- Rail

- Rolling Stock Dampers Market

Rolling Stock Dampers Market Size, Share, and Growth Forecast, 2026 – 2033

Rolling Stock Dampers Market by Product Type (Shock Dampers, Vibration Dampers, Hybrid Dampers), Application (Freight Trains, Passenger Trains, High-Speed Trains), and Regional Analysis for 2026 – 2033

Rolling Stock Dampers Market Size and Trends Analysis

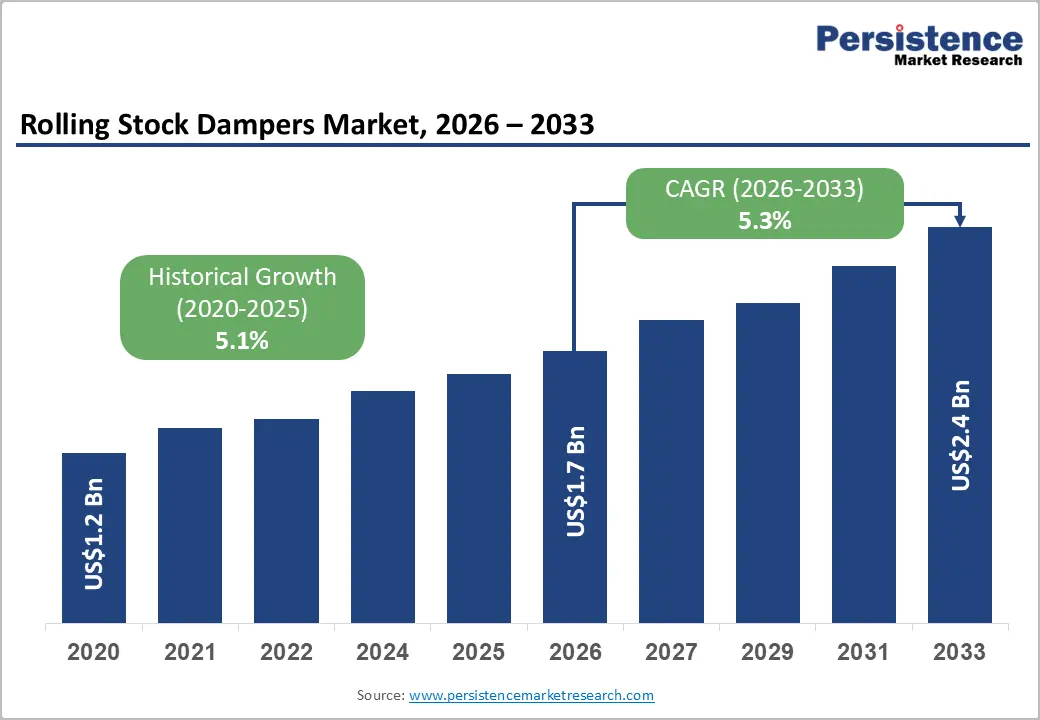

The global rolling stock dampers market size is likely to be valued at US$1.2 billion in 2026 and is expected to reach US$1.7 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033, driven by increasing investments in railway infrastructure, including high-speed rail corridors and urban transit networks, particularly across Asia Pacific and Europe. Rising focus on passenger comfort, ride stability, and vehicle safety is propelling the demand for advanced shock and vibration-damping solutions. Innovations in damper materials, such as elastomers and hybrid systems, alongside developments in smart and adaptive damping technologies, are enhancing operational efficiency and maintenance performance.

Key Industry Highlights:

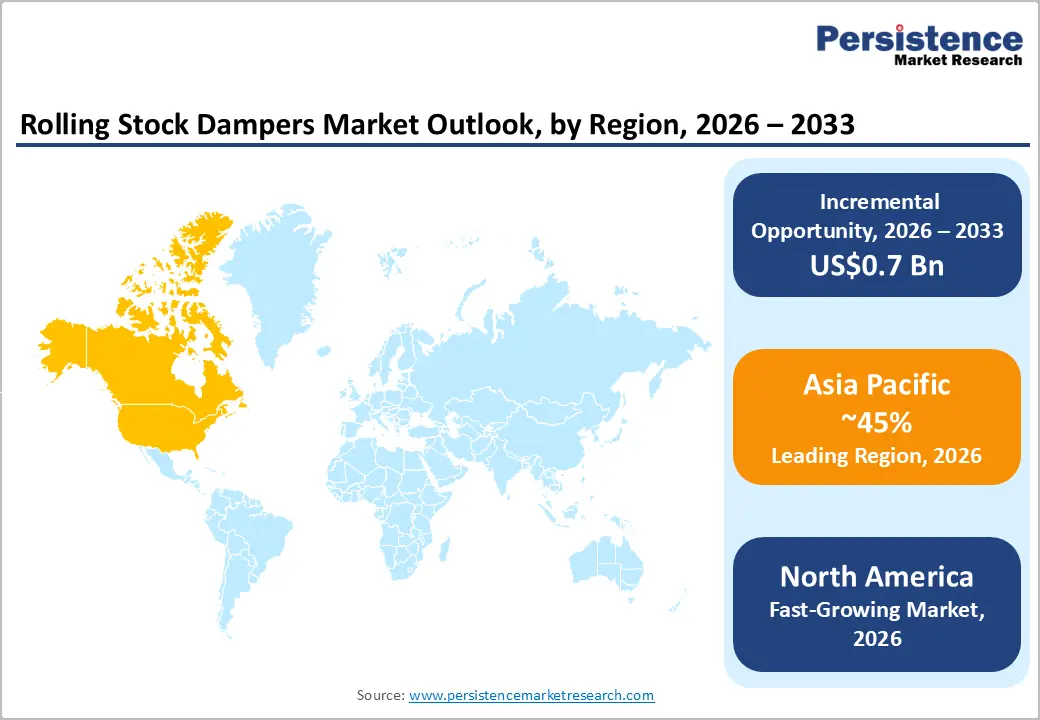

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 45% in 2026, driven by major infrastructure investments, urbanization, and strong demand from high-speed and urban rail projects.

- Fastest-growing Region: North America is likely to be the fastest-growing region in the rolling stock dampers in 2026, driven by regulatory compliance, modernization of freight and passenger rail, and investments in predictive maintenance and retrofit programs.

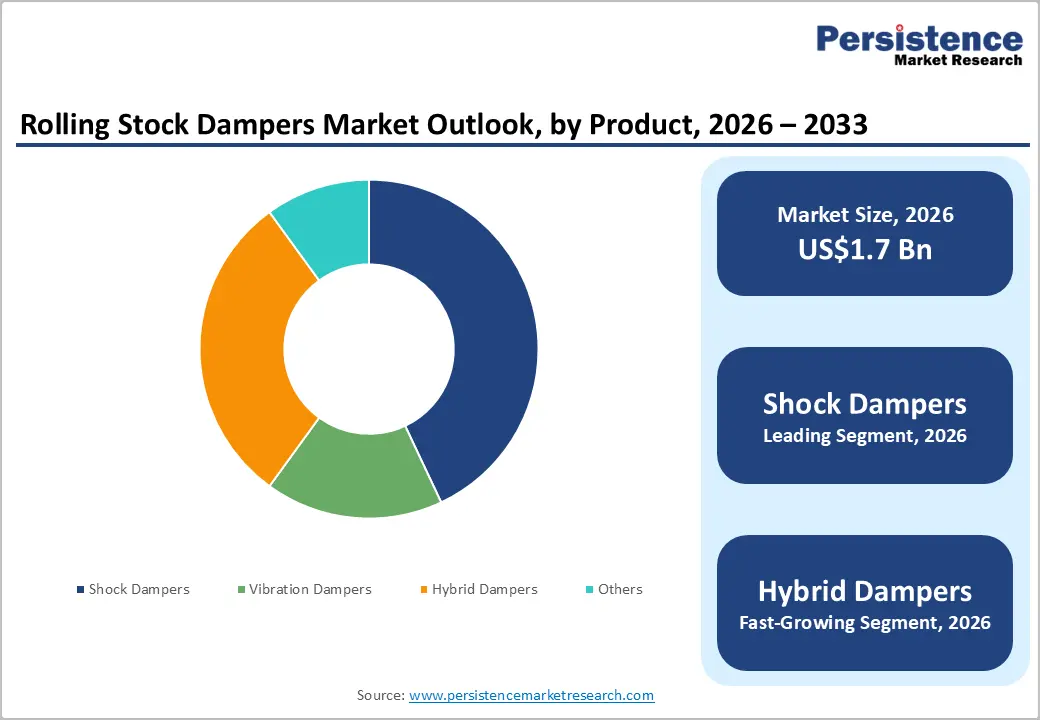

- Leading Product Type: Shock dampers are projected to represent the leading product type in 2026, accounting for 60% of the revenue share, due to their reliability in freight and passenger applications.

- Leading Application: Passenger trains are anticipated to be the leading application type, accounting for over 45% of the revenue share in 2026, supported by urban and intercity network demand for comfort.

| Key Insights | Details |

|---|---|

| Key Insights | Details |

| Rolling Stock Dampers Market Size (2026E) | US$1.7 Bn |

| Market Value Forecast (2033F) | US$2.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expansion of High-Speed and Urban Rail Networks

Governments worldwide, particularly in Asia Pacific and Europe, are investing heavily in high-speed corridors, metro systems, and light rail projects to meet growing urbanization and mobility demands. High-speed trains, with speeds exceeding 250 km/h, require advanced damping systems to ensure stability, reduce vibrations, and enhance passenger comfort. Similarly, urban transit networks operate under frequent stops, tight curves, and high passenger density, creating continuous stress on rolling stock suspension systems. Rail operators increasingly prioritize reliable damping solutions to meet strict performance and regulatory standards. The focus on reducing noise levels and track wear reinforces the need for high-quality dampers across modern rail networks.

The urban transit networks operate under frequent stops, tight curves, and high passenger density, creating continuous stress on rolling stock suspension systems. The growing deployment of new trains in these networks directly increases demand for shock, vibration, and hybrid dampers to maintain safety, performance, and ride quality. these infrastructure expansions encourage technological innovation in dampers. Hybrid and smart damping systems are increasingly integrated into modern rolling stock to provide adaptive control and predictive maintenance capabilities. The integration of sensors and predictive maintenance features helps operators reduce downtime and lifecycle costs. Rising retrofit and refurbishment programs for aging urban rail fleets increase the demand for advanced damping solutions.

Supply Chain Vulnerabilities and Raw Material Fluctuations

Dampers, including shock, vibration, and hybrid types, require specialized materials such as high-grade steel, elastomers, hydraulic fluids, and electromagnetic components. Any disruption in the supply chain, whether due to geopolitical tensions, transportation delays, or manufacturing bottlenecks, can delay the delivery of these critical components, affecting both new rolling stock production and aftermarket replacements. This may lead to extended lead times, increased operational costs, and potential project delays. Supply chain disruptions can slow the rollout of high-speed and urban rail projects, limiting the adoption of advanced damping technologies.

Raw material price volatility significantly affects the cost structure of damper manufacturing. Sudden increases in steel, elastomer, or hydraulic fluid prices can raise production expenses, while shortages of essential components can constrain output. To mitigate these risks, manufacturers are adopting strategies such as multi-sourcing, regionalized production, and inventory optimization. Fluctuations in material costs can influence the pricing of rolling stock dampers in both OEM and aftermarket segments, impacting procurement decisions by rail operators. Continuous innovation in material efficiency and design is also helping companies maintain performance standards while controlling costs in a competitive market.

Adoption of Semi-Active and Smart Dampers

Semi-active and smart dampers, unlike traditional passive systems, can adapt in real time to changes in load, speed, and track conditions, optimizing ride comfort, stability, and safety. These advanced dampers are increasingly integrated into high-speed trains, urban transit vehicles, and modern passenger coaches, where vibration control and lateral stability are critical for passenger experience. By using technologies such as electromagnetic actuators, magnetorheological fluids, and sensor-driven control systems, manufacturers can provide adaptive damping solutions that reduce wear on components, lower maintenance costs, and extend the life of rolling stock.

Rail operators are prioritizing upgrades that enhance comfort, safety, and energy efficiency, creating strong demand for smart damping solutions. The integration of predictive maintenance and IoT-enabled monitoring in these systems allows operators to improve fleet management and operational efficiency. The adoption of semi-active and smart dampers helps reduce wear and tear on critical components, lowering long-term maintenance costs. These systems are especially beneficial for high-speed and urban transit networks, where precise vibration control is essential for passenger experience. Manufacturers are increasingly focusing on developing lightweight and energy-efficient damper designs to meet evolving regulatory standards.

Category-wise Analysis

Product Type Insights

The shock dampers segment is expected to lead the rolling stock dampers market, accounting for approximately 60% of total revenue in 2026, driven by proven reliability, durability, and effectiveness in managing vertical and lateral forces across primary and secondary suspension systems. These dampers are widely used in both freight and passenger trains, where consistent energy absorption is required under heavy loads and varying track conditions. Shock dampers play a critical role in reducing structural fatigue, enhancing ride stability, and extending the lifespan of rolling stock components. For example, their extensive deployment in conventional passenger coaches and freight wagons operated by national railways, where cost-efficiency and robustness are key requirements.

Hybrid dampers are likely to represent the fastest-growing segment in 2026, driven by rising adoption in high-speed and next-generation passenger trains. These dampers combine hydraulic systems with electromagnetic or sensor-based technologies to deliver adaptive and semi-active damping performance. Hybrid dampers adapt in real-time to changes in speed, track irregularities, and load conditions, greatly enhancing ride comfort and lateral stability. They are increasingly being incorporated into high-speed rail networks in China and Europe, where advanced yaw and lateral dampers help maintain stability at elevated speeds.

Application Insights

Passenger trains are projected to lead the market, capturing around 45% of the total revenue share in 2026, driven by the large volume of urban metro systems, suburban rail, and intercity passenger services that prioritize ride comfort, noise reduction, and passenger safety. Dampers used in passenger trains must manage frequent acceleration, braking cycles, and variable passenger loads, making effective vibration and shock control essential. For example, the widespread deployment of advanced dampers in metro and regional rail systems across Europe and Asia, where comfort standards are strictly regulated. Continuous investments in fleet expansion, refurbishment, and comfort upgrades further reinforce demand.

High-speed trains are likely to be the fastest-growing application in 2026, driven by investments in high-speed rail infrastructure. These trains operate at very high velocities, requiring advanced damping systems to control yaw motion, lateral vibrations, and track-induced oscillations. For example, China’s extensive high-speed rail network, where sophisticated dampers are critical for maintaining stability and safety at speeds exceeding 300 km/h. European high-speed projects also rely heavily on advanced damping technologies to meet stringent safety and performance standards. As more countries invest in high-speed rail to reduce travel time and carbon emissions, demand for high-performance dampers continues to rise.

Regional Insights

North America Rolling Stock Dampers Market Trends

North America is likely to be the fastest-growing region in the rolling stock dampers in 2026, driven by a strong focus on safety, reliability, and operational efficiency across freight and passenger networks. The U.S., as the largest regional market, continues to prioritize upgrades that enhance vibration control and ride quality, particularly for freight operators seeking to improve load handling and reduce track wear. Regulatory emphasis on crashworthiness and vibration limits from authorities such as the Federal Railroad Administration encourages the adoption of advanced damping solutions. Technological integration, such as predictive maintenance systems and condition-based monitoring, enables rail operators to optimize fleet performance and reduce lifecycle costs.

Regional trends highlight a growing demand for adaptive and semi-active damping systems that complement broader digitalization initiatives in the rail sector. Established companies, such as ITT KONI, renowned for high-performance suspension and damping solutions, are strengthening their presence through strategic partnerships and aftermarket services to address rising expectations for improved stability and comfort. Investments in upgrading passenger rail networks, including intercity and regional lines, are also generating retrofit opportunities that support sustained market growth.

Europe Rolling Stock Dampers Market Trends

Europe is expected to be a key market for rolling stock dampers in 2026, as rail operators modernize legacy fleets to comply with stringent comfort and vibration standards set by regulatory bodies such as the European Union Agency for Railways (ERA). Robust investments in high-speed rail corridors, regional passenger services, and urban transit infrastructure are driving demand for advanced shock, vibration, and hybrid dampers. A focus on energy efficiency and emission reduction is promoting the use of lightweight, low-maintenance damping solutions that enhance ride quality while lowering lifecycle costs.

Europe is characterized by the consolidation of advanced technology suppliers and strategic partnerships with rolling stock manufacturers. Leading companies, such as Knorr-Bremse AG, a major provider of rail vehicle systems and dampers, are expanding their offerings to include smart and semi-active damping solutions with adaptive control and real-time responsiveness. Retrofit opportunities remain substantial as aging fleets in countries, including Germany, France, and the U.K., undergo suspension upgrades. Alongside ongoing high-speed rail projects in Spain and Italy, these factors are driving the adoption of innovative technologies and supporting strong growth in Europe’s rolling stock dampers market.

Asia Pacific Rolling Stock Dampers Market Trends

Asia Pacific is anticipated to be the leading region, accounting for a market share of 45% in 2026, driven by massive investments in rail infrastructure expansion and modernization. Countries such as China, India, Japan, and those in the ASEAN region are actively extending high-speed rail networks, metro systems, and intercity rail corridors to support rapid urbanization and increased passenger mobility. This surge in rail projects is driving a strong demand for shock, vibration, and hybrid dampers that enhance ride comfort, stability, and operational safety across diverse service conditions. Government initiatives focused on sustainable and energy-efficient transportation are encouraging the adoption of advanced damper technologies that reduce vibration-related wear and improve overall system resilience.

The region emphasizes technological innovation and localized manufacturing capabilities. Manufacturers are investing in research and development to introduce smart and semi-active damping systems featuring IoT-enabled monitoring, predictive maintenance, and adaptive control, specifically designed for high-speed and metro applications. For instance, CRRC Corporation Ltd., a leading rolling stock producer, is collaborating with component partners to integrate next-generation damper solutions into its high-speed and urban train fleets. Combined with cost-competitive production and robust supply chain networks, these factors enhance regional competitiveness. Supportive government policies and large-scale rail infrastructure investments further accelerate the adoption of advanced damping technologies.

Competitive Landscape

The global rolling stock dampers market is moderately fragmented, shaped by a mix of established multinational corporations and regional specialists. No single company dominates the market, but leading players leverage extensive R&D capabilities, strong OEM relationships, and broad manufacturing footprints to maintain competitive positions. These firms invest heavily in innovations such as adaptive damping technologies and IoT-enabled monitoring solutions to meet evolving regulatory requirements and customer demands for enhanced ride comfort, safety, and maintenance efficiency.

Key market leaders include ITT KONI, ZF Friedrichshafen AG, Knorr-Bremse AG, KYB Corporation, Dellner Dampers, and CRRC Corporation. Competition is driven by continuous innovation, strategic partnerships, geographic expansion, and strengthened service networks aimed at securing OEM contracts and aftermarket business. Strategic alliances for co-developing next-generation damping systems are increasingly common, emphasizing the critical role of technological advancement and integration capabilities in maintaining market leadership.

Key Industry Developments:

- In December 2025, ZF Group undertook a strategic initiative to strengthen its presence in India’s rapidly modernizing rail sector by launching advanced railway dampers through ZF India Pvt Ltd. at the International Railway Equipment Exhibition (IREE) 2025. Targeted for metro, semi-high-speed, high-speed, and locomotive applications, these dampers feature a maintenance-free twin-tube design with high dynamic stiffness, ensuring reliable performance under extreme weather conditions while reducing downtime. The customizable damping characteristics further enhance ride comfort, stability, and operational efficiency, reinforcing ZF’s commitment to delivering technologically advanced solutions for the Indian rail market.

- In March 2025, Siemens AG and Knorr-Bremse AG launched a strategic partnership to co-develop advanced noise-reduction dampers for high-speed rail applications. By combining Siemens’ expertise in systems integration with Knorr-Bremse’s leadership in damping technology, the collaboration aims to establish new performance standards for next-generation high-speed rail platforms. This initiative enhanced ride comfort and acoustic efficiency while creating standardized damper specifications, reinforcing long-term relationships with major OEMs across the global high-speed rail market.

Companies Covered in Rolling Stock Dampers Market

- ZF Friedrichshafen AG

- Knorr‑Bremse AG

- SV Shocks

- Koni

- Unipart Rail

- Trelleborg Applied Technologies

- Xi’an Zhong Rui Railway New Technology

- Dellner Dampers AB

- Addtech AB

- Tenneco Inc.

- Sigra Rolling Stock Components

- Seemonthon Industry