- Pharmaceuticals

- Short Bowel Syndrome Treatment Market

Short Bowel Syndrome Treatment Market Size, Trends, Share, Growth, and Regional Forecast, 2025 to 2032

Short Bowel Syndrome Treatment Market by Drug Class (Glucagon-like Peptide, Histamine Blockers, Proton Pump Inhibitors, Growth Hormone, Others), Distribution Channel, and Regional Analysis from 2025 to 2032

Short Bowel Syndrome Treatment Market Share and Trends Analysis

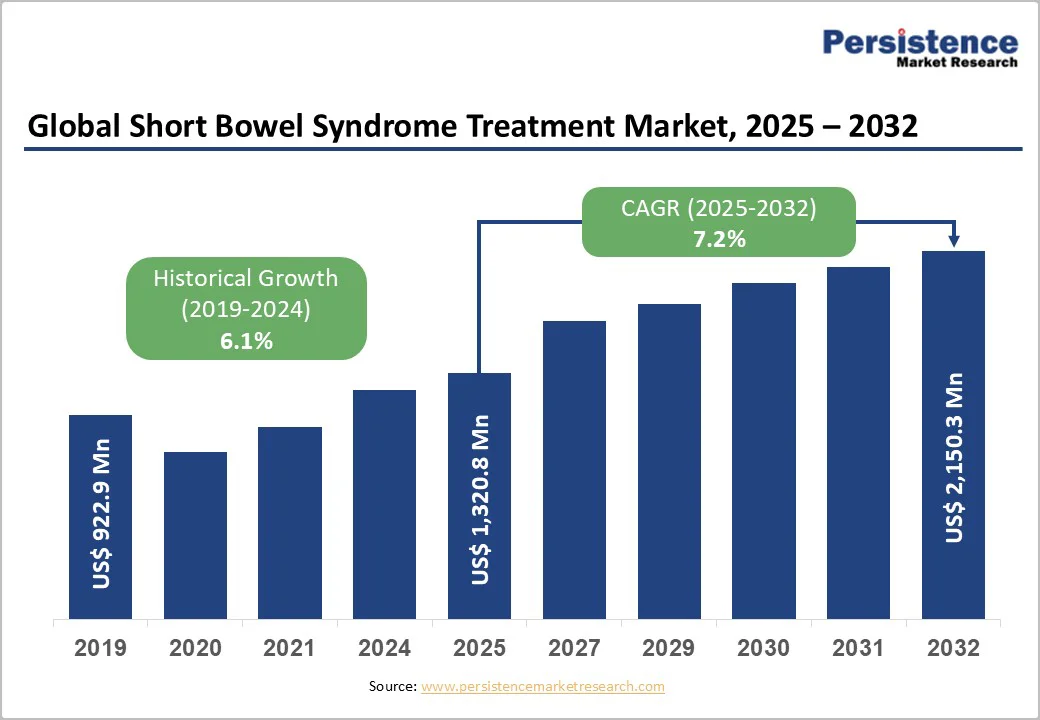

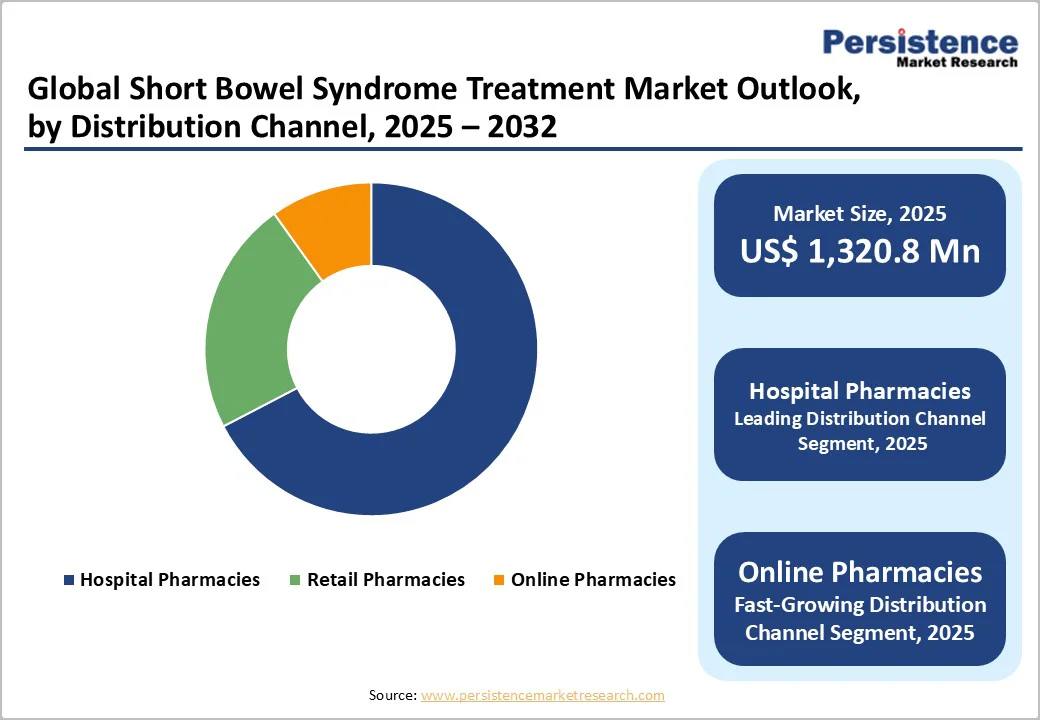

The global short bowel syndrome treatment market size is valued at US$1,320.8 million in 2025 and is projected to reach US$2,150.3 million by 2032, growing at a CAGR of 7.2% between 2025 and 2032.

Short bowel syndrome (SBS) is a malabsorptive disorder caused by major loss of small intestine or severe intestinal disease, leading to inadequate absorption of fluids, electrolytes, and nutrients. Patients commonly experience chronic diarrhea, dehydration, weight loss, and micronutrient deficiencies due to reduced intestinal functional capacity.

While SBS can occasionally become life-threatening, most cases are managed through long-term medical and nutritional support. The condition is usually acquired after surgical resections, with genetic causes being rare. Current management focuses on dietary optimization, pharmacological therapy, including GLP-2 analogs such as teduglutide, and supportive agents, such as antidiarrheals, proton-pump inhibitors, and growth hormones.

Key Industry Highlights

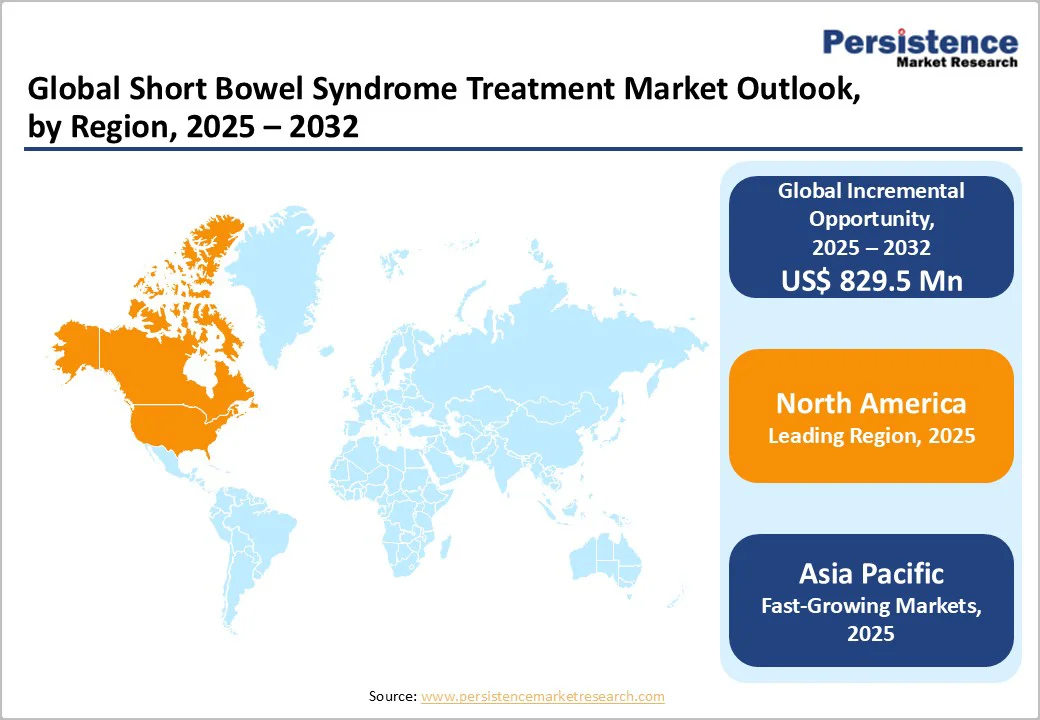

- Leading Region: North America dominates the global market, accounting for 47.1%, driven by advanced healthcare infrastructure, robust reimbursement pathways, and high adoption of GLP-2-based therapies.

- Fastest-Growing Region: The Asia Pacific market is expected to grow rapidly, with a CAGR of 9.0% over the forecast period, fueled by expanding diagnostic capacity, improved specialist access, and rising adoption of advanced SBS treatments.

- Leading Product: Glucagon-like Peptide lead with 87.4% share, supported by strong clinical efficacy, proven parenteral support reduction, and increasing physician preference for GLP-2 analogs.

- Leading Distribution Channel: Hospital pharmacies dominate with 68.1% value share, driven by specialized therapy initiation, dosing oversight, and stringent monitoring requirements in SBS management.

- Rising Disease Burden: Global SBS prevalence is steadily increasing, driven by higher intestinal surgeries and chronic gastrointestinal disorders requiring long-term nutritional and pharmacological management.

- Advances in Parenteral Nutrition: Innovations in customized parenteral nutrition formulations enhance metabolic stability and reduce complications, strengthening their role as essential supportive therapy in SBS care.

- Increasing R&D Investments: Pharmaceutical companies are accelerating their GLP-2 analog and adjunct therapy pipelines, driven by unmet needs and supportive global incentives for rare-disease research.

- Greater Clinical Trial Activity: Growing global participation in Phase 2/3 trials for next-generation GLP-2 analogs accelerates evidence generation and future market expansion.

| Key Insights | Details |

|---|---|

| Short Bowel Syndrome Treatment Market Size (2025E) | US$ 1,320.8 Million |

| Market Value Forecast (2032F) | US$ 2,150.3 Million |

| Projected Growth (CAGR 2025 to 2032) | 7.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.1% |

Market Dynamics

Driver - Advancing GLP-2 Therapies and Rising Clinical Focus Strengthen Global SBS Treatment Demand

Growing global awareness, expanding epidemiological data, and steady improvements in healthcare infrastructure are strengthening early diagnosis and long-term management of short bowel syndrome (SBS). As countries recognize SBS as a rare but high-burden intestinal disorder, public-private collaboration has intensified.

Non-profit organizations are increasingly supporting education, clinical training, and multi-centre research efforts, while government agencies in several regions now offer targeted incentives to accelerate orphan-drug development.

These supportive frameworks have encouraged manufacturers to advance novel biologics, next-generation glucagon-like peptide-2 (GLP-2) analogs and improved parenteral nutrition solutions. In March 2025, progress in peptide-based innovation continued as an oral dual-agonist GLP-1/glucagon program advanced toward clinical readiness following favourable pharmacodynamic and bioavailability data reported in September 2024.

Although SBS drug development remains at an early stage globally, rising investment, stronger regulatory backing, and increased patient-advocacy engagement are collectively driving a more innovation-friendly environment.

As these forces converge, the global SBS treatment market is positioned for sustained expansion supported by widening therapeutic options and improved long-term care pathways. Overall, the combined momentum across research, policy support, and clinical innovation is steadily transforming SBS from an underserved rare condition to an active area of therapeutic development.

Restraints - High Treatment Costs and Limited Access to Advanced SBS Therapies Restrict Wider Adoption

Despite growing research interest, the global short bowel syndrome treatment market continues to face major constraints. The most significant barrier remains the limited number of approved therapeutic options, which slows treatment uptake and restricts clinician confidence. In several regions, low physician awareness, particularly in community-level gastroenterology settings, further delays diagnosis and optimal long-term care.

Regulatory setbacks also contribute to market restraint. In December 2023, a New Drug Application (NDA) for glepaglutide, a long-acting glucagon-like peptide-2 (GLP-2) analog, was submitted to the U.S. Food and Drug Administration (FDA), supported by results from the pivotal phase 3 EASE-1 trial.

However, in December 2024, the FDA issued a Complete Response Letter (CRL), indicating that current data, despite significant reductions in parenteral support with the twice-weekly regimen, were insufficient for approval and required an additional confirmatory phase 3 trial planned for 2025.

Such regulatory delays, coupled with dependency on complex parenteral nutrition and limited long-term outcome data, continue to hinder rapid global market expansion. Overall, slow regulatory progress, constrained therapeutic availability, and uneven clinical awareness collectively limit the full growth potential of the global SBS treatment market.

Opportunity - Next-Generation Long-Acting and Oral GLP-2 Platforms Unlock Strong Pipeline and Commercial Upside

The global short bowel syndrome treatment market is entering a pivotal growth phase as innovation rapidly expands beyond traditional parenteral support. The introduction of pharmacological hormonal therapies designed to enhance intestinal adaptation, particularly glucagon-like peptide-2 (GLP-2)-based agents, continues to unlock strong commercial opportunities.

Teduglutide, a recombinant human GLP-2 analog, remains the cornerstone therapy and demonstrates the revenue potential of targeted biologics. Market expansion prospects have further strengthened with next-generation candidates such as apraglutide, a once-weekly long-acting synthetic GLP-2 analog.

In April 2025, discussions between developers and the U.S. Food and Drug Administration (FDA) confirmed that a new confirmatory Phase 3 trial will support regulatory progression, reinforcing long-term investment pathways. Apraglutide has already generated compelling Phase 3 outcomes, achieving statistically significant reductions in weekly parenteral support and enabling 27 patients to reach enteral autonomy, highlighting meaningful clinical and commercial upside.

Momentum continues with emerging oral GLP-2 analog programs; notably, in September 2025, first-in-class pharmacokinetic data for an oral GLP-2 molecule were presented at the European Society for Clinical Nutrition and Metabolism (ESPEN), signaling a shift toward more accessible, compliance-friendly therapies. Collectively, advancing biologics and next-generation oral platforms are creating a robust pipeline that positions SBS therapy as a high-value global market opportunity.

Category-wise Analysis

By Product: Glucagon-like Peptide Dominates Owing to Superior Intestinal Adaptation and Proven Reduction in Parenteral Support Needs

Glucagon-like peptide-based therapies are set to dominate the short bowel syndrome treatment landscape by 2025, capturing an estimated 87.4% global share. Their market leadership is driven by strong clinical evidence supporting enhanced intestinal adaptation, improved nutrient absorption, and meaningful reductions in dependence on parenteral nutrition.

The success of recombinant GLP-2 analogs, including once-daily and next-generation weekly formulations, continues to reshape treatment standards by offering durable, mechanism-driven benefits. Increased research investment, favourable regulatory momentum, and expanding awareness of GLP-2 efficacy further reinforce its dominant position across major markets.

By Distribution Channel: Hospital Pharmacies Lead Owing to Complex SBS Care Pathways and Controlled Dispensing Requirements

Hospital pharmacies are projected to account for nearly 68.1% of the global short bowel syndrome treatment market in 2025, owing to the specialized nature of therapy delivery and monitoring. Short bowel syndrome care requires coordinated multidisciplinary management, strict dosing oversight, and routine evaluation of intestinal function, all of which favour hospital-based dispensing.

GLP-2 analogs and supportive therapies often require prescription validation, cold-chain handling, and clinician-supervised initiation, reinforcing the hospital’s central role. Additionally, higher diagnosis rates in tertiary care centres and structured reimbursement workflows further strengthen hospital pharmacies’ dominance within the SBS treatment ecosystem.

Regional Insights

North America Short Bowel Syndrome Treatment Market Trends

By 2025, North America is projected to account for approximately 47.1% of the global short bowel syndrome (SBS) treatment market, driven by rising disease awareness, strong clinical adoption, and sustained innovation in biologics.

SBS remains a rare but severe malabsorptive condition, affecting an estimated 10,000-20,000 individuals in the United States, spanning both pediatric and adult populations. Its burden is amplified by the high rate of small-bowel (SB) resections, with SBS occurring in nearly 15% of adults undergoing major intestinal surgeries.

Furthermore, an estimated 3 million individuals in the United States live with chronic gastrointestinal disorders, and nearly 25,000 patients rely on long-term Home Parenteral Nutrition (HPN), underscoring the need for advanced therapeutic options.

Additionally, the North American market is being driven by rapid uptake of modern biologics, especially Glucagon-Like Peptide-2 (GLP-2) analogues, which offer clinically proven improvements in intestinal absorption and reduced dependency on parenteral nutrition.

Growing emphasis on early diagnosis, expanding specialist care networks, and strong payer support for rare-disease treatments further strengthen market growth. Collectively, these factors position North America as the leading and most innovative regional market for SBS treatment.

Europe Short Bowel Syndrome Treatment Market Trends

By 2025, Europe is projected to hold nearly 24.4% of the global short bowel syndrome treatment market, supported by strong clinical infrastructure, early adoption of intestinal rehabilitation strategies, and continued investment in rare-disease innovation.

SBS remains a leading cause of Intestinal Failure (IF) in the region, accounting for nearly 75% of adult IF cases, reinforcing the need for long-term nutritional and medical management. IF is a rare but life-threatening condition requiring continuous monitoring, parenteral support, and specialized multidisciplinary care.

To address this burden, Europe has established several Intestinal Rehabilitation Programs (IRPs), such as the program at Meyer Children’s Hospital - Firenze, which integrates nutritional therapy, bowel adaptation strategies, and advanced reconstructive surgery to optimize residual bowel function.

Europe’s market growth is further strengthened by research-driven initiatives, including the EU-funded INTENS project, launched to create a functional small bowel using autologous tissue engineering. This approach aims to overcome organ-donor shortages and reduce complications associated with long-term parenteral nutrition and intestinal transplantation.

With approximately 13,000 individuals affected by SBS across the European Union annually, rising awareness, sustained public-health investment, and accelerating translational research position Europe as a key growth engine for the SBS treatment landscape.

Asia Pacific Short Bowel Syndrome Treatment Market Trends

The Asia Pacific market is poised for strong expansion, projected to grow at a CAGR of 9.0% over the forecast period, driven by a rapidly increasing clinical burden and improving regional healthcare capacity.

The region is witnessing a steady rise in gastrointestinal (GI) surgical complications, including post-resection malabsorption and chronic intestinal failure (IF), which directly increases demand for long-term SBS management.

Parallelly, the adoption of advanced biologics and nutrition-support therapies is accelerating, especially in countries such as Japan, South Korea, China, and Australia, where clinicians are increasingly integrating glucagon-like peptide-2 (GLP-2) analogues and specialized parenteral nutrition (PN) regimens into routine care.

Government investment in rare-disease infrastructure has intensified since 2023, with national programs across China, Japan, and Australia prioritizing improved access to PN, pediatric intestinal rehabilitation, and home-based nutritional support.

The growing establishment of multidisciplinary intestinal rehabilitation units, modelled on North American and European programs, further strengthens treatment capacity across tertiary hospitals. With a rising recognition of SBS as a chronic but manageable GI disorder, expanding reimbursement pathways, and increasing research collaborations across Asia, the region is becoming a major growth engine for the global SBS treatment landscape.

Competitive Landscape

The global short bowel syndrome treatment market is characterized by limited availability of approved therapies, creating a high-value but tightly controlled competitive environment. Innovation in GLP-2 analogs, emerging oral formulations, and pediatric-focused trials is intensifying competition. However, symptomatic management remains crowded, with strong rivalry among established brands and minimal entry space for smaller or regional manufacturers.

Key Industry Developments:

- In August 2025, it was confirmed that a first-in-class oral GLP-2 tablet for short bowel syndrome will be presented at the September 2025 European Society for Clinical Nutrition & Metabolism Congress, highlighting progress in long-acting GLP-2 agonist development.

- In February 2025, the first pediatric short bowel syndrome with intestinal failure patient was dosed in an investigator-initiated proof-of-concept trial of crofelemer, with early 2025 data potentially supporting reimbursed early access across select European markets under specialist-led evaluation.

- In December 2024, a mid-stage trial showed that the investigational inflammatory bowel disease drug duvakitug achieved superior symptom resolution in ulcerative colitis and Crohn’s disease compared with placebo, prompting claims of best-in-class potential due to its strong efficacy profile.

Companies Covered in Short Bowel Syndrome Treatment Market

- OPKO Health, Inc.

- Pfizer Inc.

- Takeda Pharmaceutical Company Limited

- Teva Pharmaceutical Industries Ltd.

- Ironwood

- Entera Bio Ltd.

- Zealand Pharma

- Emmaus Medical, Inc.

- EMD Serono

- OxThera

- Jaguar Health

Frequently Asked Questions

The global short bowel syndrome treatment market is projected to be valued at US$ 1,320.8 Million in 2025.

Growing prevalence of intestinal failure and rising adoption of advanced biologics and parenteral nutrition therapies drive market growth.

The global short bowel syndrome treatment market is poised to witness a CAGR of 7.2% between 2025 and 2032.

Expansion of novel GLP-2 analogs, oral formulations, and pediatric-focused therapies enabling wider clinical adoption present major growth opportunities.

Major players in the global are OPKO Health, Inc., Pfizer Inc., Takeda Pharmaceutical Company Limited, Teva Pharmaceutical Industries Ltd., Ironwood, and others.