- Off-Road Equipment & Machinery

- Ship-to-Shore Container Cranes Market

Ship-to-Shore Container Cranes Market Size, Share, and Growth Forecast 2026 - 2033

Ship-to-Shore Container Cranes Market by Crane Type (Panamax STS Cranes, Post-Panamax STS Cranes, Super Post-Panamax STS Cranes, Ultra-Large STS Cranes), by Power Supply Type (Diesel, Electric, Hybrid), by Outreach (Upto 40m, 41m to 50m, 51m to 60m, Above 60m), by Application (Transshipment Ports, Domestic Ports, Specialized Cargo Terminals), by Regional Analysis, 2026 - 2033

Ship-to-Shore Container Cranes Market Size and Trend Analysis

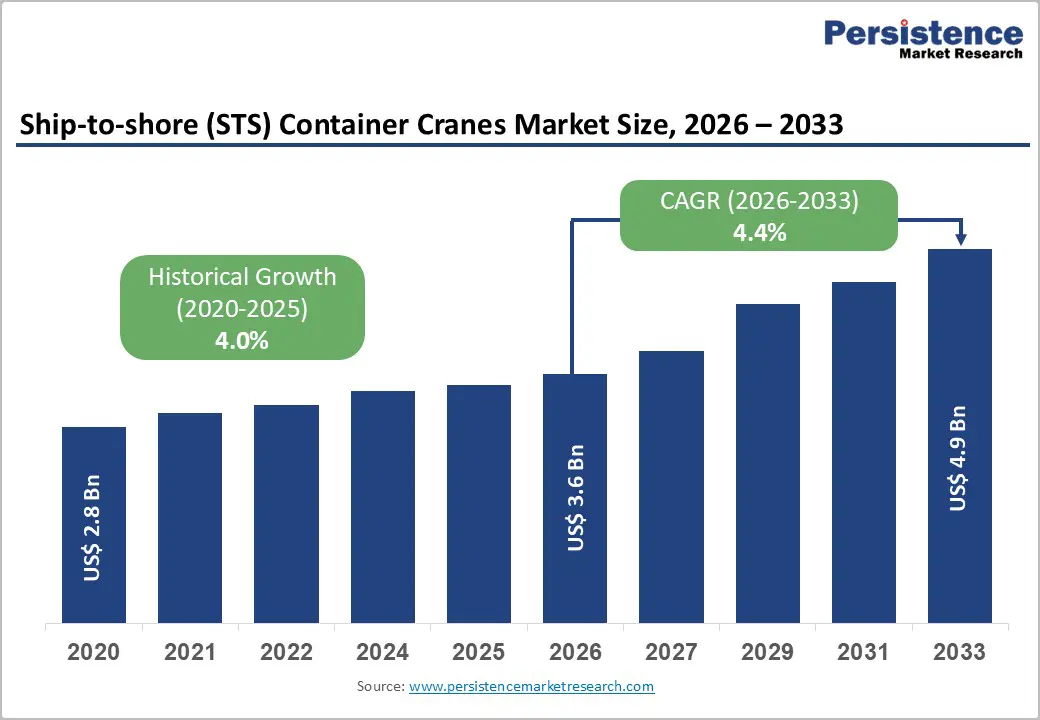

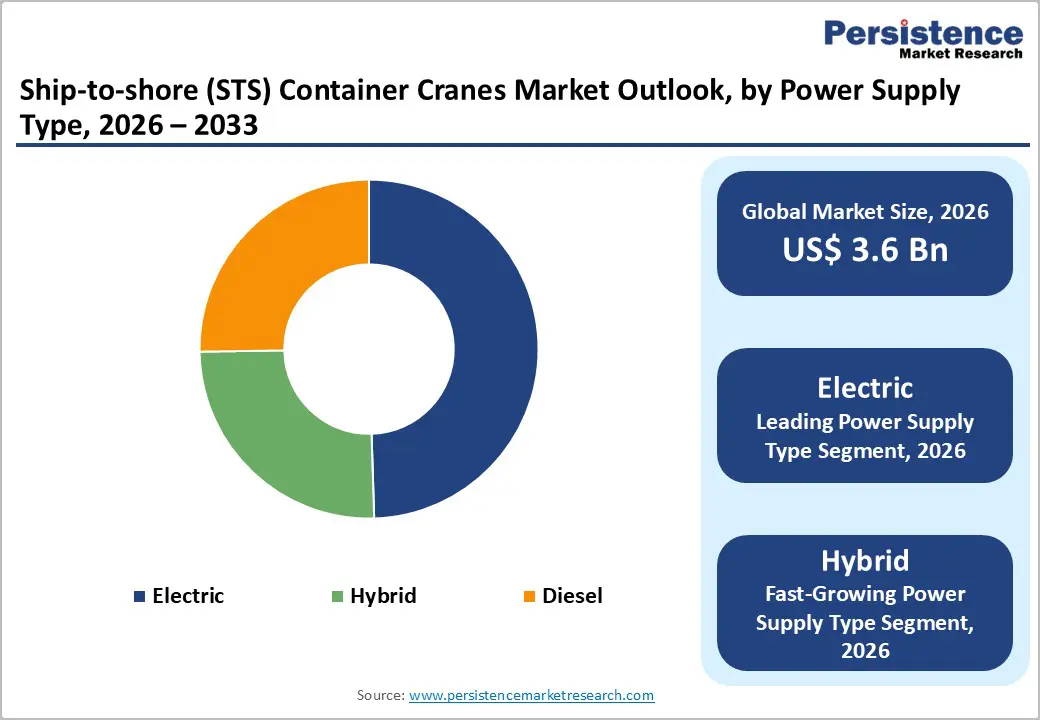

The global ship-to-shore (STS) container cranes market size is expected to be valued at US$ 3.6 billion in 2026 and projected to reach US$ 4.9 billion by 2033, growing at a CAGR of 4.4% between 2026 and 2033.

The market expansion is primarily driven by the acceleration of global containerized trade and port infrastructure modernization initiatives across emerging economies. The increasing size of vessels and the deployment of mega container ships, capable of carrying over 20,000 TEUs (twenty-foot equivalent units), necessitate investment in advanced, high-capacity crane systems. Port operators worldwide are upgrading their equipment to accommodate these larger vessels, handle increased throughput efficiently, and meet stringent environmental regulations requiring cleaner operations through electrification.

Key Market Highlights

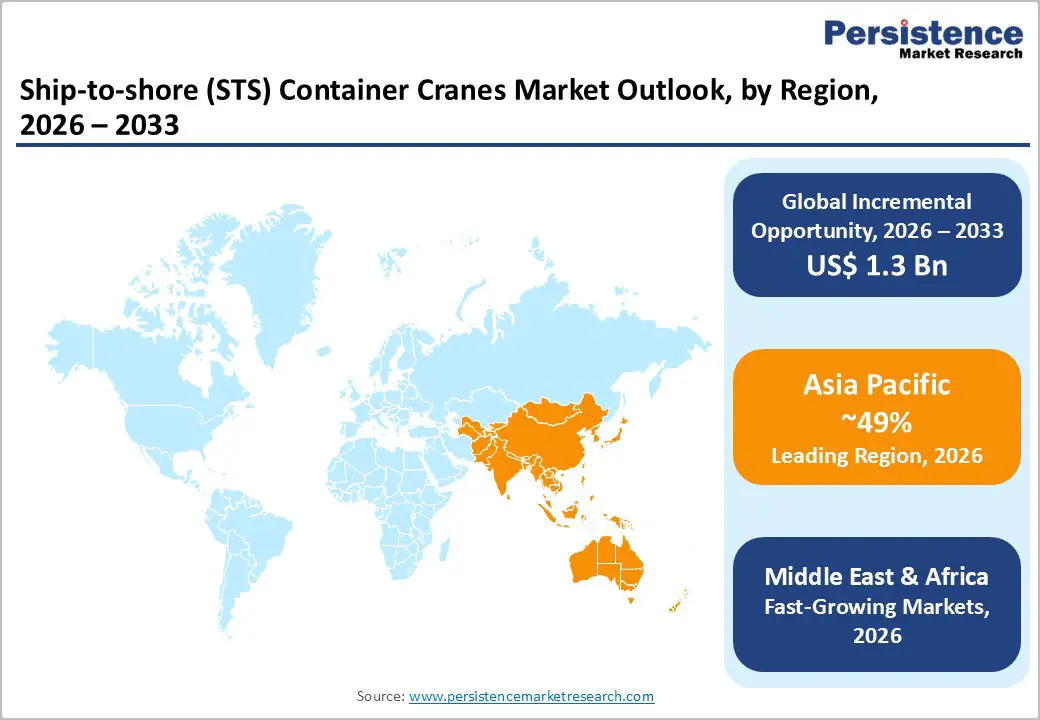

- Leading Region: Asia-Pacific dominance in global STS crane market with 49% market share in 2025, driven by robust containerized trade volumes, mega-port facilities, and government infrastructure investment programs supporting port modernization and expansion initiatives throughout the region.

- Fastest Growing Region: Middle East & Africa represents the fastest-growing regional market, projected to achieve 4.2% CAGR through 2032, supported by government infrastructure funding, vessel size expansion, automation adoption, and strategic port development projects.

- Dominant Segment: Electric-powered STS cranes represent the dominant product segment with 42% market share in 2025, reflecting accelerating adoption of sustainable port operations and compliance with environmental regulations mandating reduced carbon emissions and zero on-site operational pollution.

- Fastest Growing Segment: Hybrid-powered STS cranes emerge as the fastest-growing segment, anticipated to achieve 6.2% CAGR through 2032, offering port operators transition solutions combining operational flexibility with emissions reduction during infrastructure upgrades and power supply system modernization.

- Key Opportunity: Port automation and digital integration represent key market opportunity worth billions in value, with smart port technologies including AI-driven scheduling, IoT sensor networks, and remote operational capabilities transforming competitive dynamics and enabling ports to optimize throughput while reducing labor costs.

| Key Insights | Details |

|---|---|

|

Ship-to-Shore Container Cranes Market Size (2026E) |

US$ 3.6 billion |

|

Market Value Forecast (2033F) |

US$ 4.9 billion |

|

Projected Growth CAGR(2026-2033) |

4.4% |

|

Historical Market Growth (2020-2025) |

4.0% |

Market Dynamics

Drivers - Rising Global Trade and Port Capacity Expansion

The increasing volume of global merchandise trade continues to drive demand for advanced port infrastructure, including ship-to-shore container cranes. According to international trade organizations, global merchandise trade reached US$ 25.3 trillion in 2022, with containerized goods representing a significant portion of this activity. Emerging economies in Asia-Pacific, particularly China, India, and Southeast Asia, are experiencing rapid economic growth coupled with expanding import-export activities. These developments have prompted major port authorities to invest substantially in modern cargo handling equipment.

The trend toward establishing mega-ports and regional transshipment hubs further accelerates STS crane procurement, as ports compete for higher throughput and operational efficiency. Port development initiatives like India’s Sagarmala Program and China’s Belt and Road Initiative include substantial capital allocations for port modernization, directly increasing demand for advanced crane technology.

Shift Toward Automation and Smart Port Technology

Port automation has emerged as a transformative trend, with terminal operators investing in intelligent container handling systems to improve productivity, safety, and reliability. Modern STS cranes now integrate artificial intelligence, Internet of Things (IoT), and remote operation capabilities, enabling operators to manage crane operations without direct line-of-sight visibility. The global port automation market is projected to grow at a CAGR of 10% from 2026 to 2033.

Automated terminals equipped with STS cranes achieve significantly higher throughput rates and reduced turnaround times for vessels. For example, fully automated container terminals in Asia-Pacific and Europe demonstrate 20% to 30% improvements in handling efficiency compared to conventional operations. Leading global terminal operators are increasingly specifying automation-capable cranes during procurement cycles, recognizing that investment in these systems enhances operational resilience and competitive positioning.

Restraints - High Capital Investment and Infrastructure Constraints

The acquisition and installation of ship-to-shore container cranes represents a substantial capital commitment for port operators, with individual units ranging from US$ 8 million for Panamax cranes to over US$ 15 million for Ultra-Large STS cranes. This significant financial barrier is particularly restrictive for developing port authorities with constrained budgets. Additionally, many existing port facilities face physical constraints that limit crane installation, including insufficient quay length, inadequate power supply infrastructure, and limited space for crane operation.

Ports in developing regions of Africa, Latin America, and South Asia often struggle with outdated equipment and underfunding, with some facilities achieving only 10-20 container moves per crane hour compared to 25-30 moves at leading global ports. These operational constraints result in extended port stays and elevated demurrage costs, creating a cycle where port authorities must prioritize revenue-generating capacity expansion over equipment modernization.

Labor Market and Operational Challenges

The transition toward automation-based port operations creates significant labor market disruptions, with union opposition and workforce retraining requirements presenting substantial barriers to crane modernization initiatives. In the United States, port labor agreements often stipulate that only unionized workers can perform certain functions and that terminals maintain minimum employment levels, creating resistance to automation technology deployment.

While labor shortages exist in some regions due to aging workforces, the concentrated resistance to technological displacement in major port hubs slows adoption of advanced, automated STS cranes. Furthermore, the implementation of fully automated container terminals requires comprehensive infrastructure upgrades with estimated costs ranging from US$ 500 million to US$ 1 billion, creating financial and operational challenges that deter investment decisions.

Opportunity - Electrification and Sustainable Port Operations

Environmental regulations and port decarbonization commitments are driving substantial demand for electric and hybrid-powered STS cranes. The European Union’s maritime sustainability regulations mandate zero-emission requirements for container ships at berth beginning in 2030, while port authorities across North America and Asia-Pacific are establishing carbon neutrality targets. Electric and hybrid cranes reduce carbon emissions by 50% to 60% compared to conventional diesel-powered units while providing additional benefits including reduced operational noise and lower fuel costs.

Major port operators, including Port of Singapore Authority, have committed to replacing over 90% of diesel yard cranes with electric or hybrid variants by 2030. This massive transition represents a multi-billion-dollar market opportunity for manufacturers developing advanced electrified crane systems, regenerative braking technology, and integrated power management solutions. As renewable energy infrastructure expands globally, the operational cost advantage of electric cranes continues improving, accelerating adoption across mature and emerging port markets.

Emerging Market Port Infrastructure Development

Developing economies across Asia-Pacific, Middle East, and Africa are prioritizing port modernization as part of broader infrastructure and trade expansion strategies. The Asia-Pacific port infrastructure market alone is representing a significant growth opportunity for STS crane manufacturers. Transshipment hubs in developing regions, particularly in the Middle East and Southeast Asia are expanding capacity to accommodate mega-vessel traffic and support regional trade networks.

Government investments in these facilities create immediate procurement opportunities for advanced, high-capacity cranes capable of handling next-generation container vessels. Additionally, the container transshipment market is growing faster in creating new hubs such as Sri Lanka’s Port of Colombo and UAE’s port facilities driving equipment demand. This trend is particularly favorable for manufacturers offering comprehensive solutions including installation, financing, and technical support tailored to developing market conditions.

Category-wise Analysis

Crane Type Insights

Super Post-Panamax cranes represent the leading crane segment within the ship-to-shore market, commanding approximately 35% market share in 2025. These vessels, capable of handling 14,000 to 19,000 TEU capacities, have become the preferred choice for major global ports seeking to optimize operational economics. The predominance of Super Post-Panamax cranes reflects their optimal balance between handling capacity, operational flexibility, and acquisition cost compared to Ultra-Large alternatives.

Major container shipping alliances have standardized vessel specifications around the 18,000 to 19,000 TEU range, creating standardized procurement requirements for port terminals. The fastest-growing crane segment is Ultra-Large STS cranes, projected to achieve a 5.8% CAGR through 2033, driven by the deployment of mega container vessels exceeding 20,000 TEUs and port competition for handling capacity. These cranes feature extended outreach, enhanced lifting capacity, and advanced automation capabilities, commanding premium pricing that reflects their technological sophistication and operational advantages in high-volume transshipment terminals.

Power Supply Type Insights

Electric-powered STS cranes have emerged as the dominant power supply category, capturing approximately 42% market share in 2025, reflecting a fundamental shift toward sustainable port operations. The superior operational efficiency and zero on-site emissions of electric systems make them the preferred choice for environmentally conscious port operators and regions with stringent emissions regulations. Electric cranes demonstrate lower total cost of ownership through reduced fuel consumption and maintenance requirements while providing integration with renewable energy infrastructure.

The fastest-growing power supply segment is hybrid-powered cranes, anticipated to achieve a 6.2% CAGR through 2032 as port operators seek transition solutions that maintain operational flexibility during infrastructure upgrades. Hybrid systems combine diesel and electric power with regenerative braking capabilities, enabling ports to reduce emissions while maintaining operational reliability during peak demand periods and infrastructure transitions.

Outreach Insights

The market’s fastest-growing outreach segment is vessels exceeding 60m outreach, projected to achieve 5.5% CAGR through 2033, driven by expansion of ultra-large container vessel handling capacity. Ports investing in new terminal facilities and mega-ship accommodation specifically specify cranes with 60m+ outreach to future-proof their operations against projected vessel size increases. These extended-reach systems enable efficient loading and unloading of 20,000+ TEU vessels while maintaining operational flexibility for handling smaller conventional vessels. The escalating capital requirements and specialized engineering for extended outreach cranes create opportunities for manufacturers to capture premium pricing and establish long-term relationships with major port operators.

Application Insights

Transshipment ports have established themselves as the leading application segment, commanding approximately 44% of the STS crane market in 2025. Transshipment operations, where containers are transferred between vessels at intermediate ports, drive concentrated investments in high-capacity, high-throughput crane systems. Major transshipment hubs including Singapore, Rotterdam, Hong Kong, and Shanghai operate multiple STS cranes with advanced automation capabilities to process millions of TEUs annually. Growth in perishable goods trade, particularly for fresh produce and pharmaceutical products, has driven expansion of temperature-controlled container handling, creating demand for cranes optimized for specialized cargo operations and meeting stringent handling standards.

Regional Insights

North America Ship-to-Shore Container Cranes Market Trends and Insights

The North America ship-to-shore (STS) container cranes market is driven by sustained modernization of large container ports and rising trade-linked cargo throughput. Major U.S. ports, including Los Angeles, Long Beach, Savannah, and New York–New Jersey, collectively handle more than 40 million TEUs annually, necessitating continuous upgrades in crane capacity, outreach, and automation readiness. Strong public investment under the U.S. Port Infrastructure Development Program, with nearly US$ 580 billion allocated across 15 states and one territory, is supporting terminal expansion and equipment replacement initiatives.

The regional market is projected to grow at around 3.8% CAGR through 2033, supported by increasing vessel sizes, labor availability constraints, and the need to improve berth productivity. North American ports are progressively adopting automation-capable STS cranes, with multiple fully automated and semi-automated terminals now operational on both the West and East Coasts. Operational efficiency, safety improvement, and long-term cost optimization remain central procurement priorities.

Europe Ship-to-Shore Container Cranes Market Trends and Insights

Europe’s ship-to-shore container cranes market is shaped by mature port infrastructure and stringent environmental and emissions regulations. Leading ports such as Rotterdam, Antwerp, Hamburg, and Barcelona are increasingly investing in electric and hybrid STS cranes to align with European Union decarbonization objectives. The implementation of the European emissions trading scheme for shipping from January 2025 has further accelerated investments in low-emission port equipment, encouraging operators to reduce lifecycle carbon intensity.

The market is expected to expand at approximately 3.5% CAGR through 2033, with growth largely concentrated in electrification, automation, and digital integration. European port authorities are collaborating closely with crane manufacturers to deploy intelligent systems that enable real-time emissions monitoring, predictive maintenance, and operational optimization. Advanced drive technologies and automation capabilities remain key competitive differentiators, particularly for manufacturers leveraging engineering expertise to support sustainable port transformation and compliance with evolving regulatory frameworks.

Asia Pacific Ship-to-Shore Container Cranes Market Trends and Insights

Asia Pacific dominates the global ship-to-shore container cranes market, accounting for approximately 49% of total market share in 2025, reflecting its central role in global containerized trade. China’s extensive port network, led by Shanghai, Ningbo-Zhoushan, and Shenzhen, collectively handles over 500 million TEUs annually, with Shanghai alone exceeding 47 million containers in recent years. India is also emerging as a high-growth market, with major ports recording a 10% increase in container traffic during 2024–25 and total cargo volumes reaching 855 million tonnes, driving new crane procurement.

The regional market is projected to grow at around 5.1% CAGR through 2033, the fastest globally. Japan and South Korea continue to demonstrate leadership in automation and digital port integration, while Chinese manufacturers, led by Shanghai Zhenhua Heavy Industries, maintain global scale advantages through high-volume deliveries and competitive manufacturing capabilities.

Competitive Landscape

The global ship-to-shore container cranes market demonstrates a moderately consolidated structure, shaped by high capital intensity, long project cycles, and significant technological entry barriers. Competition is primarily driven by scale manufacturing capabilities, engineering expertise, and the ability to deliver customized solutions for large container terminals. Market participants increasingly differentiate through advanced automation readiness, electrification, and digital control systems that enhance operational efficiency and reduce lifecycle costs. Strategic emphasis is shifting toward integrated offerings that combine equipment supply with long-term maintenance, remote diagnostics, and performance optimization services.

Partnerships and selective acquisitions are being used to strengthen technology portfolios and expand service footprints across key port regions. Manufacturers are also investing in digitalization, including predictive maintenance platforms, cybersecurity features, and data-driven asset management tools, to align with evolving port operator requirements. Regional production and service localization remain critical business strategies, enabling faster project execution, regulatory compliance, and closer collaboration with port authorities and terminal operators worldwide.

Key Market Developments

- October 2024: APM Terminals Maasvlakte II placed substantial order for automated quay cranes from Konecranes as part of comprehensive port modernization initiative, confirming continued market demand for automation-capable systems in major European port hubs.

- July 2025: Liebherr announced completion of its 2000th mobile harbor crane delivery, symbolizing decades of technological advancement and establishing the company as essential partner for port operators globally seeking innovative container handling solutions.

- December 2025: Liebherr signed a contract to supply two STS cranes to Port Tampa Bay, supporting the port's Vision 2030 expansion, including a 100-acre container terminal and 1 million TEU annual capacity goal.

- December 2025: ZPMC has been awarded to supply STS cranes for DP World’s greenfield Banana Port development in the Democratic Republic of the Congo, aimed at improving direct access to global container shipping.

Companies Covered in Ship-to-Shore Container Cranes Market

- Shanghai Zhenhua Heavy Industries Co., Ltd. (ZPMC)

- Liebherr-International AG

- Sany Group

- Doosan Corporation

- Cargotec (Kalmar)

- Konecranes

- PACECO Corporation

- ANUPAM-MHI Industries Limited

- Hyundai Samho Heavy Industries Co., Ltd.

- Henan Dafang Heavy Machine Co., Ltd.

- Kawasaki Heavy Industries, Ltd.

- TMEIC Corporation

- Weihua Crane Group

- GENMA

- Bedeschi S.p.A.

Frequently Asked Questions

The global ship-to-shore container cranes market is projected to reach US$ 3.6 billion in 2026, growing at a CAGR of 4.4% through 2033.

Rising containerized trade, deployment of mega container vessels, port automation, and stricter emission regulations are the key demand drivers.

Asia-Pacific leads the market with around 49% share, supported by high trade volumes and sustained port infrastructure investments.

The shift toward electric and hybrid-powered STS cranes presents the strongest growth opportunity due to decarbonization mandates and cost efficiency benefits.

Key market players include Shanghai Zhenhua Heavy Industries (ZPMC), Liebherr, Konecranes, Cargotec (Kalmar), Doosan Corporation, and Sany Group.