- Specialty & Fine Chemicals

- Rolling Lubricants Market

Rolling Lubricants Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Rolling Lubricants Market by Source (Synthetic, Semi-synthetic, Mineral Oil-based, Other), Rolling Process (Cold Rolling, Hot Rolling), Metal Type (Steel, Aluminum, Copper, Other), Industry (Automotive, Construction, Industrial Machinery, Other), and Regional Analysis for 2025 - 2032

Rolling Lubricants Market Size and Trend Analysis

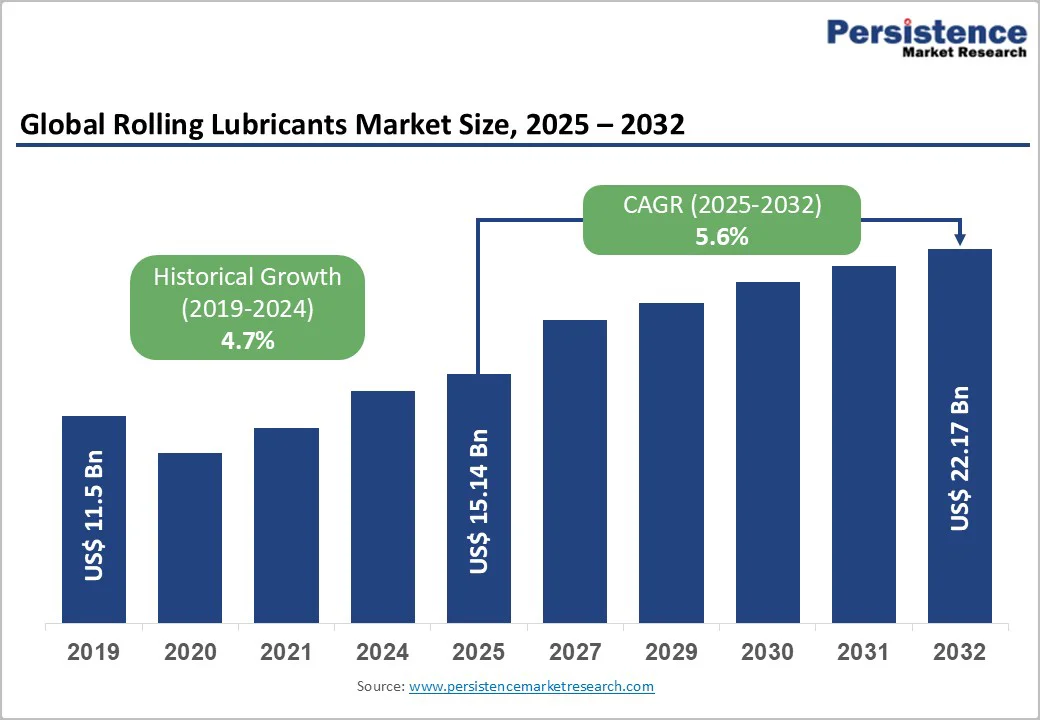

The global rolling lubricants market size is supposed to be valued at US$15.1 Bn in 2025 and is projected to reach US$22.17 Bn by 2032, growing at a CAGR of 5.6% between 2025 and 2032.

The primary drivers include surging demand for high-precision metal processing in automotive and construction sectors, where rolled steel and aluminum usage has risen significantly, necessitating advanced lubricants for friction reduction and surface quality enhancement.

According to the World Steel Association, global crude steel production reached 1,882.6 million tonnes in 2024, with significant growth observed in key markets like China (76.0 Mt in December 2024, up 11.8%) and India (13.6 Mt, up 9.5%), directly fueling the consumption of rolling oils and lubricants across hot and cold rolling operations.

Key Market Highlights

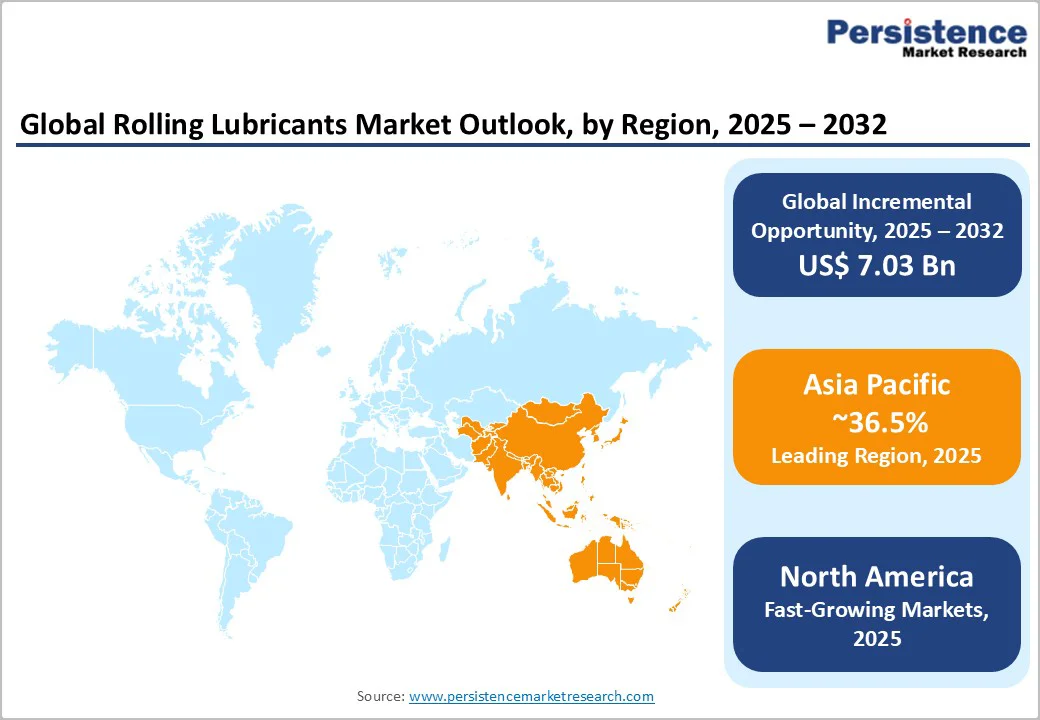

- Regional Leader: Asia Pacific leads the rolling lubricants market with 36.5% of the market share, propelled by China's steel production and India's industrialization, boosting lubricant demand in emerging economies.

- Fastest Growing Region: North America emerges as the fastest growing region for the Rolling Lubricants Market due to advanced U.S. manufacturing and regulatory support for sustainable innovations in automotive metal processing.

- Leading Segment: Synthetic rolling lubricants lead with 42% market share, driven by superior thermal stability, enhanced oxidation resistance, regulatory compliance advantages, and compatibility with high-speed precision rolling operations

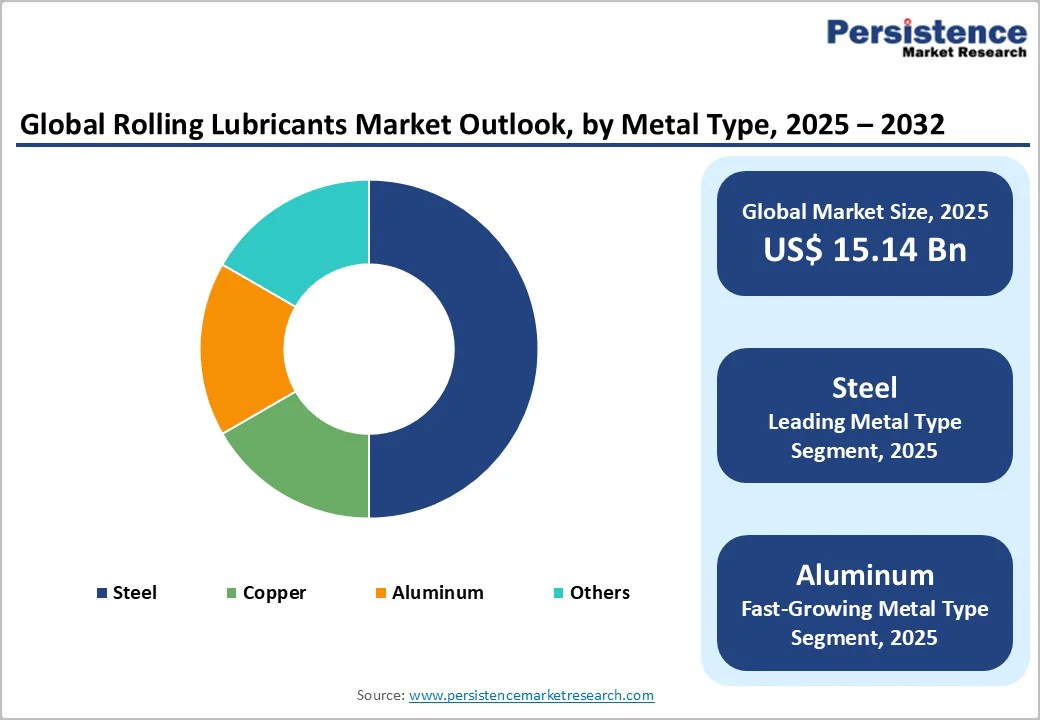

- Fastest Growing Segment: The Aluminum metal type segment demonstrates the highest growth rate, propelled by automotive lightweighting initiatives increasing aluminum usage to 208 kg per vehicle.

- Growth Opportunities: Adoption of bio-based lubricants presents a key opportunity, aligning with global sustainability policies to capture premium demand in eco-regulated markets.

| Key Insights | Details |

|---|---|

| Rolling Lubricants Market Size (2025E) | US$15.1 Bn |

| Market Value Forecast (2032F) | US$22.17 Bn |

| Projected Growth CAGR (2025 - 2032) | 5.6% |

| Historical Market Growth (2019 - 2024) | 4.7% |

Market Dynamics

Drivers - Surging Automotive Production and Lightweight Vehicle Manufacturing Initiatives

The escalating global automotive production, coupled with stringent fuel efficiency regulations, is propelling demand for rolling lubricants used in processing lightweight metals. The U.S. Environmental Protection Agency (EPA) implemented updated Corporate Average Fuel Economy (CAFE) standards requiring vehicles to achieve significantly improved fuel efficiency, with penalties of $14 per 0.1 mpg shortfall multiplied by total production volume.

This regulatory pressure has accelerated the adoption of aluminum and advanced high-strength steel in vehicle manufacturing, with aluminum usage in North American vehicles increasing from 154 kg to 208 kg per vehicle, representing consistent growth in aluminum-intensive applications like body panels, chassis components, and engine parts.

Steel's integral role in infrastructure projects worldwide has led to a 40% surge in lubricant adoption within these sectors, as cold rolling processes demand oils that ensure smoother metal deformation and reduced energy consumption.

The Rolling Mill Market expansion directly supports this trend, as modern rolling mills require high-performance lubricants capable of maintaining consistent plasto-hydrodynamic film formation under extreme rolling loads while ensuring superior surface finish quality for automotive applications.

Rapid Infrastructure Development and Industrialization in Emerging Economies

The unprecedented pace of infrastructure development and industrial expansion in emerging markets, particularly across the Asia Pacific, is driving substantial demand for rolled steel products and associated lubricants.

India reached its target steel production capacity of 205 million tons per year in the 2024/2025 fiscal year, with projects underway to expand capacity by another 167 million tons by 2030, representing one of the highest growth rates globally at 8% per year post-2020.

The Asia Pacific structural steel market is experiencing robust growth fueled by smart city initiatives, transportation infrastructure projects, and industrial facility construction, with China's Belt and Road Initiative alone generating massive demand for structural steel that requires efficient cold and hot rolling processes.

This infrastructure boom directly translates to heightened consumption of rolling lubricants that ensure optimal surface quality, reduced friction, and extended roll life in high-volume steel processing operations.

Market Restraints

Fluctuating Raw Material Prices

Volatility in crude oil prices poses a substantial restraint on the Rolling Lubricants Market, as most formulations rely on petroleum-derived bases, leading to inconsistent production costs. With crude oil prices fluctuating between $70-90 per barrel in 2024, manufacturers face margin pressures, potentially delaying investments in R&D for advanced lubricants.

Fluctuations in petroleum-based raw material costs pose a significant challenge to rolling lubricant market growth and profitability.

This volatility particularly impacts small and medium-sized lubricant producers with limited financial capacity to absorb cost increases, forcing them to either reduce profit margins or increase prices, thereby losing price-sensitive customers. This dependency exacerbates supply chain disruptions, impacting the availability of mineral-based oils that dominate traditional applications, and hindering market stability in price-sensitive regions.

Stringent Environmental Regulations

Increasingly rigorous environmental regulations, such as REACH in Europe, restrict the use of hazardous additives in rolling lubricants, compelling costly reformulations and compliance efforts. The European Union's REACH regulation continues to impose stricter controls on chemical substances, with the ECHA adding five new chemicals to the SVHC Candidate List in January 2025, bringing the total to 247 entries.

Substances like 6-[(C10-C13)-alkyl-(branched, unsaturated)-2,5-dioxopyrrolidin-1-yl]hexanoic acid, commonly used in metal working fluids and reaction mass of triphenylthiophosphate derivatives found in lubricant additives, are now classified under reproductive toxicity PBT categories, requiring immediate customer notification and compliance obligations.

These rules aim to reduce volatile organic compounds and waste, but they increase operational expenses by up to 15% for producers, slowing adoption in regulated markets. Consequently, the shift to eco-friendly alternatives remains gradual, limiting short-term growth in conventional segments.

Opportunity - Adoption of Sustainable and Bio-Based Lubricants

The growing emphasis on sustainability and circular economy principles creates significant market opportunities for manufacturers developing eco-friendly, bio-based rolling lubricants.

Several European countries now mandate the use of bio-based lubricants in environmentally sensitive applications, with companies like RSC Bio Solutions offering plant-based alternatives under their FUTERRA brand, while established players, including Castrol and FUCHS, are actively manufacturing and marketing eco-friendly lubricant portfolios.

The Asia Pacific Automotive Metal Stamping Market expansion provides additional opportunities, as metal stamping operations increasingly require environmentally compliant lubricants that offer full lifecycle oil management, closed-loop reuse capabilities, and enhanced energy efficiency while meeting stringent performance standards.

Rolling lubricant makers adopting green chemistry, advanced oil-water separation, and biodegradable formulations can gain market share as global sustainability rules tighten and customers favor eco-conscious suppliers.

Expansion in High-Growth Automotive Applications

The booming automotive industry offers significant opportunities through increased demand for lubricants in lightweight metal components, fueled by fuel efficiency mandates. Aluminum usage in vehicles is expected to rise by 70% by 2030, particularly in applications such as the Automotive Bumpers Market, where precise cold rolling ensures structural integrity.

The accelerating global transition toward electric vehicles presents substantial opportunities for rolling lubricant suppliers to develop specialized formulations for processing battery-grade metals and advanced alloys.

The shift toward battery metals, EV materials, and specialty alloys requires rolling lubricants with enhanced surface-finish optimization capabilities, particularly for thin-gauge aluminum rolling used in battery enclosures, heat management systems, and lightweight structural components.

BP Castrol expanded its EV-compatible aluminum rolling lubricants portfolio in 2025 with ultra-low volatility formulations specifically designed for precision rolling of automotive battery components, demonstrating the market potential in this emerging segment.

Category-wise Analysis

Nature Insights

Synthetic rolling lubricants command the leading position with an estimated market share of 42%, driven by their superior thermal stability, oxidation resistance, and wide temperature tolerance, making them ideal for high-speed tandem rolling and precision manufacturing.

Group IV polyalphaolefin-based formulations offer enhanced viscosity index and chemical stability compared to mineral oils, ensuring longer service life, minimal residue, and reduced roll wear under demanding conditions.

Industry leaders like ExxonMobil have introduced advanced solutions such as the Mobil Vactra CR line and chlorine-free oils for high-speed operations, reflecting strong investment in synthetic technologies. Growing regulatory pressure and end-userr preference for low-emission, high-performance lubricants further reinforce their leadership, especially as manufacturers adopt smart manufacturing and Industry 4.0-compatible formulations.

Rolling Process Insights

Cold rolling applications dominate with approximately 58% market share, reflecting the extensive use of cold-rolled products in automotive, construction, and consumer electronics industries requiring precision surface finishes.

Cold rolling lubricants play a crucial role in friction reduction, roll wear control, surface roughness improvement, and heat dissipation during metal deformation at ambient temperature, encompassing mineral oils, synthetic fluids, and emulsifiers engineered for specific metallurgical requirements.

Cold rolling requires specialized oils to lubricate at ambient temperatures, reducing friction and ensuring defect-free surfaces, as supported by the 67.1% aluminum processing reliance on these lubricants. Modern cold rolling mills operate at higher speeds and pressures, necessitating advanced lubricant formulations capable of maintaining performance under extreme conditions.

Metal Type Insights

The steel segment dominates the metal type category with roughly 50% market share in the Rolling Lubricants Market, owing to steel's ubiquity in construction and machinery, where robust lubrication handles high-temperature deformations. The rolling of various steel grades, including high-strength steel (AHSS) and ultra-high-strength steel (UHSS), requires specialized lubricants that reduce friction while preventing surface marking and mill buildup.

The World Steel Association reported global crude steel production of 1,882.6 million tonnes in 2024, with significant growth in key markets including Asia and Oceania, with 106.3 Mt in December 2024, and sustained production volumes in established markets like the European Union with 9.6 Mt.

Steel's supremacy as a base material for industrial rolling operations stems from its versatile applications spanning hot-rolled structural sections, cold-rolled sheets for automotive body panels, and precision-rolled strips for appliance manufacturing, each requiring specialized lubricant formulations optimized for specific rolling parameters and surface quality requirements.

Industry Insights

Within the Industry category, the automotive sector leads with approximately 40% market share, propelled by the extensive use of rolled sheets for body panels and components requiring superior surface quality. Automotive OEMs demand lubricants that support high-speed rolling for aluminum and steel, aligning with emission standards that boost lightweight materials by 70% by 2030.

Investment in EV production is creating new demand patterns for surface-finish-optimized rolling lubricants, with industrial hubs in Michigan, Ohio, and Pennsylvania driving consumption of semi-synthetic and synthetic ester-based products meeting both performance and environmental standards for automotive applications.

Regional Insights

North America Rolling Lubricants Market Trends

The North American market demonstrates mature market characteristics with a strong emphasis on high-performance synthetic lubricants and advanced application technologies. The region's automotive and aerospace sectors drive demand for high-performance cold rolling oils, with lightweight aluminum adoption rising to meet fuel efficiency mandates.

The U.S. market benefits from established regulatory frameworks ensuring lubricant quality and environmental compliance, with manufacturers investing in biodegradable rolling fluids and developing new-generation formulations designed for precision steel rolling applications.

Total Lubrifiants strengthened its North American presence through the strategic acquisition of Houghton International's aluminum hot rolling oil (AHRO), steel cold rolling oil (SCRO), and tinplate rolling oil (TPRO) activities, broadening its product portfolio to offer fully integrated solutions including specially formulated rolling oils, cleaners, and fluid management services.

Europe Rolling Lubricants Market Trends

Europe's Rolling Lubricants Market is characterized by harmonized regulations under REACH, emphasizing low-toxicity oils in countries like Germany, the U.K., France, and Spain. Germany, as the region's manufacturing powerhouse, maintained automotive production at 4,109,100 vehicles in 2024 with 3,173,500 units exported, sustaining demand for precision rolling lubricants supporting its advanced automotive and industrial machinery sectors.

Regulation (EU) 2024/2462 targeting PEHXA and related substances imposes concentration limits of 25 ppb in materials, driving industry transition toward alternative chemistries and sustainable formulations.

The Green Deal accelerates eco-friendly shifts, with France's steel mills adopting water-based alternatives to cut waste, boosting operational efficiency. Spain's growing infrastructure projects further integrate these lubricants, harmonizing supply chains across the EU for consistent quality standards.

Asia Pacific Rolling Lubricants Market Trends

The Asia Pacific region dominates the Rolling Lubricants Market, with 36.5% of the market share, led by manufacturing advantages in China, Japan, India, and ASEAN nations. China produced 76.0 Mt of crude steel in December 2024, up 11.8% year-over-year, while India achieved 13.6 Mt with 9.5% growth, collectively accounting for most global steel production increases and driving substantial rolling lubricant consumption.

India reached its target steel production capacity of 205 million tons per year in fiscal 2024/2025, with ambitious projects underway to expand capacity by 167 million tons by 2030, maintaining 8% annual growth rates that significantly outpace China's 2.76% and the global average of 1.77%.

Japan's precision engineering drives synthetic formulations for electronics metals, with ASEAN's infrastructure boom in Vietnam and Indonesia adding momentum through efficient cold rolling processes. These dynamics, supported by policy incentives for industrialization, position the region for sustained expansion via cost-effective, high-volume applications.

Competitive Landscape

The global rolling lubricants market exhibits a consolidated structure dominated by multinational players, with top firms holding over 60% share through extensive R&D and global distribution.

Companies pursue expansion via mergers and sustainable innovations, such as bio-based oils, to differentiate in eco-conscious segments. Key strategies include partnerships for customized formulations, while emerging models like performance-based contracts emphasize uptime guarantees and digital monitoring. This concentration fosters innovation but pressures smaller players to specialize in niche applications.

Key Market Developments

- January 2024: Quaker Houghton launched the QUAKERROL E-series synthetic emulsions for high-speed steel rolling, enhancing lubrication efficiency by 20% in automotive applications.

- March 2025: Quaker Houghton announced its agreement to acquire Dipsol Chemicals Co., Ltd., a prominent provider of surface treatment and plating solutions, for approximately 23 billion JPY (~$153 million), strengthening its advanced solutions portfolio and expanding capabilities in the Asia-Pacific automotive and industrial sectors.

- July 2024: TotalEnergies expanded its bio-based lubricant portfolio for cold rolling, targeting European markets to meet REACH requirements and reduce environmental impact.

Top Companies in the Rolling Lubricants Market

- ExxonMobil Corporation (headquartered in Irving, Texas, USA) leads with a diverse portfolio of synthetic and mineral lubricants, generating significant revenue from automotive and industrial segments through innovative additives that extend mill life. Its global influence stems from strong R&D investments, ensuring maturity in high-performance solutions.

- Quaker Houghton (headquartered in Conshohocken, Pennsylvania, USA) excels in metalworking chemistry via specialized emulsions for steel and aluminum rolling. The company's portfolio strength lies in sustainable formulations, bolstered by 2024 launches that boost efficiency.

- TotalEnergies (headquartered in Courbevoie, France) dominates in Europe with eco-friendly oils, leveraging influence in energy sectors for integrated supply chains. Its maturity is evident in bio-based innovations, driving revenue through regulatory-compliant products.

Companies Covered in Rolling Lubricants Market

- ExxonMobil Corporation

- Croda International PLC

- Total S.A.

- BP plc. (Castrol)

- Indian Oil Corporation Ltd

- Sinopec

- Quaker Houghton

- Fuchs Petrolub

- TotalEnergies

- Chevron

- Eastern Petroleum Pvt. Ltd.

- PetroChina Company Limited

- Sasol Limited

Frequently Asked Questions

The market is valued at US$15.1 Bn in 2025 and expected to reach US$22.17 Bn by 2032, reflecting a 5.6% CAGR driven by industrial growth.

Key drivers include rising steel and aluminum usage in automotive and construction, with aluminum demand surging 70% by 2030 for lightweighting, alongside formulation innovations for efficiency.

Cold rolling leads with a 60% share, essential for precision finishes in automotive metals, supported by high aluminum processing needs and energy-efficient oils.

Asia Pacific leads the rolling lubricants market with 36.5% of the market share, propelled by China's steel production and India's industrialization, boosting lubricant demand in emerging economies.

Bio-based lubricants offer growth via sustainability policies like the EU Green Deal, targeting emission reductions and capturing demand in eco-friendly aluminum rolling.

Leading players include ExxonMobil Corporation, Quaker Houghton, and TotalEnergies, dominating through R&D in synthetics and global supply chains for metalworking.