- Pharmaceuticals

- Rare Gastrointestinal Diseases Treatment Market

Rare Gastrointestinal Diseases Treatment Market Size, Share, and Growth Forecast 2026 - 2033

Rare Gastrointestinal Diseases Treatment Market by Disease Type (Short Bowel Syndrome, Hirschsprung’s Disease, Eosinophilic Gastrointestinal Disorders, Chronic Intestinal Pseudo-Obstruction, Others), Treatment Type (Medications, Nutritional Therapy, Surgery, Supportive Care), Route of Administration (Oral, Injectable, Others), End-user (Hospitals, Specialty Clinics, Others), and Regional Analysis, 2026 - 2033

Rare Gastrointestinal Diseases Treatment Market Share and Trends Analysis

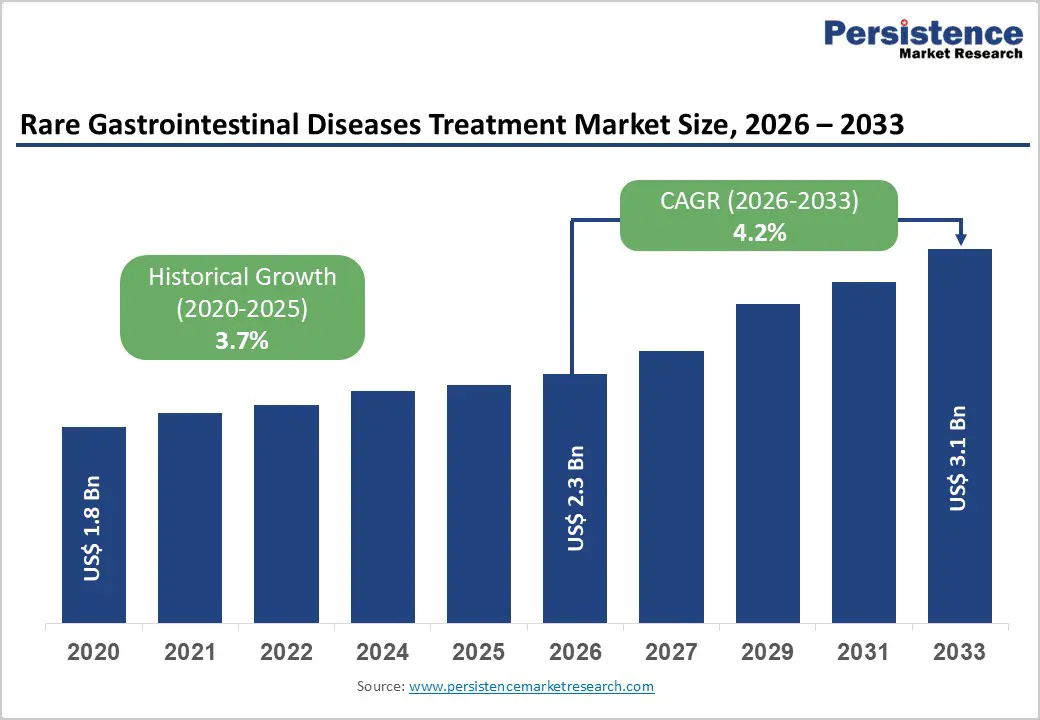

The global rare gastrointestinal diseases treatment market size is expected to be valued at US$ 2.3 billion in 2026 and projected to reach US$ 3.1 billion by 2033, growing at a CAGR of 4.2% between 2026 and 2033.

Rising diagnoses and management of conditions such as short bowel syndrome (SBS), Hirschsprung’s disease, eosinophilic gastrointestinal disorders (EGIDs), and chronic intestinal pseudo-obstruction (CIPO), combined with orphan-drug incentives, are steadily expanding the treated patient pool worldwide. Improved survival of preterm infants and children with complex congenital anomalies, together with greater utilization of advanced intestinal surgery and transplantation, is also increasing the prevalence of treatment-dependent rare gastrointestinal conditions. In parallel, strong pipelines in GLP-2 analogs, biologics such as dupilumab for EGIDs, and specialized medical nutrition solutions from players like Takeda Pharmaceutical Company and Nestlé Health Science are creating durable demand for high-value, specialty therapies.

Key Industry Highlights:

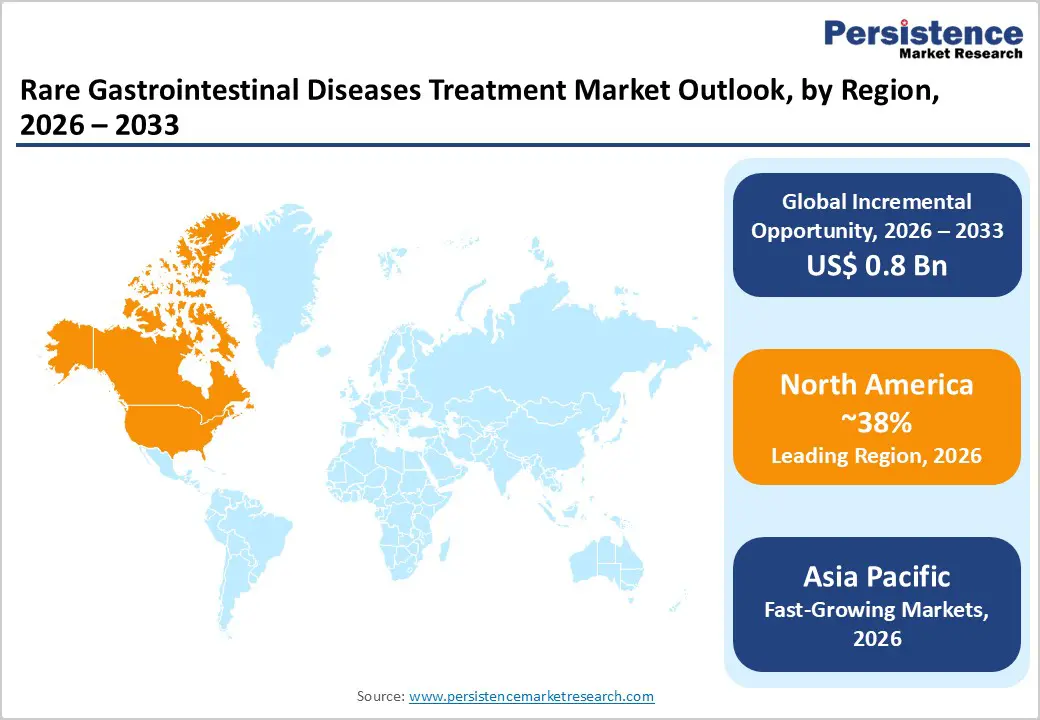

- Regional Leadership: North America remains the largest regional market, contributing about 38% of global rare gastrointestinal diseases treatment revenue in 2025, supported by strong orphan-drug frameworks, advanced intestinal rehabilitation centers, and high biologic adoption among U.S. and Canadian patients.

- Fast-growing Regional Market: Asia Pacific is projected to be the fastest-growing region through 2033, driven by expanding tertiary care capacity in China, Japan, India, and ASEAN, rising diagnosis of EGIDs and motility disorders, and gradual enhancement of rare-disease reimbursement policies.

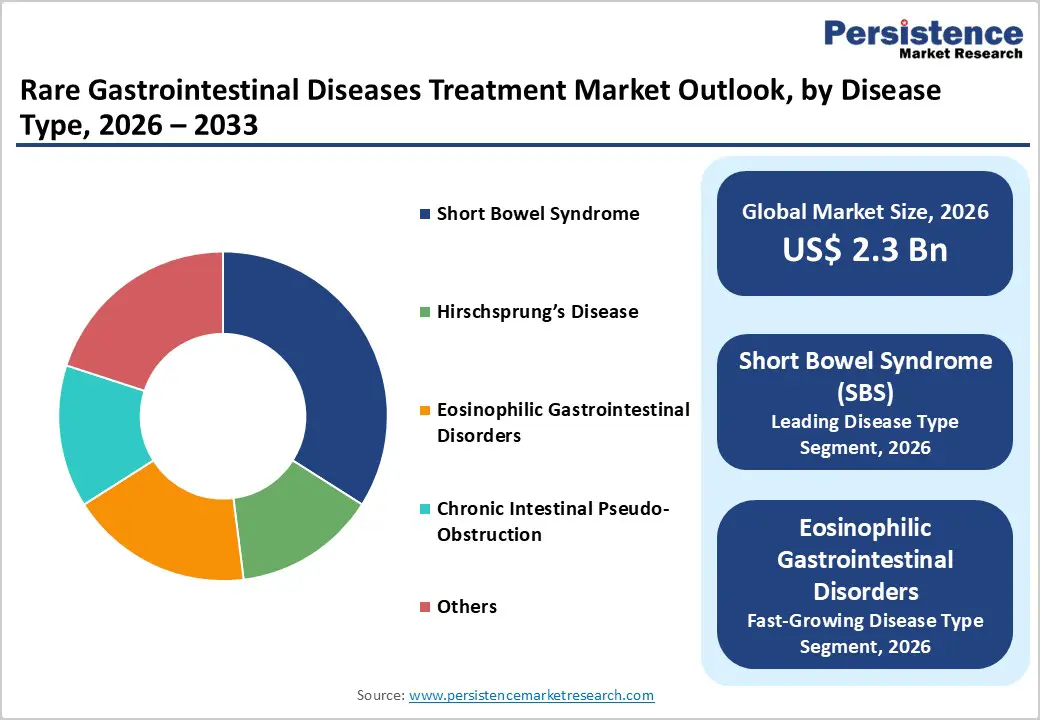

- Leading Disease Type: Short bowel syndrome (SBS) is the dominant disease-type segment with approximately 34% market share in 2025, reflecting its high treatment intensity, reliance on GLP-2 analogs, parenteral nutrition, and specialized medical nutrition, and the concentration of expertise in dedicated intestinal rehabilitation centers.

- Fast-growing Disease Type: Eosinophilic gastrointestinal disorders represent the fastest-growing disease-type segment, fueled by rising incidence, high unmet need, and the emergence of biologics such as dupilumab that show strong histologic and symptomatic remission rates in refractory patients.

- Opportunity - Integrated home-based care models combining advanced medical nutrition, GLP-2 analogs, and biologics, enabled by telehealth and coordinated rare-disease networks, which can reduce hospital utilization and improve quality of life for complex SBS, CIPO, and EGID patients.

| Key Insights | Details |

|---|---|

| Rare Gastrointestinal Diseases Treatment Market Size (2026E) | US$ 2.3 billion |

| Market Value Forecast (2033F) | US$ 3.1 billion |

| Projected Growth CAGR (2026 - 2033) | 4.2% |

| Historical Market Growth (2020 - 2025) | 3.7% |

Market Dynamics

Drivers - Growing Prevalence and Diagnosis of Rare Gastrointestinal Disorders

A key growth driver is the rising recognition and diagnosis of rare gastrointestinal diseases such as SBS, EGIDs, Hirschsprung’s disease, and CIPO, especially in high-income regions. Systematic reviews show that the global pooled prevalence of eosinophilic esophagitis alone has risen to about 40 cases per 100,000 inhabitants, with incidence and prevalence particularly high in North America and Europe, underscoring a larger base of patients eligible for long-term biologic and supportive therapies. Similarly, Hirschsprung’s disease has an estimated incidence of around 1 in 5,000 live births, and improved pediatric surgery and neonatal intensive care are increasing long-term survivors who require ongoing gastrointestinal surveillance and interventions. Greater awareness among gastroenterologists, establishment of rare disease centers, and wider use of endoscopy and histopathology have together expanded the addressable market for targeted medications, nutrition products, and surgical interventions.

Expansion of Orphan-Drug and Biologics Pipelines

The expansion of orphan-designated drugs and biologics tailored to rare gastrointestinal conditions is another powerful demand driver. Teduglutide (GATTEX®/REVESTIVE®, Takeda Pharmaceutical Company) is the first GLP-2 analog approved for SBS, and clinical trials showed response rates of 63% versus 30% for placebo in reducing parenteral support, firmly establishing pharmacologic intestinal rehabilitation as a reimbursable standard of care. New GLP-2 analogs such as glepaglutide from Zealand Pharma demonstrated clinical response rates of about 65.7% in Phase 3 trials and enabled up to 14% of patients to achieve enteral autonomy, highlighting a robust second wave of innovation. In EGIDs, biologics like dupilumab have induced histologic remission in a large proportion of eosinophilic gastritis and duodenitis patients refractory to conventional therapy, further broadening the therapeutic toolkit for rare gastrointestinal immune-mediated diseases.

Restraints- High Treatment Costs and Reimbursement Barriers

High per-patient treatment costs for orphan drugs and complex nutritional regimens remain a major restraint, especially outside high-income markets. Therapies such as GLP-2 analogs, long-term parenteral nutrition, and advanced biologics often carry annual treatment costs in the tens to hundreds of thousands of US dollars per patient, creating reimbursement pressure for payers and health systems. In many emerging economies and several parts of Latin America, Asia, and Africa, limited reimbursement pathways for rare diseases and gaps in insurance coverage sharply restrict patient access, leading to under-treatment and slower market uptake despite clear clinical need.

Clinical Complexity and Limited Specialized Infrastructure

Rare gastrointestinal diseases typically require multidisciplinary management involving specialized gastroenterologists, surgeons, dietitians, and motility experts, which is not uniformly available across regions. Conditions such as CIPO demand advanced diagnostic workups, including motility studies and expert histopathology, and patients frequently experience recurrent hospitalizations and complications despite therapy. Inadequate access to intestinal rehabilitation programs, parenteral nutrition centers, and pediatric motility units in many countries delays diagnosis and optimal treatment, thereby constraining the practical size of the treated population and dampening commercial potential for innovative therapies.

Opportunities - Biologics and Targeted Therapies for Eosinophilic Gastrointestinal Disorders

Biologics targeting type 2 inflammation in EGIDs represent one of the most attractive future opportunities in the rare gastrointestinal diseases treatment market. Meta-analytic data demonstrate rapidly rising incidence and prevalence of eosinophilic esophagitis and related EGIDs, particularly in North America and Europe, with prevalence in some cohorts exceeding 70 cases per 100,000 inhabitants. Early evidence indicates that dupilumab can induce clinical and histologic remission in 100% of eosinophilic gastritis and 66.6% of eosinophilic duodenitis patients in small series, while maintaining control of concurrent eosinophilic esophagitis, suggesting multi-segment disease modification potential. As large Phase 2 and 3 trials mature and additional biologic mechanisms (e.g., anti-Siglec-8, anti-IL-13) are explored, manufacturers such as Sanofi, Pfizer, and others will find substantial headroom to expand biologic penetration into a still under-treated, high-burden rare gastrointestinal segment.

Advanced Medical Nutrition and Home-Care Models for Short Bowel Syndrome and Motility Disorders

There is also a significant opportunity in advanced medical nutrition, enteral formulations, and home-care models for SBS and severe motility disorders. Retrospective data on peptide-based pediatric formulas like Peptamen Junior® from Nestlé Health Science showed reductions of up to 50% in abdominal distention and 39% in diarrhea, along with fewer inpatient and emergency visits over 12 months, demonstrating both clinical and economic benefits in SBS care. Companies developing specialized amino acid-based and peptide-based feeds, modular supplements, and home parenteral nutrition support programs can capture growing demand from tertiary centers that seek to improve quality of life and reduce hospital utilization in these fragile patients. As telehealth, remote monitoring, and integrated care pathways expand, scalable home-based treatment models for rare gastrointestinal disease management will become a key differentiator and revenue driver for industry participants.

Category-wise Insights

By Disease Type

Short bowel syndrome (SBS) is the leading disease-type segment, accounting for an estimated 34% share of the rare gastrointestinal diseases treatment market in 2025, reflecting its high treatment intensity and chronicity. Epidemiologic estimates suggest 10,000-15,000 adults with SBS in the United States alone, many dependent on long-term parenteral support and advanced pharmacologic intestinal rehabilitation. The availability of targeted therapies like teduglutide, as well as late-stage candidates such as glepaglutide, has transformed SBS from a purely supportive-care condition into a high-value specialty therapeutic area. In addition, robust investment in pediatric intestinal rehabilitation centers and home parenteral nutrition programs ensures sustained demand for both drugs and specialized nutrition, consolidating SBS as the dominant disease-type contributor to market revenue.

By Route of Administration

By route of administration, oral therapies are expected to hold the leading share approximately 54% of total revenue in 2025 owing to chronic use of acid suppressants, immunomodulators, and emerging targeted small molecules for rare gastrointestinal conditions. Many patients with Hirschsprung’s disease post-surgery, milder motility disorders, or low-intensity EGIDs rely on long-term oral medications and supplements to manage symptoms and nutritional status. At the same time, the injectable segment is expanding rapidly due to subcutaneous GLP-2 analogs like teduglutide and investigational glepaglutide, as well as injectable biologics for EGIDs, which are delivered via prefilled syringes or auto-injectors. As self-administration devices improve and home-care use increases, injectable routes will grow faster than the overall market, but the ubiquity and convenience of oral treatments should keep the oral segment in a leading position over the forecast period.

By End-user

Among end users, hospitals are projected to remain the dominant setting, capturing roughly 61% of rare gastrointestinal disease treatment spending in 2025. High-acuity management of SBS, CIPO, and complex Hirschsprung’s disease frequently requires inpatient care, advanced diagnostics, and multidisciplinary teams concentrated in tertiary and quaternary hospitals. Hospitals are also the primary initiation sites for GLP-2 analogs, biologics, and parenteral or specialized enteral nutrition, with subsequent transitions to home-based services coordinated by hospital-affiliated programs. Nonetheless, specialty clinics including rare disease centers, pediatric motility clinics, and allergy-gastroenterology joint practices represent the fastest-growing end-user segment as follow-up care, biologic infusions, and advanced dietary management increasingly shift to ambulatory environments to improve patient convenience and reduce costs.

Regional Insights

North America Rare Gastrointestinal Diseases Treatment Market Trends and Insights

North America holds a leading position in the rare gastrointestinal diseases treatment market, supported by advanced healthcare infrastructure, strong research capabilities, and the presence of specialized treatment centers. The region benefits from high awareness and early diagnosis of rare gastrointestinal disorders such as short bowel syndrome and eosinophilic gastrointestinal diseases. In addition, supportive regulatory frameworks, including orphan drug incentives and accelerated approval pathways from the U.S. Food and Drug Administration, encourage pharmaceutical companies to develop innovative therapies for rare conditions.

Increasing investment in biotechnology research and the presence of well-established pharmaceutical companies further strengthen market growth. The adoption of targeted biologics, advanced nutritional therapies, and personalized treatment approaches has improved disease management outcomes. Moreover, strong reimbursement systems and access to specialized healthcare services enable patients to receive high-cost therapies and long-term care. Continuous clinical research, collaborations between academic institutions and pharmaceutical firms, and growing patient advocacy initiatives are also contributing to the expansion of treatment options and improving the overall management of rare gastrointestinal diseases across the region.

Asia Pacific Rare Gastrointestinal Diseases Treatment Market Trends and Insights

Asia Pacific is emerging as a significant region in the Rare Gastrointestinal Diseases Treatment Market due to improving healthcare infrastructure, rising awareness of rare diseases, and increasing investment in advanced medical research. Countries such as China, India, Japan, and South Korea are witnessing growing demand for specialized therapies as diagnosis rates for conditions like short bowel syndrome and eosinophilic gastrointestinal disorders gradually improve. Governments across the region are introducing supportive policies and rare disease programs to encourage early detection and treatment.

Expanding healthcare spending and the rapid growth of the biotechnology and pharmaceutical industries are also contributing to market development. In addition, multinational companies are increasingly investing in clinical trials and partnerships with regional healthcare institutions to expand their presence in the Asia Pacific. Improvements in hospital infrastructure, access to advanced biologic therapies, and the gradual development of reimbursement frameworks are further supporting treatment adoption. With a large patient population and expanding research initiatives, the region is expected to experience steady growth in the coming years.

Competitive Landscape

The rare gastrointestinal diseases treatment market features a moderately competitive landscape driven by continuous innovation and increasing focus on orphan drug development. Market participants are prioritizing research and development to introduce targeted therapies, advanced biologics, and specialized nutritional treatments for rare gastrointestinal disorders. Strategic collaborations, clinical trials, and regulatory incentives for rare disease therapies are further supporting product development and market expansion. Companies are also focusing on expanding treatment accessibility through improved diagnostic tools and patient support programs. In addition, advancements in biotechnology and personalized medicine are creating new opportunities for more effective and disease-specific therapies.

Key Developments:

- In January 2026, Researchers from University College London and Great Ormond Street Hospital developed the first lab-grown “mini-stomach” that replicates the key structural and functional regions of the human stomach. The pea-sized organoid, called a multi-regional assembloid, combined three major stomach regions, the fundus, body, and antrum, grown from patient stem cells and assembled into a single model that could communicate internally and even produce stomach acid similar to a real organ.

- In February 2026, Biodexa Pharmaceuticals PLC, a clinical-stage biopharmaceutical company focused on developing innovative therapies for rare diseases with a growing emphasis on treatments for gastrointestinal cancers, added a new Phase 1-ready candidate to its portfolio aimed at targeting gastrointestinal stromal tumors (GIST).

- In April 2025, Ironwood Pharmaceuticals, Inc., following a recent discussion with the U.S. Food and Drug Administration, a confirmatory Phase 3 clinical trial would be required to support the approval of apraglutide for the treatment of patients with short bowel syndrome with intestinal failure who are dependent on parenteral support.

Companies Covered in Rare Gastrointestinal Diseases Treatment Market

- Takeda Pharmaceutical Company

- Nestlé Health Science

- Mirum Pharmaceuticals

- Recordati Rare Diseases

- Zealand Pharma

- Ironwood Pharmaceuticals

- Jaguar Health

- Lexicon Pharmaceuticals

- Alexion Pharmaceuticals

- AbbVie

- Pfizer

- Sanofi

- Regeneron Pharmaceuticals

- SOBI

- Fresenius Kabi

- Baxter International

Frequently Asked Questions

The global rare gastrointestinal diseases treatment market is expected to reach around US$ 2.3 billion in 2026.

Key demand drivers include rising prevalence and improved detection of SBS, EGIDs, Hirschsprung’s disease, and CIPO, the growing availability of orphan-designated drugs such as GLP-2 analogs and biologics, and expanding access to advanced medical nutrition and home-based intestinal rehabilitation programs.

North America is the leading regional market, supported by strong FDA orphan-drug policies, high prevalence and diagnosis rates of EGIDs, mature home parenteral nutrition infrastructure, and early adoption of innovative therapies such as GATTEX® (teduglutide) and investigational glepaglutide.

A major opportunity lies in developing integrated care models that combine biologics for EGIDs, GLP-2 analogs for SBS, and advanced peptide-based and amino acid-based nutrition into coordinated home-care pathways, enabled by telehealth and rare disease networks to reduce hospitalizations and improve long-term outcomes.

Leading companies include Takeda Pharmaceutical Company, Nestlé Health Science, Zealand Pharma, Recordati Rare Diseases, Jaguar Health, Lexicon Pharmaceuticals, Alexion Pharmaceuticals, AbbVie, Pfizer, and Sanofi, alongside specialized nutrition and rare-disease players such as Fresenius Kabi, Baxter International, and SOBI.