- Specialty & Fine Chemicals

- Refinery Process Chemical Market

Refinery Process Chemical Market Size, Share, and Growth Forecast 2026 - 2033

Refinery Process Chemical Market by Chemical Type (Catalysts, pH Adjusters, Anti-fouling Agents, Corrosion Inhibitors, Demulsifiers), Application (Crude Oil Distillation, Hydrotreating, Catalytic Cracking, Alkylation, Isomerization), End-user (Petroleum Refineries, Petrochemical Plants, Chemical Processing Facilities, Other), and Regional Analysis for 2026 - 2033

Refinery Process Chemical Market Size and Trend Analysis

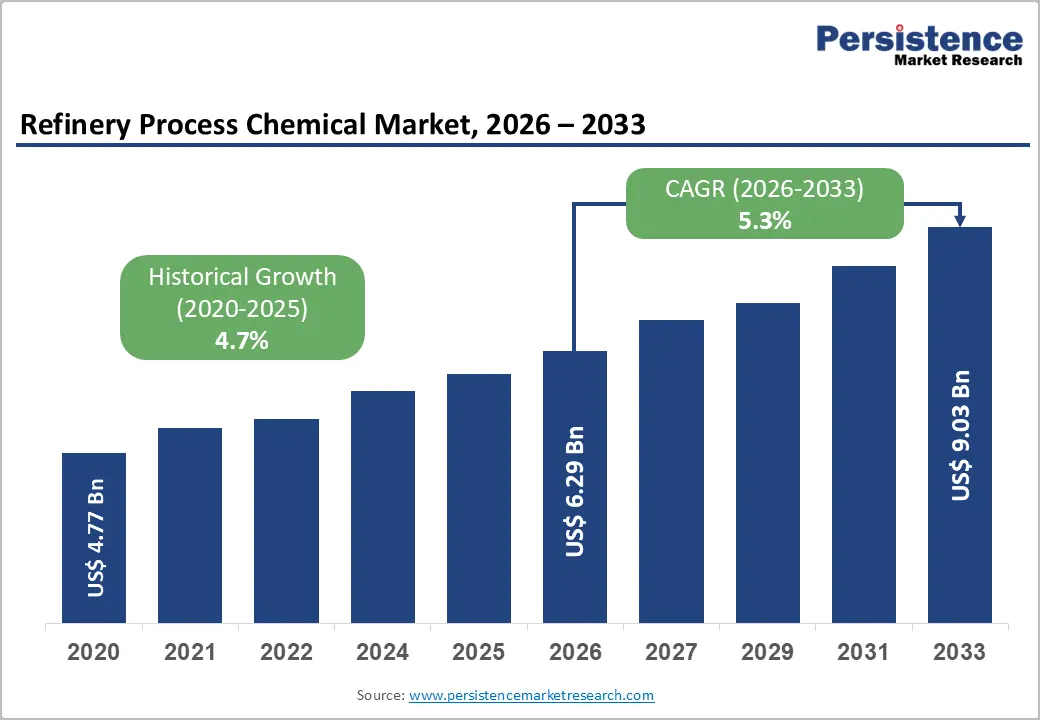

The global refinery process chemical market size is supposed to be valued at US$ 6.3 Bn in 2026 and is projected to reach US$ 9.0 Bn by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

Market expansion is primarily driven by stringent environmental regulations mandating ultra-low-sulfur fuel production, with the U.S. Environmental Protection Agency (EPA) implementing Tier 3 standards that require a reduction in sulfur content to 10 parts per million (ppm) from the previous 30 ppm level. According to the Global Energy Association, the anticipated increase of 2.6-4.9 million barrels per day (b/d) in global refining capacity through 2028, concentrated in the Asia-Pacific and Middle Eastern regions, is generating substantial demand for specialized process chemicals, including catalysts, corrosion inhibitors, and demulsifiers.

Key Industry Highlights

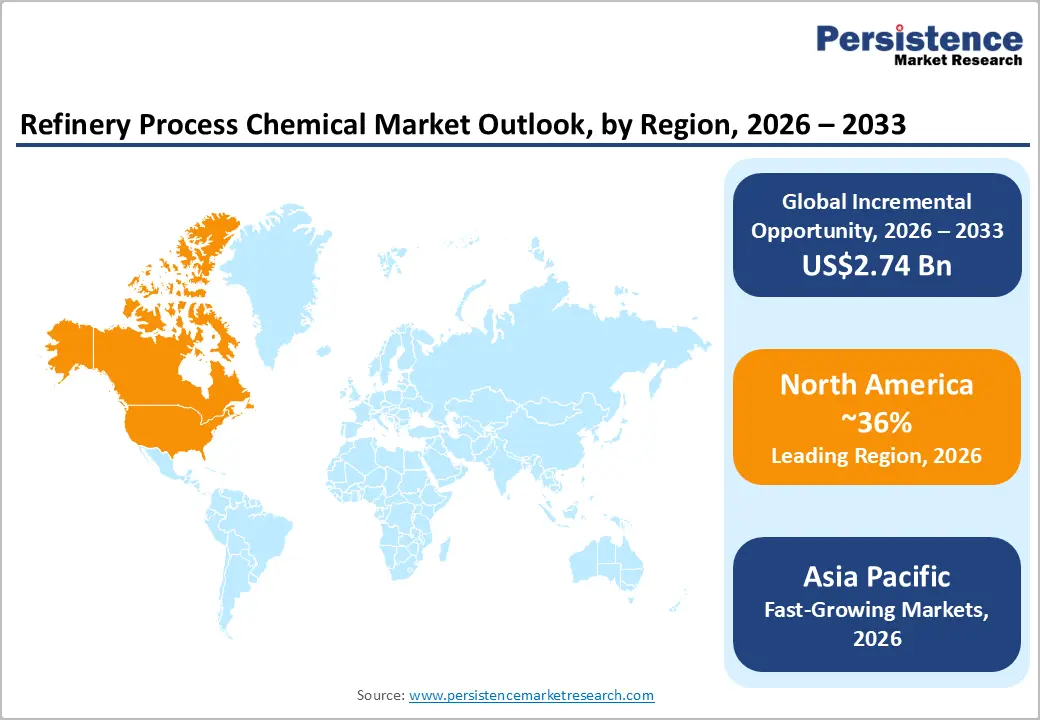

- Leading Region: North America leads the refinery process chemicals market, with 36% market share, due to the dominance of U.S. refining capacity, stringent EPA regulations, and ongoing expansions by major operators.

- Fastest Growing Region: Asia Pacific represents the fastest-growing regional market, propelled by India's 20% refining capacity expansion by 2028 and China's capacity crossing 19 million barrels per day in 2024, with new greenfield refineries including Yulong Petrochemical, and multiple brownfield expansions driving accelerated process chemical consumption growth.

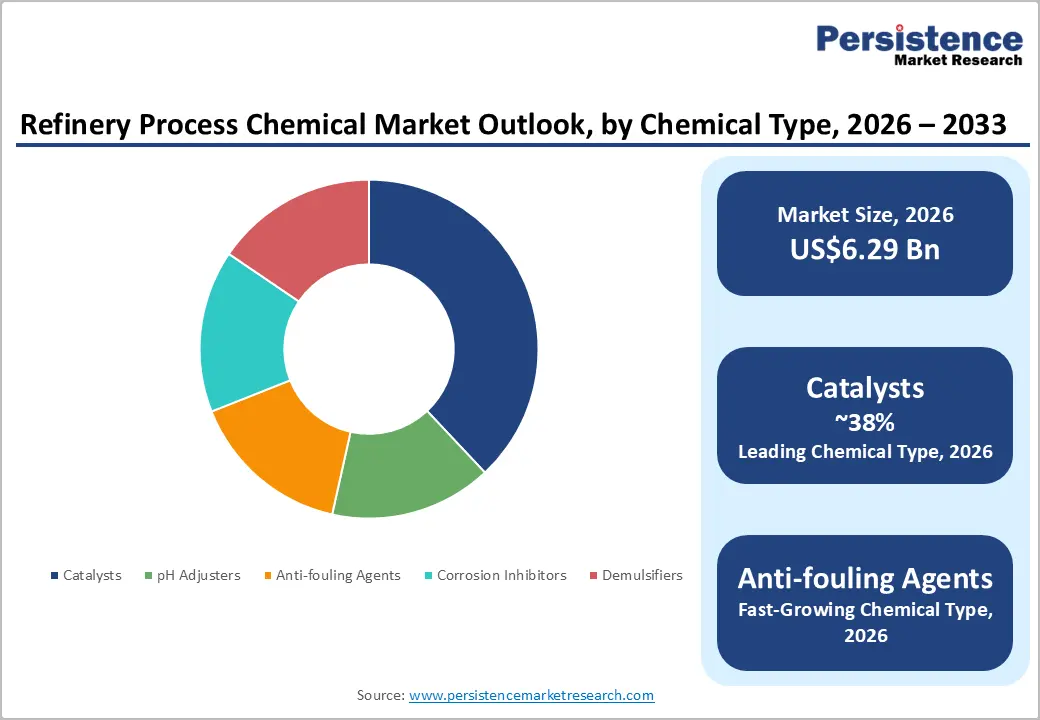

- Dominant Segment: Catalysts dominate the chemical type category with approximately 38% market share, driven by their indispensable role in hydrotreating, catalytic cracking, and hydrocracking processes essential for meeting stringent EPA Tier 3 sulfur standards.

- Fastest Growing Segment: The anti-fouling agents represent the fastest-growing segment, driven by increased processing of opportunity crudes containing elevated acid numbers and contaminant loadings requiring specialized chemical packages preventing equipment fouling and corrosion while enabling efficient desalting operations.

- Key Market Opportunity: Advanced catalyst technologies incorporating proprietary innovations like BASF's AIM and MFT technologies present substantial opportunities, as demonstrated by Fourtiva™ catalyst's superior economic performance in maximizing butylene yields while reducing carbon footprints, addressing refiners' dual objectives of profitability enhancement and sustainability compliance in an increasingly carbon-constrained operating environment.

| Key Insights | Details |

|---|---|

| Refinery Process Chemicals Market Size (2026E) | US$ 94.3 Bn |

| Market Value Forecast (2033F) | US$ 137.2 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.5% |

| Historical Market Growth (2020 - 2025) | 5.1% |

Market Dynamics

Drivers Stringent Environmental Regulations Driving Demand for Advanced Process Chemicals

Global regulatory frameworks increasingly require refineries to produce cleaner fuels with significantly lower sulfur content, thereby elevating demand for specialized refinery process chemicals. The EPA’s Tier 3 gasoline sulfur standard, fully enforced since 2017, mandates sulfur levels of 10 ppm, necessitating extensive use of hydrotreating catalysts and pH-adjusting agents to ensure compliance. Likewise, regulations aimed at mitigating corrosion-related incidents and minimizing operational downtime are compelling refineries to invest proactively in advanced corrosion inhibitors, particularly as aging infrastructure demands more frequent protection.

The industry’s transition toward environmentally sustainable inhibitor formulations offering enhanced efficiency and longer service life is gaining notable momentum, supported by growing recognition of the substantial economic losses associated with corrosion damage. Collectively, these regulatory pressures and the broader global shift toward sustainability are reshaping refinery chemical consumption patterns and accelerating market growth.

Expansion of Global Refining Capacity in Emerging Markets

The rapid expansion of refining capacity across the Asia-Pacific region, particularly in China and India, is driving exceptional demand for refinery process chemicals. Global refining capacity reached 103.5 million barrels per day in 2023, with an additional 2.6 to 4.9 million barrels per day expected to come online by 2028. China is scheduled to commission four new refineries between 2025 and 2027, while India’s refining capacity is projected to grow by more than 20% by 2028, reaching nearly 300 million metric tons.

The Yulong Petrochemical refinery in Shandong, with a capacity of 400,000 barrels per day, began trial operations in 2024. These greenfield and brownfield projects require substantial volumes of catalysts, corrosion inhibitors, and demulsifiers to support efficient operations and protect equipment, especially as refineries increasingly process complex, heavy feedstocks.

Restraints - Refinery Closures and Capacity Reductions in Mature Markets

European refining capacity is experiencing a pronounced contraction as the energy transition accelerates. The International Energy Agency (IEA) projects that between 1.0 and 1.5 million barrels per day of refining capacity may be shut down across Europe by 2030, significantly exceeding the historical annual closure average of 220,000 b/d. Major facilities in Germany, Italy, and the United Kingdom have already announced closures or substantial capacity reductions, including Shell’s planned cessation of crude processing at its Wesseling site by 2025 and BP’s one-third capacity reduction at Gelsenkirchen.

Clariant AG has also confirmed the shutdown of its phenol plant in Gladbeck, along with propylene oxide and propylene glycol production in Cologne. Refinery utilization rates in North-Western Europe are expected to decline from 84% in 2024 to 81% by 2027, with further accelerated shutdowns anticipated between 2029 and 2030. These developments are directly constraining regional demand for refinery process chemicals, creating significant challenges for market participants with substantial exposure to European operations.

Volatile Refining Margins Impacting Chemical Procurement

Global refining margins have weakened considerably, leading refineries to adjust operations in ways that reduce consumption of process chemicals. The IEA lowered its global refinery throughput forecast for 2024 to 82.8 million b/d, a decrease of 180,000 b/d, and for 2025 to 83.4 million b/d, down 210,000 b/d, largely due to declining margins driven by deteriorating gasoline, jet fuel, and diesel cracks.

Throughout 2024, the IEA cumulatively cut refinery run expectations by 500,000 b/d, with the majority of reductions occurring in China despite higher throughput in OECD countries such as the United States. In such environments, refiners, particularly in North America, are implementing economic run cuts and deferring maintenance, directly reducing near-term demand for process chemicals. S&P Global Commodity Insights further reduced fourth-quarter 2024 run forecasts by 50,000 b/d as economic run cuts spread across Europe and other regions, underscoring mounting pressure on refinery profitability.

Opportunity - Advanced Catalyst Technologies for Efficiency and Sustainability

The advancement and commercialization of next-generation catalyst technologies are creating significant growth opportunities for market participants, as refineries increasingly prioritize operational efficiency, higher product yields, and lower carbon footprints. BASF SE introduced Fourtiva™, an advanced Fluid Catalytic Cracking (FCC) catalyst, in 2024, incorporating its proprietary Advanced Innovative Matrix (AIM) and Multiple Frameworks Topology (MFT) technologies designed for gasoil to mild-resid feedstocks.

Commercial trials have validated its strong economic performance. Additionally, BASF’s inauguration of its Catalyst Development and Solids Processing Center in Ludwigshafen in December 2024 has strengthened its innovation capabilities by accelerating the transition of lab-scale catalyst developments to production. As refineries adopt more advanced catalysts across hydrotreating and catalytic cracking units, opportunities continue to expand for suppliers with strong research and development capabilities.

Emissions Abatement Technologies and Flare Gas Recovery Systems

Growing regulatory pressure to reduce greenhouse gas emissions and improve flare gas recovery is creating significant opportunities for companies offering integrated solutions that combine refinery process chemicals with advanced monitoring technologies. Baker Hughes has demonstrated a major advancement through its collaboration with bp, utilizing the flare.IQ emissions-abatement technology to quantify methane emissions from flares. This platform, part of the Panametrics portfolio, enables operators to analyze parameters such as temperature, pressure, gas velocities, and composition to optimize combustion efficiency while reducing emissions.

In November 2024, Baker Hughes and SOCAR signed a contract at COP29 for an integrated gas recovery and hydrogen sulfide (H-S) removal system at the Heydar Aliyev Oil Refinery. Expected to recover 7 million Nm³ of methane annually and cut CO- emissions by 11,000 tons, the project will also lower fuel gas consumption, underscoring the value of combined chemical and recovery-system solutions.

Category-wise Analysis

Chemical Type Insights

Catalysts hold approximately 38% of the refinery process chemicals market due to their essential role in hydrotreating, catalytic cracking, and hydrocracking. They are critical for meeting stringent fuel quality standards, particularly in hydrotreating, where catalysts remove sulfur, nitrogen, and other impurities under temperatures of 300°F to 800°F and pressures of 400 to 2,000 psi.

Shell Catalysts & Technologies reports that its advanced hydrotreating systems, including CENTERA™ second-generation catalysts (DN-3636 and DC-2635), deliver significant improvements in hydrodesulfurization, hydrodenitrogenation, and aromatic saturation, while maintaining stability with challenging feedstocks. Growing adoption of advanced catalyst technologies that enhance light hydrocarbon yields, fuel quality, and energy efficiency continues to reinforce catalyst dominance. Companies are increasingly investing in more selective and durable catalytic solutions to support complex refining operations and reduce carbon footprints across FCC and hydroprocessing units.

Application Insights

Hydrotreating is the leading application segment, accounting for about 32% of market share due to its critical role in producing ultra-low sulfur fuels and preparing feedstocks for downstream processes. It is a core refining operation in which oil fractions react with hydrogen over catalysts to generate cleaner products under conditions tailored to specific requirements. The process maintains the molecular structure of the feedstock while improving quality and ensuring compliance with environmental regulations, including the EPA’s Tier 3 mandate of 10 ppm sulfur in gasoline.

It is commonly used before hydrocracking to remove sulfur, nitrogen, and other impurities that can deactivate catalysts and hinder efficiency. Hydrotreating also provides operational benefits such as improved availability, higher on-stream factors, and reduced turnaround duration, reinforcing its position as the dominant application for refinery process chemicals.

End-user Insights

Petroleum refineries represent the largest end-use segment, accounting for about 62% of market share, as they consume substantial volumes of catalysts, corrosion inhibitors, demulsifiers, and other process chemicals across various unit operations. Global refining capacity reached 103.5 million barrels per day in 2023, with significant additions expected through 2028, particularly in the rapidly expanding Asia-Pacific region.

Refineries require continuous chemical inputs for crude oil distillation, hydrotreating, catalytic cracking, alkylation, and isomerization to maintain operational efficiency, meet fuel quality standards, and mitigate corrosion and fouling. Aging infrastructure in mature markets further increases demand for corrosion inhibitors and anti-fouling agents, while processing more complex feedstocks such as heavy crude and resid necessitates advanced process chemical solutions. The IEA forecasts refinery throughput to reach 83.4 million b/d in 2025, underscoring sustained demand for process chemicals.

Regional Insights

North America Refinery Process Chemical Market Trends

North America leads the refinery process chemicals market, with 36% share, due to the dominance of U.S. refining capacity, stringent EPA regulations, and ongoing expansions by major operators such as ExxonMobil. The EPA’s Tier 3 sulfur standard, finalized in 2014 and implemented in 2017, reduced gasoline sulfur limits from 30 ppm to 10 ppm, prompting substantial investments in hydrotreating catalysts and related process chemicals. The accompanying ABT credit-trading program supported compliance until the transition period ended in 2020.

U.S. refinery capacity as of January 2025 continues to support strong chemical demand. The region also benefits from a robust innovation ecosystem, with leading chemical companies advancing catalyst development. Despite regulatory pressures, North American refiners saw improved margins in 2024, reinforcing demand for advanced catalysts, corrosion inhibitors, and integrated emissions-abatement solutions.

Europe Refinery Process Chemical Market Trends

Europe’s refining sector is undergoing a major structural shift as the energy transition accelerates. The IEA projects that 1.0 to 1.5 million b/d of refining capacity may be shut down by 2030, far exceeding the historical annual closure average of 220,000 b/d. Major facilities in Germany are leading these reductions, with Shell planning to end crude processing at Wesseling by 2025 and BP cutting capacity at Gelsenkirchen by one-third.

Additional shutdowns include Italy’s Livorno refinery and the potential closure of the Grangemouth refinery in the United Kingdom. Declining fossil-fuel demand, driven by electric-vehicle adoption and CO--reduction policies, is reshaping chemical consumption patterns, with utilization rates expected to fall from 84% in 2024 to 81% in 2027. Despite these pressures, stringent EU environmental standards continue to support demand for advanced process chemicals, while companies such as Clariant and Shell streamline operations and reinforce sustainability commitments.

Asia Pacific Refinery Process Chemical Market Trends

Asia Pacific is the fastest-growing region for refinery process chemicals, driven by substantial capacity expansions in China and India. China’s refining capacity is projected to exceed 19 million barrels per day in 2024, supported by major developments such as the 400,000 b/d Yulong Petrochemical refinery and multiple new facilities planned between 2025 and 2027. The region will account for the majority of the 2.6 to 4.9 million b/d of global refining capacity additions expected between 2023 and 2028.

India is witnessing similarly strong growth, with refining capacity set to rise more than 20% by 2028, supported by both brownfield expansions and new Euro-6-compliant projects. Lower EV adoption compared with China ensures continued gasoline and diesel demand, while favorable investment conditions in ASEAN nations further reinforce Asia Pacific’s dominant position in the global refinery process chemical market growth.

Competitive Landscape

The refinery process chemical market shows moderate consolidation, with major multinational companies such as BASF SE, Dow Inc., Clariant AG, Honeywell UOP, and Baker Hughes holding substantial market shares through broad product portfolios, global distribution networks, and long-standing relationships with leading refiners. Market leaders increasingly prioritize innovation-driven growth, establishing advanced catalyst development centers and launching next-generation products based on proprietary technologies. Strategic partnerships with end-users, such as Baker Hughes’ collaboration with bp on emissions-abatement technologies, are becoming more common. Companies are also expanding into high-growth regions, particularly Asia-Pacific, while rationalizing operations in mature markets. A shift toward integrated solutions that combine chemicals, monitoring technologies, services, and performance guarantees is emerging as a key competitive differentiator.

Key Developments:

- August 2024: BASF SE announced the commercial launch of Fourtiva™, a new Fluid Catalytic Cracking (FCC) catalyst incorporating Advanced Innovative Matrix (AIM) and Multiple Framework Topology (MFT) technologies, designed to maximize butylene yields and selectivity while improving naphtha octane, LPG olefinicity, and minimizing coke and dry gas production.

- November 2024: Baker Hughes and SOCAR signed a contract at COP29 in Baku, Azerbaijan, for an integrated gas recovery and hydrogen sulfide (H-S) removal system at SOCAR's Heydar Aliyev Oil Refinery, expected to recover flare gas equivalent to 7 million Nm³ of methane annually and reduce CO- emissions by 11,000 tons per year, with commissioning targeted within 24 months.

- December 2024: BASF SE officially opened its new Catalyst Development and Solids Processing Center in Ludwigshafen, Germany, strengthening its innovative capabilities and enabling faster transition of lab-developed catalysts to production scale to provide customers with high-quality pilot samples of new catalysts more flexibly.

Top Companies in the Refinery Process Chemical Market

- BASF SE (Ludwigshafen, Germany) maintains a leading position in the refinery process chemicals market through its extensive portfolio of catalysts and process chemicals, backed by substantial research and development investments. The company's recent launch of Fourtiva™ FCC catalyst in 2024, incorporating proprietary AIM and MFT technologies, demonstrates its innovation leadership in helping refiners maximize profitability while reducing carbon footprints.

- Baker Hughes (Houston, Texas, U.S.) distinguishes itself through integrated emissions-abatement and process-optimization solutions that combine hardware, software, and chemicals. The company's flare.IQ technology, successfully deployed with bp to quantify methane emissions from flares, represents a breakthrough innovation in emissions monitoring. Baker Hughes' contract with SOCAR for an integrated gas recovery and H-S removal system signed at COP29 in November 2024 exemplifies its ability to deliver rapid solutions (concept to contract in nine months) that simultaneously address environmental compliance and operational efficiency, creating compelling value propositions for refiners facing emissions reduction mandates.

- Clariant AG (Muttenz, Switzerland) operates as a prominent specialty chemical company with significant exposure to refinery catalysts and process chemicals. The company is implementing a differentiated purpose-led growth strategy focused on innovation arenas expected to deliver approximately 70% of profitable growth, with an innovation rate targeted to reach approximately 20% by 2027. Clariant's commitment to sustainability, including upgraded non-financial targets with increased greenhouse gas emission reductions aligned with 1.5°C scenarios, positions the company favorably as refiners increasingly prioritize environmentally friendly process chemical solutions.

Companies Covered in Refinery Process Chemical Market

- BASF SE

- Dow Inc.

- Evonik Industries

- Barry Chemicals

- Buckman

- Cestoil

- Chemiphase

- Chevron Phillips Chemical Company LLC

- Clariant AG

- Honeywell UOP

- Baker Hughes

- Exxon Mobil Corporation

- Lubrizol

- Shell Catalysts & Technologies

- Nalco Water

- SUEZ

- Arkema Group

Frequently Asked Questions

The global Refinery Process Chemical Market is projected to reach US$ 9.0 Bn by 2033, growing from US$ 6.3 Bn in 2026 at a compound annual growth rate (CAGR) of 5.3% during the forecast period.

Stringent environmental regulations, particularly the EPA's Tier 3 sulfur standard requiring 10 ppm sulfur content in gasoline, are the primary demand drivers, necessitating extensive use of hydrotreating catalysts and related process chemicals.

Catalysts dominate the chemical type category, accounting for approximately 38% of market share, driven by their critical role in key refining processes, including hydrotreating, catalytic cracking, and hydrocracking.

North America leads the refinery process chemicals market, with 36% market share, due to the dominance of U.S. refining capacity, stringent EPA regulations, and ongoing expansions by major operators.