- Medical Devices

- Transcatheter Pulmonary Valve Market

Transcatheter Pulmonary Valve Market Size, Share, and Growth Forecast, 2026 – 2033

Transcatheter Pulmonary Valve Market by Procedure Type (Valve-in-Valve, Native Outflow Tract), Technology Type (Balloon-expandable, Self-expanding), Application (Pulmonary Regurgitation, Pulmonary Stenosis, Mixed Disease), and Regional Analysis 2026 – 2033

Transcatheter Pulmonary Valve Market Size and Trends Analysis

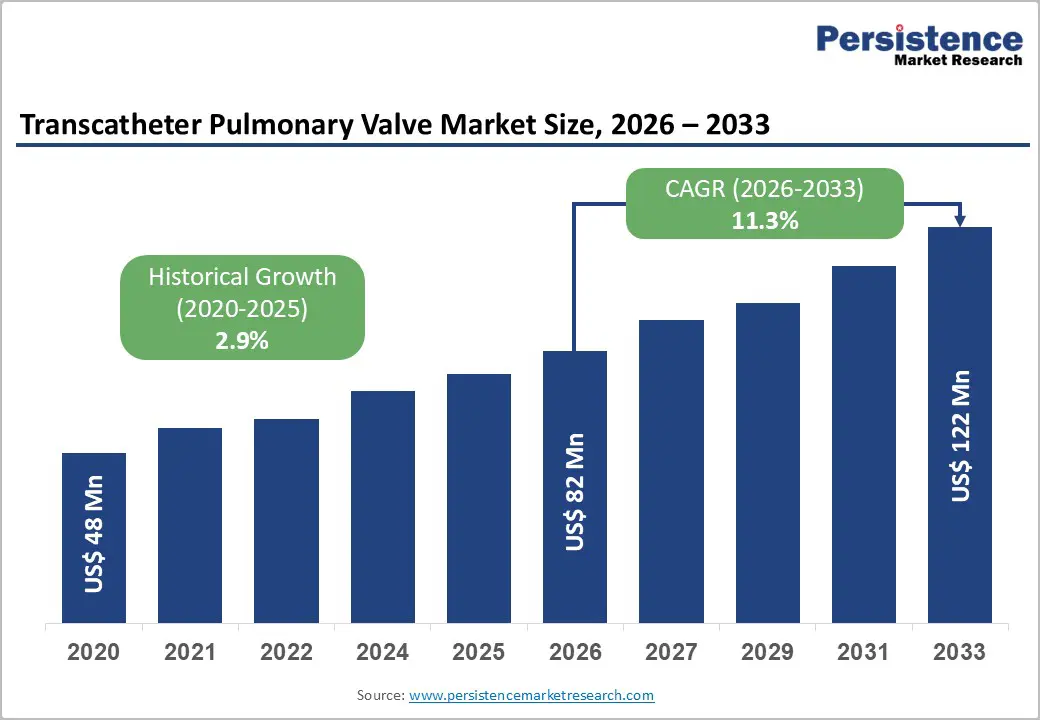

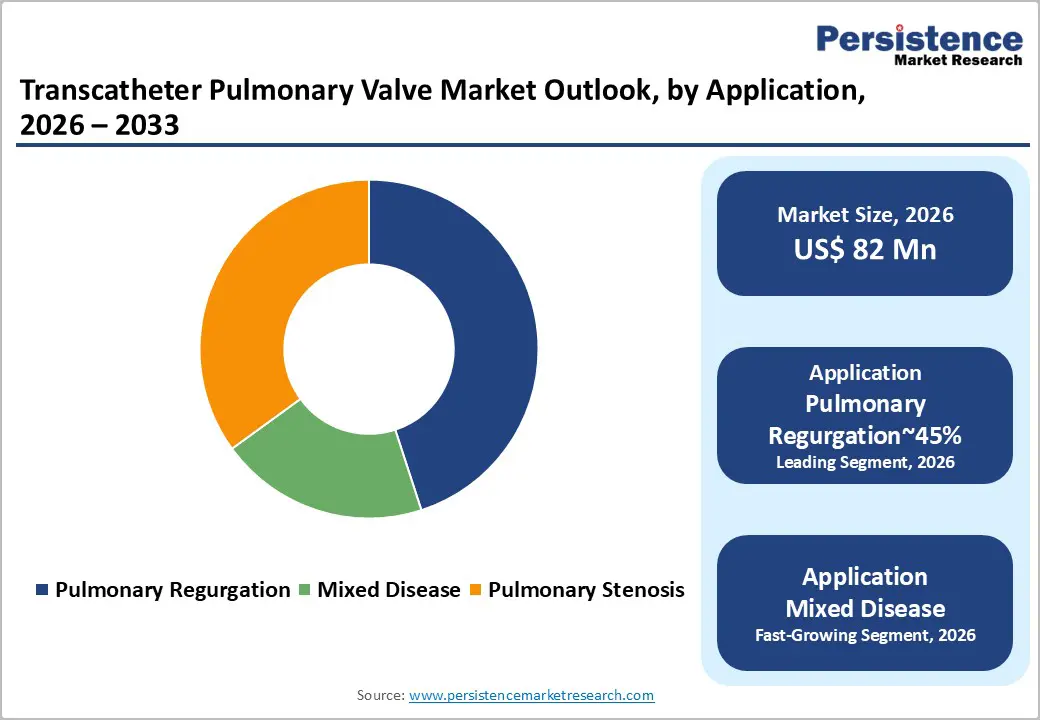

The global transcatheter pulmonary valve market size is likely to be valued at US$82 million in 2026 and is expected to reach US$122 million by 2033, growing at a CAGR of 5.8% during the forecast period from 2026 to 2033.

The market is undergoing a significant pivot from niche "valve-in-valve" procedures toward broader indications involving native right ventricular outflow tracts (RVOT). This expansion is primarily driven by the rising adult congenital heart disease (ACHD) population requiring re-interventions and the commercial approval of next-generation self-expanding valve systems. Key factors include advanced imaging integration and expanding adult congenital patient pools, supported by clinical evidence of reduced recovery times.

Key Industry Highlights:

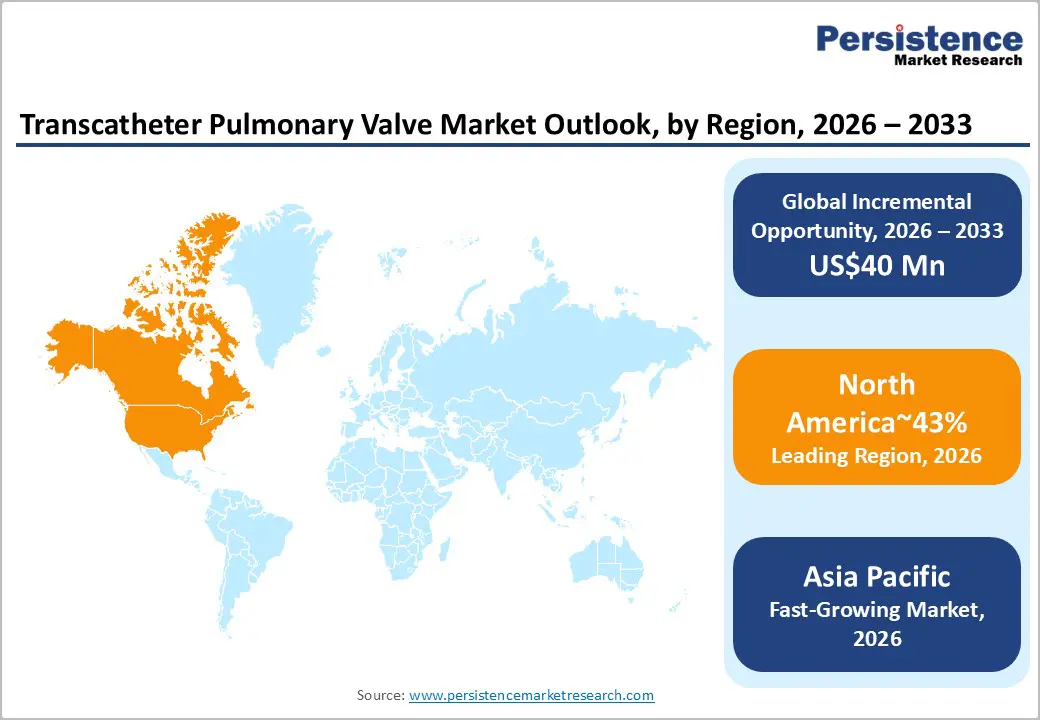

- Leading Region: America is anticipated to lead with around 43% share, supported by early technology adoption, strong structural heart reimbursement frameworks, concentration of specialized cardiac centers, and rapid uptake of newly approved TPV platforms.

- Leading Procedure Type: Valve-in-valve procedures are projected to remain the leading procedure type, accounting for approximately 58% share, as a large installed base of surgically implanted pulmonary valves creates sustained demand for minimally invasive repeat interventions.

- Leading Technology Type: Balloon-expandable valves are anticipated to remain the leading technology type, holding around 63% share, as long-standing clinical validation, broad physician familiarity, and extensive procedural track records continue to reinforce their preference in routine TPV interventions.

- Leading Application: Pulmonary regurgitation is expected to remain the leading application, accounting for approximately 45% share, driven by the high prevalence of post-surgical right ventricular outflow tract dysfunction in congenital heart disease patients and the growing clinical shift toward minimally invasive valve replacement strategies.

| Global Market Attributes | Key Insights |

|---|---|

| Transcatheter Pulmonary Valve Market Size (2026E) | US$82 Mn |

| Market Value Forecast (2033F) | US$122 Mn |

| Projected Growth (CAGR 2026 to 2033) | 11.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Prevalence of Adult Congenital Heart Disease (ACHD)

The growing population of adults with repaired congenital heart defects, particularly Tetralogy of Fallot, is driving demand for pulmonary valve and right ventricular outflow tract (RVOT) interventions. Advances in pediatric cardiac surgery and improved long-term survivorship have shifted the burden of care from pediatric to adult cardiology, creating a predictable treatment cycle within specialized adult congenital heart disease (ACHD) centers. A significant portion of congenital heart disease patients present with RVOT anatomical abnormalities, which lead to pulmonary regurgitation and progressive right ventricular dysfunction as they age. This transition from corrective surgery in childhood to recurrent valve management in adulthood expands the patient pool for pulmonary valve interventions.

Biological pulmonary valves have finite durability and require reintervention over time, leading to an increasing demand for secondary and tertiary pulmonary valve replacements, both surgically and via transcatheter approaches. As ACHD care pathways formalize and adult congenital programs expand, diagnosis, follow-up, and referral rates improve. This establishes a recurring demand cycle for valve replacement technologies. Medtronic’s CE Mark approval for the Harmony TPV system in January 2025 expands minimally invasive treatment options for patients with severe pulmonary regurgitation in Europe. This innovation promises reduced open-heart surgeries and improved quality of life, reinforcing the ongoing need for pulmonary valve replacement in the ACHD population.

Accelerating Demand for Minimally Invasive Transcatheter Pulmonary Valve Procedures

The growing preference for minimally invasive transcatheter pulmonary valve (TPV) interventions is reshaping the pulmonary valve and RVOT treatment landscape. Compared to repeat open-heart surgery, TPV procedures offer shorter hospital stays, faster recovery, and lower perioperative risks, particularly for adult congenital heart disease (ACHD) patients requiring multiple lifetime interventions. High short-term durability and hemodynamic performance have boosted physician confidence in catheter-based approaches, while device refinements have broadened anatomical eligibility across native and conduit-based RVOT anatomies. Regulatory approvals and product relaunches by leading manufacturers have further cemented TPV as a frontline reintervention strategy in tertiary care centers.

From a health system perspective, TPV solutions align with cost-containment objectives by reducing total episode-of-care costs and intensive care utilization, presenting favorable economic value for payers and providers. The simplicity and reproducibility of balloon-expandable and self-expanding valve platforms are enabling growth beyond traditional surgical centers, expanding into high-throughput catheterization labs and select ambulatory settings. Superior recovery profiles, expanded clinical validation, and cost efficiencies are driving increased TPV adoption and procedural volume growth in RVOT interventions.

Barrier Analysis - Anatomical Heterogeneity and Device Sizing Constraints in RVOT Interventions

Despite continuous innovation in transcatheter pulmonary valve (TPV) platforms, the extreme anatomical variability of the right ventricular outflow tract (RVOT) limits patient eligibility. RVOT geometries are highly irregular due to congenital malformations, prior surgeries, patch augmentations, and conduit degeneration, often exceeding the size limits of off-the-shelf valve systems or exhibiting non-cylindrical shapes that hinder anchoring stability. For these patients, clinicians often resort to open surgery or complex hybrid strategies, which increases procedural complexity and slows the adoption of fully percutaneous solutions.

Clinical risks in complex RVOT cases further hinder adoption. Irregular landing zones raise the likelihood of device migration, malposition, and paravalvular leaks, potentially compromising hemodynamic outcomes and requiring reintervention. This "clinical hesitation" threshold is more pronounced in borderline anatomies, where procedural predictability is lower. Unlike the more standardized aortic valve ecosystem, the pulmonary valve market lacks uniformity and mature sizing algorithms, making procedural reproducibility challenging. Until more adaptable valve designs and patient-specific solutions become clinically scalable, anatomical variability will continue to limit procedural volumes and hinder the rapid adoption seen in TAVR for aortic valves.

Opportunity Analysis - Integration of AI-Driven Sizing and Procedural Planning

The integration of AI-enabled sizing, 3D computational modeling, and virtual fit-testing into pre-procedural planning offers a transformative opportunity to reduce procedural risks in transcatheter pulmonary valve (TPV) interventions. By converting heterogeneous RVOT anatomies into quantifiable digital twins, advanced imaging analytics can simulate device deployment, anchoring behavior, and post-implant hemodynamics. This enables precise pre-validation of device selection, optimizing landing zone strategies, and anticipating failure modes such as malapposition or paravalvular leak. As procedural outcomes become more predictable, vendors can differentiate based on clinical confidence and planning support, rather than just device hardware, thus boosting physician preference and accelerating adoption.

AI-driven planning directly addresses the core challenge of anatomical variability, expanding eligibility to previously excluded “borderline” patient cohorts. Virtual fit-testing can de-risk cases that would otherwise require surgical or hybrid approaches, enhancing percutaneous solutions while reducing procedure iteration and reintervention risk. From a commercial perspective, this planning capability strengthens customer lock-in, shifting competition toward outcome assurance rather than price. As regulatory bodies and payers prioritize safety, reproducibility, and value-based outcomes, AI-driven planning platforms unlock incremental procedure volumes and improve conversion rates. The anticipated December 2025 publication by the National Institutes of Health underscores the growing importance of advanced modeling and predictive simulation for enhancing procedural predictability and patient safety in TPV interventions.

R&D Collaborations for Next-Generation Transcatheter Valves

Strategic R&D collaborations between device manufacturers, academic centers, and clinical consortia are crucial for accelerating next-generation transcatheter pulmonary valve innovation. Programs such as PROTEUS IDE demonstrate how shared clinical data, iterative prototyping, and early physician feedback enhance design relevance for complex RVOT anatomies.

Emphasis on tissue-engineered and bioadaptive materials is driven by the need for improved durability, hemocompatibility, and long-term remodeling. These collaborations enable risk-sharing, earlier regulatory alignment, and improved trial design. They also advance hybrid valve systems for mixed disease profiles, expand patient pools with modular architectures, and strengthen intellectual property. As competition intensifies, sustained partnerships will be essential to delivering clinically effective valve platforms, increasing procedural volumes, and converting ineligible patients.

Category–wise Analysis

Procedure Type Insights

Valve-in-Valve (ViV) is set to dominate the Transcatheter Pulmonary Valve (TPV) market, capturing around 58% of the share. This is driven by the increasing number of adult congenital heart disease survivors with failing surgical bioprostheses transitioning to catheter-based reintervention. ViV is favored in clinical centers due to predictable anatomy, established workflows, and compatibility with devices such as Medtronic Melody, Harmony TPV, Edwards Lifesciences SAPIEN 3 Ultra, and Abbott’s Navitor.

These devices streamline case planning and inventory, while advanced CT-driven sizing, fusion imaging, and procedural simulation software enhance landing-zone predictability and reduce coronary obstruction risks. High procedural success, shorter recovery times, and the use of next-generation tissue treatments, including Edwards RESILIA, reinforce ViV’s position as the default for repeat pulmonary valve interventions.

The Native Outflow Tract (NOT) segment is expected to grow rapidly, fueled by self-expanding frames and adaptive docking systems that enable treatment of large, irregular RVOT anatomies. Devices such as Medtronic Harmony TPV, Edwards SAPIEN 3 with Alterra, and Venus Medtech’s VenusP-Valve expand native tract coverage and support more patient-specific treatment.

Technologies, including 3D modeling, pre-stenting, and fusion imaging, improve anchoring precision and reduce migration risks. The shift toward minimally invasive management in Tetralogy of Fallot patients and increasing confidence in native-tract durability will drive rapid procedural growth in high-volume centers.

Technology Type Insights

Balloon-expandable (BE) technology is projected to maintain dominance in the Transcatheter Pulmonary Valve (TPV) market, holding around 63% market share. This is driven by its predictable deployment, high radial strength, and familiarity with valve-in-valve procedures. Edwards Lifesciences leads this segment with the SAPIEN 3 and SAPIEN 3 Ultra valves, featuring RESILIA tissue, alongside the Alterra Adaptive Prestent, expanding use in larger right ventricular outflow tracts (RVOTs).

Medtronic’s Melody TPV is favored for smaller conduits and redo cases. Emerging technologies such as Andramed’s Andra Valve are designed for larger diameters with cobalt-chromium frames, offering better circularity retention. Enhanced delivery systems and minimalist cath-lab protocols are expected to improve procedure efficiency and control.

Self-expanding (SE) technology is the fastest-growing segment, driven by the need to treat native outflow tracts in addition to conduit cases. Medtronic’s Harmony TPV is gaining traction in larger, compliant RVOTs, while Venus Medtech’s VenusP-Valve is expanding its reach in Asia and Europe for tapered anatomies.

Low-profile delivery systems and advanced nitinol frames enhance performance in smaller patients and dynamic vessels. As native-tract procedures expand in structural heart programs, SE technologies are set to capture a larger share of the market by offering a solution for anatomies where BE systems may struggle.

Regional Insights

North America Transcatheter Pulmonary Valve Market Trends

North America is projected to maintain its position as the leading region in the Transcatheter Pulmonary Valve (TPV) market, accounting for approximately 43% of the global share. This dominance is supported by a highly developed structural heart care infrastructure, early adoption of minimally invasive valve therapies, and favorable reimbursement policies for FDA-approved indications. The region benefits from a dense network of tertiary cardiac centers, widespread hybrid catheterization labs, and established referral pathways for managing congenital heart disease across both pediatric and adult populations.

Clinical demand is driven by a growing adult congenital heart disease (ACHD) patient population requiring repeat pulmonary valve interventions, alongside a shift toward catheter-based procedures due to their lower perioperative burden and quicker recovery. Regulatory frameworks, particularly accelerated review pathways for novel valve designs, are likely to fuel innovation, with a focus on enhancing durability, anti-calcification properties, and mitigating endocarditis risks.

Technology vendors are increasingly integrating advanced imaging, procedural planning software, and precision delivery systems to optimize placement accuracy, especially in complex right ventricular outflow tract anatomies. The U.S. will continue to lead market performance, bolstered by a robust congenital heart disease care system, high-volume structural heart centers, and strong payer coverage. Canada is expected to see gradual TPV adoption, driven by centralized provincial cardiac programs aimed at reducing repeat surgeries and improving access to minimally invasive valve replacements. The region’s growth is further supported by the clinical trend toward lifetime valve management strategies and continued device innovation.

Europe Transcatheter Pulmonary Valve Market Trends

Europe is expected to maintain a key position in the global Transcatheter Pulmonary Valve (TPV) market due to its deep clinical expertise, extensive network of tertiary cardiac centers, and strong research collaborations between hospitals and device manufacturers. The market will be influenced by the transition to stricter regulatory frameworks under the Medical Device Regulation (MDR), impacting product launches, clinical evidence requirements, and portfolio prioritization by manufacturers. The growing adoption of lifetime valve management strategies in adult congenital heart disease care is expected to further fuel demand.

As Heart Team models become more institutionalized, the region is likely to see continued procedural migration toward minimally invasive valve replacements, with a focus on refining delivery systems, imaging-guided planning, and addressing complex right ventricular outflow tract anatomies in both native and enlarged tracts.

Germany is expected to be the hub of technology adoption, supported by its high-volume transcatheter ecosystem, advanced reimbursement structures, and active clinical trial involvement. France will remain a key reference market, driven by strong public hospital networks and early participation in European post-market surveillance. Established device platforms will continue to dominate routine practice, with self-expanding valve systems gaining traction as regulatory clarity improves for native RVOT indications. The regulatory environment is likely to favor well-capitalized firms that can meet MDR compliance and sustain long-term clinical evidence generation.

Asia Pacific Transcatheter Pulmonary Valve Market Trends

Asia Pacific is projected to be the fastest-growing region in the Transcatheter Pulmonary Valve (TPV) market, driven by rapid capacity buildout and increasing access to advanced structural heart interventions. The region’s growth is fueled by a large, untreated congenital heart disease burden, expanding cath lab and hybrid OR footprints, particularly in China and India, and the rising adoption of minimally invasive cardiology within tertiary referral networks. The demand is expected to be focused on first-time transcatheter interventions rather than replacement procedures, reflecting historically lower surgical coverage in many APAC health systems.

Market development is also influenced by the localization of device manufacturing, with region-specific valve platforms designed for native right ventricular outflow tract anatomies. Medical tourism corridors in countries, including India, Thailand, and Singapore, are channeling complex congenital heart disease cases to high-volume centers.

China is expected to be the regional market leader, driven by domestic device manufacturers, fast-track regulatory pathways, and widespread use of self-expanding TPV systems. Japan will remain a high-value market due to strong reimbursement coverage and institutional adoption of balloon-expandable valves. India, with its rapidly expanding cath lab infrastructure and cost-effective domestic TPV development, is positioned for the fastest growth in procedure volume. Australia will serve as an innovation testbed with early adoption of advanced imaging and simulation technologies. Collectively, APAC's growth is supported by cost innovation, regulatory harmonization, and expanded clinical training.

Competitive Landscape

The global transcatheter pulmonary valve market is highly consolidated, led by Medtronic, Edwards Lifesciences, and Abbott, which collectively shape technology direction, clinical adoption, and regulatory momentum through scale, deep cardiovascular portfolios, and strong physician relationships. Medtronic’s dual-portfolio strategy across native and conduit anatomies and Edwards’ platform-led approach anchored in durable tissue technology define leadership positioning, while Abbott and Boston Scientific maintain relevance through delivery-system innovation and procedural integration. Competitive power is reinforced by global distribution reach, long clinical validation cycles, and high regulatory thresholds that raise switching costs and protect incumbent positions across major care centers.

Beyond the leaders, competition is intensifying as Venus Medtech and Meril Life Sciences expand in Asia and Europe with anatomy-specific solutions, and specialized innovators pursue novel frames and bioresorbable designs. Market strategies center on next-generation durability, AI-guided imaging and planning, faster regulatory pathways, and targeted geographic expansion. Industry behavior reflects rising emphasis on platform extensibility, procedural success rates, and differentiated anatomical fit, signaling sustained competitive pressure as challengers scale and incumbents accelerate innovation to defend premium clinical segments.

Key Industry Highlights

- In January 2026, Edwards Lifesciences posted a Therapy Development Manager role focused on Transcatheter Pulmonary Valve Implantation (TPVI). This move signaled the company's continued investment in expanding the adoption of TPV therapy and enhancing physician support for the growing market.

- In January 2026, the FDA approved a PMA supplement for the Medtronic Harmony Transcatheter Pulmonic Valve System, supporting the ongoing regulatory compliance and opening the door for future labeling or design refinements. This approval was key in enhancing the product's regulatory standing and further solidifying its position in the TPV market.

- In December 2025, Edwards Lifesciences completed a pivotal clinical study on the SAPIEN XT THV in the pulmonic position. The study further contributed to the clinical evidence base for balloon-expandable TPV options, reinforcing the therapy's viability for both pediatric and adult patients with pulmonary valve issues.

Companies Covered in Transcatheter Pulmonary Valve Market

- Medtronic plc

- Edwards Lifesciences

- Abbott Laboratories

- Boston Scientific Corporation

- Venus Medtech

- Meril Life Sciences

- Micro-Port Scientific

- Andramed GmbH

- NVT AG

- Jena Valve Technology

- Xeltis

- Colibri Heart Valve

- Biotronik SE & Co. KG

- Meril Life Sciences Pvt. Ltd

- Foldax

Frequently Asked Questions

The global transcatheter pulmonary valve market is projected to be valued at US$82 million in 2026 and is expected to reach US$122 million by 2033, driven by the expanding adult congenital heart disease population and the clinical shift toward minimally invasive reinterventions.

The growing population of adults with repaired congenital heart defects, who require repeated pulmonary valve interventions over their lifetime, creates a predictable, long-term demand cycle for TPV procedures as a less invasive alternative to repeat open-heart surgery.

The transcatheter pulmonary valve market is forecast to grow at a compound annual growth rate CAGR of 5.8% from 2026 to 2033, reflecting steady adoption as technology indications expand.

North America is the leading regional market, accounting for approximately 43% share, supported by early technology adoption, strong reimbursement frameworks, a high concentration of specialized cardiac centers, and rapid uptake of newly approved TPV platforms.

The transcatheter pulmonary valve market is highly consolidated and led by Medtronic plc, Edwards Lifesciences, and Abbott Laboratories. These leaders define the competitive landscape through comprehensive portfolios, deep clinical validation, and strong physician relationships in structural heart disease.