- Off-Road Equipment & Machinery

- Ride-On Aerator Market

Ride-On Aerator Market Size, Share, and Growth Forecast, 2026 – 2033

Ride-On Aerator Market by Product Type (Mechanical, Hydraulic), Power Source (Gasoline, Electric, Battery-Powered), Application (Residential, Commercial, Sports Grounds, Golf Courses), and Regional Analysis for 2026-2033

Ride-On Aerator Market Share and Trends Analysis

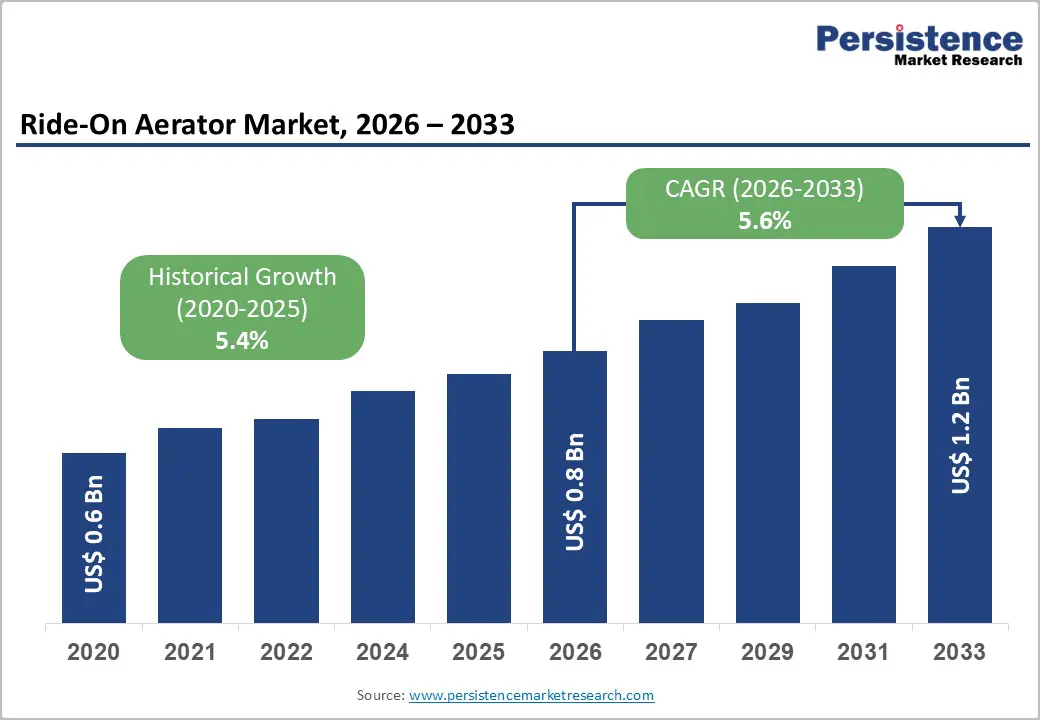

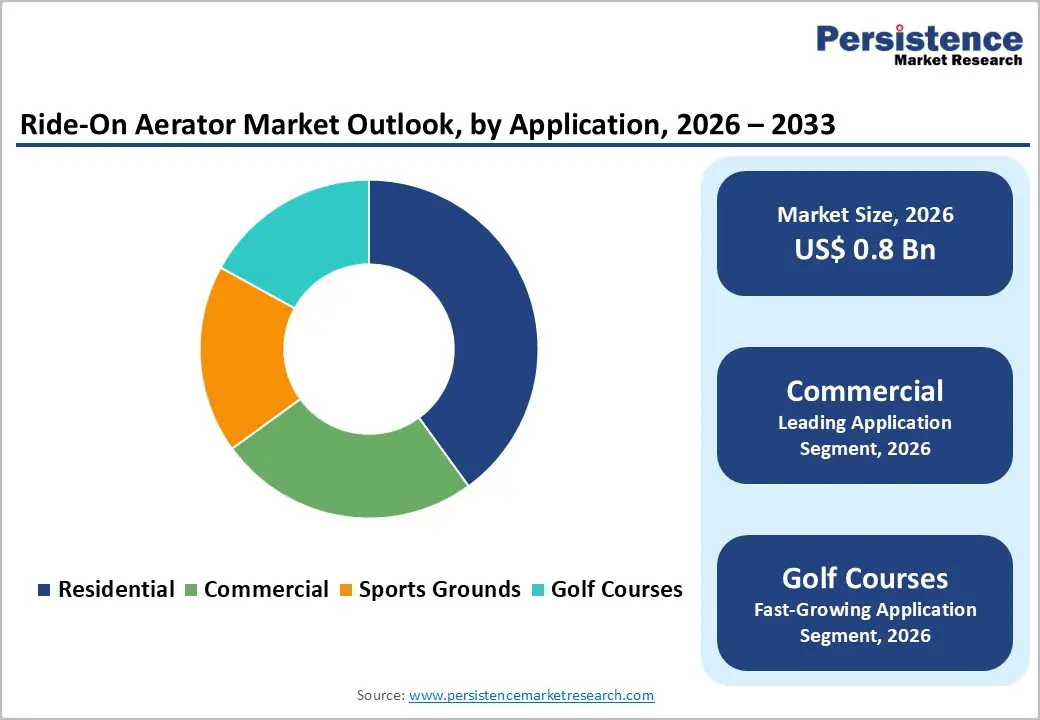

The global ride-on aerator market size is likely to be valued at US$ 0.8 billion in 2026, and is projected to reach US$ 1.2 billion by 2033, growing at a CAGR of 5.6% during the forecast period 2026−2033.

The market demonstrates sustained expansion potential, supported by increasing institutional focus on turf health management across sports infrastructure, commercial landscaping, and recreational land assets. Market progression reflects a shift from labor-intensive aeration practices toward mechanized, operator-efficient solutions that improve soil oxygenation consistency and operational productivity. Urbanization-driven green space development expands the addressable base for professional turf maintenance equipment, while rising awareness regarding long-term soil compaction management reinforces demand durability. Technological integration, including precision depth control and operator comfort systems, strengthens equipment adoption among professional service providers seeking predictable maintenance outcomes. Public and private investments in sports grounds, golf courses, and municipal landscaping infrastructure improve procurement visibility for ride-on aeration equipment.

Key Industry Highlights

- Leading Application: The commercial segment is slated to hold a revenue share of nearly 40% in 2026, driven by recurring turf quality standards and uniform soil treatment.

- Fastest-growing Application: Golf courses are forecasted to be the fastest-growing through 2033, supported by precision aeration, turf quality standards, and investment in advanced ride-on platforms.

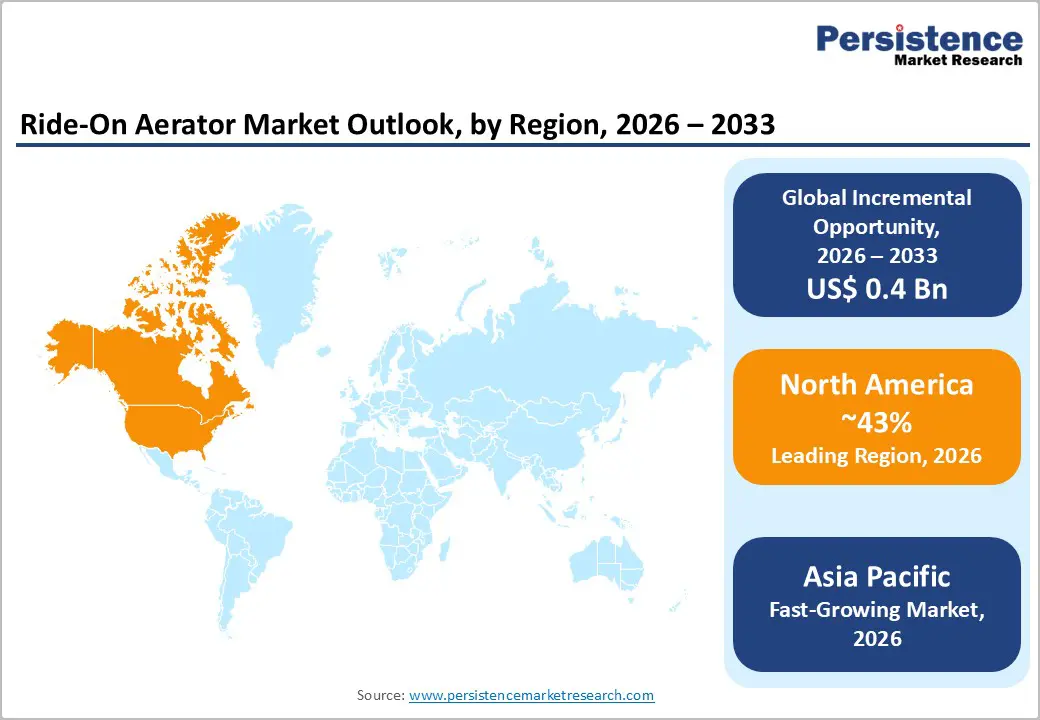

- Dominant Region: North America is projected to capture an estimated 43% share in 2026, owing to the widespread presence of professional turf infrastructure and high-demand sports facilities.

- Fastest-growing Market: Asia Pacific is forecasted to be the fastest-growing market through 2033, fueled by soaring investments in sports and recreational facilities.

| Key Insights | Details |

|---|---|

|

Ride-On Aerator Market Size (2026E) |

US$ 0.8 Bn |

|

Market Value Forecast (2033F) |

US$ 1.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expansion of Professional Turf Management Infrastructure

Investment in professional turf management infrastructure drives demand for ride-on aeration equipment due to the expanding government commitment to develop quality sports and recreational facilities. In the Government of India’s Union Budget 2025–26, the Khelo India sports program received an allocation of INR 1,000 crore, up from INR 800 crore in the previous year, reflecting a sharp policy focus on infrastructure creation and upgrade across the country’s athletic facilities. This increased funding supports construction and enhancement of playfields, tracks, stadia and multi-purpose grounds, all of which require consistent and technical turf care to maintain performance and safety standards.

Growing investment in facility infrastructure transforms turf management into an operational priority for organizers, administrators and facility owners. As professional green spaces proliferate, turf conditions increasingly influence user satisfaction, player safety and long-term cost efficiency of grounds upkeep. Mechanized aeration equipment delivers operational productivity by covering large surfaces quickly and reducing downtime between uses. Facilities with scheduled competitions and community use are under constant pressure to maintain high surface standards, creating recurring procurement and replacement cycles for specialized maintenance machines.

Technological Advancements Enhance Equipment Efficiency

The adoption of advanced technologies in turf maintenance equipment drives operational performance improvements and measurable efficiency gains. Government analyses of off-road vehicle and equipment sectors, which include commercial turf maintenance machinery, highlight that emissions and energy efficiency are central policy concerns. These assessments show that innovations targeting energy use and emissions offer pathways to lower operating costs and comply with evolving environmental regulations, reinforcing investment in smarter machine design. For example, U.S. Environmental Protection Agency (EPA) data indicate that commercial turf equipment accounts for a significant portion of off-road equipment usage, underscoring the importance of efficiency improvements in this category to support broader federal emissions reduction goals and operational cost savings across extensive use fleets.

Enhanced machine functionality directly influences performance outcomes in real-world use. Technological upgrades such as integrated sensors, GPS guidance, automated depth control, and telematics enable dynamic adjustment to soil conditions, ensuring aeration is executed precisely where and when required. These systems improve coverage uniformity, reduce unnecessary passes, and optimize fuel or power consumption per unit area maintained. In the context of professional turf management, these advances translate into significant labour and resource savings while enhancing turf quality metrics such as water infiltration and root development. Built-in diagnostic capabilities also support predictive maintenance, reducing downtime and extending equipment lifecycle.

High Initial Capital Outlay and Ownership Cost Sensitivity

Acquisition of professional-grade aeration machinery requires substantial upfront investment that can exceed the budget capacity of smaller operators and landscaping service providers. Capital allocation must be justified against expected utilization and revenue generation, with limited use reducing cost efficiency. Large investment thresholds create structural barriers for new entrants, restricting competition and slowing adoption in cost-sensitive segments. Enterprises with limited access to financing encounter additional challenges, as fixed costs reduce flexibility in capital planning and operational decision-making. The economics of entry are therefore dictated by both purchase price and the scale of deployment required to achieve returns.

Operational expenditures further increase sensitivity to ownership cost. Fuel consumption, maintenance, parts replacement, and labor for skilled operation generate ongoing financial commitments that accumulate over the machine lifecycle. Organizations often evaluate leasing, rental, or contract-based alternatives to avoid high recurring costs. Lifecycle cost assessment, emphasized in government agricultural equipment guidelines, shows that sustained financial outlay influences procurement decisions and limits willingness to invest, even when operational benefits are apparent. Effective cost management and total expenditure evaluation remain primary considerations for enterprises assessing machinery deployment.

Seasonal Demand Patterns Limit Utilization

Agronomic and climatic conditions determine optimal periods for turf aeration. Guidance from U.S. government sources indicates that core aeration should be performed during active grass growth phases, typically in early spring or early fall, when soil moisture and root activity allow for effective penetration and nutrient absorption. Performing aeration outside these windows reduces its effectiveness and can damage turf, limiting the operational timeframe for grounds maintenance activities.

This constrained window of agronomically justified work affects equipment utilization and operational planning. In regions with cold winters or heavy rainfall, soils are often unsuitable for aeration for extended periods, resulting in significant idle time for machinery. Seasonal peaks in demand create concentrated periods of activity, while off-peak months see equipment largely unused, reducing overall return on investment and complicating workforce management.

Electrification and Low-Emission Equipment Transition

Government policies and public health priorities are reshaping demand toward electrified, low emission turf equipment as a strategic opportunity. National and sub national regulators are restricting internal combustion engines in landscape machinery to reduce harmful emissions and improve air quality. Colorado’s Regulation 29 will limit gasoline powered lawn and garden equipment during high ozone seasons starting June 1, 2025, reflecting a broader compliance environment for turf maintenance fleets. Electric alternatives eliminate direct exhaust, substantially cutting pollutants at the point of use and aligning with federal and state emissions reduction goals.

From a business perspective, end users face evolving compliance requirements and incentive structures that favor low emission assets. Government tax credits and incentive programs for zero emission landscape machinery improve total cost of ownership for commercial fleets and support investment decisions. Electric machines deliver lower operational noise and reduced maintenance overhead, improving worker productivity in noise sensitive environments and expanding acceptable use cases for service providers. Public sector procurement of electric equipment creates reference demand that can drive scale efficiencies and technology advancement, shortening payback periods.

Service-based Equipment Deployment and Rental Models

The growing adoption of pay-per-use and rental approaches has transformed how turf maintenance machinery is accessed, offering significant operational flexibility for businesses and institutions. These models allow users to deploy equipment without the burden of high capital expenditure, making advanced machinery accessible to smaller landscaping firms and municipal operations. Organizations can scale equipment usage according to seasonal demand, optimizing cost efficiency while maintaining high-quality turf management standards. The ability to access well-maintained, technologically advanced machines on a temporary basis enhances productivity and reduces downtime associated with equipment ownership, repairs, and storage.

Such approaches also accelerate the integration of innovative features into routine operations. Service-based deployment ensures machines are maintained by providers, guaranteeing performance consistency and minimizing operational risks. Rental arrangements enable experimentation with different aeration techniques and equipment specifications, supporting data-driven decision-making for turf health and maintenance strategies. Operational agility achieved through these models aligns with sustainability goals by maximizing machine utilization and minimizing idle resources.

Category-wise Analysis

Product Type Insights

Mechanical is poised to lead with a forecasted 60% of the ride-on aerator market revenue share in 2026, owing to established reliability, lower system complexity, and widespread operator familiarity across professional turf maintenance environments. These machines deliver consistent core extraction and soil penetration without requiring complex hydraulic calibration, allowing operators to focus on operational efficiency rather than system adjustments. Predictable performance across different soil types and conditions reduces scheduling disruptions and ensures maintenance targets are consistently met. Simplified servicing procedures and readily available spare parts minimize downtime, while institutional buyers favor platforms that combine durability, ease of repair, and operational simplicity. Widespread aftermarket support further enhances confidence in long-term fleet management.

Hydraulic ride-on-aerators are anticipated to be the fastest-growing segment between 2026 and 2033, fueled by demand for precision control, adjustable aeration depth, and enhanced operator ergonomics. Advanced hydraulic systems allow operators to fine-tune machine performance in real time, ensuring uniform soil treatment across variable terrains. Automated depth control and adaptive response to surface conditions increase operational efficiency and reduce manual intervention. High-end golf courses, professional sports grounds, and premium landscaping services increasingly adopt these machines for superior turf quality. Enhanced comfort, reduced operator fatigue, and integration with digital monitoring systems further reinforce hydraulic solutions as a growth-oriented, technologically sophisticated option.

Application Insights

The commercial is slated to hold a dominant position, with an anticipated 40% of the ride-on aerator market share in 2026, driven by recurring turf quality requirements mandated by sports governing bodies and facility operators. Consistent aeration ensures that playing surfaces maintain optimal resilience, effective water drainage, and safety for athletes, reducing the risk of injuries during high-intensity use. Professional facility managers prioritize uniform soil treatment across large fields to meet regulatory and performance standards. Stable budget allocations within sports organizations enable planned equipment procurement and lifecycle management, allowing maintenance teams to deploy ride-on aerators effectively throughout peak and off-peak seasons.

Golf courses are projected to be the fastest-growing end users during the 2026-2033 forecast period, boosted by heightened focus on turf aesthetics, playability standards, and competitive differentiation. Golf course operators leverage precision aeration to preserve greens, fairways, and tee boxes under high foot traffic and seasonal stress. Ride-on aerators improve coverage efficiency, reducing labor intensity and minimizing disruption to playing surfaces. Investment in technologically advanced platforms aligns with premium course positioning and customer expectations, supporting consistent turf quality. Adoption is further driven by long-term maintenance planning, operational efficiency, and the pursuit of superior player experience.

Regional Insights

North America Ride-On Aerator Market Trends

North America is anticipated to capture an estimated 43% share of the ride-on aerator market in 2026, reflecting extensive professional turf management infrastructure and a high concentration of premium sports and recreational facilities. Strong presence of golf courses, stadiums, and athletic complexes drives continuous demand for large-capacity machines capable of delivering consistent soil penetration and core extraction across expansive surfaces. Operators benefit from well-established service networks and training programs, enabling efficient deployment, maintenance, and lifecycle management. Strategic capital planning within commercial operations encourages adoption of mechanically reliable and technologically advanced platforms that balance performance consistency with predictable operating costs.

High operational standards and intensive usage patterns on maintained turf create a need for machines that minimize downtime while sustaining surface quality. Facilities prioritize precision and repeatability to ensure compliance with performance and safety benchmarks, making ride-on aerators critical tools for operational efficiency. Integration of leasing and service-based deployment enhances utilization rates and reduces total cost of ownership, while advanced platforms support optimized aeration cycles, labor reduction, and improved water and nutrient management.

Europe Ride-On Aerator Market Trends

Europe is expected to maintain a strong position in the market for ride-on-aerators in 2026 and beyond, supported by well-established sports infrastructure, commercial landscaping practices, and stringent turf quality regulations. High concentration of golf courses, professional sports facilities, and municipal parks creates steady demand for reliable and precision-driven aeration equipment. Operators increasingly prioritize machines capable of uniform soil penetration and core extraction across varying turf types to ensure compliance with regulatory and performance standards. Emphasis on operational efficiency, including reduced labor requirements and predictable maintenance schedules, drives preference for mechanically robust and technologically integrated platforms.

Sustainability initiatives and environmental considerations play a significant role in shaping adoption trends. Operators favor low-emission, fuel-efficient platforms and systems that optimize water and nutrient management, aligning equipment use with environmental guidelines. Growth in premium sports facilities and commercial landscaping projects fuels interest in platforms with advanced features such as adjustable aeration depth, operator ergonomics, and terrain responsiveness. Leasing and service-based deployment models are increasingly utilized to reduce upfront investment and improve operational flexibility.

Asia Pacific Ride-On Aerator Market Trends

Asia Pacific is predicted to be the fastest-growing market for ride-on-aerators from 2026 to 2033, driven by rapid expansion of urban infrastructure and increasing investment in high-quality recreational and sports facilities. Rising development of golf courses, stadiums, and landscaped commercial properties creates significant demand for large-capacity aeration platforms capable of covering extensive turf areas efficiently. Emerging landscaping service providers are adopting technologically advanced ride-on solutions to differentiate offerings and meet growing client expectations for turf aesthetics and durability. Government initiatives to enhance public green spaces, combined with rising awareness of soil health and turf maintenance standards, further accelerate adoption.

Growing commercial interest in premium turf management, particularly in high-traffic sports grounds and hospitality properties, reinforces forecasted demand for advanced aeration equipment. Operators prioritize machines that combine precision, operator ergonomics, and adaptability to diverse soil types, allowing scalable deployment across newly developed and existing sites. Expanding access to financing options, rental arrangements, and service-based deployment models lowers barriers for mid-sized operators, supporting rapid uptake of ride-on platforms. The introduction of local manufacturing hubs and import partnerships reduces equipment lead times and enhances availability of spare parts and technical support.

Competitive Landscape

The global ride-on-aerator market features a moderately fragmented structure, with several global manufacturers and regional specialists contributing to competitive dynamics. Leading companies such as The Toro Company, Deere & Company, Husqvarna AB (publ), Briggs & Stratton, ANDREAS STIHL PVT LTD, and Kubota Australia maintain meaningful market shares through established brand recognition, extensive dealer networks, and robust after-sales service capabilities. Competitive advantage is derived from delivering high-performance, durable platforms that address diverse turf management requirements, ranging from commercial landscaping to sports and recreational facilities.

Entry into the market is moderated by high capital intensity and the need for established dealer and service networks, which create tangible barriers for new entrants. Aftermarket expectations, including maintenance support, spare part availability, and technical training, further reinforce market stability for established players. Strategic investments in technological enhancements, service-based deployment models, and regional customization allow leading manufacturers to differentiate offerings and sustain competitive positioning. Focus on lifecycle value, equipment uptime, and operator productivity ensures that market leaders retain influence while smaller regional operators capture niche demand segments.

Key Industry Developments

- In January 2026, Spruce published a review of the top 6 riding lawn mowers of 2026, highlighting gas and battery models that deliver performance, ease of use, and efficiency for a range of property sizes and terrain types.

- In January 2025, John Deere extended its strategic marketing agreement with Wiedenmann to let all John Deere dealerships in the U.K., Ireland and Europe offer Wiedenmann turf and golf maintenance equipment, including deep aerators such as the Terra Spike SL6 paired with GPS equipped tractors, enhancing technology sharing and dealer access for professional turf and golf course care.

Companies Covered in Ride-On Aerator Market

- The Toro Company.

- Deere & Company.

- Husqvarna AB (publ).

- Briggs & Stratton.

- ANDREAS STIHL PVT LTD

- Kubota Australia.

- Textron Specialized Vehicles.

- YANMAR HOLDINGS CO., LTD.

- Generac Power Systems, Inc.

Frequently Asked Questions

The global ride-on aerator market is projected to reach US$ 0.8 billion in 2026.

Increasing demand for efficient turf maintenance, precision soil aeration, and high-quality sports and recreational surfaces is driving the market.

The market is poised to witness a CAGR of 5.6% from 2026 to 2033.

Adoption of service-based deployment and rental models, integration of advanced aeration technologies, with premium turf segment expansion are major market opportunities.

Some of the key market players include The Toro Company, Deere & Company, Husqvarna AB (publ), Briggs & Stratton, ANDREAS STIHL PVT LTD, and Kubota Australia.