- Off-Road Equipment & Machinery

- Container Handling Equipment Market

Container Handling Equipment Market Size, Share, and Growth Forecast, 2026 – 2033

Container Handling Equipment Market by Propulsion Type (Diesel, Electric, Hybrid), Automation Level (Manual, Semi-Automated, Fully Automated), End-user (Seaports, Inland Container Depots, Railway Terminals), and Regional Analysis 2026 – 2033

Container Handling Equipment Market Size and Trend Analysis

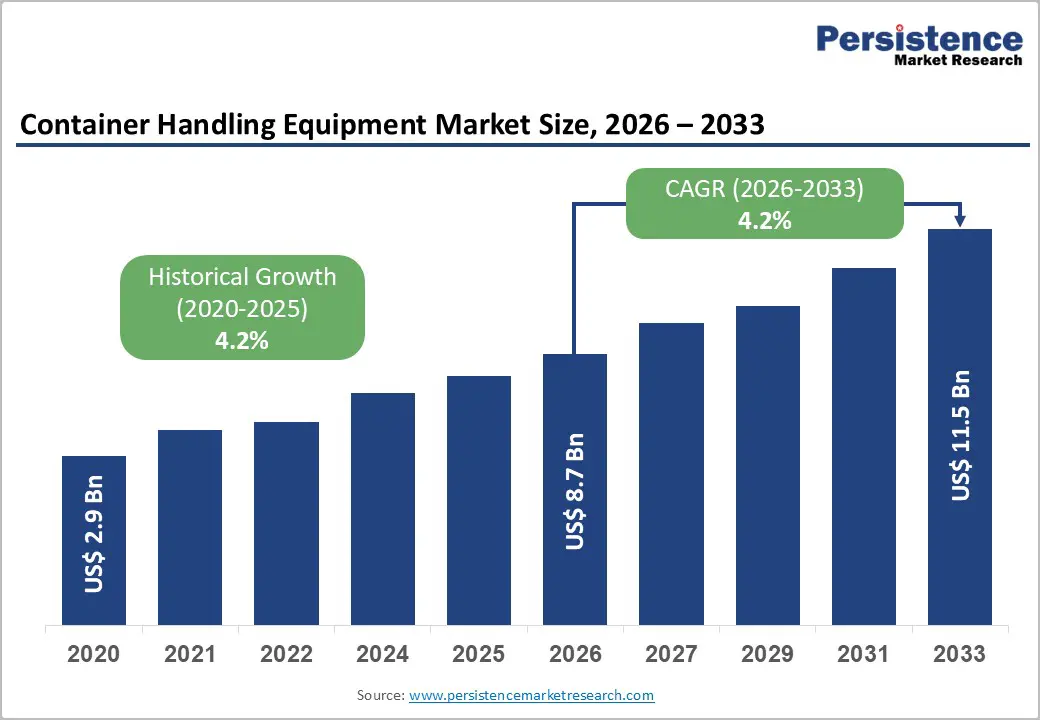

The global container handling equipment market size is likely to be valued at US$8.7 billion in 2026 and is expected to reach US$11.5 billion by 2033, growing at a CAGR of 4.2% during the forecast period from 2026 to 2033, driven by the resurgence of global maritime trade volumes following post-pandemic disruptions, necessitating higher throughput efficiency at major terminals.

Growth is further accelerated by the rapid electrification of port infrastructure to meet strict decarbonization targets set by the International Maritime Organization (IMO) and local governments. A structural shift toward port automation and smart logistics is fueling the replacement of legacy manual equipment with automated stacking cranes (ASCs) and intelligent transport solutions.

Key Industry Highlights:

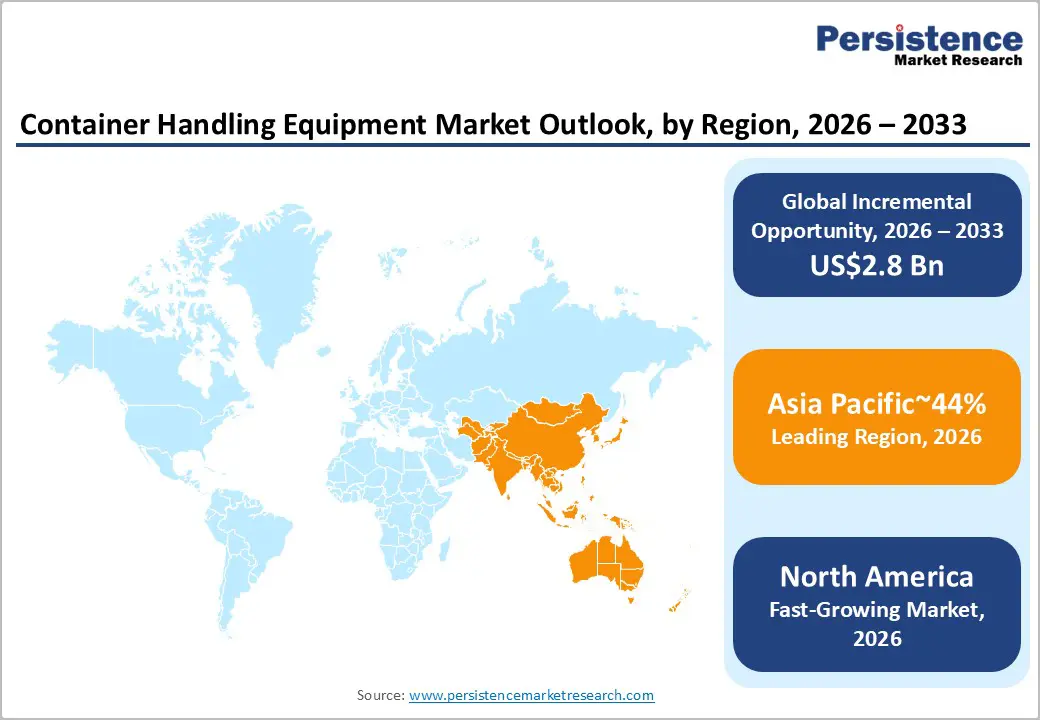

- Leading Region: Asia Pacific, to hold approximately 44% share in 2026, supported by high container throughput across China, Southeast Asia, and India, large-scale port capacity expansions, manufacturing export concentration, and sustained public and private investment in port mechanization and terminal automation.

- Fastest-growing Region: North America is expected to rank among the fastest-growing regions in the container handling equipment market, fueled by port modernization efforts, tighter emissions standards, and ongoing federal infrastructure investments.

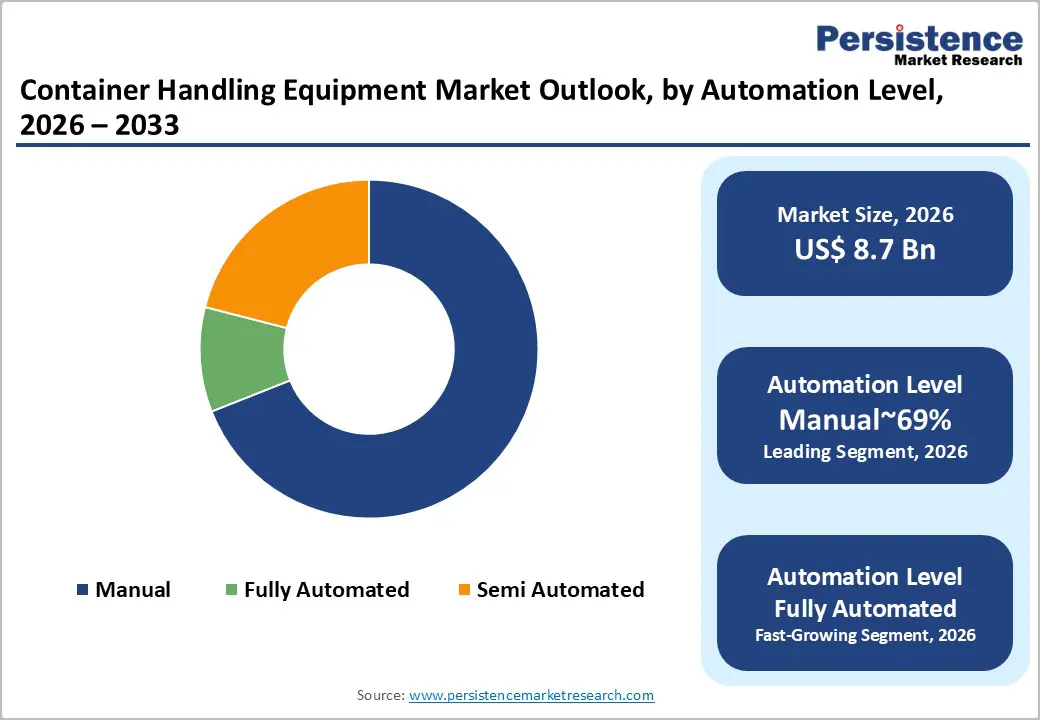

- Leading Automation Level: Manual equipment operations represent approximately 69% share, reflecting the continued dominance of conventional operator-driven equipment across small and mid-scale terminals and developing port markets where capital-intensive automation adoption remains gradual.

- Leading Propulsion Type: Diesel-powered equipment holds around 58% share, supported by its entrenched installed base in heavy-duty port operations, high torque requirements for loaded container handling, and continued reliance on diesel infrastructure in emerging market ports.

| Key Insights | Details |

|---|---|

| Container Handling Equipment Market Size (2026E) | US$8.7 Bn |

| Market Value Forecast (2033F) | US$11.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Global Trade Expansion and Port Capacity Growth

Rising seaborne trade and diversification of trade lanes are driving higher throughput pressure on global ports, increasing demand for high-capacity, and automated container handling equipment. Growth in manufacturing and cross-border e-commerce is intensifying vessel call frequency and yard density, pushing terminals to upgrade ship-to-shore interfaces, horizontal transport, and stacking infrastructure to maintain service levels. The geographic shift in trade flows toward intra-regional corridors and emerging maritime hubs requires ports to adapt equipment fleets for varying vessel sizes and cargo types. These shifts align equipment renewal cycles with broader goals of trade elasticity and network resilience.

Simultaneously, port infrastructure expansion is reshaping capital and technology profiles, with larger vessel classes and chronic congestion raising dwell time costs. This strengthens the need for automated stacking systems, high-reach cranes, and digitally orchestrated yard equipment. Regulatory pressures around safety, emissions, and efficiency are pushing ports toward electrified, automation-ready machinery, further driving demand for advanced container handling systems.

Electrification Mandates and Decarbonization Push

Regulatory decarbonization frameworks are reshaping demand across the container handling equipment value chain, turning electrification from a sustainability choice into a compliance necessity. International maritime decarbonization targets drive port-level mandates for zero-emission berth operations and terminal electrification, while regional policies impose emissions limits on cargo handling fleets. These regulations increase the risk for diesel-powered assets, accelerating the shift to electric and alternative energy platforms. As ports adopt climate disclosure and air quality standards, equipment procurement now prioritizes lifecycle emissions alongside productivity, influencing vendor selection and investment strategies.

Cost structures are also evolving, with energy price fluctuations and lower maintenance needs making electrified drivetrains more cost-effective than internal combustion engines. This reduces the total cost of ownership, partly offsetting higher initial capital costs. Financing conditions also support the transition, as ESG-linked funding offers lower-cost capital for measurable decarbonization progress. Battery-electric and hydrogen systems offer distinct technology paths based on duty cycles and uptime, integrating energy infrastructure into long-term terminal strategies.

Barrier Analysis – Geopolitical Volatility and Supply Chain Fragmentation

The production footprint of heavy container handling equipment remains geographically concentrated, embedding geopolitical exposure into equipment availability, pricing stability, and delivery reliability. Trade tensions, sanctions regimes, and disruptions across critical maritime corridors fragment component supply chains and elevate logistics risk across upstream steel, power electronics, and control systems sourcing. This concentration amplifies vulnerability to policy-driven trade frictions and corridor insecurity, translating geopolitical events into tangible delays in equipment manufacturing and cross-border delivery. As ports and terminal operators depend on synchronized availability of large-format machinery, these disruptions propagate across project timelines and capital deployment cycles.

At the value-chain level, extended lead times for semiconductors, control modules, and specialty steel propagate into deferred commissioning of port expansion and modernization programs. Schedule slippage increases carrying costs on partially completed infrastructure and erodes expected efficiency gains from automation and electrification programs. Regulatory compliance timelines and financing milestones become harder to align with volatile delivery windows, raising execution risk for large-scale terminal investments. These constraints structurally limit near-term equipment throughput and reinforce procurement diversification strategies, while elevating inventory buffering and supplier qualification costs across the industrial logistics ecosystem.

Opportunity Analysis – Brownfield Terminal Automation Retrofitting

Automation demand in container terminals is increasingly focused on brownfield environments, where legacy infrastructure limits full replacement, but pressure on throughput, safety, and land-use efficiency remains high. Hybrid automation solutions allow phased integration of automated stacking, guided transport, and digitally orchestrated yard management alongside human-operated equipment, maintaining operational continuity while boosting productivity and space utilization. This modular approach suits the physical and contractual limitations of existing terminals, where berth design, yard layout, and power systems hinder complete greenfield automation. As congestion and labor coordination complexity grow, retrofit-compatible automation becomes essential for enhancing capacity within fixed port footprints.

Retrofit programs shift capital expenditure toward software-defined control layers, sensors, and partial equipment upgrades rather than full terminal redevelopment. This drives value toward integrators capable of connecting automation modules with existing legacy systems. Regulatory safety and continuity requirements further favor incremental automation, expanding the market for modular automation kits, control software, and interoperability services in mature port ecosystems.

Hydrogen and Modular Charging Innovations

Decarbonizing terminal equipment is facing operational bottlenecks as battery-electric fleets struggle with continuous duty cycles and limited charging opportunities in high-throughput port environments. This challenge increases the strategic importance of hydrogen fuel cell systems and modular energy solutions capable of supporting round-the-clock operations without compromising emissions goals. Hydrogen platforms offer the energy density and refueling speed needed for heavy-duty equipment, while modular power units and mobile storage address grid capacity limitations, enabling simultaneous charging at scale. These solutions integrate energy provision into terminal design, linking equipment uptime with on-site fueling, storage, and power management.

At the value-chain level, alternative energy deployments shift capital toward fueling networks, containerized energy modules, and digital charging orchestration, broadening the market beyond equipment into infrastructure and services. Regulatory decarbonization mandates increase compliance risks for terminals with grid limitations, driving demand for interoperable, deployable energy solutions. Retrofitting mechanical platforms with alternative drivetrains further extends asset utility, creating opportunities for providers at the intersection of electrification, energy infrastructure, and modular retrofitting.

Category-wise Analysis

Propulsion Type Insights

Diesel propulsion is projected to dominate the container handling equipment market, accounting for approximately 58% share, underpinned by entrenched fleet bases, high torque requirements for heavy-duty lift cycles, and constrained grid capacity across developing port ecosystems. Adoption remains anchored by diesel’s superior energy density, operational resilience in continuous duty cycles, and reliability across climate extremes, with terminal operators prioritizing throughput stability and uptime in just-in-time logistics environments. Ongoing platform evolution, including compliance with Stage V and Tier 4 Final standards, integration of telematics for idle reduction, hybrid diesel-electric architectures, and compatibility with renewable diesel fuels, continues to extend asset life and utilization intensity. Vendors such as SANY, ZPMC, Caterpillar, Cummins, and Liebherr are expanding compliant powertrains and retrofit pathways to lock in long-term fleet contracts.

Electric propulsion is projected to be the fastest-growing segment within the container handling equipment market, driven by port decarbonization mandates and tightening emissions regulations across major trade corridors. Growth is being catalyzed by falling battery costs, robotic battery swapping, Battery as a Service models, and AI-driven battery management, which materially improve duty-cycle viability, charging turnaround, and total cost of ownership. Accelerating adoption is supported by microgrids, on-site energy storage integration, and zero-emission berth requirements, lowering operational friction for first-time electric fleet deployments. Companies including Konecranes, Kalmar, Hyster, SANY, and GAUSSIN are scaling electric platforms and automation-ready architectures to capture early-cycle demand and embed switching costs.

Automation Level Insights

Manual operations are expected to remain dominant in the container handling equipment market, comprising around 69% of the share by 2026. This dominance is driven by constraints in brownfield port environments, existing labor frameworks, and the high capital cost of full terminal automation. Manual operations continue to be favored due to human operators’ ability to manage exceptions in dynamic, chaotic yard environments, with terminals prioritizing flexibility, scalability, and resilience in the face of weather disruptions or network failures. Ongoing advancements in human-in-the-loop control, remote piloting, AI-based active safety, and terminal operating system integration are enhancing productivity without displacing operators. Companies such as SANY, Hyster-Yale, Liebherr, Taylor Machine Works, and Kalmar are focusing on ergonomics, ADAS features, and automation-ready designs to ensure fleet upgrades and secure service contracts, maintaining manual operations’ dominance in global ports.

Fully automated operations are projected to be the fastest-growing segment in the market, fueled by Industry 4.0 technologies, labor shortages, and the rise of ultra-large container vessels. Key drivers include private 5G networks, digital twin orchestration, autonomous yard tractors, and predictive maintenance. Automation-as-a-service models, greenfield port developments, and interoperability frameworks are reducing entry barriers for mid-sized terminals. Major players such as ZPMC, Konecranes, Kalmar, ABB, TEREX Gottwald, and Gaussin are scaling automation solutions to capture early demand. As regulatory clarity around AI and cyber resilience evolves, fully automated terminals are set to outpace overall market growth.

Regional Insights

Asia Pacific Container Handling Equipment Market Trends

Asia Pacific is expected to lead the global container handling equipment market, commanding an estimated 44% share in 2026. This regional dominance is driven not only by volume but also by the concentration of nine of the world’s ten busiest container ports, creating continuous demand for high-capacity and automated equipment. China, India, and Singapore are the core contributors, with Chinese manufacturers such as ZPMC and SANY exporting turnkey automated terminal solutions, while India’s Adani Ports and Singapore’s Tuas Port showcase large-scale deployment of electric and automated machinery.

Industrial developments underscore the region’s leadership. ZPMC has secured major contracts for fully automated Ship-to-Shore cranes across Southeast Asia, while SANY and Fosun are trialing hydrogen-powered reach stackers in tropical conditions. Advanced technologies, including AI-vision systems for container identification and 5G-enabled port ecosystems in Ningbo-Zhoushan, allow simultaneous real-time control of hundreds of machines. Cost advantages, ongoing Greenfield port construction, and government-backed infrastructure programs such as China’s Belt and Road Initiative and India’s Sagarmala Programme reinforce APAC’s scale advantage, while high utilization rates accelerate equipment replacement cycles, solidifying the region’s position as the global growth powerhouse.

North America Container Handling Equipment Market Trends

North America is projected to be one of the fastest-growing regions in the container handling equipment market, driven by port modernization initiatives, stricter emissions regulations, and continued federal infrastructure funding. The region's growth is underpinned by the U.S.’s port automation agenda and Canada’s intermodal capacity upgrades. Regulatory tightening on emissions and cybersecurity is expected to reinforce demand for electric and digitally enabled equipment, positioning North America as a high-value, compliance-driven market relative to Asia Pacific’s volume-led profile. Demand is expected to concentrate around automated yard systems and electric handling fleets as terminals seek to address labor scarcity, congestion, and service-level requirements across coastal and inland logistics corridors.

Infrastructure funding under the Infrastructure Investment and Jobs Act is expected to continue translating into procurement cycles for zero-emission and automated equipment, while California Air Resources Board at-berth rules and EPA DERA incentives are likely to anchor replacement demand through regulatory deadlines rather than discretionary capex. Technology adoption is anticipated to prioritize digital twin simulation, IoT-enabled asset monitoring, and secure-by-design control systems, with early deployments concentrated at West Coast gateways. Competitive positioning is expected to remain anchored by established OEMs and platform providers, including Konecranes, Kalmar, Hyster-Yale, Taylor Machine Works, and Mi-Jack, which are increasingly aligning product roadmaps to electrification, automation, and cybersecurity compliance requirements across North American port and intermodal environments.

Europe Container Handling Equipment Market Trends

Europe remains a strategically significant container handling equipment market, characterized by its mature infrastructure yet strong orientation toward technological modernization. Leading hubs such as Rotterdam, Hamburg, Antwerp-Bruges, Genoa, and Gdansk exemplify the regional diversity, with Northern ports focusing on high-volume industrial throughput and Southern ports emphasizing retrofit and automation initiatives. Growth is driven by the adoption of advanced electrified and hybrid equipment, including electric RTGs, automated straddle carriers, and hydrogen-ready handlers. Industry players such as Konecranes and Kalmar are shaping the market by integrating modular drivetrains, IoT connectivity, and digital twin platforms, allowing proactive maintenance, predictive operational management, and enhanced terminal efficiency. Ports are increasingly prioritizing automation to mitigate labor volatility, while retrofit electrification programs provide scalable solutions for constrained brownfield terminals, ensuring that modernization occurs independently of new port construction.

Industrial momentum is further reinforced by targeted investments from leading European operators. Konecranes’ hydrogen fuel-cell straddle carriers and hybrid modular systems are being tested across major Northern European terminals, while Kalmar focuses on autonomous rubber-tired gantry solutions and digital service platforms. Port operators such as HHLA, EUROGATE Hamburg, and Luka Koper are spearheading adoption by procuring electric and hybrid units that can be retrofitted for future energy sources. This approach underscores a market logic centered on high-value technological replacement rather than volumetric expansion. European innovation emphasizes energy-efficient automation, operational safety, and integration of advanced control systems, positioning the region as a global laboratory for next-generation port operations. The combination of leading OEMs, forward-looking port operators, and concentrated hubs ensures Europe maintains a competitive edge in high-performance container handling, despite its mature physical footprint.

Competitive Landscape

The global heavy crane and automated systems market is moderately consolidated, led by major players such as ZPMC, Konecranes, Kalmar, Liebherr, Hyster-Yale, and Sany. European firms excel in automation, digitalization, and service models, while Asian leaders focus on cost, scale, and fast delivery. Companies differentiate through horizontal and vertical strategies, with Western firms emphasizing advanced technology and Asian firms leveraging volume and competitive pricing. Niche specialization targets areas such as mobile equipment and automated ports. The market sees ongoing consolidation via M&A, particularly in service offerings, ensuring uptime. Digital integration and automation drive platform evolution, while Chinese vertical integration challenges European pricing. Trends suggest a balance between innovation and scale in future competition.

Key Industry Developments:

- In February 2026, the Union Government of India signed a Memorandum of Understanding to establish the Bharat Container Shipping Line (BCSL) as part of an integrated domestic container ecosystem. This initiative, backed by a ?10,000 crore (US$1.2 billion) outlay, aims to scale indigenous production and reduce reliance on global supply chain fluctuations while boosting the local manufacturing sector.

- In January 2026, Adani Ports marked a significant milestone for India's export-import trade. The increased handling of over 44.8 million metric tons demonstrates improved port management capabilities and higher operational efficiency across liquid, container, and dry cargo segments.

- In October 2025, the global debut of the Noell hydrogen fuel-cell straddle carrier at the TOC Americas event will follow successful trials in Hamburg. This breakthrough product offers a zero-emission alternative for heavy-duty lifting without the long charging downtimes of standard electric units, supporting global net-zero maritime targets.

Companies Covered in Container Handling Equipment Market

- Kalmar

- Konecranes

- ZPMC (Shanghai Zhenhua Heavy Industries)

- Liebherr Group

- SANY Group

- Hyster-Yale Materials Handling

- Terex Corporation (Gottwald)

- Mitsui E&S Machinery

- Mitsubishi Logisnext

- Anhui Heli

- Lonking Holdings

- CVS Ferrari

- Taylor Machine Works

- Gaussin

- Hoppecke Batterien

Frequently Asked Questions

The global container handling equipment market is projected to be valued at US$8.7 billion in 2026 and is expected to reach US$11.5 billion by 2033, driven by the resurgence of global maritime trade and the accelerating electrification and automation of port infrastructure.

Rising seaborne trade and port congestion are increasing pressure on terminals, requiring investments in high-capacity, automated equipment to boost vessel turnaround and yard efficiency, while aligning with broader trade growth and port modernization efforts.

The global container handling equipment market is forecast to grow at a CAGR of 4.2% from 2026 to 2033, reflecting a steady demand from port capacity expansions and the gradual replacement of legacy fleets with more efficient, automated, and electric models.

Asia Pacific is the leading regional market, accounting for approximately 44% share, supported by the world's busiest container ports, massive port capacity expansions, and concentrated manufacturing and export activity across China, Southeast Asia, and India.

The container handling equipment market is moderately consolidated, with Chinese leaders like ZPMC and SANY competing on scale and cost, while European firms such as Kalmar and Konecranes lead in automation and advanced electric solutions. Other key players include Liebherr, Hyster-Yale, and Terex.