- Specialty & Fine Chemicals

- Resol Resins Market

Resol Resins Market Size, Share, and Growth Forecast, 2025 - 2032

Resol Resins Market by Component (Phenol, Formaldehyde), Application (Molding Compounds, Woodworking Adhesives, Laminations, Insulation, Paper Impregnation, Coatings), End-use (Automotive and Transportation, Building and Construction, Furniture, Consumer Electronics, Oil and Gas), and Regional Analysis for 2025 - 2032

Resol Resins Market Size and Trend Analysis

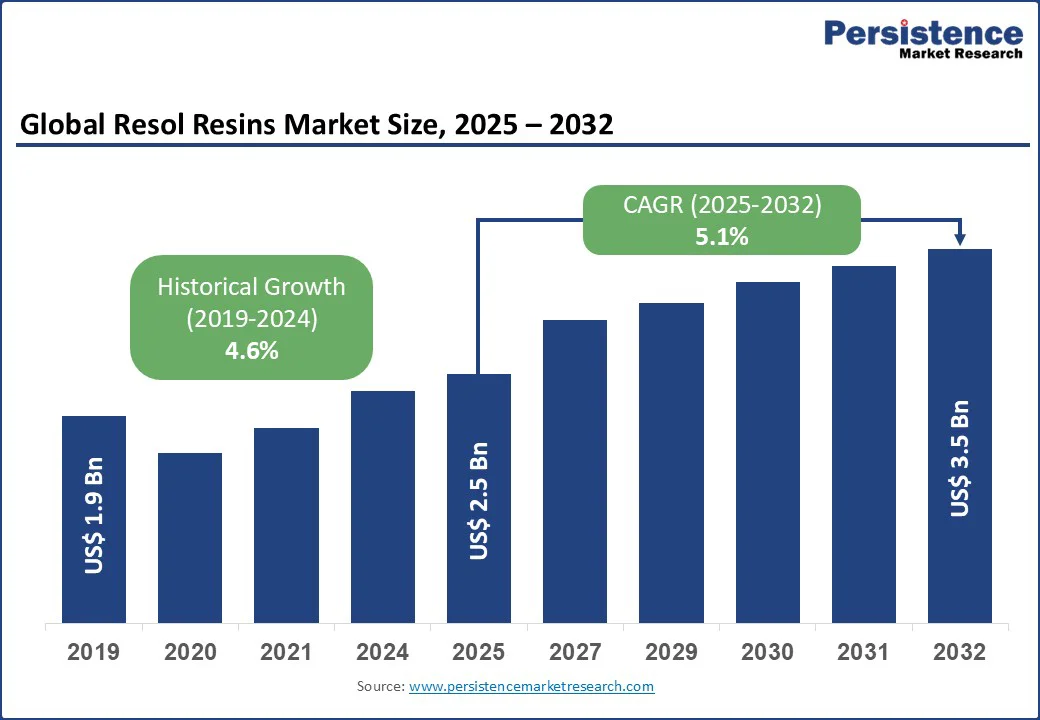

The global resol resins market size is likely to value at US$2.5 Bn in 2025 and reach US$3.5 Bn by 2032, growing at a CAGR of 5.1% during the forecast period from 2025 to 2032, driven by increasing demand from industries such as automotive, construction, and consumer electronics, where high thermal stability and chemical resistance are essential.

Key Industry Highlights:

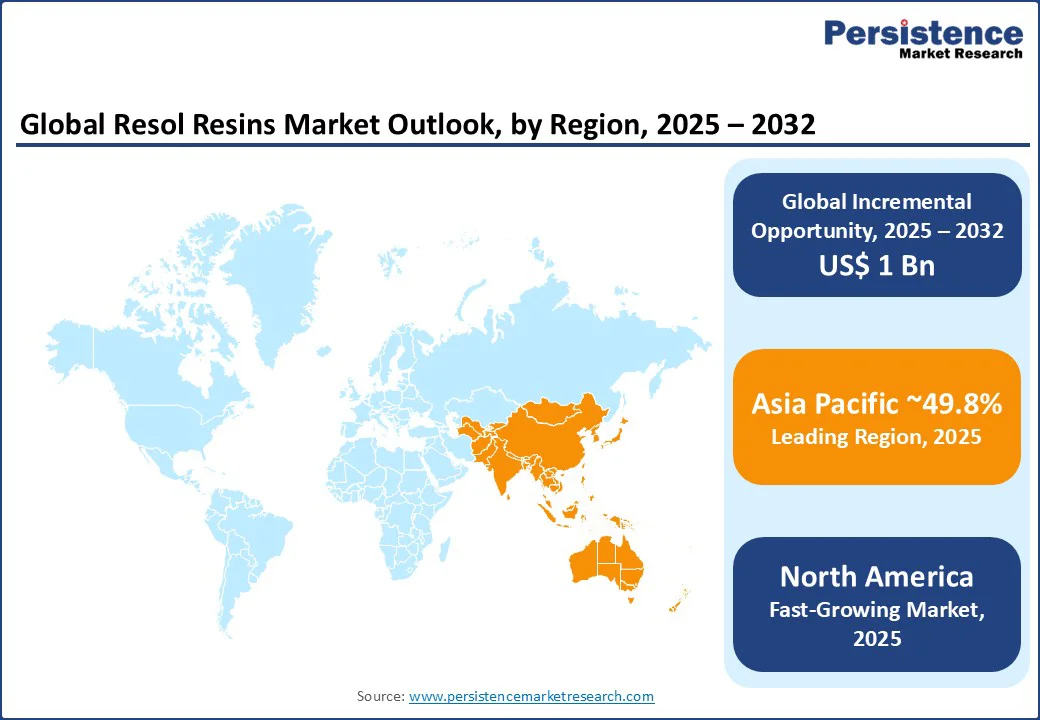

- Leading Region: Asia Pacific is likely to account for a 49.8% share in 2025, driven by rapid industrialization, construction activities, and high production capacities in countries such as China and India.

- Fastest-Growing Region: North America is the fastest-growing region, propelled by strong demand from the automotive and construction sectors in the U.S. and Canada, supported by advanced manufacturing infrastructure.

- Investment Plans: China’s 14th Five-Year Plan (2021-2025) emphasizes sustainable construction, with investments in green building materials, boosting demand for resol resins in adhesives and coatings.

- Dominant Component: Phenol accounts for nearly 62.5% of the resol resins market share, due to its cost-effectiveness and superior chemical properties for industrial applications.

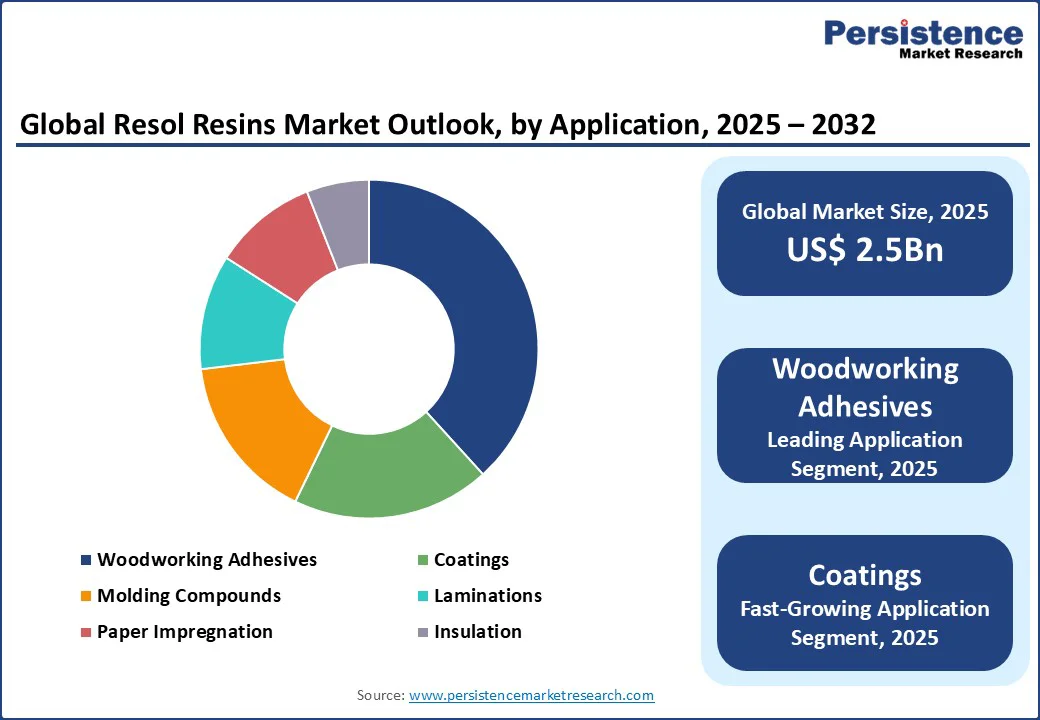

- Leading Application: Woodworking adhesives contribute over 38.4% of market revenue, driven by global demand for furniture and construction materials.

| Key Insights | Details |

|---|---|

| Resol Resins Market Size (2025E) | US$ 2.5Bn |

| Market Value Forecast (2032F) | US$ 3.5Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.6% |

Market Dynamics

Driver: Surge in Construction and Furniture Industries Fuels Market Growth

The global resol resins market is witnessing significant expansion due to the rising demand from the construction and furniture industries. Resol resins are vital in woodworking adhesives and laminations, providing strong bonding and durability for plywood, particleboard, and furniture manufacturing.

According to the report of Global Infrastructure Outlook, by GI Hub and Oxford Economics, the global infrastructure investment will reach US?$94?trillion by 2040, with significant contributions from emerging economies. In the Asia Pacific, China’s Belt and Road Initiative and India’s Smart Cities Mission drive demand for resol-based adhesives in infrastructure projects.

In North America, the U.S. construction sector, valued at $2.14 trillion in 2025 per the U.S. Census Bureau, relies on resol resins for structural applications. Companies such as BASF SE reported a 2024 sales increase in woodworking adhesives, reflecting robust demand. Government initiatives promoting sustainable construction and rising urbanization ensure sustained market growth through 2032.

Restraint: Volatility in Raw Material Prices and Environmental Regulations

The resol resins market faces challenges due to fluctuating raw material prices and stringent environmental regulations. Phenol and formaldehyde, key components, are subject to price volatility due to their dependence on petrochemical feedstocks. In 2023, phenol prices fluctuated, impacting production costs for manufacturers. This volatility creates pricing pressures, particularly for smaller players.

Additionally, environmental regulations, such as the EU’s REACH framework, impose restrictions on formaldehyde emissions due to health concerns, increasing compliance costs. Synthetic alternatives, such as bio-based resins, are gaining traction due to their eco-friendly profiles, posing competition.

Limited standardization in some regions and concerns over emissions in high-temperature applications further restrain adoption, particularly in cost-sensitive markets, hindering overall market growth.

Opportunity: Growing Demand in Automotive and Consumer Electronics Sectors

The increasing focus on the automotive and consumer electronics sectors presents significant growth opportunities. Resol resins are critical in molding compounds and coatings for automotive components, offering heat resistance and durability. The International Organization of Motor Vehicle Manufacturers (OICA) states that global vehicle production was 92.5 million units in 2024, driving demand for resol-based materials.

In consumer electronics, resol resins are used in laminations and insulation for circuit boards and devices. Companies such as Sumitomo Bakelite are innovating with high-performance resins for electronics, aligning with sustainability trends.

Government incentives, such as the EU’s Green Deal and U.S. clean energy policies, encourage investments in lightweight, durable materials, creating opportunities for manufacturers to develop advanced, eco-friendly resol resins to meet evolving industry needs through 2032.

Category-wise Insights

By Component

- Phenol holds the largest market share, approximately 62.5% in 2025, due to its cost-effectiveness and superior chemical properties. Widely used in woodworking adhesives and molding compounds, phenol-based resol resins are favored for their thermal stability and strong bonding capabilities. Companies such as BASF SE and Hexion Inc. lead with extensive portfolios, catering to demand in the construction and automotive sectors across the Asia Pacific and North America.

- Formaldehyde is the fastest-growing component, driven by its critical role in resin synthesis for laminations and coatings. Its adoption is rising in consumer electronics and furniture applications, with brands such as Mitsui Chemicals expanding offerings in Europe and the Asia Pacific, supported by growing demand for high-performance, durable resins in industrial settings.

By Application

- The woodworking adhesives segment accounts for over 38.4% of market revenue in 2025, driven by global demand for furniture and construction materials. Resol resins provide strong bonding for plywood and particleboard, with major players such as Georgia-Pacific Chemicals supplying high-performance adhesives for projects in the U.S. and China, where infrastructure investments fuel demand.

- The coatings segment is the fastest-growing, propelled by rising demand in automotive and consumer electronics. Resol-based coatings offer excellent heat and chemical resistance, with companies such as DIC Corporation innovating for high-performance applications. Growth in Asia Pacific and North America, driven by industrial manufacturing, supports this segment’s rapid expansion.

By End-use

- The building and construction sector dominates, contributing approximately 42.8% market revenue in 2025, driven by global infrastructure projects and urbanization. Resol resins are critical for adhesives and laminations in structural applications. Major players, such as Bakelite Synthetics, supply high-quality resins for projects in China and the U.S., where government investments in infrastructure fuel demand.

- The consumer electronics sector is the fastest-growing, driven by rising demand for laminations and insulation in circuit boards and devices. Resol resins offers durability and heat resistance, with companies such as Sumitomo Bakelite innovating for high-performance applications. Growth in Asia Pacific and Europe, supported by electronics manufacturing, drives this segment’s expansion.

Regional Insights

Asia Pacific Resol Resins Market Trends

Asia Pacific is likely to lead with 49.8% share in 2025. This dominance is driven by accelerated industrialization, robust construction activities, and substantial chemical production capacities in countries such as China and India.

China, home to major players such as the China National Chemical Corporation, plays a pivotal role in global resin output, benefiting from its mature manufacturing infrastructure. In India, infrastructure initiatives such as the Smart Cities Mission significantly increase demand for resol-based adhesives, coatings, and insulation materials.

Additionally, the region’s thriving furniture and consumer electronics sectors contribute to resin consumption, with companies such as Chang Chun Group and Mitsui Chemicals actively expanding their operations. Rising investment in government-led projects, particularly in housing, transportation, and urban development, further accelerates demand.

As the Asia Pacific continues to scale up its industrial output and urban development, the region is expected to maintain its market leadership through 2032.

North America Resol Resins Market Trends

North America stands out as the fastest-growing region, propelled by strong demand from the automotive and construction sectors in the U.S. and Canada. The region benefits from a well-established advanced manufacturing infrastructure, enabling high production capacities and innovation.

In January 2025, U.S. construction spending reached a seasonally adjusted annual rate of $2.19 trillion, with a significant portion relying on resol resins for adhesives, laminations, and coatings used in building and infrastructure projects.

Canada’s thriving electronics industry further fuels demand for high-performance resol resins, as highlighted by the Canadian Manufacturers & Exporters association. Leading companies such as Hexion Inc. and SI Group dominate the resol resins market, supported by expansive distribution networks that effectively serve automotive and infrastructure clients.

Additionally, growing consumer preference for sustainable and high-quality resin products reinforces North America’s competitive edge, ensuring continued market growth and innovation through 2030 and beyond.

Europe Resol Resins Market Trends

Europe ranks as the second fastest-growing region, propelled by stringent environmental regulations and expanding demand from the automotive and electronics sectors. Countries such as Germany and France lead infrastructure development, creating a robust base for resol resin consumption in adhesives, coatings, and laminations.

Germany’s automotive industry, a major user of resol-based molding compounds, benefits from established chemical giants such as BASF SE and Kolon Industries, which supply high-performance resins tailored to evolving industry needs.

The European Union’s ambitious Green Deal further accelerates market growth by promoting sustainable construction practices and the adoption of eco-friendly materials. This regulatory push increases demand for environmentally responsible resins used in both electronics manufacturing and building applications.

With continued investment in infrastructure modernization and a strong focus on sustainability, Europe is poised to sustain impressive growth through 2032, supporting innovation and greener product development across multiple end-use industries.

Competitive Landscape

The global resol resins market is highly competitive, characterized by a fragmented landscape with numerous domestic and international players. Leading companies, such as BASF SE, Hexion Inc., and Sumitomo Bakelite dominate through extensive product portfolios and global distribution networks.

Regional players such as Shandong Laiwu Runda, focus on localized offerings in the Asia Pacific. Companies are investing in sustainable resin formulations and advanced manufacturing technologies to enhance market share, driven by demand for high-performance resins in construction and electronics.

Key Industry Developments

- March 2025: Hexion Inc. launched a new eco-friendly resol resin for woodworking adhesives, designed for low formaldehyde emissions, targeting sustainable construction projects in Europe and North America. Hexion announced a collaboration with Bloom Biorenewables to develop a renewable, high-performance alternative to synthetic adhesives. Bloom's innovative process preserves the natural adhesive properties of lignin, a component found in wood, allowing for the creation of 100% plant-based adhesives.

- August 2021: SI Group announced plans to expand its resole resin production capacities at facilities in Rotterdam Junction, New York, and Lote, India, with a targeted increase of over 25%. The debottlenecking investments were slated for completion later in 2021, addressing the growing global demand for resole resins used in the automotive and adhesive sectors.

Companies Covered in Resol Resins Market

- BASF SE

- Chang Chun Group

- Georgia-Pacific Chemicals LLC

- Mitsui Chemicals Inc.

- Sumitomo Bakelite Co., Ltd.

- DIC Corporation

- Hexion Inc.

- Kolon Industries Inc.

- Shandong Laiwu Runda New Material Co., Ltd.

- SI Group, Inc.

- Bakelite Synthetics

- Others

Frequently Asked Questions

The resol resins market is projected to reach US$2.5 Bn in 2025.

Growing construction and furniture industries, and expanding applications in automotive and electronics, are key market drivers.

The resol resins market is poised to witness a CAGR of 5.1% from 2025 to 2032.

Rising demand in the automotive and consumer electronics sectors is the key market opportunity.

BASF SE, Hexion Inc., Sumitomo Bakelite, and Mitsui Chemicals are key market players.