- Display Technologies

- Screenless Display Market

Screenless Display Market Size, Share, Trends, and Growth Forecast, 2026 - 2033

Screenless Display Market by Product Type (Visual Image, Retinal Display, and Synaptic Interface), Application (Consumer Electronics, Automotive & Transportation, Healthcare, Defence & Security, Industrial & Enterprise, Education & Training, Entertainment & Media), and Regional Analysis for 2026 - 2033

Screenless Display Market Size and Trends Analysis

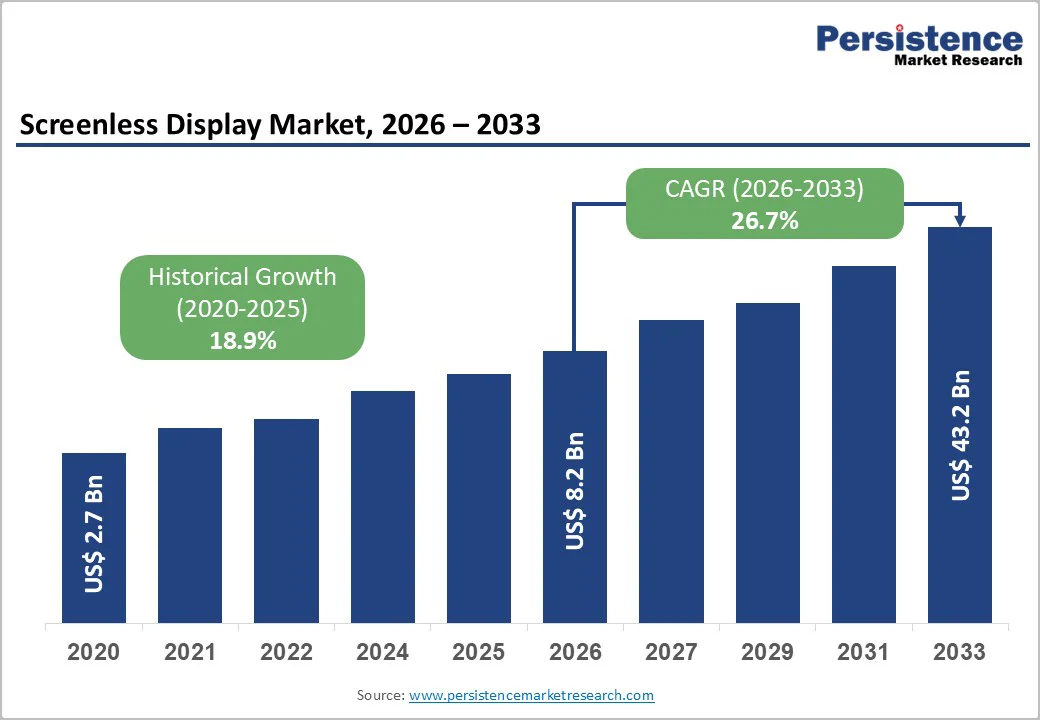

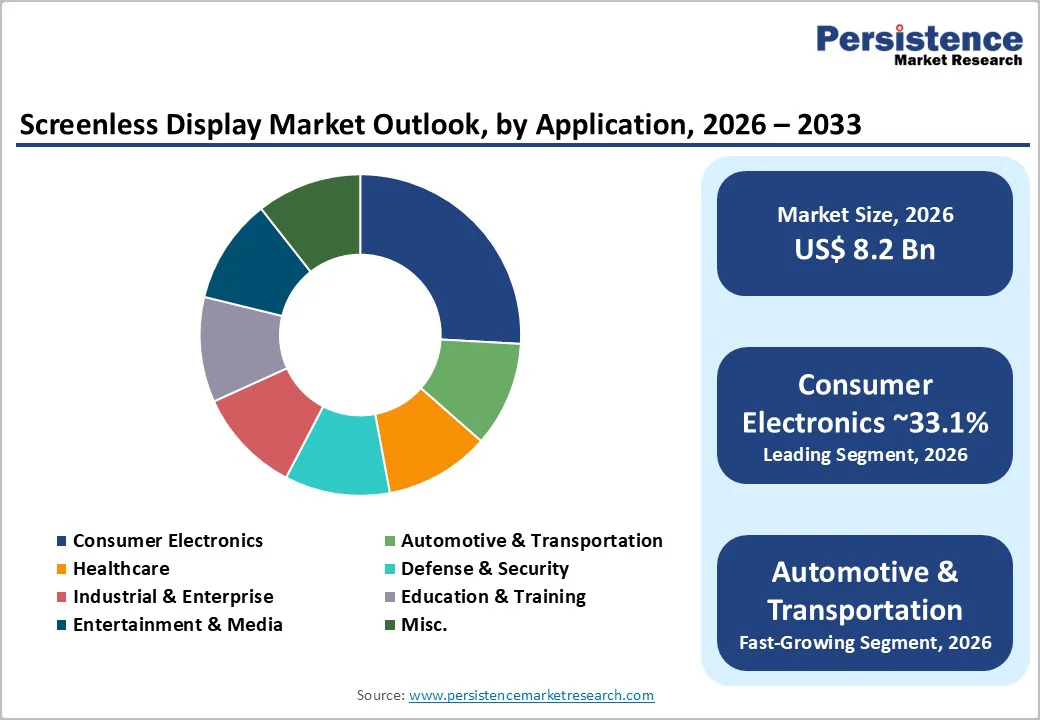

The global screenless display market size is valued at US$8.2 billion in 2026 and is projected to reach US$43.2 billion by 2033, growing at a CAGR of 26.7% between 2026 and 2033.

This exceptional growth trajectory reflects the convergence of multiple technological innovations and expanding demand across diverse industry verticals.

The market expansion is primarily driven by the accelerating adoption of augmented reality and virtual reality technologies, advancements in holographic projection capabilities, the miniaturization of micro-LED components, and the proliferation of spatial computing applications across consumer electronics, automotive systems, healthcare visualization, and defense platforms.

These interconnected factors are fundamentally reshaping how users interact with digital information, eliminating the need for traditional physical screens, and positioning the Screenless Display Market as a critical enabler of the emerging spatial computing era.

Key Industry Highlights:

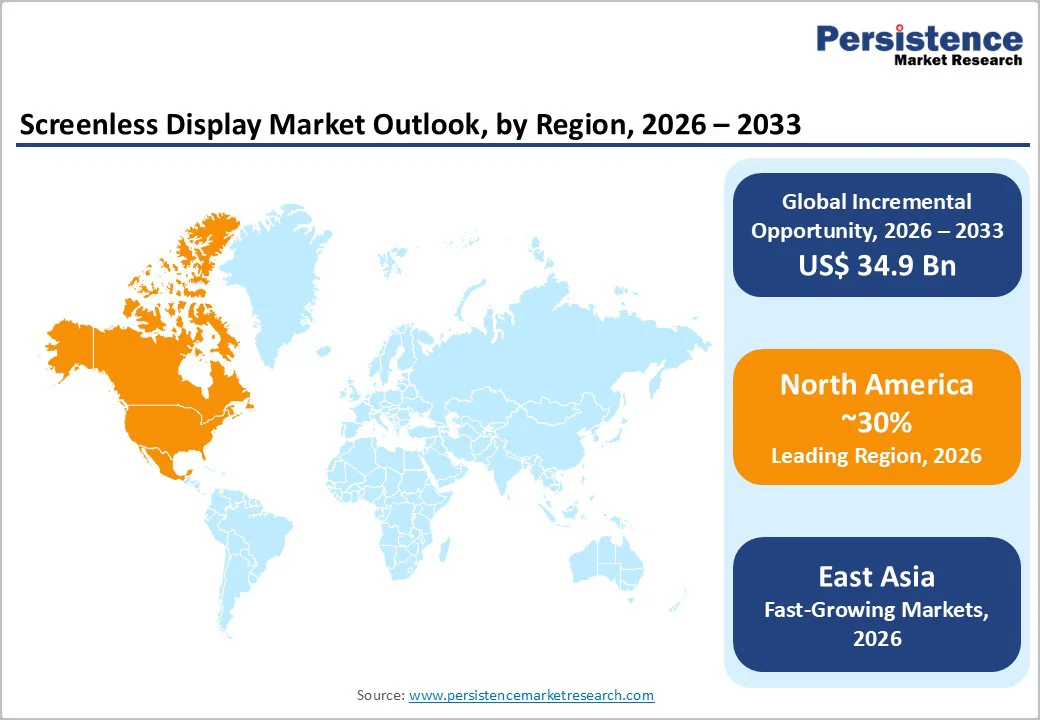

- Regional Leadership: North America holds 30.2% of the global market share in 2026, driven by technology hubs in the U.S. and strong healthcare and enterprise adoption, including military procurement contracts.

- Fastest-Growing Region: East Asia is poised for substantial growth, capturing 20.3% market share, led by China's "Digital China" initiative, which supports immersive technology development and AI integration.

- Leading Segment - Consumer Electronics: The Consumer Electronics segment commands 33.1% market share, fueled by growing adoption of AR-enabled wearables and immersive gaming platforms, alongside the rise of social media AR applications.

- Emerging Segment - Automotive & Transportation: The automotive sector emerges as the fastest-growing segment, driven by regulatory mandates for advanced driver-assistance systems and the transition to full-windshield holographic displays.

- Technology Dominance - Visual Image: Visual image screenless display technologies, including holographic projections and light-field displays, dominate the market with a 61.3% share in 2026 due to technical maturity and broad application across sectors.

- Government Digital Transformation Support: Government initiatives in Asia Pacific, particularly in China and India, create substantial infrastructure investments in smart cities and immersive technologies, accelerating screenless display commercialisation.

| Key Insights | Details |

|---|---|

| Screenless Display Market Size (2026E) | US$ 8.2 Bn |

| Market Value Forecast (2033F) | US$ 43.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 26.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 18.9% |

Market Dynamics

Drivers - Technological Miniaturization and Component Cost Reduction

The Global Screenless Display Market is experiencing substantial momentum driven by unprecedented advancements in optical engineering and materials science. Over the past three years, manufacturers have achieved critical breakthroughs in reducing the physical footprint of holographic projectors, retinal display optics, and waveguide technology-key enablers of practical screenless solutions.

Industry research indicates that optical component costs have declined by approximately 15-20% annually, with projections suggesting continued reductions as production scales. These innovations enable integration of screenless display technology into consumer wearables, automotive windshields, and industrial equipment without significant form-factor penalties.

The transition from laboratory prototypes to commercially viable products in sectors like luxury automotive, with full-windshield holographic displays introduced at CES 2025 and medical imaging, demonstrates that technical feasibility constraints have been substantially overcome.

Integration of Augmented Reality and AI-Powered Visualization

Augmented reality and virtual reality applications are catalyzing unprecedented demand for screenless display infrastructure, particularly across enterprise and professional sectors. A significant portion of the growth in AR and VR is dependent on screenless display technologies.

In healthcare specifically, AI-driven holographic visualization platforms enable surgeons to manipulate 3D anatomical models of patient organs without glasses or physical interfaces-directly addressing procedural precision and safety requirements.

Medical training institutions are adopting AR-enabled screenless displays for immersive surgical simulations, with research confirming that learners utilizing these systems demonstrate 25-35% higher skill acquisition rates compared to traditional methods.

The Global Screenless Display Market benefits directly from this confluence of AR/VR adoption and AI integration, as intelligent projection systems now adapt visual content in real-time based on user behaviour, environmental conditions, and task requirements.

Enterprise deployments in manufacturing, logistics, and field services validate commercial viability, with companies reporting workflow optimisation gains of 20-40% when implementing screenless AR solutions for remote expert guidance and collaborative design workflows.

Government Digital Transformation Initiatives and Smart City Infrastructure

Asia Pacific governments are deploying comprehensive digital transformation strategies that inherently favour screenless display technologies for urban infrastructure, education, and enterprise applications. China's "Digital China" strategy prioritises next-generation visual interfaces for smart cities, while India's draft AVGC-XR (Animation, Visual Effects, Gaming, and Extended Reality) policies explicitly allocate fiscal incentives for immersive technology development.

The Government of India has committed reimbursement of up to 35% of qualified production expenditure, capped at INR two crore for AR/VR and holographic projects, directly supporting screenless display ecosystem development. Singapore's "Smart Nation" initiative and Japan's "Society 5.0" framework establish regulatory clarity and infrastructure support for immersive technologies.

The global screenless display market is capitalizing on these policy commitments, which reduce commercialisation barriers and create predictable demand for enterprise implementations. Smart city infrastructure investments across the Asia Pacific are projected to exceed around US$ 2.16 trillion by 2030, with urban Visualization, transportation management, and public services increasingly incorporating screenless display solutions.

Government backing ensures sustained investment in 5G connectivity, edge computing infrastructure, and technical standards-critical enablers for complex screenless display applications requiring ultra-low latency and high bandwidth.

Restraint - High Development and Implementation Costs

Despite component cost reductions, comprehensive screenless display systems require substantial capital investment, creating barriers to adoption among small and mid-sized enterprises. Integrated solutions combining optics, processing hardware, software architecture, and integration services typically range from US$50,000 to US$500,000+, depending on application complexity.

For healthcare facilities, manufacturing operations, and educational institutions with constrained budgets, these costs may exceed justifiable return-on-investment timeframes. Supply chain constraints in waveguide-grade optical materials persist, with specialised polymers and crystalline substrates experiencing production limitations that sustain elevated component pricing through 2026.

The complexity of system calibration and maintenance further increases total cost of ownership, particularly in resource-constrained markets outside North America and Western Europe.

Key Market Opportunities

Healthcare Innovation Through Precision Visualization and Surgical Planning

The intersection of screenless display technology and advanced healthcare delivery creates substantial commercial opportunities within the global screenless display market. Holographic visualization platforms enable surgeons to manipulate patient-specific 3D anatomical models during preoperative planning, significantly enhancing procedure precision and reducing complication rates.

RealView Imaging's deployment of HOLOSCOPE-i systems at major UAE hospitals during 2024-25 demonstrates clinical validation for interactive holographic visualization. Medical training institutions are actively adopting AI-powered augmented reality simulations for anatomy, surgical procedures, and diagnostic training, with pedagogical research confirming superior knowledge retention and procedural competency compared to traditional methods.

The addressable market within global healthcare extends beyond surgical applications to diagnostic imaging, telemedicine, medical device design, and clinical education. As healthcare institutions increasingly prioritize precision medicine and outcome optimisation, screenless display solutions offering real-time 3D visualization represent differentiated value.

Implementation opportunities encompass hospital operating rooms, diagnostic imaging centres, medical schools, and pharmaceutical development facilities. The Global Screenless Display Market benefits from healthcare's historical willingness to invest in advanced technologies when clinical outcomes justify expenditure, creating a foundation for sustained adoption acceleration.

Automotive and Transportation Sector Transformation

The automotive industry represents one of the most commercially advanced adoption channels for global screenless display market technologies, particularly through full-windshield holographic displays and advanced driver-assistance integration.

Hyundai Mobis introduced the world's first full-windshield holographic display at CES 2025, fundamentally reimagining in-vehicle information presentation without traditional screen components. This breakthrough validates technical feasibility for mass-market automotive applications requiring durability, reliability, and integration with existing vehicle architectures.

Heads-up display technology, historically limited to premium vehicles, is transitioning toward broader market segments as costs decline and functional sophistication increases-current systems now integrate real-time traffic data, collision warnings, and navigation cues directly into driver's field-of-view.

Regulatory pressure for enhanced driver safety, autonomous vehicle development requirements, and consumer preferences for premium user experiences create sustained demand drivers for screenless automotive implementations. The defence and aerospace sectors similarly demand advanced Visualization solutions for pilot training, mission planning, and the display of real-time tactical information.

The global screenless display market offers opportunities in commercial vehicles, public transportation, and logistics platforms, where operational efficiency gains from advanced Visualization justify the implementation costs.

Strategic partnerships between automotive OEMs, technology companies, and screenless display manufacturers indicate intensifying competitive focus on this application segment, positioning automotive as a primary commercial engine for market expansion through 2033.

Category-wise Analysis

Product Type Insights

Visual image screenless display technology, encompassing holographic projections, laser-scanned imagery, and light-field displays, commands the market with a dominant 61.3% market share in 2026. This leadership position reflects both technical maturity and broad applicability across commercial applications.

Holographic display technology has achieved practical implementation in retail advertising, medical imaging, and entertainment applications, establishing proven value propositions that drive continued investment. The visual image segment benefits from lower technical complexity compared to retinal direct and synaptic interface alternatives, reducing implementation barriers and accelerating adoption timelines.

Retinal display technology represents the fastest-growing segment within the Global Screenless Display Market segmentation, with research indicating growth rates exceeding the overall market CAGR of 26.7%. This segment encompasses virtual retinal display (VRD) systems and direct retinal projection technologies that beam images directly onto the user's retina, eliminating external display components.

End-user Insights

The Consumer Electronics segment maintains market leadership with 33.1% of overall market share in 2026, driven by increasing adoption of AR-enabled wearables, smart glasses, and immersive gaming platforms. This segment encompasses personal devices, including head-mounted displays, smartphone-integrated AR experiences, and wearable visual systems.

The proliferation of consumer-grade AR applications in social media platforms, gaming environments, and retail experiences has created substantial installed bases of users familiar with screenless display paradigms.

The Automotive & Transportation segment emerges as the fastest-growing end-use application for Global Screenless Display Market technologies, driven by regulatory mandates for advanced driver-assistance systems (ADAS), consumer preferences for premium in-vehicle experiences, and autonomous vehicle development requirements.

Full-windshield holographic displays eliminate traditional physical dashboards while maintaining superior information accessibility and driver safety. Heads-up display technology, historically exclusive to luxury vehicles, is transitioning across automotive market segments as costs decline and functional capabilities expand.

Commercial vehicle operators increasingly recognise operational efficiency gains from real-time holographic Visualization of cargo management, maintenance diagnostics, and navigation data. The aerospace and defence sectors similarly demonstrate accelerating adoption, with military aircraft, helicopters, and ground vehicles implementing advanced HUD systems for tactical information integration and situational awareness enhancement.

Regional Insights and Trends

North America Screenless Display Market Trends

North America commands 30.2% of the global screenless display market value, establishing the region as the primary commercial epicentre for technology development, enterprise adoption, and consumer market growth.

The United States represents the geographic nexus, hosting the majority of leading market participants, including Microsoft, Google, Apple, NVIDIA, and Intel, alongside specialized screenless display innovators, including Magic Leap, Avegant, and RealView Imaging. This geographic concentration of technology talent, venture capital infrastructure, and customer sophistication creates reinforcing dynamics favouring the dominance of North America.

The U.S. Army's IVAS contracts represent substantial volume commitments that provide capital certainty for component suppliers and system integrators, enabling manufacturing scale economies that reduce costs, benefiting civilian applications.

Healthcare institutions throughout North America are aggressively adopting AR-enabled surgical Visualization platforms and immersive medical training systems, creating enterprise deployment momentum that validates commercial viability for enterprise markets.

Regulatory clarity from the FDA and related bodies provides business certainty for healthcare and medical device applications, reducing implementation hesitation compared to less-developed regulatory jurisdictions.

East Asia Screenless Display Market Trends

East Asia represents 20.3% of the global screenless display market share, positioning the region as a critical growth engine for the forecast period expansion through 2033. China emerges as the dominant regional player, leveraging government digital transformation strategies that explicitly prioritise next-generation visual technologies for smart cities, manufacturing, and education.

The "Digital China" initiative allocates substantial capital to 5G infrastructure, AI integration, and immersive technology development-creating enabling conditions for screenless display commercialisation.

Manufacturing capabilities in China provide cost advantages in component production, with specialised optical materials and holographic display systems increasingly produced domestically. Consumer electronics demand remains robust across East Asia, with high technology adoption rates in Japan, South Korea, and China creating sizable markets for AR wearables and immersive applications.

Europe Screenless Display Market Trends

Europe maintains 24.5% of the global screenless display market share, characterised by substantial enterprise adoption, strong healthcare implementation, and regulatory-driven demand for advanced Visualization technologies. Western European technology companies, including Siemens, BMW, Mercedes-Benz, and Audi, are integrating advanced HUD and holographic display systems into automotive and industrial applications.

German automotive OEMs have established clear competitive positioning through proprietary AR/HUD development programs, with strategic partnerships between technology leaders (including the ZEISS and tesa partnership announced in May 2025 for holographically functionalized films targeting automotive windshields), reinforcing technological leadership.

Competitive Landscape

The Global Screenless Display market is consolidated, dominated by a few leading telecom equipment providers that hold significant market share and technological expertise. Key players such as Huawei Technologies Co., Ltd., Nokia, Ericsson, Samsung, and ZTE Corporation lead the market with extensive portfolios spanning network infrastructure, software solutions, and advanced 5G deployment capabilities.

The market is characterized by high entry barriers due to substantial capital requirements, regulatory complexities, and the need for continuous innovation in radio access networks, core network solutions, and spectrum technologies. Intense competition exists among these incumbents, who differentiate themselves through advanced technology, large-scale deployments, and strategic partnerships with telecom operators globally.

Smaller players and regional vendors exist but have limited influence, making the market largely oligopolistic in nature, with innovation and scale being critical success factors. The ongoing rollout of 5G and LTE Advanced networks continues to reinforce the dominance of these major players while driving investment in next-generation network technologies.

Key Industry Developments:

- In October 2025, Magic Leap showcases its AR expertise with a new glasses prototype and an extended Google partnership. The collaboration focuses on integrating Magic Leap's waveguides and optics with Google's Raxium microLED light engine to develop AR glasses with improved visual quality, comfort, and manufacturability. The joint effort aims to create practical, all-day wearable AR glasses, with the prototype revealed at the Future Investment Initiative (FII) marking a significant step towards advancing AR technology for everyday use.

- In May 2022, Leia Inc., in partnership with Anatomage Inc., has launched a 3D medical education solution using Leia's Lume Pad tablet and Anatomage's VR software. The collaboration enables eyewear-free, immersive 3D learning experiences by projecting realistic, interactive 3D anatomical bodies on the Lume Pad's 3D Lightfield display. This solution is aimed at enhancing medical education by offering a portable and accessible platform for high school anatomy and life science programs.

Companies Covered in Screenless Display Market

- AVEGANT

- Realview Imaging Ltd.

- Microsoft

- Magic Leap, Inc.

- Synaptics Incorporated

- Holoxica Ltd.

- EON Reality

- Leia Inc.

- Sony Corporation

- Sightful

Frequently Asked Questions

The global screenless display market is projected to be valued at US$ 8.2 Bn in 2026.

The visual image segment is expected to account for approximately 61.3% of the global screenless display market by product type in 2026.

The screenless display market is expected to witness a CAGR of 26.7% from 2026 to 2033.

The growth of the Screenless Display Market is driven by technological miniaturisation, component cost reduction, integration of augmented reality and AI-powered Visualization, and government digital transformation initiatives supporting immersive technologies.

Key market opportunities in the screenless display market include healthcare innovations through precision visualization and surgical planning, and automotive sector transformation with full-windshield holographic displays and advanced driver-assistance systems.

The key players in the Screenless Display market include Avegant, RealView Imaging Ltd., Microsoft, Magic Leap, Inc., and Synaptics Incorporated.