- Pharmaceuticals

- Pulmonary Fibrosis Treatment Market

Pulmonary Fibrosis Treatment Market Size, Share, Growth, and Regional Forecast, 2025 to 2032

Pulmonary Fibrosis Treatment Market by Drug (Pirfenidone, Nintedanib, Others), Route of Administration (Oral , Injectable), Indication (Idiopathic Pulmonary Fibrosis (IPF), Progressive Pulmonary Fibrosis (PPF), Others), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) , and Regional Analysis from 2025 to 2032

Pulmonary Fibrosis Treatment Market Share and Trends Analysis

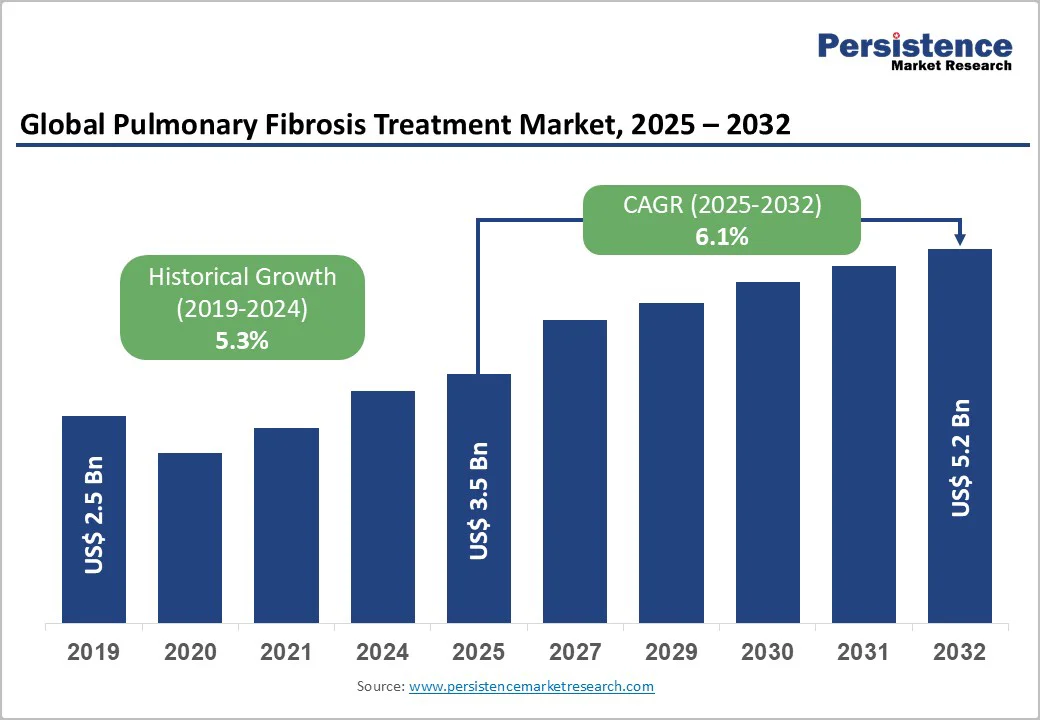

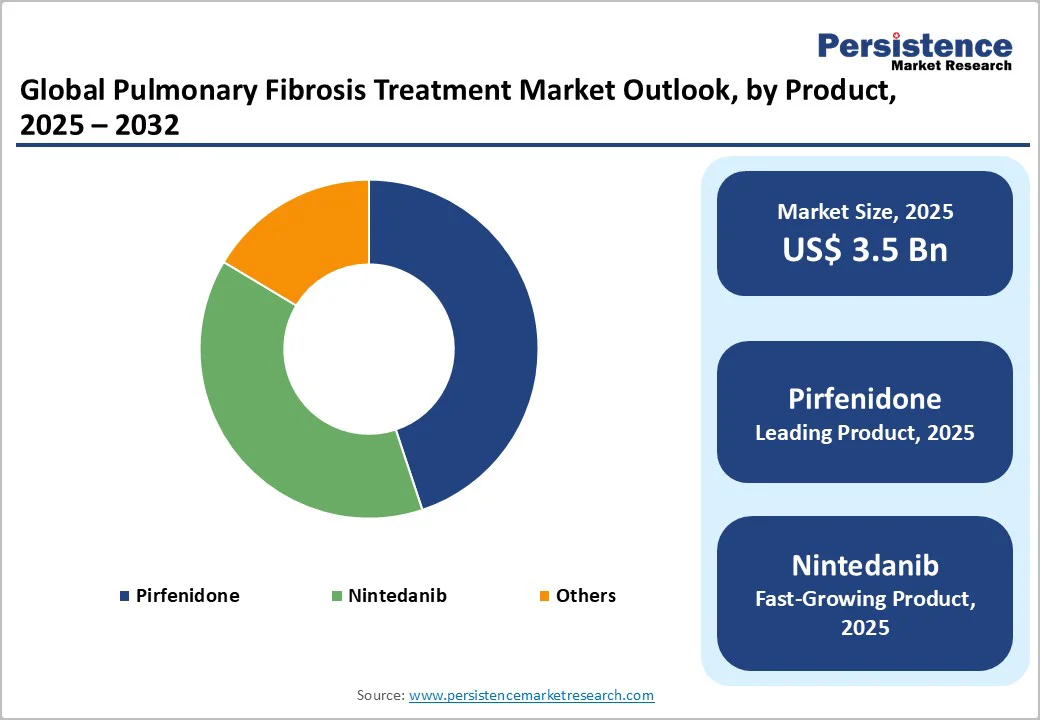

The global pulmonary fibrosis treatment market size is estimated to grow from US$3.5 billion in 2025 and is projected to reach US$5.2 billion at a CAGR of 6.1% during the forecast period from 2025 to 2032.

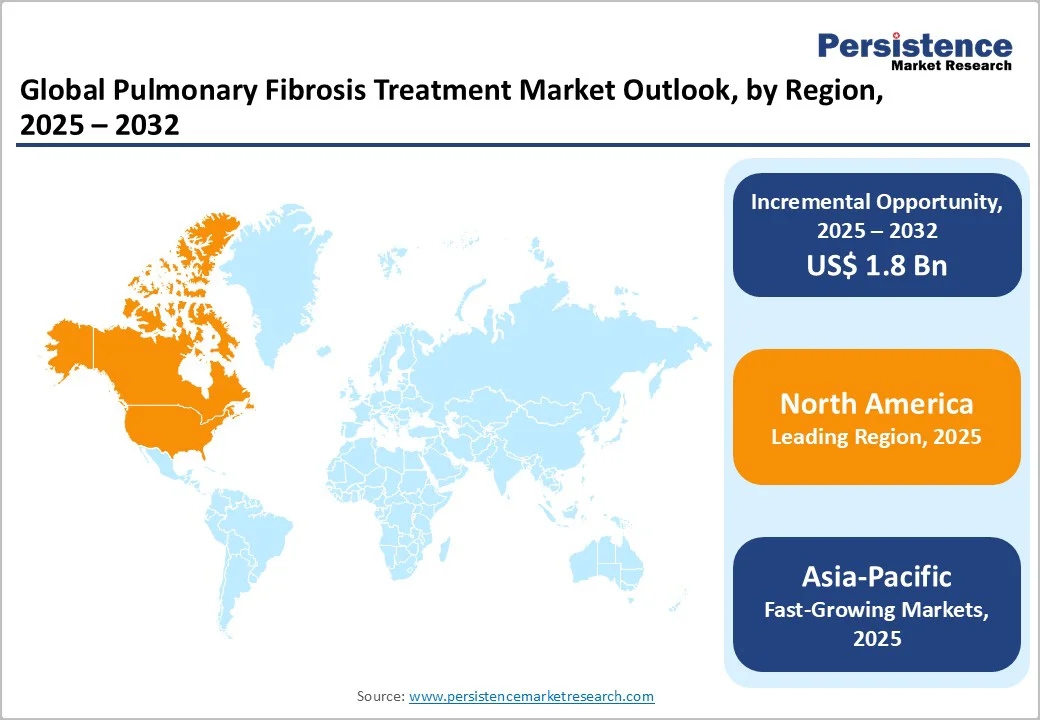

The global pulmonary fibrosis treatment industry is growing steadily, driven by increasing cases of idiopathic and progressive pulmonary fibrosis, rising disease awareness, and advancements in antifibrotic therapies. North America dominates due to strong infrastructure and reimbursement support, while Asia-Pacific is the fastest-growing region, propelled by higher healthcare spending and expanding pulmonary care access.

Key Industry Highlights

- Dominant Drug: Pirfenidone holds about 44.9% share of the Pulmonary Fibrosis Treatment Market, favored for its proven efficacy, safety, and oral convenience. It remains the primary therapy for idiopathic pulmonary fibrosis across major global markets.

- Dominant Route of Administration: Oral drugs account for around 75.4% share, driven by the popularity of antifibrotics like pirfenidone and nintedanib. Their ease of administration, improved compliance, and wide availability support long-term management of pulmonary fibrosis.

- Dominant Region: North America, accounting for approximately 41.0% of global revenue, leads the market owing to advanced diagnostic capabilities, established reimbursement systems, high adoption of approved therapies, and a strong presence of key pharmaceutical manufacturers and research institutes.

- Investment Plans: Asia-Pacific is witnessing rapid growth, supported by rising healthcare spending, the expansion of pulmonary specialty centers, increasing awareness of interstitial lung diseases, and growing investments from global and local drug makers in clinical trials and manufacturing capacity.

- Market Drivers: Rising prevalence of idiopathic pulmonary fibrosis and other chronic lung disorders, growing geriatric population, favorable government initiatives for rare disease management, and ongoing R&D in targeted and combination therapies.

- Market Opportunity: Development of next-generation antifibrotic agents with improved tolerability, advancement in inhaled and combination formulations, partnerships between pharma firms and research institutes, and expansion into emerging markets with limited access to advanced pulmonary care.

| Global Market Attributes | Key Insights |

|---|---|

| Global Pulmonary Fibrosis Treatment Market Size (2025E) | US$3.5 Bn |

| Market Value Forecast (2032F) | US$5.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.3% |

Market Dynamics

Driver - Rising Drug Approvals and Launches

Rising approvals of new drugs and product launches are significantly driving the growth of the Pulmonary Fibrosis Treatment Market. The U.S. FDA’s approval of pirfenidone and nintedanib in 2014 marked a major advancement, offering the first effective therapies to slow disease progression in idiopathic pulmonary fibrosis (IPF).

In 2020, nintedanib received expanded FDA approval for treating chronic fibrosing interstitial lung diseases (ILDs) with a progressive phenotype, widening its patient base. According to the National Institutes of Health (NIH), pulmonary fibrosis affects over 200,000 Americans, creating a growing demand for effective therapies.

Continuous R&D efforts have led to the development of next-generation antifibrotics and combination regimens aimed at improving efficacy and tolerability. Additionally, accelerated regulatory pathways, such as the FDA’s Fast Track and Orphan Drug Designation, have encouraged pharmaceutical companies to innovate and bring advanced therapies to market more quickly, thereby propelling overall market expansion and treatment accessibility.

Restraints - Limited Treatment Options & Comorbidities Interfering with Treatment

The pulmonary fibrosis treatment market faces major restraints due to limited therapeutic options and the high prevalence of comorbidities among patients. According to the National Heart, Lung, and Blood Institute (NHLBI), there is currently no cure for idiopathic pulmonary fibrosis (IPF), and existing drugs like pirfenidone and nintedanib only slow disease progression.

A Korean national cohort (2011 - 2019) reported an increase in IPF prevalence from 7.5 to 23.2 per 100,000, underscoring rising unmet need. Comorbidities further complicate management. Studies show that over 91% of IPF patients have at least one comorbidity, while 37.8% present with four or more, including hypertension, gastroesophageal reflux disease (70.8%), and dyslipidemia (62.9%).

These conditions increase mortality and limit tolerance to antifibrotic therapy. Moreover, drug side effects such as liver toxicity and gastrointestinal distress often lead to treatment discontinuation. Together, these factors hinder therapeutic efficacy, elevate healthcare costs, and restrict the overall growth of the pulmonary fibrosis treatment market.

Opportunity - Expansion of Inhaled and Combination Therapies

The expansion of inhaled and combination therapies presents a significant growth opportunity in the pulmonary fibrosis treatment market. Inhaled formulations deliver the drug directly to lung tissue, enhancing local efficacy while minimizing systemic side effects often seen with oral antifibrotics.

According to the National Institutes of Health (NIH), idiopathic pulmonary fibrosis (IPF) affects about 100,000 people in the U.S., with around 30,000 new cases annually, underscoring the need for safer long-term therapies. Current trials, such as those evaluating inhaled pirfenidone (AP01) and dry-powder nintedanib, show promise in improving tolerability and patient adherence.

The FDA’s growing interest in combination therapies, integrating antifibrotic and anti-inflammatory drugs, further strengthens this opportunity. By enabling synergistic effects and individualized dosing, these approaches could expand treatment eligibility, delay disease progression, and improve patient outcomes, particularly in moderate-to-severe cases where monotherapy has limited benefit.

This shift marks a pivotal step toward more effective and tolerable management of pulmonary fibrosis.

Category-wise Analysis

By Drug, Pirfenidone Dominates the Pulmonary Fibrosis Treatment Market

The Pirfenidone dominates the market with a 44.9% share in 2025, due to its proven clinical efficacy, early regulatory approvals, and strong physician preference. Studies published by the National Institutes of Health (NIH) and PubMed Central show that pirfenidone significantly slows the decline in forced vital capacity (FVC) and reduces disease progression in patients with idiopathic pulmonary fibrosis (IPF).

Approved first in Japan (2008) and later in the U.S. (2014) and EU (2011), pirfenidone gained a strong global foothold as the first antifibrotic with established long-term survival benefits. Its oral formulation ensures better patient compliance and accessibility. Combined with widespread generic availability, pirfenidone remains the most prescribed therapy for IPF, reinforcing its dominant market position over newer or adjunctive treatment options.

By Route of Administration, Oral is gaining traction due to its convenience, proven efficacy, and preference for long-term outpatient management of pulmonary fibrosis.

Oral administration dominates the pulmonary fibrosis treatment market as both key antifibrotic drugs, Pirfenidone and Nintedanib, are available in oral formulations, ensuring convenience and adherence for long-term use. According to the Pulmonary Fibrosis Foundation, these medications are taken two to three times daily and have demonstrated significant clinical benefits in slowing lung function decline.

Clinical trials reported that Pirfenidone reduced the decline in forced vital capacity (FVC) by 47.9%, while Nintedanib reduced it by 68.4% compared to placebo. Oral drugs are preferred for outpatient management, minimizing the need for hospital visits and invasive procedures. Their proven efficacy, ease of dosing, and inclusion in international treatment guidelines make oral administration the leading route in pulmonary fibrosis therapy.

Regional Insights

North America Pulmonary Fibrosis Treatment Market Trends

North America dominates the pulmonary fibrosis treatment market with 41.0% share in 2025, due to its high disease prevalence, advanced healthcare infrastructure, and strong access to approved therapies. In the U.S. alone, idiopathic pulmonary fibrosis (IPF) affects around 100,000 people, with nearly 30,000-40,000 new cases diagnosed each year, according to the Pulmonary Fibrosis Foundation.

Studies published in the American Journal of Respiratory and Critical Care Medicine estimate IPF prevalence in North America at 2.4-2.98 per 10,000 persons, higher than in other regions.

The region’s leadership is further supported by widespread adoption of high-resolution CT imaging, pulmonary function testing, and favorable reimbursement for antifibrotic drugs like pirfenidone and nintedanib. These factors collectively make North America the leading region in the adoption and innovation of pulmonary fibrosis treatments.

Europe Pulmonary Fibrosis Treatment Market Trends

Europe is one of the leading regions in the pulmonary fibrosis treatment market, driven by its strong clinical infrastructure, early adoption of antifibrotic drugs, and coordinated rare disease management. The prevalence of idiopathic pulmonary fibrosis (IPF) in Europe ranges between 1.25 and 23.4 cases per 100,000 population, with mortality rates reaching 3.9 per 100,000 person-years across 24 EU nations from 2013-2018.

According to the European Respiratory Journal, cases are steadily increasing, reflecting greater diagnostic awareness and an aging population. The European Union was also among the first to approve Pirfenidone in 2011, establishing early access to proven therapies. Combined with robust reimbursement systems and multidisciplinary pulmonary care centers, these factors solidify Europe’s strong leadership in pulmonary fibrosis management.

Asia-Pacific Pulmonary Fibrosis Treatment Market Trends

Asia-Pacific is the fastest-growing region in the pulmonary fibrosis treatment market, driven by an expanding elderly population, improved diagnostic capabilities, and rising healthcare investments. According to a meta-analysis published in the European Respiratory Journal, the adjusted prevalence of idiopathic pulmonary fibrosis (IPF) in Asia-Pacific can reach up to 4.51 cases per 10,000 persons, higher than Europe’s 0.33-2.51 per 10,000.

Countries like Japan, China, and South Korea are leading in early diagnosis through advanced imaging and screening programs. Japan, in particular, has one of the world’s highest IPF incidence rates due to its aging population. Additionally, increasing the number of clinical trials, government support for rare disease management, and faster access to antifibrotic drugs are propelling the region’s rapid market growth and treatment adoption.

Market Competitive Landscape

Leading companies in the pulmonary fibrosis treatment market are prioritizing innovation, regulatory approvals, and strategic collaborations. They are developing advanced antifibrotic and inhaled formulations, expanding clinical trials, and strengthening global reach through partnerships and acquisitions. These efforts aim to enhance treatment efficacy, improve patient compliance, and address unmet needs in pulmonary fibrosis management.

Key Industry Developments:

- In November 2025, The U.S. Food and Drug Administration (FDA) approved a phosphodiesterase-4 (PDE4) inhibitor for the treatment of idiopathic pulmonary fibrosis (IPF), marking a major advancement in managing this chronic and progressive lung disease. The approval provided a new therapeutic option after more than a decade dominated by antifibrotic agents like pirfenidone and nintedanib. Clinical studies showed that the PDE4 inhibitor significantly slowed lung function decline and reduced disease progression in IPF patients.

- In October 2025, The U.S. Food and Drug Administration (FDA) approved Boehringer Ingelheim’s JASCAYD® (nerandomilast tablets) as the first new treatment for adults with idiopathic pulmonary fibrosis (IPF) in more than a decade. The approval marked a major milestone in pulmonary fibrosis care, expanding therapeutic options beyond existing antifibrotic drugs such as pirfenidone and nintedanib.

Companies Covered in Pulmonary Fibrosis Treatment Market

- F. Hoffman - La Roche Ltd.

- Boehringer Ingelheim

- International GmbH

- Cipla Ltd

- MediciNova, Inc.

- Intas Pharmaceuticals Ltd.

- Others

Frequently Asked Questions

The global pulmonary fibrosis treatment market is projected to be valued at US$ 3.5 Bn in 2025.

Rising prevalence of idiopathic pulmonary fibrosis, growing awareness, improved diagnostics, and advancements in antifibrotic and targeted drug therapies drive market growth.

The global pulmonary fibrosis treatment market is poised to witness a CAGR of 6.1% between 2025 and 2032.

Development of inhaled and combination therapies, biomarker-based precision medicine, and expansion in emerging markets offer major growth opportunities.

F. Hoffman - La Roche Ltd., Boehringer Ingelheim, International GmbH, Cipla Ltd, MediciNova, Inc.