- Pharmaceuticals

- Short Bowel Syndrome Market

Short Bowel Syndrome Market Size, Share, and Growth Forecast 2026–2033

Short Bowel Syndrome Market by Product Type (GLP-2 Analog, Growth Hormone, Glutamine), Distribution Channel (Hospital Pharmacies, Online & Retail Pharmacies), and Regional Analysis, 2026 – 2033

Short Bowel Syndrome Market Size and Trends Analysis

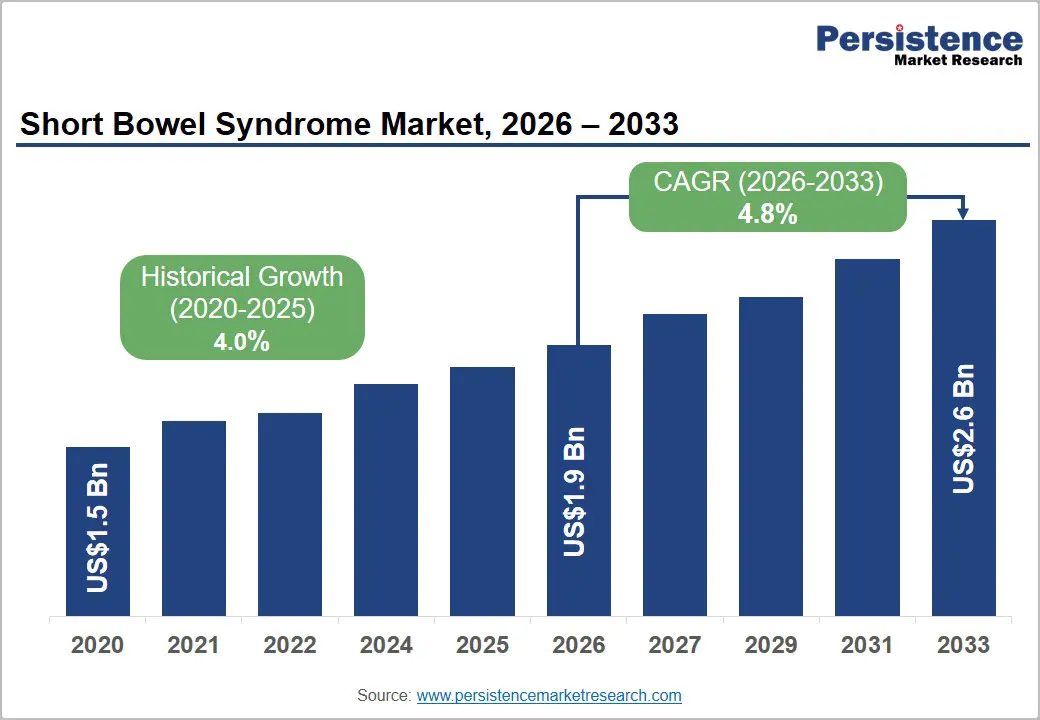

The global short bowel syndrome market size is likely to be valued at US$1.9 billion in 2026 and is expected to reach US$2.6 billion by 2033, growing at a CAGR of 4.8% during the forecast period from 2026 to 2033, driven by the increasing prevalence of short bowel syndrome (SBS), a complex malabsorptive disorder caused by extensive surgical resection of the small intestine, which leaves patients with inadequate absorptive capacity to maintain proper nutrition, hydration, and electrolyte balance. The condition most commonly develops following surgical treatment for Crohn's disease, mesenteric ischemia, volvulus, traumatic intestinal injury, and necrotizing enterocolitis in neonates.

Key Market Highlights:

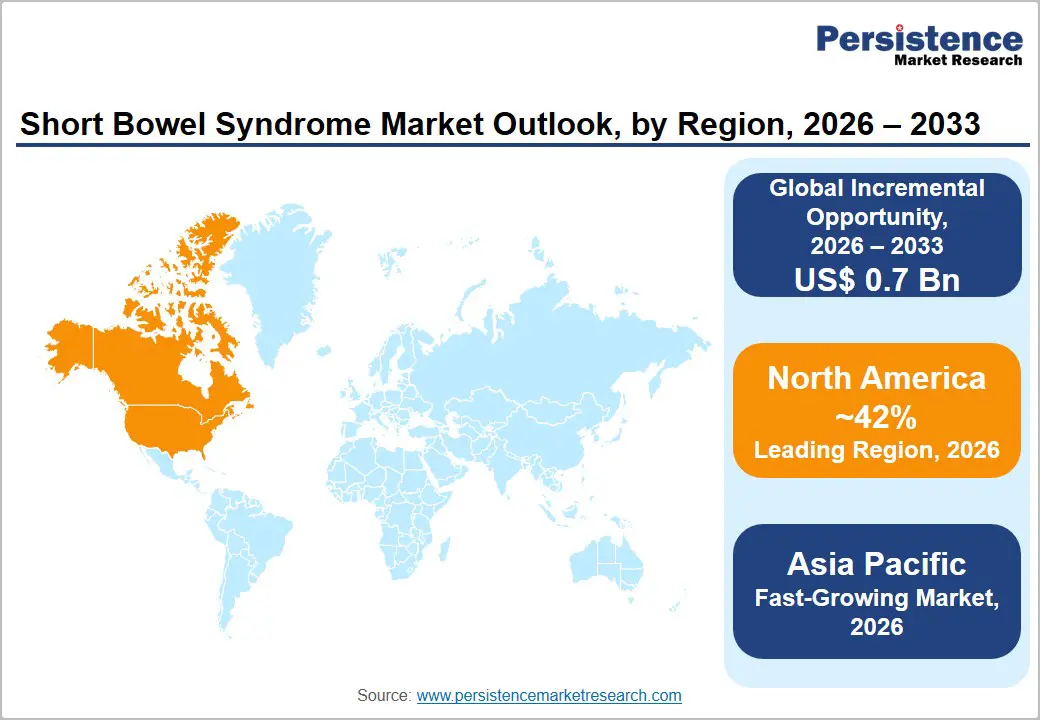

- Leading Region: North America is forecast to dominate, with an approximately 42% share in 2026, driven by high SBS diagnosis rates, a strong reimbursement infrastructure for GLP-2 therapies, and the presence of leading pharmaceutical innovators.

- Fastest-growing Region: Asia Pacific is projected to grow at a CAGR of approximately 6.2% through 2033, supported by rising surgical volumes, improving recognition of rare diseases, and expanding healthcare infrastructure in China and India.

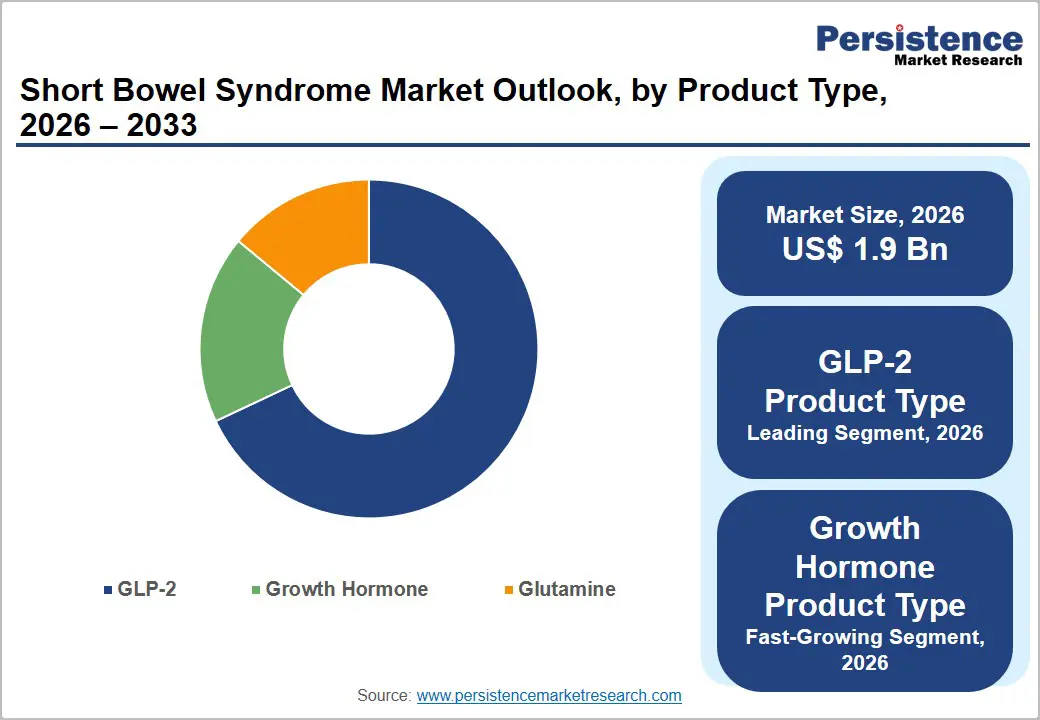

- Dominant Product Type: GLP-2 analogs are anticipated to lead the product segment, commanding approximately 68% of product type revenue in 2026, anchored by the clinical efficacy and regulatory approvals of teduglutide-based therapies.

- Fastest-growing Product Type: Growth hormone is estimated to register the fastest product growth at a CAGR of approximately 5.5% through 2033, driven by adjunctive use alongside GLP-2 therapy and enteral nutrition optimization protocols.

- Dominant Distribution Channel: Hospital pharmacies account for the largest channel share at approximately 72% in 2026, reflecting the specialist-managed and high-complexity nature of SBS treatment initiation and monitoring.

- Key Market Opportunity: Oral and subcutaneous next-generation GLP-2 formulations in clinical development, combined with expanding pediatric SBS indications, represent the highest-value pipeline opportunity for market participants through 2033.

- Sustainability Trend: Patient-centric care models and home parenteral nutrition programs are reducing hospital dependency, creating new demand for long-term pharmacological management and specialty pharmacy services.

DRO Analysis

Driver – Rising Prevalence of Crohn's Disease and Surgical Intestinal Resections

The increasing global burden of inflammatory bowel disease (IBD), particularly Crohn's disease, is the single most significant upstream driver of Short Bowel Syndrome prevalence. The Crohn's & Colitis Foundation estimates that over 3.1 million adults in the U.S. are affected by IBD, with Crohn's disease accounting for a substantial proportion. Beyond Crohn's disease, mesenteric ischemia, intestinal volvulus, and neonatal necrotizing enterocolitis collectively contribute to SBS incidence across all age groups.

The European Society for Clinical Nutrition and Metabolism (ESPEN) has published guidelines acknowledging chronic intestinal failure, of which SBS is the most common cause, as a growing clinical and health system burden. As the global prevalence of IBD continues to rise across both developed and emerging markets, driven by dietary, microbiome, and environmental factors, the patient population requiring SBS-specific pharmacological management is expected to expand steadily through the forecast period.

Barrier – Limited Disease Awareness and Diagnostic Underidentification

Short bowel syndrome remains underdiagnosed in many healthcare settings, particularly in emerging markets where specialist gastroenterological and intestinal rehabilitation services are limited. The rarity of the condition, combined with symptom overlap with other gastrointestinal disorders, contributes to diagnostic delays that reduce the identified patient population available for pharmacological intervention.

In pediatric settings, neonatal SBS following necrotizing enterocolitis or intestinal atresia repair may not be systematically tracked within national disease registries, obscuring true prevalence and limiting population-level epidemiological data. The absence of standardized SBS diagnostic registries in many countries constrains market development by delaying patient identification, specialist referral, and treatment initiation, suppressing the addressable market relative to actual disease burden.

Opportunity – Next-Generation GLP-2 Formulations and Expanded Pediatric Indications

The development of a next-generation GLP-2 analog with improved dosing convenience represents a high-value commercial and clinical opportunity. Zealand Pharma's glepaglutide, VectivBio's apraglutide, and oral GLP-2 delivery platforms under development by Entera Bio are targeting differentiated market positions through weekly or less-frequent dosing regimens and oral bioavailability, which would substantially improve patient convenience relative to daily subcutaneous injection.

Expanded pediatric labeling for existing and pipeline GLP-2 products addresses a medically underserved population with high lifetime treatment value. The FDA Rare Pediatric Disease designation and EMA Orphan Medicinal Product designation provide regulatory incentives, including priority review and market exclusivity, that enhance commercial attractiveness. Pipeline success in these areas could meaningfully expand the addressable SBS patient population and generate premium pricing opportunities through the forecast period.

Category-wise Analysis

Product Type Insights

GLP-2 analogs are projected to dominate the global product type segment, commanding approximately 68% of the total product type revenue in 2026. The segment's leadership reflects the clinical paradigm shift driven by teduglutide (Gattex/Revestive), the first and most widely adopted disease-modifying therapy for SBS. GLP-2 analogs work by stimulating intestinal epithelial growth, increasing villous height and crypt depth, and enhancing mucosal absorptive surface area. This mechanism directly addresses the underlying pathophysiology of SBS, enabling meaningful reductions in parenteral nutrition volume in a significant proportion of patients.

Growth hormone is estimated to be the fastest-growing product type, advancing at a CAGR of approximately 5.5% through 2033. Recombinant human growth hormone, approved for SBS management as Zorbtive (somatropin) in the U.S., is used as an adjunctive therapy alongside specialized oral diet and often in combination with GLP-2 analog treatment. Growth hormone enhances intestinal adaptation and promotes lean body mass accretion in SBS patients, supporting its use as a complementary agent in intestinal rehabilitation protocols.

Distribution Channel Insights

Hospital pharmacies are the dominant distribution channel, estimated to represent approximately 72% of the total channel share in 2026. The complexity of SBS diagnosis and treatment initiation, the requirement for specialist gastroenterologist or intestinal failure unit oversight, and the need for patient education and monitoring make hospital pharmacy the primary dispensing point for GLP-2 analog therapies and growth hormone products.

Online and retail pharmacies are projected to be the fastest-growing distribution channel, registering a CAGR of approximately 6.8% through 2033. As patients with short bowel syndrome transition from inpatient treatment initiation to long-term disease management, the dispensing of ongoing GLP-2 analog prescriptions through specialty and mail-order pharmacies continues to increase. The expansion of specialty pharmacy networks, home infusion services, and digital prescription management platforms is further accelerating the shift of maintenance-phase SBS therapy toward online and retail pharmacies, enhancing patient convenience, treatment accessibility, and long-term adherence.

Regional Insights

North America Short Bowel Syndrome Market Trends and Insights

North America is projected to be the leading regional market, capturing approximately 42% of the global share in 2026, growing at a CAGR of approximately 4.5% through 2033. The region's dominance reflects the early regulatory approval of GLP-2 analog therapies, a well-developed rare disease reimbursement infrastructure, a high density of intestinal failure specialty centers, and a large identified SBS patient population.

U.S. Short Bowel Syndrome Market Trends and Insights

The U.S. is expected to command approximately 85% of the North America market share in 2026. The FDA approval of teduglutide under the Orphan Drug Act and robust commercial launch infrastructure have established the U.S. as the global center of GLP-2 therapy adoption. Medicare and Medicaid coverage pathways for SBS-related parenteral nutrition and pharmacotherapy, combined with strong advocacy from patient organizations such as the Oley Foundation, support patient access and treatment adherence.

Canada Short Bowel Syndrome Market Trends and Insights

Canada accounts for approximately 15% of the regional market share in 2026. Health Canada approved teduglutide for adult SBS management, and provincial drug benefit programs provide reimbursement pathways for eligible patients. The country's universal healthcare framework supports access to parenteral nutrition and specialist care through academic hospital networks in Ontario, British Columbia, and Quebec.

Europe Short Bowel Syndrome Market Trends and Insights

Europe is estimated to be the second-largest regional market, accounting for approximately 28% of the global share in 2026, growing at a CAGR of approximately 4.2% through 2033. The EMA approval of teduglutide as Revestive provides the clinical foundation for European market development. ESPEN clinical guidelines on intestinal failure management support consistent specialist prescribing practices across member states, though national HTA reimbursement variations create market access fragmentation.

Germany Short Bowel Syndrome Market Trends and Insights

Germany is estimated to hold approximately 24% of the Europe market share in 2026. As Europe's largest healthcare market, Germany benefits from the AMNOG benefit assessment framework that provides early access to approved orphan medicines, including GLP-2 analog, before price negotiation completion. Strong specialist gastroenterology and intestinal rehabilitation infrastructure in academic centers across Berlin, Munich, and Hamburg supports prescription activity.

U.K. Short Bowel Syndrome Market Trends and Insights

The U.K. is expected to account for approximately 18% of Europe's market share in 2026. The National Health Service (NHS) Highly Specialised Services program for intestinal failure supports centralized SBS management and GLP-2 therapy prescribing at designated intestinal failure units. NICE technology appraisals for teduglutide inform commissioning decisions and support national reimbursement, making the U.K. one of Europe's more accessible markets for SBS pharmacotherapy.

Asia Pacific Short Bowel Syndrome Market Trends and Insights

Asia Pacific is projected to be the fastest-growing regional market, advancing at a CAGR of approximately 6.2% through 2033, driven by rising surgical volumes, increasing IBD prevalence, improving rare disease recognition, and expanding healthcare infrastructure in major economies. Regulatory approvals and growing physician awareness of GLP-2 therapies in key markets are expected to drive above-average regional growth through the forecast period.

China Short Bowel Syndrome Market Trends and Insights

China is projected to hold approximately 45% of the market share in 2026. The country is experiencing rising IBD incidence, with the Chinese Society of Gastroenterology documenting increasing Crohn's disease diagnoses across urban populations. Regulatory approvals for GLP-2 therapies through the National Medical Products Administration (NMPA) and inclusion of orphan disease therapies in the National Reimbursement Drug List (NRDL) updates are expected to progressively improve SBS therapy access within China's tiered hospital system.

India Short Bowel Syndrome Market Trends and Insights

India is expected to be the fastest-growing regional market, supported by increasing surgical volumes at tertiary care hospitals, rising awareness of inflammatory bowel disease (IBD) through initiatives led by the Indian Society of Gastroenterology, and government efforts to strengthen rare disease care under the National Policy for Rare Diseases 2021. These factors are creating a more favorable environment for the growth of the short bowel syndrome (SBS) therapy market. However, limited reimbursement for high-cost orphan therapies continues to be the primary barrier to patient access in the country.

\

Competitive Landscape

The global short bowel syndrome market is a relatively concentrated rare disease segment, with a small number of specialized pharmaceutical companies competing in the GLP-2 analog and intestinal rehabilitation therapy space. Takeda Pharmaceutical Company Limited holds the dominant commercial position through its teduglutide franchise (Gattex in North America, Revestive in Europe), supported by established payer relationships, patient support programs, and a recognized clinical evidence base across adult and pediatric SBS populations.

The competitive landscape is characterized by active pipeline investment and regulatory designation activity. VectivBio and Entera Bio are pursuing next-generation GLP-2 formulations targeting improved patient convenience through less frequent or oral administration routes. Nestlé Health Science and Sancilio & Company contribute nutritional and adjunctive therapeutic solutions across the SBS care continuum. Strategic collaborations, licensing agreements, and orphan designation leverage are key competitive tools shaping market positioning as the pipeline matures toward commercialization through 2033.

Key Industry Developments:

- In April 2025, researchers at Weill Cornell Medicine developed a preclinical gene-editing strategy that reprogrammed colon cells to function like nutrient-absorbing cells of the small intestine, offering a potential new treatment approach for short bowel syndrome. By deleting the SATB2 gene, the team converted cells in the upper colon into ileum-like cells, restoring nutrient absorption, reversing weight loss, and significantly improving survival in preclinical models. The researchers also successfully applied the approach to human colon organoids using an adeno-associated virus (AAV)-based gene-editing system, supporting its future potential as a gene therapy for short bowel syndrome.

Companies Covered in Short Bowel Syndrome Market

- Takeda Pharmaceutical Company Limited

- Zealand Pharma

- Hanmi Pharm Co. Ltd.

- Jaguar Health

- Entera Bio Ltd.

- Nestlé Health Science

- Ardelyx

- VectivBio

- Sancilio & Company