- Food Packaging

- Spout Pouches Market

Spout Pouches Market Size, Share, and Growth Forecast, 2026 - 2033

Spout Pouches Market By Product Type (Beverages, Cleaning Solutions, Others), Material (Plastic, Aluminum, Others), End-user Industry, Structure, and Regional Analysis for 2026 - 2033

Spout Pouches Market Size and Trends Analysis

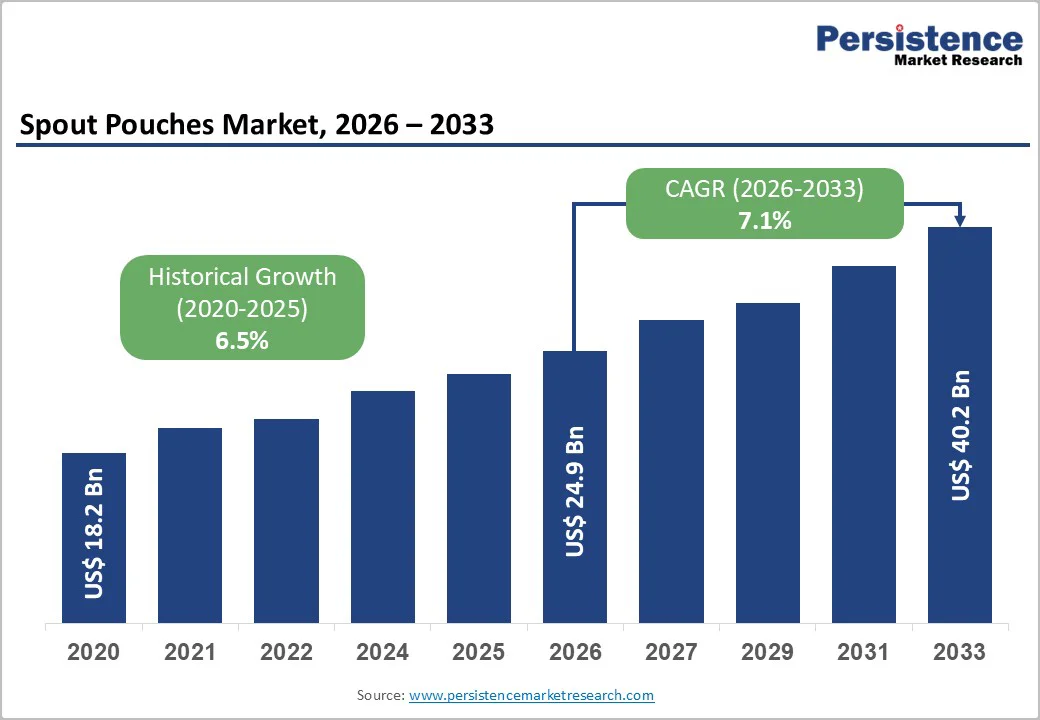

The global spout pouches market size is likely to be valued at US$24.9 billion in 2026 and is expected to reach US$40.2 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033, driven by the rising demand for convenient, portion-controlled liquid and semi-liquid packaging across food & beverage and personal-care applications, strong adoption in emerging economies, and accelerated innovation in mono-material and recyclable pouch structures aligned with tightening packaging regulations.

Modern retail growth, expanding e-commerce fulfillment, and cost advantages over rigid packaging remain key demand drivers. Strong market fundamentals are reinforced by major flexible-packaging players expanding capacity and introducing recycle-ready solutions across premium and value segments.

Key Industry Highlights

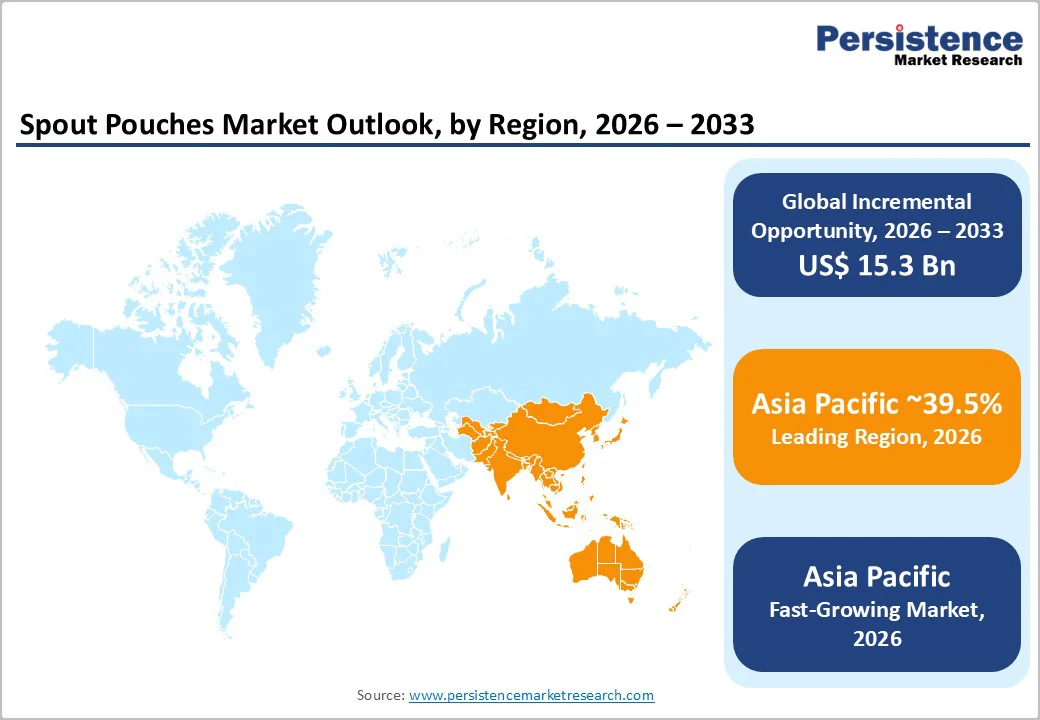

- Leading Region: Asia Pacific is projected to hold the largest share of the market, accounting for over 39.5% of the market, supported by large-scale manufacturing capacity, cost-efficient production, and strong demand from the food, beverage, and household product industries.

- Fastest-growing Region: Asia Pacific is also likely to be the fastest-growing regional market, driven by rising consumption of packaged beverages, dairy products, edible oils, and condiments, as well as increasing adoption of lightweight and refill-oriented packaging formats in emerging economies.

- Investment Plans: Investment activity is concentrated on mono-material and recyclable spout pouch structures, expansion of localized manufacturing facilities in the Asia Pacific, and upgrades to aseptic and high-speed filling technologies in North America and Europe to support premium beverages and refill applications.

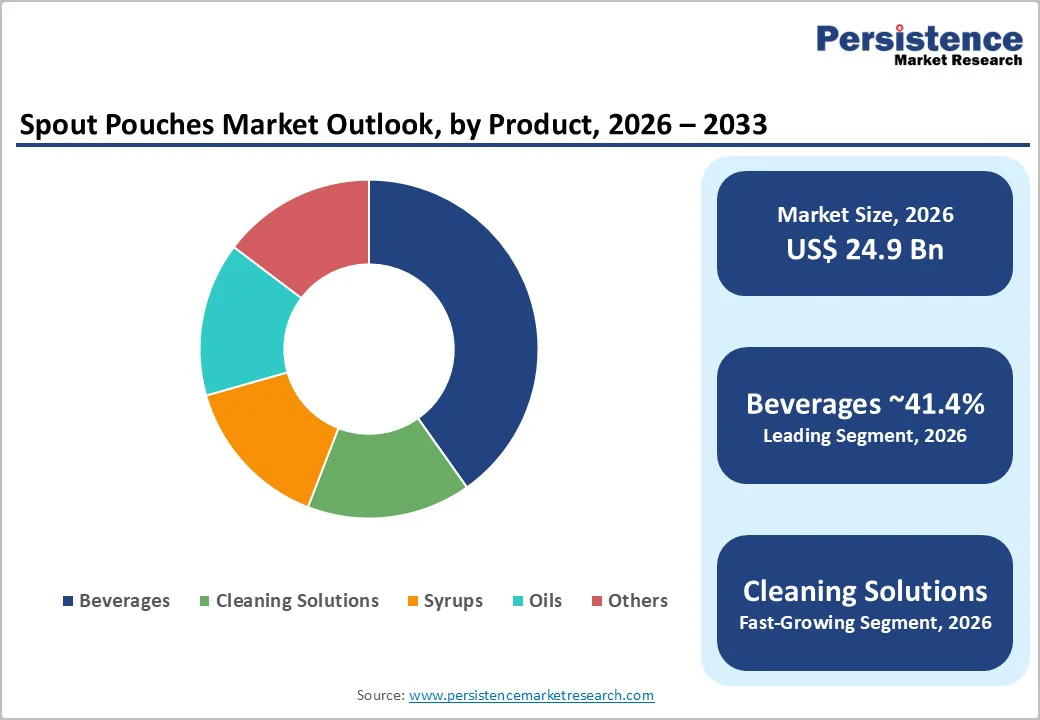

- Dominant Product Type: Beverages are anticipated to represent the dominant product type, accounting for approximately 41.4% of the global demand, driven by strong usage in juices, liquid dairy alternatives, sports nutrition, and child-focused packaged drinks.

- Leading Material: Plastic materials are estimated to lead the market with around 43.6% share, due to their cost efficiency, durability, and compatibility with high-speed filling and sealing operations across multiple end-user industries.

| Key Insights | Details |

|---|---|

| Spout Pouches Market Size (2026E) | US$24.9 Bn |

| Market Value Forecast (2033F) | US$40.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Convenience and End-user Adoption in Beverages and On-The-Go Personal Care

Spout pouches offer portion control, easy pouring, resealability, and low transportation weight, attributes that have accelerated adoption across beverages, baby foods, and concentrated home-care products. Beverages, including energy drinks, juices, and liquid dairy, account for a substantial share of spout pouch volumes, with leading beverage SKUs frequently representing over 41.4% of packaged liquid applications.

This trend is reinforced by urbanization, smaller household sizes, and the expansion of convenience retail and e-commerce channels that favor lightweight, space-efficient packaging. Operationally, spout pouches enable faster shelf rotation and reduced logistics costs, improving total landed cost when compared with rigid containers.

Sustainability Policy and Mono-Material Design Innovations

Tightening environmental regulations and corporate sustainability commitments are accelerating the transition toward mono-material and recycle-ready spout pouch solutions. Packaging producers are introducing all-polyethylene and paper-dominant structures that maintain required barrier properties while improving recyclability.

These innovations allow brand owners to meet packaging waste regulations and unlock premium positioning in markets with strict sustainability requirements. As a result, investments in retrofitting filling lines and advanced sealing technologies compatible with mono-material spouts have become standard capital priorities among leading converters, supporting long-term structural growth.

Scale Economics and Penetration into Industrial and Large-Format Refill Channels

Large-format spout pouches used in bulk foodservice, industrial lubricants, and household refill programs reduce packaging material per unit of product and significantly lower storage and transportation requirements. These formats can reduce the transport volume of packaged products by approximately 30-60% compared with rigid drums or jerrycans, improving carbon efficiency per liter shipped.

Adoption is accelerating as retailers and suppliers prioritize refill-first initiatives and logistics optimization. The expansion into bulk and industrial formats broadens the addressable market beyond single-serve retail applications while improving average selling prices through differentiated, high-capacity solutions.

Barrier Analysis - Recycling System Mismatch and Collection Infrastructure Limitations

Despite advancements in mono-material designs, effective recycling outcomes remain dependent on local collection and sorting infrastructure. In many developing and mid-income markets, limited curbside separation and low flexible packaging recovery rates create a disconnect between recyclable design intent and real-world recyclability.

This gap increases reputational and compliance risks for brand owners and may elevate costs through extended producer responsibility fees. Conservative public investment in recycling infrastructure continues to slow the transition from multi-layer laminates to mono-material spout pouches in these regions.

Barrier Performance Trade-Offs Versus Recyclability

High-barrier protection against oxygen, moisture, and aroma remains critical for certain applications such as syrups, edible oils, and pharmaceutical liquids. Achieving comparable barrier performance with mono-material or paper-dominant structures is technically complex and often more costly for extended-shelf-life products.

In cases where barrier compromise is unacceptable, brand owners continue to rely on multi-layer aluminum or composite laminates. This technical limitation creates segmented demand and constrains the pace of universal adoption for recyclable spout pouch formats.

Opportunity Analysis - Refillable and Bulk-Format Packaging Programs

The expansion of refill programs presents a sizable growth opportunity for spout pouches, particularly in home-care and foodservice applications. Bulk-format spout pouches could represent a multi-hundred-million-dollar opportunity by 2030 as refill models scale across Europe and parts of Asia.

By combining mono-material pouch designs with retail refill infrastructure, brands can achieve measurable reductions in lifecycle emissions and per-unit packaging costs. Converters that provide certified, recycle-ready formats, along with filling-line integration capabilities, are positioned to benefit from early-mover advantages.

Paper and Hybrid Paper-Dominant Spout Pouch Solutions

Paper-dominant spout pouches are gaining traction in markets with strong paper recycling systems and consumer preference for natural packaging aesthetics. These structures are well-suited for dry food concentrates, detergents, and select low-moisture liquid products. Pilot programs demonstrate paper content exceeding 80% in certain designs, enabling disposal within paper recycling streams.

Growth rates for paper-dominant spout pouches in select European markets are expected to exceed the overall market average, creating a focused opportunity for converters with advanced paper-lamination capabilities.

Geographic Expansion across ASEAN and South Asia

Asia Pacific continues to represent the fastest-growing regional opportunity, driven by rising packaged food consumption, expanding quick-service restaurant formats, and localized manufacturing ecosystems. Investments in regional production facilities and technical service centers enable converters and fitment suppliers to shorten lead times and accelerate brand conversions.

Market entry strategies that integrate regulatory alignment, partnerships with local fillers, and pilot packaging launches can translate into sustainable market share gains as domestic brands upgrade packaging formats.

Category-wise Analysis

Product Type

Beverages are expected to be the largest application segment in the market, accounting for approximately 41.4% of global demand in 2026. The segment’s dominance is supported by strong adoption across juices, flavored drinks, liquid dairy alternatives, sports nutrition products, and child-oriented beverages.

Spout pouches provide critical functional advantages for beverage packaging, including resealability, controlled dispensing, lightweight construction, and reduced risk of breakage compared with rigid containers. These attributes align well with on-the-go consumption patterns and modern retail requirements.

Growth within the beverages segment is reinforced by continuous packaging innovation. Manufacturers are increasingly incorporating child-safe caps, tamper-evident closures, and advanced aseptic filling technologies to meet stringent food safety and shelf-life requirements.

The compatibility of spout pouches with high-speed filling lines and their strong performance in convenience retail, vending, and e-commerce channels further support repeat purchasing behavior. As beverage brands expand product portfolios in functional and single-serve formats, spout pouches are expected to retain their position as the leading product type.

Cleaning solutions and home-care concentrates are likely to be the fastest-growing product type within the market. Growth is driven by the rising adoption of concentrated formulations, refill-based consumption models, and sustainability initiatives aimed at reducing plastic waste and transportation emissions.

Spout pouches enable efficient dispensing of liquid detergents, surface cleaners, and specialty home-care products while minimizing packaging material per unit of product.

Large-format refill pouches are gaining traction among retailers and manufacturers seeking to lower packaging costs and improve environmental performance across supply chains. Technical advancements in barrier films, spout sealing, and chemical-resistant fitments have expanded the suitability of spout pouches for viscous and chemically active formulations.

These developments allow cleaning solution brands to transition away from rigid plastic containers without compromising product integrity, positioning this segment for sustained above-average growth during the forecast period.

Material Insights

Plastic materials are anticipated to account for approximately 43.6% of the total spout pouch consumption, making them the leading material segment.

Polyethylene-based laminates dominate this category due to their favorable balance of cost efficiency, mechanical strength, flexibility, and compatibility with high-speed pouch forming and filling operations. Plastic-based spout pouches offer reliable sealing performance, resistance to moisture and puncture, and suitability for a wide range of liquid and semi-liquid products.

Material innovation within this segment increasingly focuses on mono-polyethylene structures that simplify recycling while maintaining the required barrier and durability characteristics. These designs support compliance with evolving packaging waste regulations and corporate sustainability commitments.

As brand owners prioritize recyclable packaging solutions without incurring significant cost increases, plastic-based spout pouches are expected to remain the dominant material choice across food, beverage, personal care, and household applications.

Paper-based and paper-dominant spout pouches are likely to represent the fastest-growing material segment, driven by strong sustainability positioning and consumer preference for fiber-based packaging. These structures enable partial or full compatibility with paper recycling streams, particularly in regions with well-established fiber recovery infrastructure.

Paper-dominant pouches are increasingly used for dry concentrates, powdered mixes, and select low-moisture liquid applications where barrier requirements are less demanding.

Advancements in paper lamination, coating technologies, and spout integration have improved the functional performance of these formats, expanding their commercial viability. Brands adopting paper-based spout pouches benefit from enhanced environmental messaging and differentiation on retail shelves.

While penetration remains lower than plastic-based alternatives, accelerated growth rates indicate a rising role for paper materials as sustainability-driven purchasing decisions continue to influence packaging strategies.

Regional Insights

Asia Pacific Spout Pouches Market Trends- Manufacturing Scale and High-Volume Consumer Adoption

Asia Pacific is projected to lead the market with a share of 39.5% and is likely to be the fastest-growing region. Growth is underpinned by large-scale manufacturing capacity, cost-efficient production, and rapidly expanding consumer markets across China, India, Japan, and Southeast Asia.

In China, spout pouches are widely used for sauces, cooking oils, dairy beverages, and condiments, driven by high urban consumption and strong domestic food-processing industries. Local brands increasingly favor spout pouches for their logistical efficiency and shelf-space optimization in modern retail formats.

Regional developments also reflect increasing sophistication in packaging technology and sustainability initiatives. In Japan, long-standing adoption of spout pouches for liquid seasonings and ready-to-use foods continues to influence regional design standards, particularly in cap functionality and precision dispensing.

India and Southeast Asian countries are witnessing accelerated adoption in beverages and personal care, supported by expanding middle-class populations and growing demand for affordable, single-use and refill packaging formats.

Packaging manufacturers across the region have invested in localized production facilities and advanced filling lines, reducing lead times and enabling rapid customization. These investments, combined with rising sustainability awareness, are expected to sustain Asia Pacific’s leadership position throughout the forecast period.

North America Spout Pouches Market Trends - Mono-Material Innovation and Refill-Oriented Adoption

North America represents a mature market characterized by high per-capita packaged beverage consumption, strong brand-driven innovation, and advanced filling infrastructure. The U.S. leads regional demand, supported by premium beverage formulations, functional nutrition products, and widespread adoption of aseptic filling technologies.

Major beverage and food brands in the U.S. have increasingly shifted single-serve juices, smoothies, and children’s nutrition products from rigid bottles to spout pouches to improve portability and reduce packaging weight. This transition has reinforced steady baseline demand across convenience retail, club stores, and e-commerce fulfillment channels.

Recent developments in the region highlight a strong focus on recyclability and mono-material compatibility. Flexible packaging converters operating in the U.S. have expanded production of all-polyethylene spout pouch structures designed to align with existing store drop-off recycling streams.

Household and personal care brands have piloted refill-oriented spout pouch formats for detergents and cleaning concentrates, particularly in large retail chains emphasizing waste reduction commitments.

These initiatives have accelerated collaboration among packaging suppliers, resin producers, and recycling organizations, shaping a market environment in which technical compliance with recycling systems is increasingly a prerequisite for commercial adoption.

Europe Spout Pouches Market Trends - Regulatory-Led Circular and Paper-Based Pouch Development

Europe demonstrates robust spout pouch adoption driven by regulatory harmonization, extended producer responsibility requirements, and strong consumer demand for sustainable packaging. Western European countries, including Germany, the U.K., France, and Spain, lead regional demand, particularly in food, beverage, and home-care applications.

European beverage brands have expanded the use of spout pouches for fruit purees, baby food, and sports nutrition products, supported by advanced aseptic processing and strict food safety standards. This has strengthened the role of spout pouches as a preferred format for premium and health-focused product lines.

Recent developments across Europe emphasize recyclable and paper-dominant pouch solutions. Packaging manufacturers operating in the region have launched paper-based spout pouch structures compatible with local fiber recycling systems, responding to both regulatory pressure and retailer sustainability targets.

In parallel, refill programs for household and personal care products have expanded in countries such as Germany and the U.K., where retailers actively promote concentrated formulations packaged in spout pouches as alternatives to rigid plastic bottles. These developments have positioned Europe as a testing ground for circular packaging models, influencing product design and material selection across the global spout pouches market.

Competitive Landscape

The global spout pouches market is moderately concentrated, with leading global converters holding a significant share alongside numerous regional players. Competitive differentiation is driven by recyclable material innovation, fitment technology, and integrated filling solutions. Recent activity highlights investments in mono-material bulk pouches, refill-oriented designs, and cross-industry applications beyond food and personal care.

Key strategies include sustainability-led innovation, vertical integration with fitment suppliers, cost leadership through regional manufacturing, and collaborative product development with brand owners.

Key Industry Developments

- In February 2025, Mondi introduced paper-based stand-up pouches with over 85% paper content in Spain and Portugal, expanding spout pouch applications into more environmentally friendly household categories and aligning packaging formats with sustainability goals.

- In March 2025, AptarGroup announced a strategic partnership with Pouch Partners to co-develop recyclable spout pouch closures, aimed at improving recyclability and reducing carbon footprint across flexible packaging applications.

Companies Covered in Spout Pouches Market

- Amcor plc

- Berry Global Group, Inc.

- Mondi plc

- Smurfit Kappa Group

- Sealed Air Corporation

- Sonoco Products Company

- ProAmpac

- Printpack, Inc.

- Glenroy, Inc.

- Scholle IPN / SIG

- Huhtamaki Oyj

- Winpak Ltd.

- Guala Pack S.p.A.

- Coveris Holdings S.A.

Frequently Asked Questions

The global spout pouches market is estimated to be valued at US$24.9 billion in 2026.

By 2033, the spout pouches market is projected to reach US$40.2 billion.

Key trends include rising adoption of convenient, on-the-go beverage packaging, increasing use of refill and bulk-format pouches for home and personal care products, growing focus on mono-material and recyclable pouch structures, and expanding usage in e-commerce-friendly lightweight packaging formats.

Beverages represent the leading product segment, accounting for around 41.4% of total market demand, driven by strong consumption of juices, liquid dairy alternatives, sports nutrition, and child-focused packaged drinks.

The spout pouches market is expected to grow at a CAGR of 7.1% between 2026 and 2033.

Major players include Amcor, Mondi, Berry Global, Sealed Air, and ProAmpac.