- Semiconductor Materials & Components

- Satellite Bus Subsystems Market

Satellite Bus Subsystems Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Satellite Bus Subsystems Market by Satellite Type (Small Satellites, Medium Satellites, Large Satellites), Application (Earth Observation, Communication, Navigation, Scientific Research & Exploration, Military & Defense, Others), End-Use (Commercial, Government, Defense), and Regional Analysis for 2025 - 2032

Satellite Bus Subsystems Market Size and Trends Analysis

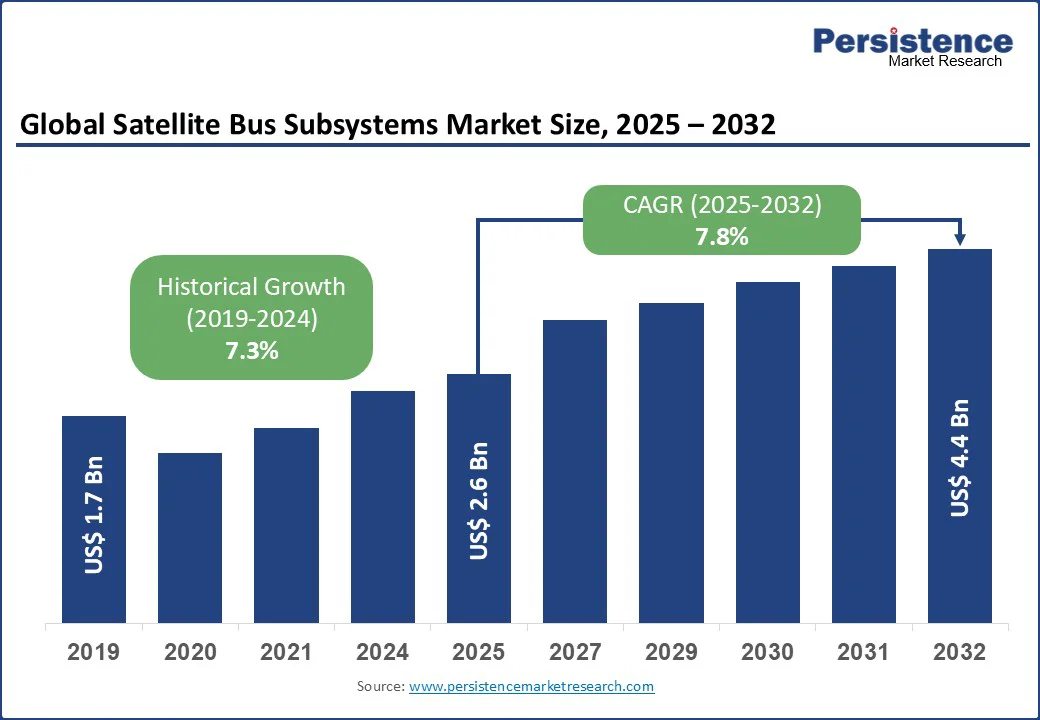

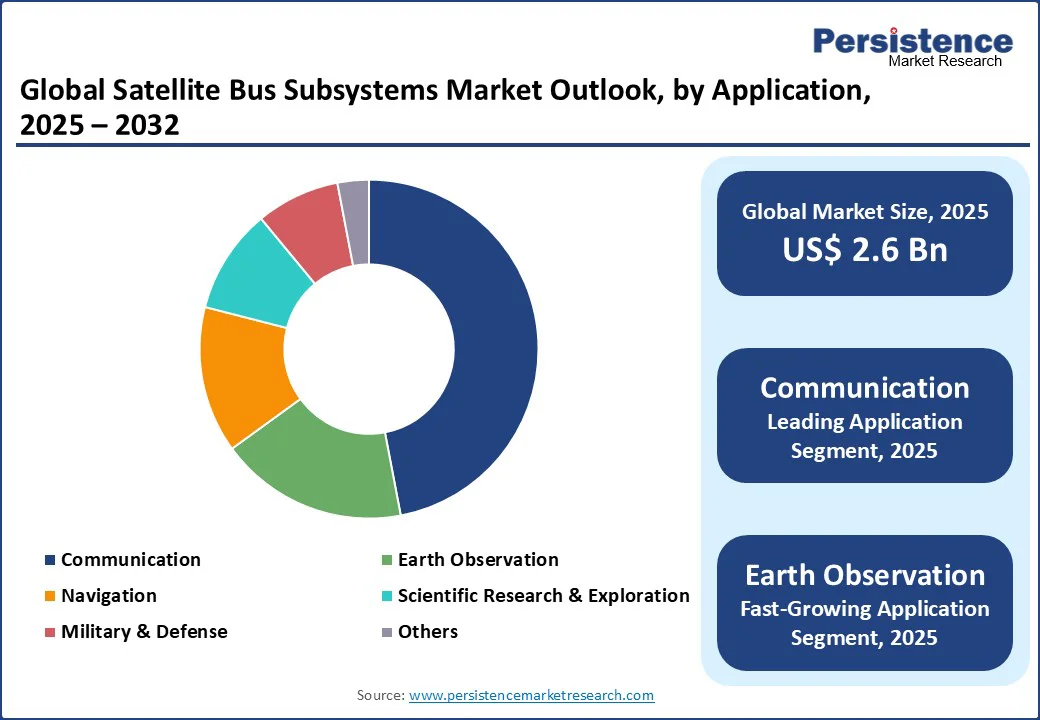

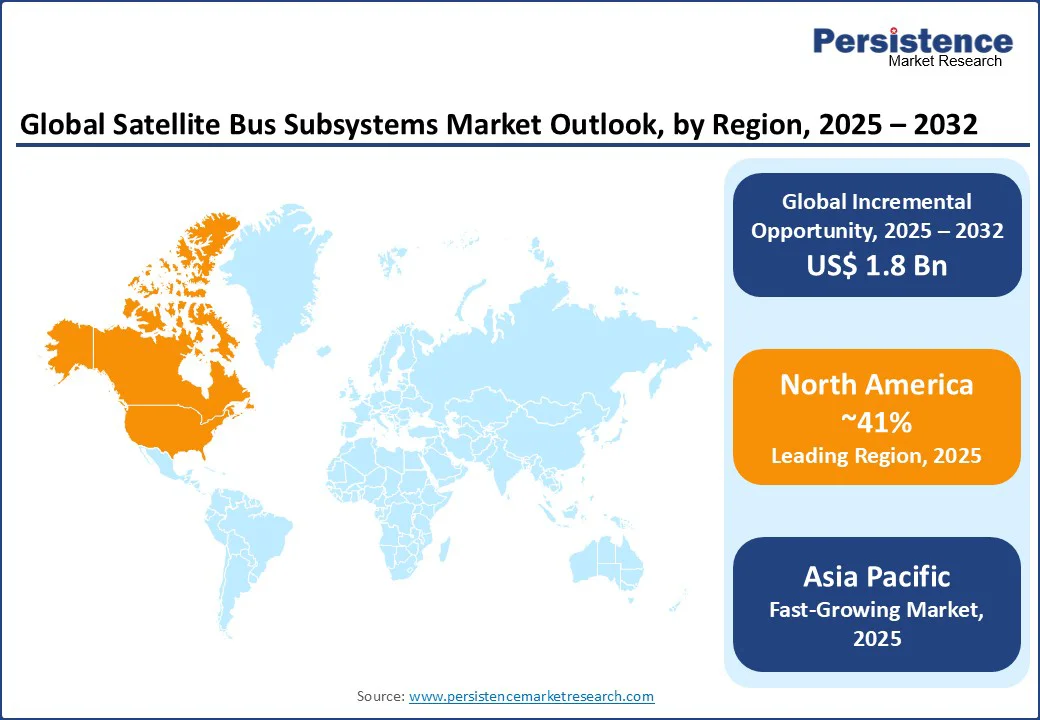

The global satellite bus subsystems market size is likely to be valued at US$ 2.6 Bn in 2025 and is expected to reach US$ 4.4 Bn by 2032, growing at a CAGR of 7.8% during the forecast period from 2025 to 2032.

The satellite bus subsystems market has experienced significant growth, driven by the increasing need for advanced space missions, rising adoption of small satellite constellations across industries, and advancements in modular and miniaturized technologies.

The demand for reliable subsystems in complex satellite operations, particularly in communication, earth observation, and defense sectors, has significantly boosted market expansion.

Key Industry Highlights:

- Leading Region: North America, holding a 41% market share in 2025, driven by the presence of major aerospace hubs in the U.S., high adoption of advanced satellite technologies, and strong demand for space exploration and defense applications.

- Fastest-growing Region: Asia Pacific is emerging as the fastest-growing market, fueled by rapid space program developments, increasing government investments in satellite infrastructure, and growing demand for earth observation and communication satellites in countries such as China and India.

- Dominant Satellite Type: Small Satellites, commanding nearly 60% market share, due to their cost-effectiveness, rapid deployment, and widespread adoption in constellations for various applications.

- Leading Application: Communication, accounting for over 47% of market revenue, driven by the need for efficient data transmission and global connectivity in expanding telecom networks.

|

Global Market Attribute |

Key Insights |

|

Satellite Bus Subsystems Market Size (2025E) |

US$ 2.6 Bn |

|

Market Value Forecast (2032F) |

US$ 4.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.3% |

Market Dynamics

Driver - Increasing deployment of small satellites

The growing deployment of small satellites in industries such as communication, earth observation, navigation, and defense has significantly driven the adoption of satellite bus subsystems. Over the past decade, the demand for compact, cost-effective, and easily deployable satellites has surged across both commercial and government sectors. Small satellites are widely used for applications such as Earth observation, communication, scientific research, navigation, and defense, making them a versatile solution for organizations seeking rapid access to space-based capabilities. Their relatively lower cost of development and shorter production cycles compared to large satellites have made them particularly attractive to universities, startups, and emerging space companies.

The rising trend of satellite constellations, especially for global broadband connectivity projects led by companies such as SpaceX (Starlink) and OneWeb, has further accelerated the deployment of small satellites. This growth creates significant demand for reliable and efficient bus subsystems, including power, thermal control, propulsion, and data handling. For instance, CubeSats and nanosatellites rely heavily on advanced miniaturized bus subsystems to achieve mission objectives despite their limited size. As the space industry shifts toward high-volume satellite launches, the demand for advanced small satellite bus subsystems is expected to remain a critical driver of market expansion.

Restraint - High Development and Regulatory Costs

The high costs associated with developing and regulating satellite bus subsystems hamper market growth. Designing and building satellite bus subsystems requires advanced engineering, specialized materials, and extensive testing to ensure performance, reliability, and safety in space. These processes involve significant financial investment, which often poses a challenge for small and medium enterprises (SMEs) and new entrants in the sector.

Additionally, compliance with stringent space regulations and international standards further adds to development costs. Regulatory bodies such as the U.S. Federal Communications Commission (FCC), European Space Agency (ESA), and International Telecommunication Union (ITU) impose strict licensing, frequency allocation, and safety requirements that demand time-consuming and costly approval processes.

Furthermore, delays in regulatory clearances or design modifications to meet compliance often led to extended project timelines and increased expenditures. The complexity of integrating subsystems with launch vehicles and payloads also raises overall costs. For instance, OneWeb faced cost escalations and delays in its satellite constellation deployment due to stringent regulatory and integration challenges, highlighting how compliance issues can increase financial strain. While large aerospace corporations can manage these financial demands, smaller players face significant barriers to entry, ultimately limiting innovation and slowing market expansion.

Opportunity - Advancements in modular and AI-integrated bus technologies

Advancements in modular and AI-integrated satellite bus technologies present a significant growth opportunity for the domain. Modular designs allow satellite manufacturers to build flexible and scalable bus subsystems that can be customized for diverse missions, ranging from earth observation and communication to scientific exploration and defense. This reduces both development time and overall costs, making satellites more accessible for commercial operators, research institutions, and emerging space startups.

Additionally, modularity supports easier upgrades and component replacements, extending satellite lifespans and improving return on investment. For instance, OneWeb has adopted modular bus architectures to accelerate the deployment of its satellite constellation for global broadband connectivity, reducing costs and ensuring faster scalability.

The integration of artificial intelligence (AI) into bus subsystems further enhances satellite performance by enabling autonomous operations, predictive maintenance, and efficient resource management. AI-driven systems can optimize power distribution, navigation, and thermal management in real time, reducing dependency on ground control and ensuring higher mission reliability.

For instance, ESA has been exploring AI-integrated bus technologies for small satellites to autonomously adapt mission parameters in orbit, thereby improving operational efficiency. As space exploration accelerates and demand for cost-effective, intelligent, and scalable satellite platforms increases, modular and AI-integrated bus technologies are expected to open new avenues for innovation and long-term market growth.

Category-wise Analysis

Satellite Type Insights

Small Satellites dominate, expected to account for approximately 60% of the share in 2025. Its dominance stems from its cost-effectiveness, rapid development cycles, and ease of integration with constellations for applications such as earth observation and communication. Small satellite bus subsystems, such as those offered by Ball Corporation and Sierra Nevada Corporation, enable real-time updates, constellation scalability, and seamless collaboration across missions, making them a preferred choice for industries such as commercial telecom and defense. Their modular designs also reduce upfront costs, driving adoption among startups and SMEs.

The large satellites segment is the fastest-growing, driven by industries with high-performance requirements, such as scientific research and military surveillance. Large satellite bus subsystems offer greater payload capacity and customization, appealing to large enterprises with complex missions. The growing focus on deep space exploration and high-resolution imaging, such as NASA’s initiatives, is accelerating the adoption of large bus systems in regions such as North America and Europe, with significant growth potential in high-stakes applications.

Application Insights

Communication leads the satellite bus subsystems market, holding a 47% share in 2025. The segment’s dominance is driven by the need for efficient data transmission and global connectivity in expanding telecom networks, particularly in geostationary and low-earth orbit constellations. Bus subsystems streamline the integration of communication payloads, reduce errors, and improve operational efficiency, making them critical for providers such as Airbus and Mitsubishi Electric.

The earth observation segment is the fastest-growing, fueled by the rapid growth of remote sensing and the need for real-time environmental monitoring. The rise in climate tracking platforms and the increasing demand for high-resolution imagery have spurred the adoption of bus subsystems in this sector. The Asia Pacific region, with its booming earth observation needs, is driving rapid adoption in this segment.

End-use Insights

Commercial holds the largest market share, accounting for approximately 49% of revenue in 2025. Commercial end-use allows vendors such as Lockheed Martin and Israel Aerospace Industries to maintain close relationships with customers, offer tailored subsystems, and provide dedicated support. This end-use is particularly dominant in applications with complex requirements, such as communication and earth observation, where customized bus solutions are critical.

The Defense end-use is the fastest-growing, driven by the increasing adoption of advanced satellite technologies and the rise of military constellations for surveillance and navigation. These platforms offer seamless access to bus subsystems, enabling faster development and integration with other space services. The growing popularity of defense-focused satellites among governments and militaries is accelerating the adoption of bus solutions through this end-use, particularly in North America and the Asia Pacific.

Regional Insights

North America Satellite Bus Subsystems Market Trends

North America is projected to account for nearly 41% of the global satellite bus subsystems market, reflecting its leadership in space innovation and technology adoption. The region’s dominance is primarily driven by the presence of major aerospace hubs in the United States, which host leading companies such as Lockheed Martin, Northrop Grumman, and Boeing. These firms play a pivotal role in developing advanced bus subsystems that support critical missions in communication, navigation, earth observation, and defense.

The region’s strong adoption of cutting-edge satellite technologies is further fueled by robust government investments, particularly through NASA, the U.S. Department of Defense, and the Space Force, which continue to prioritize space exploration, security, and intelligence gathering. Additionally, the rising demand for low Earth orbit (LEO) constellations, particularly for broadband connectivity, has accelerated the development of cost-effective and modular bus subsystems. With a combination of defense-driven demand, commercial space initiatives, and private investments in satellite startups, North America continues to set global standards in reliability, performance, and innovation, making it a frontrunner in shaping the future trajectory of the satellite bus subsystems market.

Europe Satellite Bus Subsystems Market Trends

Europe is emerging as a significant player in the satellite bus subsystems market, supported by strong institutional frameworks and collaborative space programs. The European Space Agency (ESA), along with national agencies such as the UK Space Agency, CNES (France), and DLR (Germany), is driving extensive investments in satellite missions for earth observation, navigation, scientific exploration, and defense. These initiatives are fueling demand for advanced and modular bus subsystems capable of supporting multi-mission requirements.

The region is also home to leading aerospace companies, including Airbus Defence and Space, Thales Alenia Space, and OHB SE, which are at the forefront of developing cutting-edge bus technologies. With a focus on modular architectures, electric propulsion, and AI-enabled operations, European manufacturers are increasingly catering to both commercial and government end-users. Europe’s growing emphasis on sovereign space capabilities and reducing reliance on external suppliers is encouraging greater R&D in subsystems that enhance autonomy and resilience. The rising demand for satellite-based communication, climate monitoring, and navigation services such as Galileo further strengthens Europe’s market position, ensuring steady growth in the coming years.

Asia Pacific Satellite Bus Subsystems Market Trends

Asia Pacific is positioned as the fastest-growing market for satellite bus subsystems, supported by rapid advancements in space programs and rising government investments in satellite infrastructure. Countries such as China, India, and Japan are leading the region’s expansion, with China accelerating its satellite constellation programs for communication, navigation, and earth observation, while India’s ISRO continues to launch cost-effective satellites with global recognition. Japan, through JAXA, is focusing on scientific research missions and next-generation space technologies.

The increasing need for high-resolution earth observation satellites to support agriculture, disaster management, urban planning, and climate monitoring is driving demand for compact, efficient, and modular bus subsystems. Similarly, the surge in communication satellites to expand broadband and telecom networks across underserved regions is boosting commercial adoption. Private players and emerging space startups are also contributing by leveraging small satellite bus technologies to deliver affordable solutions. With supportive government policies, advancements in AI-enabled bus subsystems, and expanding commercial applications, the Asia Pacific is expected to dominate future satellite deployment, creating substantial opportunities for subsystem vendors.

Competitive Landscape

The global satellite bus subsystems market is characterized by intense competition, regional strengths, and a mix of global and niche players. In developed regions such as North America and Europe, large firms such as Airbus S.A.S., Lockheed Martin Corporation, and Northrop Grumman Corporation dominate through scale, advanced R&D capabilities, and established partnerships with space agencies.

In the Asia Pacific, rapid space developments and increasing demand for small satellites are attracting significant investments from both international players, such as Ball Corporation and Mitsubishi Electric Corporation, and regional vendors. Companies are focusing on product innovation, modular designs, and strategic alliances to gain a competitive edge.

The development of AI-powered and miniaturized bus subsystems has emerged as a key differentiator, enabling faster adoption in communication, earth observation, and defense sectors. Strategic collaborations, acquisitions, and digital-first approaches for supply chain and marketing are further intensifying the competitive landscape. The industry exhibits a dual nature, consolidated at the top by global giants while remaining fragmented across numerous regional and niche players catering to local preferences and cost-sensitive segments.

Key Developments:

- In April 2024, Airbus won a contract from the UK Ministry of Defence to build a large satellite system. Earlier, in January 2024, the company also announced plans to develop a medium-sized satellite for earth observation.

- In February 2024, Ball Aerospace, previously a key bus subsystem player, was acquired by BAE Systems. This acquisition marks a transition and consolidation of its satellite subsystem capabilities under BAE's Space & Mission Systems division.

Companies Covered in Satellite Bus Subsystems Market

- Airbus S.A.S.

- Ball Corporation

- Israel Aerospace Industries (IAI)

- Martin Corporation

- Mitsubishi Electric Corporation

- Northrop Grumman Corporation

- Sierra Nevada Corporation

- Others

Frequently Asked Questions

The global Satellite Bus Subsystems Market is projected to reach US$ 2.6 Bn in 2025.

The increasing deployment of small satellites is a key driver.

The satellite bus subsystems market is poised to witness a CAGR of 7.8% from 2025 to 2032.

Advancements in modular and AI-integrated bus technologies are a key opportunity.

Airbus S.A.S., Ball Corporation, Israel Aerospace Industries (IAI), Lockheed Martin Corporation, and Northrop Grumman Corporation are key players.