- Hardware & Software IT Services

- Regulatory Information Management System Market

Regulatory Information Management System Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Regulatory Information Management System Market by Component (Software and Services), by Deployment Mode (Cloud-Based, On-Premises, and Hybrid), by Application (Registration Management, Regulatory Submission Management, Publishing & eCTD Management, Regulatory Intelligence & Change Management, Labeling Management, Document Management, Submission Planning & Tracking, and Others) End-user, and Regional Analysis from 2026 to 2033

Regulatory Information Management System Market Share and Trend Analysis

The global regulatory information management system market size is estimated to grow from US$ 534.8 billion in 2026 to US$ 878.5 billion by 2033. The market is projected to grow at a CAGR of 5.5% from 2026 to 2033. Global adoption of regulatory information management solutions is expanding steadily as life sciences organizations face increasing regulatory scrutiny, growing product pipelines, and rising submission complexity across international markets. Pharmaceutical, biotechnology, and medical device companies are prioritizing digital platforms that centralize regulatory data, streamline submission workflows, and ensure lifecycle compliance.

The transition from manual documentation toward automated, cloud-enabled environments is improving operational efficiency and reducing approval delays. Greater emphasis on electronic submissions, data traceability, and audit readiness is accelerating implementation across enterprises of all sizes. Additionally, expanding clinical development activities and globalization of product commercialization strategies are increasing the need for standardized regulatory coordination. Continuous technological advancements, including AI-enabled regulatory intelligence, analytics-driven decision support, and integrated collaboration tools, are enhancing productivity and compliance accuracy. Growing investment in digital transformation initiatives and modernization of regulatory operations continues to support widespread adoption across both mature and emerging healthcare markets.

Key Industry Highlights:

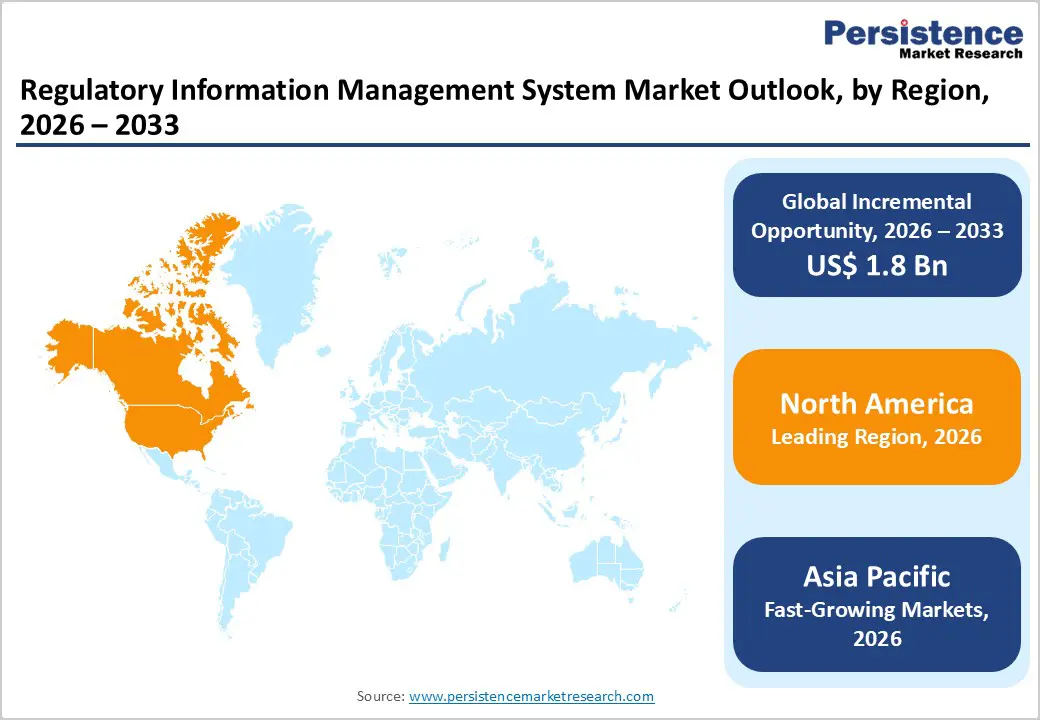

- Leading Region: North America accounts for the largest share at 46.7%, supported by the strong presence of global pharmaceutical companies, early adoption of digital compliance platforms, advanced IT infrastructure, and continuous investment in regulatory automation technologies.

- Fastest-Growing Region: Asia Pacific is witnessing the fastest expansion due to increasing pharmaceutical manufacturing, regulatory modernization initiatives, rising clinical trial activities, and growing adoption of cloud-based enterprise systems.

- Leading Component Segment: Software dominates the market owing to its ability to centralize regulatory data, automate submissions, and support end-to-end lifecycle management.

- Fastest-Growing Component Segment: Services are expanding rapidly as organizations increasingly require implementation support, validation, system integration, and regulatory consulting expertise.

- Leading Deployment Mode Segment: Cloud-based solutions remain the primary deployment model due to scalability, global accessibility, and faster regulatory collaboration.

- Fastest-Growing Deployment Mode Segment: On-premises deployment continues to grow as large enterprises prioritize data control, customization, and internal compliance governance requirements.

| Key Insights | Details |

|---|---|

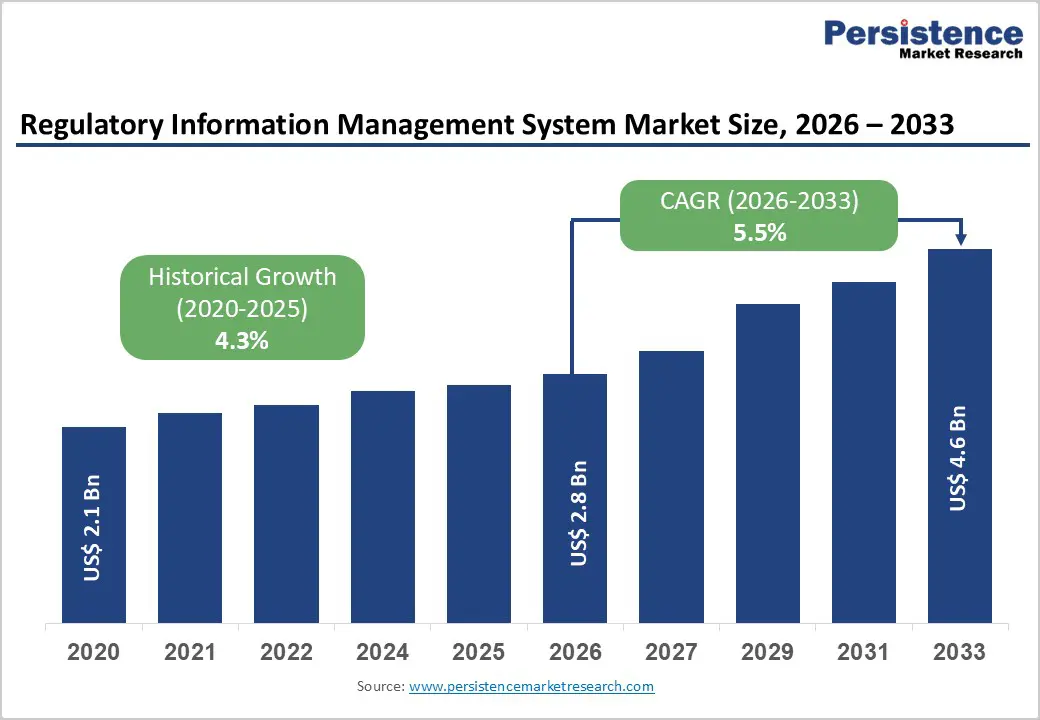

| Regulatory Information Management System Market Size (2026E) | US$ 2.8 Bn |

| Market Value Forecast (2033F) | US$ 4.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Driver - Increasing Regulatory Complexity and Accelerated Digital Transformation Across Life Sciences

The growing complexity of global regulatory frameworks is a major force encouraging organizations to adopt structured regulatory information management platforms. Pharmaceutical, biotechnology, and medical device companies now operate across multiple jurisdictions, each governed by evolving submission standards, documentation requirements, and post-approval obligations. Managing variations, renewals, labeling updates, and lifecycle records through manual or fragmented systems creates compliance risks and operational inefficiencies. As product pipelines expand and approval timelines become more competitive, companies increasingly rely on centralized digital environments that enable standardized data management and submission tracking.

Regulatory authorities worldwide are promoting electronic submissions and harmonized documentation formats, pushing organizations toward automated regulatory infrastructures. Modern RIMS platforms improve transparency, enable audit readiness, and reduce duplication of regulatory data across departments. Integration with clinical, quality, and pharmacovigilance systems enhances cross-functional collaboration while supporting faster decision-making. Additionally, globalization of clinical trials and the rising biologics development generate higher submission volumes, strengthening demand for scalable solutions. Cloud adoption, automation capabilities, and AI-supported regulatory intelligence tools further accelerate implementation. As organizations prioritize efficiency, compliance accuracy, and faster product commercialization, digital regulatory management systems are becoming essential operational assets rather than optional tools.

Restraints - Implementation Complexity, High Transition Costs, and Organizational Change Barriers

Despite strong adoption momentum, several operational and financial factors continue to restrain widespread deployment of advanced regulatory information management solutions. Implementation often requires substantial upfront investment, including software licensing, system validation, infrastructure upgrades, and integration with existing enterprise platforms. For small and mid-sized organizations, transitioning from legacy or paper-based processes can be resource-intensive, both financially and operationally. Migration of historical regulatory data into standardized digital formats presents additional challenges, particularly when records exist across disconnected repositories.

Organizational readiness also influences adoption speed. Successful deployment requires trained regulatory professionals capable of managing structured data environments and adapting to automated workflows. Resistance to workflow changes and dependence on established manual processes can slow digital transformation initiatives. Furthermore, customization requirements to align systems with region-specific regulations increase implementation timelines and operational complexity. Data security concerns and compliance validation obligations add further layers of scrutiny before full deployment. Inconsistent regulatory harmonization across countries may also require ongoing configuration adjustments. These technical, financial, and cultural barriers can delay adoption, especially among emerging companies or organizations operating with constrained IT resources, thereby moderating overall market expansion despite clear long-term benefits.

Opportunity - AI-Enabled Regulatory Intelligence and Expansion into Emerging Life Sciences Markets

Rapid advances in digital technologies are opening significant growth avenues through intelligent and connected regulatory management ecosystems. Artificial intelligence and advanced analytics are transforming how organizations monitor regulatory changes, interpret guidelines, and prepare submissions. Automated regulatory intelligence tools can track evolving global requirements, identify compliance gaps, and support proactive planning, significantly reducing manual workload for regulatory teams. Predictive analytics further enable companies to optimize submission strategies and improve approval success rates.

Expansion of pharmaceutical manufacturing and clinical development activities in emerging economies presents another substantial opportunity. As companies in Asia Pacific, Latin America, and parts of the Middle East expand international market participation, the need for standardized regulatory infrastructure becomes increasingly critical. Cloud-based platforms allow scalable deployment without heavy capital investment, making adoption accessible to growing enterprises. Increasing outsourcing to contract research and manufacturing organizations also drives demand for collaborative regulatory environments that enable secure data sharing across partners. Integration with digital quality management and real-world evidence systems enhances lifecycle oversight beyond initial approvals. As healthcare innovation accelerates globally and regulatory oversight becomes more data-driven, intelligent, and interoperable, and automation-focused regulatory management solutions are positioned to unlock long-term growth potential.

Category-wise Analysis

By Component Insights

The software segment is projected to dominate the global regulatory information management system market in 2026, accounting for a 67.8% revenue share. Its leadership stems from increasing reliance on centralized digital platforms that manage regulatory data, submissions, product registrations, and lifecycle documentation across multiple regions. Life sciences companies are replacing fragmented manual systems with integrated regulatory software to improve compliance accuracy and accelerate approval timelines. These platforms enable automated workflows, standardized documentation, audit readiness, and real-time collaboration between regulatory, quality, and clinical teams. Growing submission volumes, evolving global regulations, and the need for structured data governance further strengthen adoption. Advanced capabilities such as cloud accessibility, analytics dashboards, and AI-assisted regulatory intelligence enhance operational efficiency. Continuous upgrades supporting eCTD publishing, global tracking, and compliance monitoring ensure scalability, making software solutions the foundation of modern regulatory operations and sustaining their dominant position within the component landscape.

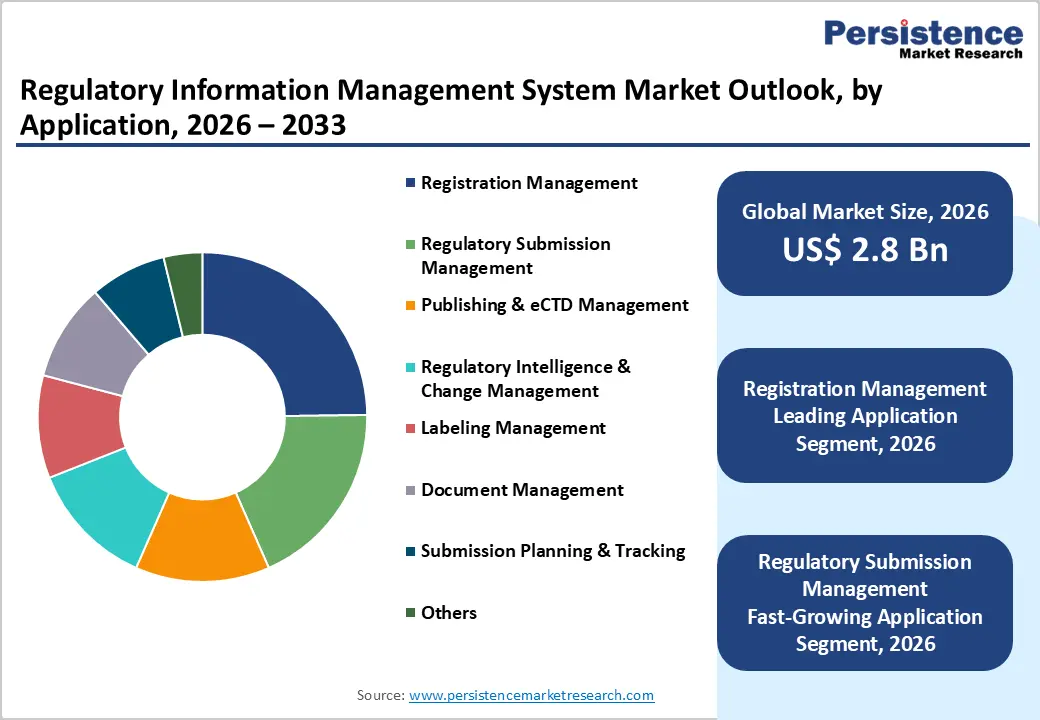

By Application Insights

The cloud-based segment is expected to lead the global regulatory information management system market in 2026, capturing a 59.6% revenue share. Organizations increasingly prefer cloud infrastructure to support geographically distributed regulatory teams managing simultaneous submissions across multiple health authorities. Cloud deployment enables centralized data access, faster system updates, reduced IT infrastructure costs, and improved interoperability with quality and clinical systems. The shift toward remote regulatory operations and digital transformation initiatives has accelerated migration from legacy on-premise platforms. Cloud environments also allow rapid adaptation to changing compliance requirements and evolving submission standards without extensive system downtime. Enhanced cybersecurity frameworks, validated environments, and subscription-based pricing models further encourage adoption among both large enterprises and mid-sized firms. Integration with analytics tools and regulatory intelligence databases improves decision-making efficiency, enabling faster approvals and lifecycle management, thereby reinforcing the segment’s sustained market leadership.

By End-user Insights

The pharmaceutical and biotechnology companies segment is projected to dominate the global regulatory information management system market in 2026, holding a 44.3% revenue share. These organizations manage extensive product pipelines requiring continuous regulatory submissions, variations, renewals, and post-market compliance activities across multiple jurisdictions. Increasing drug development activities and globalization of clinical trials significantly elevate regulatory documentation requirements, driving reliance on structured information management platforms. RIMS solutions help streamline approval workflows, maintain submission consistency, and ensure adherence to evolving global standards. Adoption is further strengthened by regulatory pressure for transparency, electronic documentation, and lifecycle traceability. Pharmaceutical firms benefit from automation features that reduce manual errors and improve inspection preparedness. Growing biologics and specialty drug development, along with expanding international market entry strategies, continue to generate sustained demand, positioning pharmaceutical and biotechnology companies as the primary contributors to market revenue.

Regional Insights

North America Regulatory Information Management System Market Trends

North America is anticipated to remain the largest regional market in 2026, representing a value share of 46.7%, led primarily by the United States. The region benefits from a mature life sciences ecosystem, a strong presence of multinational pharmaceutical and biotechnology companies, and early adoption of digital regulatory technologies. Organizations increasingly deploy advanced RIMS platforms to manage complex submission requirements imposed by regulatory authorities and to support accelerated drug approval pathways. High investment in research and development generates substantial regulatory documentation volumes, necessitating automated data governance solutions.

Companies prioritize integrated systems that connect regulatory affairs with quality management, pharmacovigilance, and clinical operations to improve operational transparency. Strong emphasis on compliance readiness, electronic submissions, and standardized data formats further drives implementation. Additionally, widespread cloud adoption, expansion of AI-enabled regulatory analytics, and ongoing modernization initiatives across enterprises strengthen regional growth. Continuous innovation by technology vendors and strategic collaborations between software providers and life sciences firms sustain North America’s leadership and stable revenue expansion.

Europe Regulatory Information Management System Market Trends

Europe’s regulatory information management system market is expected to experience steady growth in 2026, supported by stringent regulatory frameworks and increasing digital transformation across the pharmaceutical and medical device industries. Countries including Germany, the U.K., France, and Italy demonstrate strong adoption as organizations adapt to evolving regional compliance requirements and harmonized regulatory standards. Companies are investing in structured regulatory data platforms to manage complex variations, renewals, and cross-border submissions efficiently. The growing emphasis on transparency, data traceability, and lifecycle documentation encourages migration from legacy systems toward integrated RIMS environments.

Expansion of biologics development and personalized medicine further increases submission complexity, reinforcing demand for automation. European firms also focus on improving collaboration between regional affiliates through centralized regulatory databases. Continuous upgrades in cloud infrastructure, interoperability capabilities, and analytics integration enhance operational performance. Supportive regulatory modernization initiatives and increasing adoption among mid-sized enterprises continue to strengthen long-term market expansion across the region.

Asia Pacific Regulatory Information Management System Market Trends

The Asia Pacific regulatory information management system market is projected to register a higher CAGR of around 8.7% between 2026 and 2033, driven by the rapid expansion of pharmaceutical manufacturing and growing participation in global clinical development. Countries such as China, India, Japan, and South Korea are witnessing increasing regulatory modernization, encouraging companies to adopt digital compliance platforms. Rising drug exports and international market entry strategies require standardized submission processes aligned with global regulatory authorities, accelerating RIMS implementation. Governments across the region are strengthening approval frameworks and promoting electronic documentation systems, creating favorable adoption conditions.

Expanding biotechnology ecosystems and increasing investments from multinational firms further contribute to demand. Cost-efficient cloud solutions enable adoption among emerging domestic manufacturers seeking scalable compliance infrastructure. Additionally, workforce digitalization, growing outsourcing activities, and collaboration between regional affiliates and global headquarters support the integration of centralized regulatory databases. Continuous improvements in connectivity, automation, and analytics capabilities are enhancing operational efficiency, positioning the Asia Pacific as the fastest-growing regional market.

Competitive Landscape

The global regulatory information management system market is highly competitive, with strong participation from AmpleLogic, ArisGlobal, Calyx, Dassault Systemes, DDi, and DXC Technology. These players leverage established global client networks, regulatory expertise, and continuous innovation in cloud platforms, data integration, compliance automation, and submission management solutions to support complex regulatory workflows.

Increasing regulatory scrutiny, rising product approvals, and digital transformation across life sciences organizations are accelerating adoption. Vendors are focusing on scalable cloud deployments, AI-driven regulatory intelligence, interoperability, and real-time data visibility, while strengthening strategic partnerships, expanding into emerging markets, and investing in advanced compliance and lifecycle management capabilities.

Key Industry Developments:

- In February 2026, U.S. Food and Drug Administration introduced the Technology-Enabled Meaningful Patient Outcomes (TEMPO) for Digital Health Devices Pilot, aligned with the Center for Medicare and Medicaid Innovation’s ACCESS model, aiming to expand patient access to selected digital health devices while maintaining strong safety and regulatory oversight standards.

- In May 2024, Rimsys announced the beta launch of Rimsys Intel, a community-driven centralized platform designed to provide global regulatory intelligence data for the medtech industry. The solution expands the company’s mission of improving access to life-enhancing medical technologies by offering users free regulatory insights, including legislation updates, regulatory affiliations, UDI requirements, device risk classifications, and country-specific market access information for medical devices and IVDs.

- In February 2023, ArisGlobal announced the launch of Investigational Product RIMS, a solution developed to address the specific regulatory management requirements of life sciences and medical device companies during the investigational phases of drug development, further expanding its LifeSphere® platform to support automated and streamlined regulatory workflows.

Companies Covered in Regulatory Information Management System Market

- AmpleLogic

- ArisGlobal

- Calyx

- Dassault Systemes

- DDi

- DXC Technology

- Ennov

- Ithos Global (Cordance Group)

- Kalypso (Rockwell Automation)

- Korber

- LORENZ Life Sciences Group

- MasterControl

- PhlexGlobal

- Rimsys

- Veeva Systems

- Others

Frequently Asked Questions

The global regulatory information management system market is projected to be valued at US$ 2.8 Bn in 2026.

Increasing global regulatory complexity and the shift toward digital, cloud-based compliance management systems are driving the adoption of regulatory information management platforms to streamline submissions and lifecycle compliance.

The global regulatory information management system market is poised to witness a CAGR of 5.5% between 2026 and 2033.

Growing adoption of AI-enabled regulatory automation and expanding pharmaceutical and medical device activities in emerging markets create major opportunities for advanced RIMS deployment.

AmpleLogic, ArisGlobal, Calyx, Dassault Systemes, DDi, and DXC Technology are some key players in the regulatory information management system market.