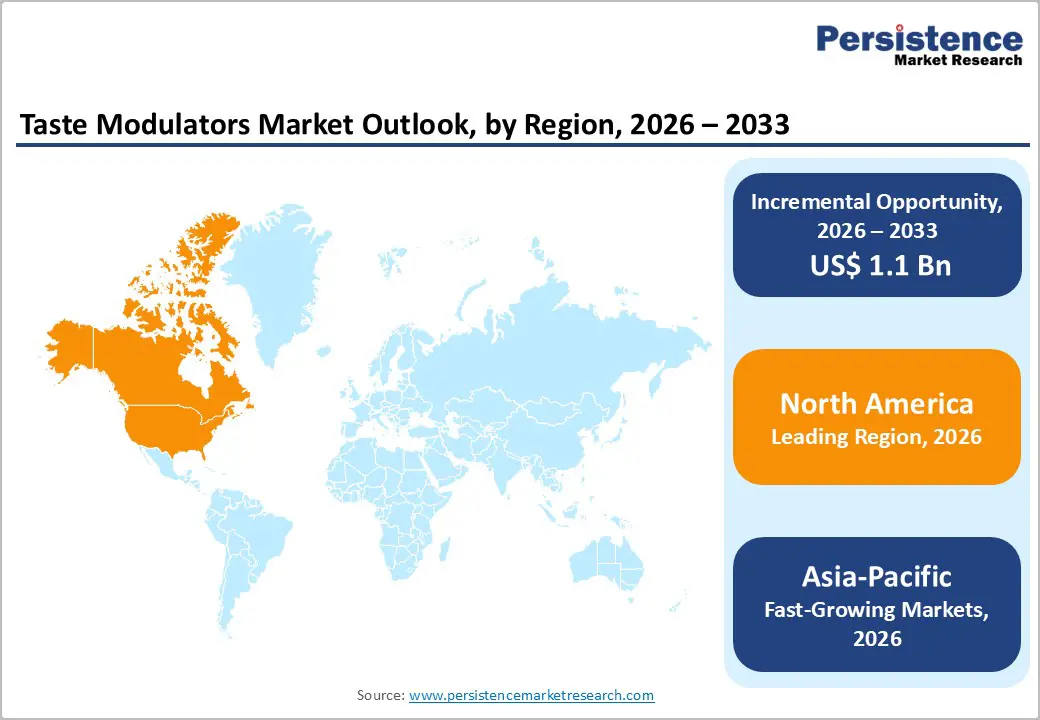

The global taste modulators market is estimated to grow from US$ 1.8 billion in 2026 to US$ 3.0 billion by 2033 and is projected to record a CAGR of 7.2% during the forecast period from 2026 to 2033.

It is growing steadily, driven by rising awareness of digestive health, demand for functional foods, and dietary supplement consumption. North America leads due to high nutraceutical adoption, while Asia-Pacific grows fastest, driven by urbanization, shifting diets, and health-conscious consumers. Increasing regulatory support and clean-label trends further boost market expansion globally.

Key Industry Highlights:

- Dominant Product: Sweet modulators held the largest share, 59.1%, in 2025, driven by demand for sugar reduction in foods, beverages, and confectionery.

- Regional Leadership: North America led the market in 2025 with 34.0% share, supported by strong health awareness and reformulation trends.

- Growth Indicators: Growth is fueled by sugar and sodium reduction initiatives, rising demand for functional foods, and clean-label trends.

- Market Opportunity: Opportunities exist in salt modulators, expansion in Asia-Pacific, product innovation, personalized nutrition, and broader use in beverages, snacks, and supplements.

| Key Insights | Details |

|---|---|

|

Taste Modulators Market Size (2026E) |

US$ 1.8 Bn |

|

Market Value Forecast (2033F) |

US$ 3.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.2% |

Market Dynamics

Driver: Rising Demand for Sugar and Salt Reduction

Global health bodies have underscored the urgency of reducing dietary intake of sugar and sodium to curb non-communicable diseases. The World Health Organization (WHO) recommends that free sugars contribute no more than 10% of total daily energy intake, and ideally under 5% (about 25g/day) to help reduce obesity and diabetes risks. Similarly, WHO guidelines advise limiting sodium intake to less than 2g/day (approximately 5kg of salt) to reduce hypertension and subsequent cardiovascular disease risk. Real-world consumption patterns far exceed these limits in many countries, particularly in processed foods and sugar-sweetened beverages, which remain staples of contemporary diets. This gap between recommendations and actual consumption is prompting national health agencies and industry groups to push for reformulation targets and voluntary reduction initiatives, directly heightening the need for effective taste modulation solutions.

Food and beverage manufacturers respond to regulatory pressure and consumer demand for healthier products by reformulating recipes to reduce sugar and salt while preserving palatability. Taste modulators, ingredients that enhance perceived sweetness or saltiness without increasing actual sugar or sodium content, have become essential tools in these reformulation strategies. Their adoption enables companies to deliver “reduced sugar” or “low-sodium” labels without significantly compromising flavor, which is crucial for consumer acceptance and repeat purchases. As health awareness increases, with a large proportion of consumers indicating a preference for lower-sugar, lower-salt versions of familiar products, the use of modulators in beverages, snacks, and plant-based foods continues to grow.

Restraint: High Cost of Taste Modulator Ingredients

The development and production of effective taste modulators often entail higher costs than those of conventional flavor enhancers or basic salt and sugar ingredients. This is especially true for natural or plant-based modulators, where raw materials and extraction processes are complex, resource-intensive, and seasonally variable. For example, some botanical extract sources used for natural modulation may cost 5–7 times as much as synthetic alternatives, imposing a significant cost premium on finished modulators. Additionally, extraction yields for high-performance modulators (e.g., steviol glycosides from plant leaves) can be low, sometimes only 2–3% of raw material mass, meaning large volumes of plant input and processing are required, which increases production expenses.

These elevated ingredient costs translate into higher formulation and final product prices, which can restrict adoption by price-sensitive manufacturers and consumers, particularly in emerging markets. May food formulators be reluctant to incorporate high-cost modulators when lower-cost synthetic flavor enhancers or sugar/sodium replacements are available, even if they do not align with clean-label trends. Furthermore, variability in natural ingredient supply chains, driven by seasonal and geographic factors, can cause price volatility, further constraining consistent production planning. This cost dynamic may reduce the widespread utilization of taste modulators, particularly in mass-market, low-margin products where cost pressures are acute.

Opportunity: Innovation in Plant-Based and Natural Modulators

Consumer preference for clean-label, plant-based, and natural ingredients is reshaping product development in the food and beverage industry. Many manufacturers now actively seek alternatives to artificial additives, aligning with global trends toward wellness and sustainability. Natural taste modulators derived from botanical extracts, fermentation-based systems, and plant proteins offer a pathway to achieve desirable sensory profiles while maintaining minimal, recognizable ingredient lists. Recent analyses indicate that botanical extracts alone account for a substantial share (e.g., around 33%) of natural flavor modulator solutions used in industry formulations, reflecting a rising willingness among developers to invest in nature-derived sensory tools.

This shift toward plant-based taste modulation extends beyond sweetness enhancement to include bitterness masking and flavor balancing in plant proteins, fortified beverages, and alternative dairy products. In 2024, a significant proportion (over 65%) of new plant-based product launches featured taste modulators to improve mouthfeel and sensory acceptance, especially in products that use high-protein or fortified matrices where off-notes are common. Such trends underscore a major opportunity: by innovating novel natural modulators, including those tailored to specific flavor challenges ingredient suppliers can help food brands meet both nutritional and sensory expectations of increasingly health-oriented consumers. This opportunity is amplified by demand in functional foods, beverages, and dietary supplements, where taste remains a primary driver of consumer choice.

Category-wise Analysis

By Product Type Insights

Sweet modulators dominate because excess sugar consumption remains a global public health concern, driving reformulation across foods and beverages. The World Health Organization (WHO) reports that average global added sugar intake often exceeds recommendations, contributing to obesity and type 2 diabetes. WHO guidelines state that free sugars should account for less than 10% of total energy intake, with an ideal target of 5%, but many diets exceed this. As a result, food manufacturers are reformulating products to lower sugar while maintaining taste, relying on sweet taste modulators. For example, sugar-sweetened beverages and confectionery are major contributors to daily sugar intake, saw increased scrutiny by health authorities, leading to sugar-reduction policies in countries like the UK and US. This regulatory and consumer pressure creates higher demand for sweet modulators, making them the largest product type segment in the market.

By Source Insights

Natural taste modulators dominate because consumer preference for clean-label and recognizable ingredients has surged globally. Surveys conducted by credible nutrition and food policy organizations consistently show that a majority of consumers prefer products with natural ingredients, associating them with better health and transparency. For instance, a 2023 International Food Information Council (IFIC) survey found that over 70% of U.S. consumers actively look for products with natural ingredients or minimal processing. Regulatory guidance, such as the FDA’s emphasis on transparent labeling, reinforces this trend. Additionally, natural sweeteners and plant-derived peptides, such as stevia and monk fruit, are widely accepted in functional foods and beverages and align with health-oriented diets. This strong consumer and regulatory bias toward natural sources contributes to their dominance in the taste modulators market.

Regional Insights

North America Taste Modulators Market Trends

North America’s dominance in the taste modulators market is strongly linked to dietary patterns and public health priorities in the United States and Canada, where highly processed foods contribute a large portion of daily caloric intake. According to the Centers for Disease Control and Prevention (CDC), more than 55% of calories consumed by Americans come from ultra-processed foods items high in sugar, salt, and additives that drive demand for improved taste profiles when reformulated toward healthier versions. The U.S. Dietary Guidelines now emphasize limiting added sugars and sodium to support health outcomes, encouraging product reformulation across food categories to meet these targets. As manufacturers work to reduce sugar and salt while maintaining palatability, the adoption of taste modulators has accelerated, making North America the largest regional market.

Europe Taste Modulators Market Trends

Europe plays a significant role in the taste modulators market due to longstanding public health nutrition initiatives and industry reformulation frameworks. The European Union’s common salt reduction framework sets coordinated targets to cut salt intake across major food categories including bread, cheeses, and ready meals, aiming for measurable reductions at the population level. Many EU member states also include added sugar reduction and reformulation strategies in national nutrition plans to align diets with WHO and EFSA dietary recommendations that limit added sugars and unhealthy ingredients. The emphasis on nutrient-balanced diets and reduction of risk factors for noncommunicable diseases has led European food manufacturers to integrate taste modulation technologies into healthier product formulations, reinforcing Europe’s strategic position in this market.

Asia Pacific Taste Modulators Market Trends

Asia Pacific is the fastest-growing region in the taste modulators market, driven by rapid urbanization, changing dietary habits, and growing demand for health and wellness foods. Across countries such as China, Japan, India, and Australia, consumers increasingly seek functional foods, fortified beverages, and products supporting immune and digestive health, reflecting a shift toward preventive nutrition. Large middle-class populations with rising disposable incomes are adopting Westernized diets with higher consumption of processed and convenience foods, which increases awareness of the need for healthier alternatives formulated with lower sugar and sodium. At the same time, governments in the region are intensifying public health campaigns and dietary guidelines aimed at improving nutrition outcomes, sparking growth in health-oriented food innovation, and creating favorable conditions for the adoption of taste modulators.

Competitive Landscape:

The taste modulators market is competitive, driven by key players emphasizing product innovation, functional benefits, and expanded applications. Companies focus on developing soluble and specialty modulators, increasing production capacity, ensuring regulatory compliance, and strengthening distribution to meet growing demand across functional foods, beverages, dietary supplements, and pharmaceutical products worldwide.

Key Developments:

- In October 2025, Symrise invested in Cellibre, a U.S.-based biotechnology company, to strengthen its capabilities in taste balancing and cosmetic actives. The partnership aimed to accelerate innovation by leveraging Cellibre’s biotech expertise, enabling Symrise to develop advanced solutions for flavor modulation and functional cosmetic ingredients.

- In January 2024, Ingredion launched its PureCircle Clean Taste Solubility Solution, designed to enhance taste and solubility in reduced-sugar and sugar-replacement formulations. The solution aimed to improve sweetness perception and product stability across beverages, functional foods, and other applications, helping manufacturers deliver clean-label, lower-sugar products without compromising flavor.

Companies Covered in Taste Modulators Market

- Kerry Group

- Symrise AG

- International Flavors & Fragrances Inc.

- Cargill, Incorporated

- Ingredion Incorporated

- Givaudan S.A.

- Koninklijke DSM NV

- Tate & Lyle

- Corbion

- Archer Daniels Midland Company

- Sensient Technologies Corp.

- The Flavor Factory

- Apura Ingredients, Inc.

- Flavorchem & Orchidia Fragrances

- Carmi Flavor & Fragrance Co., Inc.

- Others

Frequently Asked Questions

The global taste modulators market is projected to be valued at US$ 1.8 Bn in 2026.

Rising sugar and salt reduction demand, health awareness, functional foods growth, and clean-label trends drive the market growth.

The global taste modulators market is poised to witness a CAGR of 7.2% between 2026 and 2033.

Expansion in Asia Pacific, plant-based innovations, personalized nutrition, clean-label products, and applications in supplements and beverages.

Kerry Group, Symrise AG, International Flavors & Fragrances Inc., Cargill, Incorporated, Ingredion Incorporated, and Givaudan S.A.