- Automotive Components & Materials

- Sway Bar Market

Sway Bar Market Size, Share, and Growth Forecast 2026 - 2033

Sway Bar Market by Product Type (Solid and Hollow), Material Type (Aluminum and Steel), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and Heavy Commercial Vehicles), Sales Channel (OEM and Aftermarket), and geographic regions including North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, extending through 2033.

Sway Bar Market Size and Trend Analysis

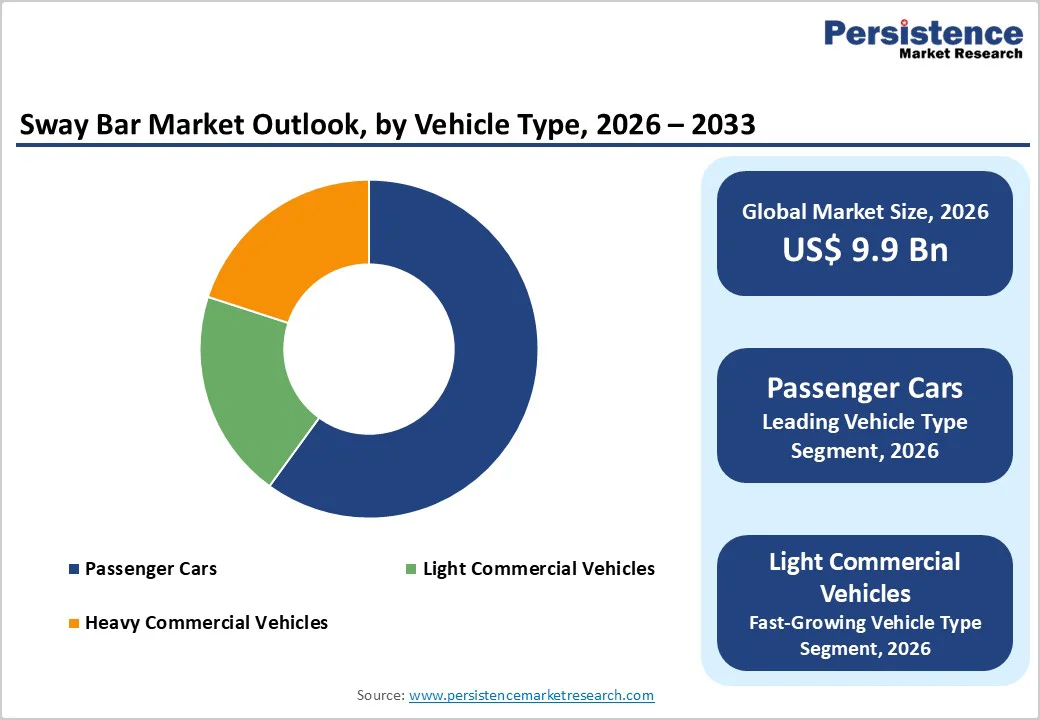

The global sway bar market size is expected to be valued at US$ 9.9 billion in 2026 and projected to reach US$ 14.7 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033.

The expansion of this market is driven by increasing production of light and heavy commercial vehicles, accelerating adoption of electric vehicles that require advanced suspension components, and growing consumer demand for enhanced vehicle stability and handling performance. Additionally, stringent regulatory frameworks governing vehicle safety and performance standards across major automotive markets are compelling manufacturers to integrate higher-quality sway bar systems into their vehicle architectures. The surge in vehicle electrification, particularly the 40% year-over-year growth in electric vehicle sales in 2024, has created substantial demand for specialized suspension components to manage the unique weight distribution of battery-laden vehicles.

Key Market Highlights

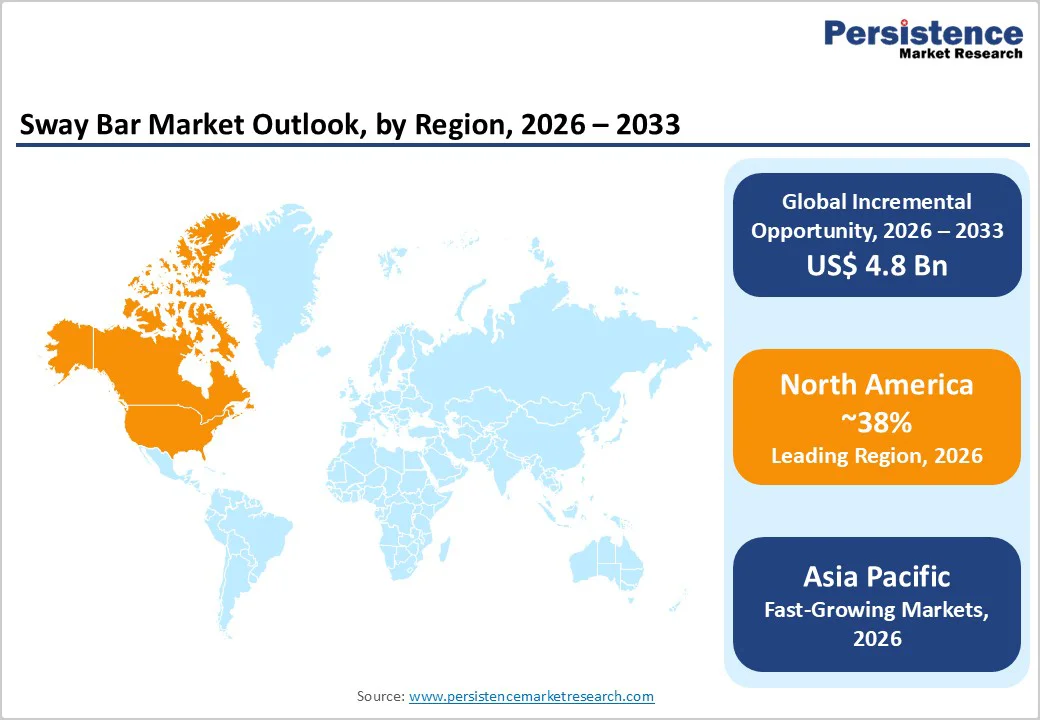

- Leading Region: North America dominates the global sway bar market with approximately 38% market share in 2025, driven by exceptional vehicle production volumes, substantial aftermarket infrastructure, and high consumer demand for premium suspension components supporting diverse vehicle categories including pickup trucks and sport utility vehicles.

- Fastest Growing Region: Asia Pacific is projected to expand at 6.8% CAGR through 2033, led by China’s unprecedented vehicle manufacturing capacity, India’s emerging logistics networks, and the rapid transition toward electric vehicle platforms across the region, creating substantial component demand.

- Dominant Segment from Product Type: Hollow sway bars command 62% market share in 2025, delivering 20-50% weight reductions compared to solid alternatives while maintaining equivalent torsional rigidity, making them preferred choice for lightweight vehicle development initiatives.

- Fastest Growing Segment from Material Type: Aluminum material segment is projected to expand at 6.8% CAGR through 2033, driven by electric vehicle weight optimization requirements, premium vehicle manufacturing, and superior corrosion resistance characteristics supporting extended component service life.

- Key Market Opportunity: The aftermarket performance modification segment is the fastest-growing sales channel, with a 8.5% CAGR through 2033, driven by vehicle fleet aging, growing consumer awareness of suspension maintenance, and the expansion of digital distribution channels, which enable direct access to performance enthusiasts and specialized retailers.

| Key Insights | Details |

|---|---|

| Sway Bar Market Size (2026E) | US$ 9.9 billion |

| Market Value Forecast (2033F) | US$ 14.7 billion |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Dynamics

Market Growth Drivers

Rising Demand from Sport Utility Vehicles and Light Commercial Vehicles

The automotive market has witnessed a paradigm shift toward larger vehicle categories, with SUVs and pickups commanding a record 79% share of new vehicle sales in the United States, according to the Cox Automotive 2023 U.S. Auto Market Review. This structural transformation in consumer preferences creates elevated demand for robust suspension systems, particularly sway bars, which are essential in controlling body roll and maintaining vehicle stability in these higher-center-of-gravity platforms. Light commercial vehicles, which carry substantial cargo loads and operate under demanding conditions, require specialized sway bar formulations with enhanced durability and stress resistance.

The expanding global logistics sector, fueled by the exponential growth of e-commerce and last-mile delivery networks, has resulted in unprecedented fleet expansion, particularly in Asia-Pacific and emerging markets, where light commercial vehicle production is projected to grow at 8.0% CAGR through 2033. These vehicle categories inherently place greater demands on suspension component manufacturers to develop systems that deliver superior handling characteristics without compromising ride comfort, thereby creating sustained demand across both original equipment and replacement channels.

Electric Vehicle Proliferation and Advanced Suspension Requirements

The accelerating global transition toward electric vehicle adoption represents a transformative growth catalyst for the sway bar market, as these advanced powertrains impose unique engineering requirements on suspension systems. According to the International Energy Agency Global EV Outlook 2024, electric vehicle sales reached approximately 17 million units by the end of 2024, creating a rapidly expanding baseline for specialized suspension components. Electric vehicles present distinct challenges due to their concentrated mass distribution, with heavy battery packs positioned in the vehicle floor, creating substantially different weight characteristics compared to conventional internal combustion engine vehicles.

Automotive original equipment manufacturers are allocating substantial resources to suspension system innovation, with US$200 billion committed to electric vehicle development through 2025, according to McKinsey research. Manufacturers are increasingly integrating lightweight materials, including aluminum and carbon fiber composites, into sway bar assemblies, achieving approximately 15% weight reductions while maintaining structural integrity and performance specifications required for modern electric platforms.

Market Restraints

Raw Material Price Volatility and Supply Chain Disruption

The sway bar manufacturing sector faces significant headwinds from volatile commodity markets, which are affecting fundamental input materials, particularly natural rubber and petrochemical derivatives essential for bushing components. According to the Association of Natural Rubber Producing Countries (ANRPC), global natural rubber demand reached 13.9 million tons in 2024, significantly exceeding the production capacity of 12.7 million tons, creating persistent cost pressures and supply scarcity risks. This structural imbalance in the natural rubber market forces component manufacturers to navigate unpredictable pricing fluctuations that compress profit margins and complicate long-term supply agreements with automotive original equipment manufacturers.

The elevated costs of premium materials required for electric vehicle suspension systems, particularly high-strength steel and specialty alloys, represent additional financial burdens that potential suppliers must absorb in an increasingly price-competitive market. Many supply agreements lack flexible pricing mechanisms, obligating suppliers to bear the financial burden of sudden commodity price spikes, thereby limiting their capacity to invest in capacity expansion or pursue research and development initiatives essential for technological advancement.

Intense Market Competition and Pricing Pressure

The sway bar market exhibits elevated competitive intensity, with numerous manufacturers competing aggressively on pricing while simultaneously attempting to differentiate through technological innovation and quality enhancements. Original equipment manufacturers maintain significant bargaining power in supplier relationships, continuously exerting downward pressure on component pricing to optimize their own cost structures and profitability metrics.

The proliferation of aftermarket alternatives and the emergence of low-cost manufacturers from developing economies intensify competitive pressures, forcing established market participants to invest continuously in process optimization and product innovation to maintain their competitive positions without sacrificing quality standards or operational profitability.

Market Opportunities

Lightweight Materials and Sustainability-Driven Innovation

The global automotive industry’s commitment to sustainability and regulatory compliance regarding emissions reduction creates unprecedented opportunities for sway bar manufacturers to develop innovative solutions utilizing advanced lightweight materials. The European Union’s CO2 emission targets requiring 95 g/km by 2025 have catalyzed substantial investments in lightweight component development, with manufacturers achieving 15% weight reductions through advanced material integration while maintaining structural performance specifications. Carbon fiber composites, aluminum alloys, and engineered polymers present compelling alternatives to conventional steel sway bars, enabling manufacturers to capture premium market segments willing to invest in performance enhancements and environmental responsibility.

The integration of bio-based and recyclable elastomer materials represents an emerging frontier, with manufacturers increasingly replacing conventional petrochemical derivatives with sustainable alternatives derived from renewable sources. This technological evolution aligns with corporate carbon neutrality commitments and consumer preferences for environmentally responsible automotive components, positioning early adopters as category leaders in the rapidly growing sustainable suspension market segment. Research and development investments in novel materials and manufacturing processes promise to unlock significant market expansion opportunities, particularly in developed markets where environmental consciousness drives purchasing decisions.

Aftermarket Growth and Vehicle Fleet Maintenance Requirements

The expansion of the global vehicle fleet and the increasing average age of vehicles in circulation present substantial opportunities for aftermarket sway bar component sales and replacement services. The United States automotive aftermarket industry is valued at an estimated US$ 534 billion, according to the Auto Care Association 2024 report, providing a stable economic foundation for suspension component replacements and upgrades. Growing consumer awareness of suspension system maintenance, combined with improved internet-based information access, is driving increased adoption of aftermarket performance upgrades among vehicle enthusiasts and professional fleet operators alike.

Heavy commercial vehicle operators, tasked with maintaining aging fleets while managing total cost of ownership, increasingly recognize the value proposition of high-quality replacement sway bars that enhance vehicle stability and extend the overall service life of the suspension system. Performance enthusiasts represent another significant market segment actively seeking specialized sway bar upgrades that deliver enhanced handling characteristics and cornering performance, with community discussions across automotive forums and social media platforms demonstrating consistent and growing demand for premium aftermarket suspension solutions.

Category-wise Insights

Product Type Analysis

Hollow sway bars dominate the product type category, accounting for nearly 62% of market share in 2025, driven by their ability to deliver high torsional stiffness with significantly lower weight than solid alternatives. Their tubular construction allows manufacturers to meet handling and stability requirements while supporting vehicle lightweighting objectives. Weight reductions of up to 20–50% directly contribute to improved fuel efficiency, extended electric vehicle range, and enhanced driving dynamics. As OEMs increasingly prioritize mass reduction across new vehicle platforms, hollow sway bars are becoming the preferred standard, particularly in premium and performance-oriented models. This segment is projected to grow at a 6.2% CAGR through 2033, reflecting sustained adoption across both internal-combustion and electric-vehicle architectures.

Material Type Analysis

Steel remains the leading material in the sway bar market, holding approximately 74% share in 2025 due to its optimal balance of strength, stiffness, durability, and cost efficiency. High-strength and alloy steel grades provide excellent torsional performance, fatigue resistance, and vibration control under diverse driving conditions. Steel’s compatibility with established manufacturing processes and its recyclability further reinforce its widespread adoption across OEM and aftermarket channels. Continuous improvements in steel metallurgy enable weight optimization without compromising structural integrity, supporting ongoing relevance despite lightweighting trends. As a result, steel remains the material of choice for high-volume vehicle platforms requiring reliable, cost-effective suspension components.

Vehicle Type Analysis

Passenger cars represent the largest vehicle type segment, accounting for nearly 68% of sway bar demand in 2025, supported by high global production volumes and the universal integration of suspension across vehicle classes. From compact cars to premium sedans and SUVs, passenger vehicles rely on sway bars to meet safety, ride comfort, and handling performance requirements. OEMs place strong emphasis on suspension tuning in this segment to comply with regulatory standards and meet consumer expectations for stability and driving dynamics. The dominance of passenger cars ensures consistent, large-scale demand for sway bars, making this segment central to volume-driven market growth.

Sales Channel Analysis

The OEM channel leads the sway bar market, capturing around 70% share in 2025, reflecting the sway bar's critical role in new vehicle assembly. OEM procurement emphasizes long-term supply contracts, stringent quality standards, and close engineering collaboration, positioning sway bar suppliers as strategic partners. High-volume production programs provide demand stability and predictable revenue streams for manufacturers. Integration at the design stage allows sway bars to be optimized for vehicle-specific performance and safety targets. As vehicle platforms become more complex, especially with electrification, the OEM channel remains the primary driver of technological advancement and sustained market demand.

Regional Insights

North America Sway Bar Market Trends and Insights

North America remains the largest sway bar market, accounting for roughly 38% of global demand in 2025, supported by high vehicle ownership, strong production volumes, and a mature aftermarket ecosystem. The region’s vehicle mix is heavily skewed toward SUVs and light trucks, driving sustained demand for robust suspension systems that manage higher vehicle weight and stability requirements. Consumers in the region show a strong willingness to invest in suspension upgrades, reinforcing steady aftermarket sales through specialty retailers and digital platforms.

Regulatory emphasis on vehicle safety and performance standards continues to encourage OEMs to integrate advanced suspension components at the design stage. The aging vehicle fleet further supports replacement demand, while electrification policies and infrastructure investments are accelerating the transition toward electric platforms that require redesigned sway bar architectures. Overall, North America combines stable OEM demand with a dynamic aftermarket, creating a structurally balanced and resilient regional market.

Europe Sway Bar Market Trends and Insights

Europe is the second-largest sway bar market, characterized by strict environmental regulations, high safety standards, and strong demand for precise vehicle handling. Regulatory pressure to reduce vehicle emissions has accelerated the adoption of lightweight suspension components, positioning sway bars as critical contributors to overall vehicle efficiency. The region’s automotive industry is dominated by premium and performance-oriented vehicle platforms, where advanced suspension tuning plays a central role in differentiation.

High electric vehicle penetration further supports demand for innovative sway bar designs optimized for battery weight distribution and chassis dynamics. Western Europe continues to lead in technology development, while Eastern Europe is emerging as a high-growth manufacturing hub due to rising production capacity and cost competitiveness. European suppliers increasingly emphasize sustainable manufacturing practices, advanced materials, and modular designs to align with evolving regulatory and OEM requirements, reinforcing the region’s focus on innovation-led growth.

Asia Pacific Sway Bar Market Trends and Insights

Asia Pacific is the fastest-growing regional market, projected to expand at a 6.8% CAGR through 2033, driven by large-scale automotive production, rapid industrialization, and expanding commercial vehicle fleets. The region dominates global vehicle manufacturing volumes, generating consistent OEM demand for suspension components across passenger and commercial segments. Accelerated electric vehicle adoption, supported by policy incentives and cost-efficient manufacturing, is increasing demand for sway bars optimized for electrified platforms.

India is emerging as a high-growth market due to logistics expansion and rising light commercial vehicle production, while Japan and South Korea continue to lead in advanced suspension engineering. Abundant raw material availability and localized supply chains further enhance regional cost competitiveness, positioning the Asia Pacific as the primary growth engine of the global sway bar market.

Competitive Landscape

The global sway bar market demonstrates a moderately consolidated structure, characterized by a clear tiered hierarchy of large original equipment suppliers and a fragmented base of regional and specialized players. Leading suppliers benefit from scale-driven cost efficiencies, long-term OEM contracts, and vertically integrated manufacturing, enabling consistent quality and high-volume supply. Smaller and mid-sized participants compete through product differentiation, customization, and aftermarket-focused strategies, targeting performance enhancement and vehicle-specific applications.

Competitive strategies increasingly prioritize the adoption of lightweight materials, process automation, and sustainable manufacturing practices to meet evolving regulatory and OEM requirements. Market participants are also strengthening positions through selective mergers, partnerships, and technology collaborations aimed at accelerating innovation and expanding geographic reach. In parallel, the aftermarket segment is witnessing structural shifts toward direct-to-consumer and digital distribution models, allowing manufacturers to improve margins and customer engagement.

Key Market Developments

- July 2025: ZF Friedrichshafen AG introduced its new Smart Chassis Sensor integrated directly into ball joints of independent suspension systems, enabling precise wheel-to-body motion measurement and improving suspension control while reducing separate sensor requirements.

- March 2025: SuperPro Suspension launched a comprehensive range of sway bars and bushings specifically engineered for the BMW 1 Series, incorporating proprietary Roll Control technology designed to enhance steering response and reduce body roll without compromising ride comfort.

- June 2024: DRiV Incorporated, a Tenneco subsidiary, announced major expansion of its Monroe Steering and Suspension product line, highlighting intelligent bushings that improve LiDAR sensor accuracy by minimizing chassis vibrations, representing significant advancement toward active suspension solutions.

Companies Covered in Sway Bar Market

- ZF Friedrichshafen AG

- CARROSSER Co. Ltd.

- Sikky Manufacturing

- Hellwig Products Company, Inc.

- Tanabe USA Inc.

- Whiteline USA

- ADDCO Manufacturing Company, Inc.

- Mubea

- Swaytec Co. Ltd.

- Nengun Co. Ltd.

- TSL Turton Ltd.

- Ridetech

- MOOG

- Alta Performance

- Superpro Europe Ltd.

- Dorman Products, Inc.

- Schaeffler AG

- Continental AG

- KYB Corporation

- NHK Spring Co., Ltd.

Frequently Asked Questions

The global sway bar market is projected to reach approximately US$ 9.9 billion in 2026.

Key drivers include rising SUV and LCV sales, rapid electric vehicle adoption, stringent safety regulations, and demand for improved vehicle handling.

North America leads the market, accounting for about 38% of global share.

The aftermarket segment presents the strongest opportunity, growing at around 8.5% CAGR.

Key companies include ZF Friedrichshafen AG, Mubea, Hellwig Products, Whiteline, Superpro, MOOG, and Dorman Products.