- Pharmaceuticals

- Prostate Cancer Hormone Therapy Market

Prostate Cancer Hormone Therapy Market Size, Share, and Growth Forecast 2026 - 2033

Prostate Cancer Hormone Therapy Market by Drug Class (Androgen Receptor Inhibitors, Gonadotropin-Releasing Hormone (GnRH) Agonists, GnRH Receptor Antagonists, Anti-Androgens, Combination Therapies), Indication, Route of Administration, Sales Channel, and Regional Analysis, 2026–2033

Prostate Cancer Hormone Therapy Market Size and Trend Analysis

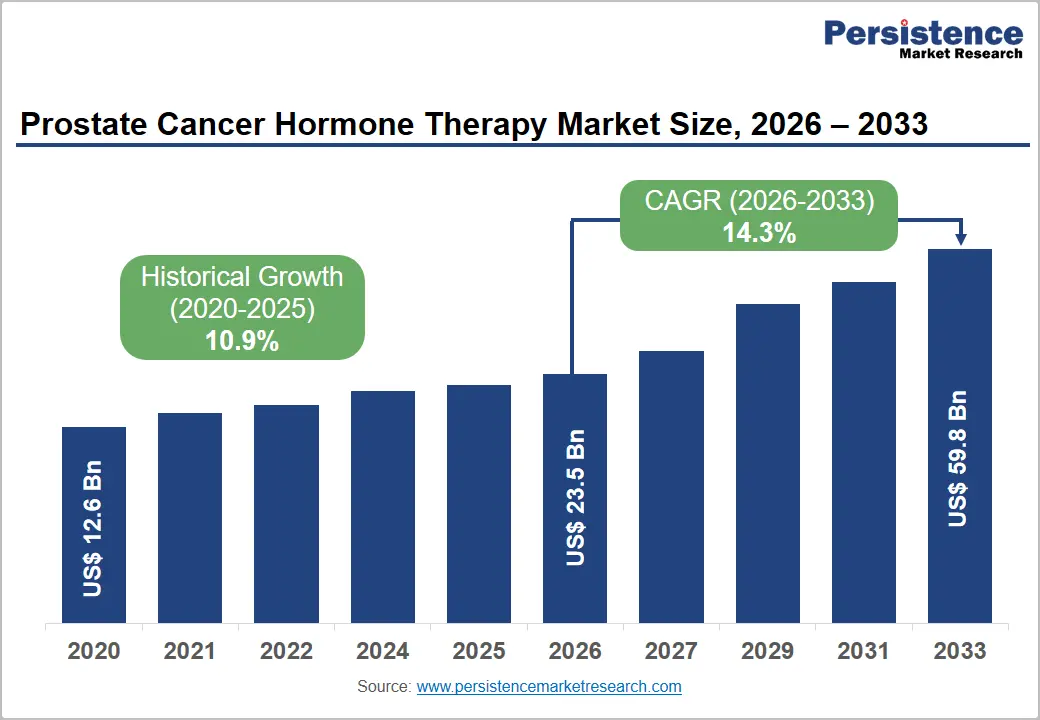

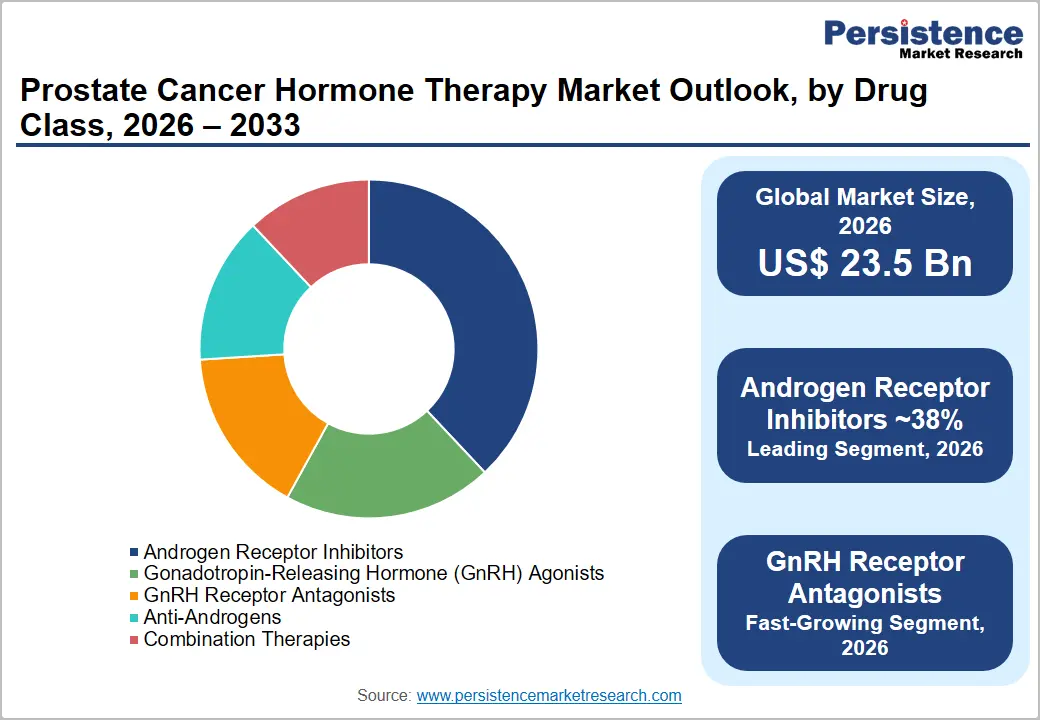

The global prostate cancer hormone therapy market size is expected to be valued at US$ 23.5 billion in 2026 and projected to reach US$ 59.8 billion by 2033, growing at a CAGR of 14.3% between 2026 and 2033. Prostate cancer is a malignant tumor that develops in the prostate gland, a small gland in men responsible for producing seminal fluid and is one of the most common cancers among men worldwide. Hormone therapy, particularly androgen deprivation therapy (ADT), remains a cornerstone in managing prostate cancer, especially in advanced stages. Increasing adoption of targeted hormone therapies and next-generation androgen receptor inhibitors is reshaping treatment protocols and improving patient outcomes. Technological advancements, favorable reimbursement policies, and expanding healthcare infrastructure in emerging economies are further fueling market growth.

Key Industry Highlights:

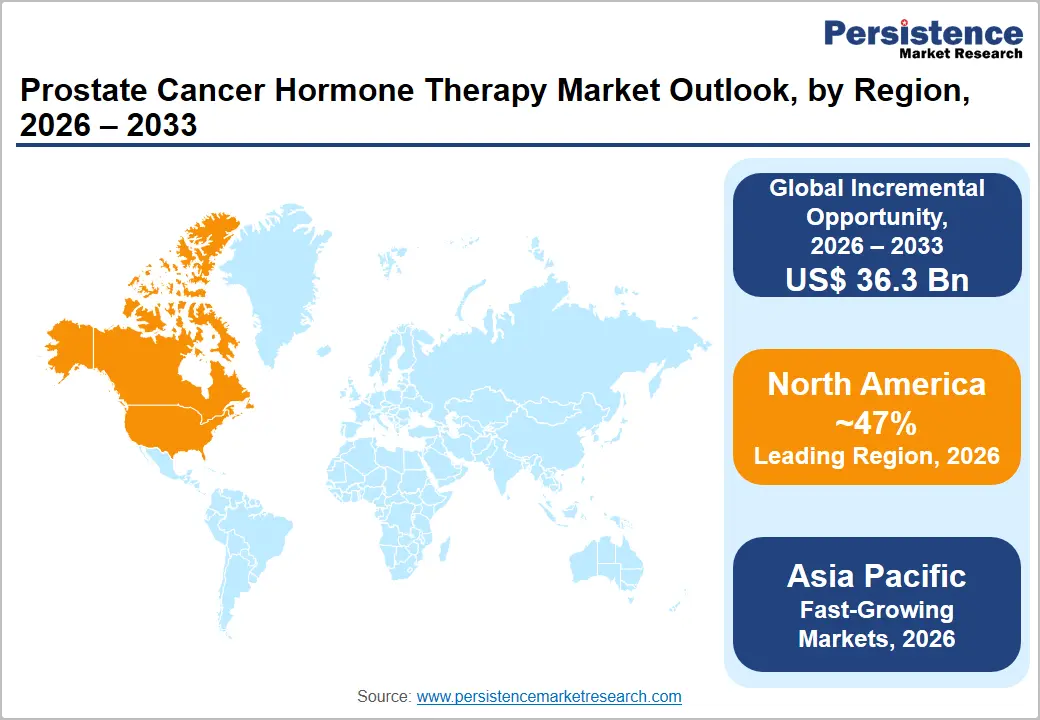

- Leading Region: North America leads the global prostate cancer hormone therapy market with 47% market share in 2025, driven by high disease prevalence, premium drug pricing, strong reimbursement frameworks, and rapid adoption of next-generation androgen receptor inhibitors across the U.S. and Canada.

- Fast-Growing Market: Asia Pacific is projected to register the highest CAGR, fueled by expanding healthcare infrastructure, improving cancer diagnostic capabilities, government reimbursement expansions, and rising prostate cancer incidence across China, India, Japan, and Southeast Asian nations.

- Dominant Segment: Androgen Receptor Inhibitors hold the leading position in the Drug Class category with 38% share in 2026, supported by multiple FDA and EMA approvals, superior clinical efficacy data, and broad adoption across mCRPC and hormone-sensitive prostate cancer indications globally.

- Fastest Growing Segment: Gonadotropin-Releasing Hormone (GnRH) Agonists represent the fastest growing drug class segment, driven by increasing combination therapy protocols, expanded indications, and growing prescriptions in emerging markets where cost-effectiveness is prioritized by clinicians and payers.

- Key Opportunity: The growing adoption of combination hormonal therapy protocols across mCRPC and mHSPC indications, supported by landmark trial evidence, is creating significant revenue expansion opportunities worth an incremental US$ 36.3 billion in absolute dollar terms between 2026 and 2033.

Market Dynamics

Drivers - The Integration of AI-Based Personalized Hormone Therapy for Prostate Cancer is Enabling Tailored Treatment Plans Based on Genetic Profiling

The increasing clinical adoption of GnRH receptor antagonists for castration-resistant prostate cancer is reshaping treatment protocols due to their rapid testosterone suppression and reduced cardiovascular risks. Physicians are favoring non-surgical hormone therapy alternatives for advanced prostate cancer, especially for elderly patients with comorbidities. This shift is supported by growing clinical data and regulatory approvals for agents such as relugolix. The demand for therapies that minimize resistance and improve tolerability is pushing pharmaceutical companies to innovate in this market.

The market is also witnessing strong momentum in oral androgen receptor inhibitors for metastatic prostate cancer therapy, which offer better patient compliance and targeted action. Drugs such as darolutamide and enzalutamide are gaining traction due to their efficacy in delaying disease progression. Moreover, the integration of AI-based personalized hormone therapy for prostate cancer is enabling tailored treatment plans based on genetic profiling, improving outcomes, and reducing adverse effects. Strategic collaborations between biotech firms and oncology centers are accelerating the development of next-generation hormone therapies with enhanced bioavailability and precision.

Restraints - The Underperformance of Therapeutic Cancer Vaccines for Metastatic Prostate Cancer Has Led to Reduced Investment, Slowing Innovation and Adoption

Immunotherapy for hormone-refractory prostate cancer has shown limited efficacy in real-world settings. Treatments such as sipuleucel-T face skepticism due to modest survival benefits and complex administration protocols. The lack of biomarkers for predicting immunotherapy response in prostate cancer further restricts its clinical utility. The underperformance of therapeutic cancer vaccines for metastatic prostate cancer has also led to reduced investment in this segment, slowing innovation and adoption.

The effectiveness of late-line hormone therapy for metastatic castration-resistant prostate cancer (mCRPC) remains a concern, especially in patients previously treated with androgen receptor inhibitors. Resistance mechanisms, such as AR splice variants, diminish the efficacy of second-generation agents. Moreover, the lack of predictive genomic profiling tools for hormone therapy response limits personalized treatment strategies. These challenges hinder the expansion of next-generation hormone therapy for advanced prostate cancer, particularly in a heavily pre-treated population.

Opportunities - The Growing Clinical Adoption of Dual-Modality Treatment Strategies Expected to Redefine Therapeutic Standards

The emergence of radioligand therapy for metastatic prostate cancer presents a transformative opportunity when combined with hormone-based treatments. Agents such as 177Lu-PSMA-617 are showing promising results in reducing tumor burden and extending survival. This is opening new avenues for combination hormone therapy protocols in advanced prostate cancer, especially for patients resistant to conventional ADT. The growing clinical adoption of dual-modality treatment strategies is expected to redefine therapeutic standards and expand the market’s scope.

The use of AI-based hormone therapy optimization tools for prostate cancer is gaining traction among oncology centers. These platforms analyze patient-specific genomic and clinical data to tailor hormone therapy regimens, improving efficacy and minimizing side effects. The rise of digital biomarkers for hormone therapy response prediction is enabling early intervention and better disease monitoring. This convergence of digital health and oncology is creating a scalable opportunity for precision hormone therapy in prostate cancer management, especially in personalized medicine ecosystems.

Category-wise Analysis

Drug Class Insights

Androgen receptor inhibitors dominate the drug class segment, accounting for 38% share in 2026. Their stronghold is attributed to the widespread use of enzalutamide, apalutamide, and the newer darolutamide, all of which target androgen receptors to inhibit the growth of prostate cancer cells.

GnRH receptor antagonists, the fastest growing segment, offer faster testosterone suppression and improved cardiovascular safety profiles. These drugs, such as degarelix and the newly introduced relugolix, provide immediate testosterone suppression without an initial surge, making them safer for patients with cardiovascular comorbidities.

Disease State Insights

Metastatic castration-resistant prostate cancer (mCRPC) holds the largest share, contributing to 56% of the market in 2026. This is due to the growing number of late-stage diagnoses, especially in the aging male population, and the widespread adoption of next-generation hormone therapies as first- and second-line treatment options. Non-metastatic castration-resistant prostate cancer (nmCRPC) is the fastest-growing disease segment, supported by early screening initiatives, rising adoption of prostate-specific antigen (PSA) monitoring, and recent drug approvals targeting this disease stage. Agents such as apalutamide, enzalutamide, and darolutamide have received regulatory approval specifically for nmCRPC, demonstrating significant delay in metastasis-free survival and improving long-term outcomes.

Regional Insights

North America Prostate Cancer Hormone Therapy Market Trends and Insights

North America leads the global market, holding a 47% market share. The region benefits from advanced healthcare infrastructure, early diagnosis programs, and widespread adoption of androgen receptor inhibitors. The U.S. leads in clinical trials and drug approvals, with companies such as Pfizer, Sanofi, and AstraZeneca actively developing next-generation hormone therapies. The National Cancer Institute (NCI) and the Department of Veterans Affairs fund large-scale prostate cancer research, with a growing focus on biomarker-driven and precision medicine approaches.

The country also benefits from early screening initiatives, such as Medicare-covered PSA testing, and a significant aging male population, with 60% of diagnoses occurring in men aged 65 and above. The demand for oral androgen receptor inhibitors, especially enzalutamide and apalutamide, is steadily rising due to physician familiarity and insurance coverage.

U.S. Prostate Cancer Hormone Therapy Market Size

The United States accounts for ~85% of the North American market, driven by high disease prevalence, premium drug pricing, and deep insurance penetration. The ACS projects over 299,000 new diagnoses in 2024, sustaining high prescription volumes for branded AR inhibitors and GnRH agents. Favorable reimbursement under Medicare Part D and Part B further reinforces treatment accessibility and revenue concentration in the U.S.

Europe Prostate Cancer Hormone Therapy Market Trends and Insights

Europe is the second-largest market, supported by increasing prostate cancer screening programs and favorable reimbursement policies. Countries such as Germany, France, and the UK are investing in AI-based hormone therapy optimization and expanding access to oral androgen receptor inhibitors. Germany leads the regional market due to strong reimbursement systems, many specialized oncology centers, and a focus on personalized hormone therapy regimens. The German Cancer Research Center (DKFZ) is conducting real-world evidence (RWE) studies to compare AR inhibitors and emerging radiopharmaceuticals, influencing both treatment pathways and procurement trends.

France continues to scale up nationwide screening programs, particularly in high-risk male populations over age 60. French hospitals are increasingly using AI algorithms to match patients with the most appropriate androgen-deprivation therapies (ADT) based on disease progression. The government’s support for biosimilar and generic drug use is enhancing access to affordable therapies.

Germany Prostate Cancer Hormone Therapy Market Size

Germany holds the largest individual country market share in Europe, contributing an estimated 25% of regional revenues. Germany’s statutory health insurance (SHI) system provides comprehensive oncology drug coverage, and the country’s high per-capita healthcare expenditure enables access to premium androgen receptor inhibitors. Active oncology research centers and strong urology specialist networks further reinforce market depth.

UK Prostate Cancer Hormone Therapy Market Size

The UK accounts for ~20% of the European market. The National Health Service (NHS) has progressively expanded reimbursement for second-generation AR inhibitors, including enzalutamide and apalutamide via NICE appraisals. With prostate cancer ranking as the most common male cancer in the UK, sustained investment in urology and oncology services supports consistent prescription growth.

France Prostate Cancer Hormone Therapy Market Size

France contributes ~17% of European market revenues, underpinned by the Haute Autorité de Santé (HAS) reimbursement framework covering approved hormone therapies. French oncology centers have demonstrated high uptake of combination hormonal regimens consistent with ESMO guidelines. Government-backed cancer plans and national prostate cancer awareness campaigns are expected to further accelerate early diagnosis and treatment initiation.

Asia Pacific Prostate Cancer Hormone Therapy Market Trends and Insights

Asia Pacific is the fastest-growing region, projected to expand at a CAGR exceeding 17% during the forecast period. Growth is driven by rising prostate cancer incidence, aging populations, and improving healthcare access in countries such as China, India, and Japan. China is witnessing a significant rise in prostate cancer diagnoses, especially in urban and aging male populations.

The Healthy China 2030 initiative is enabling broader access to early screening, while hospitals in cities such as Beijing, Shanghai, and Guangzhou are adopting oral hormone therapies as first-line outpatient treatments. Domestic pharmaceutical companies Jiangsu Hengrui and BeiGene are entering into strategic licensing deals with global players to co-develop advanced hormone therapies.

Countries such as Thailand, Indonesia, and Vietnam are expanding access to prostate cancer treatment through public-private partnerships and regional pharmaceutical collaborations. Thailand, in particular is focusing on expanding its medical tourism services, where prostate cancer treatment packages now include next-generation therapies for international patients.

India Prostate Cancer Hormone Therapy Market Size

India’s market is rapidly expanding as prostate cancer awareness and PSA screening programs gain traction across urban centers. India contributes an estimated 10% of Asia Pacific revenues, with growth supported by a large aging male population and increasing availability of generic and branded hormone therapy options. Government cancer schemes such as Ayushman Bharat are progressively extending oncology coverage to lower-income populations.

Japan Prostate Cancer Hormone Therapy Market Size

Japan represents a mature and high-value market within Asia Pacific, contributing ~22% of regional revenues, driven by universal health insurance coverage and a high median age population. Japan’s Pharmaceuticals and Medical Devices Agency (PMDA) has approved major androgen receptor inhibitors, and Japan’s clinical oncology community maintains high guideline adherence, sustaining strong per-patient drug utilization rates.

Competitive Landscape

The global prostate cancer hormone therapy market is highly fragmented, with a mix of established pharmaceutical giants, emerging biotech firms, and regional manufacturers competing across various therapy classes. The landscape is shaped by rapid innovation in androgen receptor inhibitors, GnRH receptor antagonists, and combination hormone therapies, each targeting specific disease stages. The shift toward oral hormone therapies has intensified competition, especially in outpatient and retail channels, where patient convenience drives product preference.

Through strategic collaborations, licensing agreements, and acquisitions, particularly in Asia Pacific and Latin America, local firms are partnering with global players to expand access and affordability. The rise of AI-driven hormone therapy personalization platforms is also influencing competitive positioning, as companies race to integrate digital tools into treatment planning.

Key Developments

- In May 2026, Novartis announced new findings from the PSMAddition study showing improved prostate-specific antigen (PSA) responses with Pluvicto combined with standard of care (SoC) in patients with PSMA-positive metastatic hormone-sensitive prostate cancer (mHSPC). The data were presented during a rapid oral session at the American Urological Association Annual Meeting 2026.

- In May 2025, Pfizer Inc. and Astellas Pharma announced label expansion data for enzalutamide (Xtandi®) in hormone-sensitive prostate cancer patients based on updated Phase III trial analyses, reinforcing their leading market position.

- In October 2024, Foresee Pharmaceuticals Co., Ltd. announced the submission of a New Drug Application (NDA) to the U.S. FDA for the 3-month version of CAMCEVI, a ready-to-use leuprolide mesylate depot formulation. Designed for the palliative treatment of advanced prostate cancer, this formulation offers a more convenient dosing schedule compared to monthly injections, potentially improving patient compliance and reducing clinic visits

- In August 2023, Johnson & Johnson Services, Inc. announced that the U.S. FDA approved AKEEGA, a novel combination therapy of niraparib and abiraterone acetate for the treatment of metastatic castration-resistant prostate cancer (mCRPC). This dual-action regimen targets both androgen signaling and DNA repair pathways, offering a new therapeutic option for patients with BRCA mutations and other homologous recombination repair (HRR) gene alterations.

Global Prostate Cancer Hormone Therapy Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 12.6 Billion |

|

Current Market Value (2026) |

US$ 23.5 Billion |

|

Projected Market Value (2033) |

US$ 59.8 Billion |

|

CAGR (2026–2033) |

14.3% |

|

Leading Region |

North America, 47% share (2026) |

|

Dominant Drug Class |

Androgen Receptor Inhibitors, 38% share (2026) |

|

Incremental Opportunity |

US$ 36.3 Billion (2026–2033) |

Companies Covered in Prostate Cancer Hormone Therapy Market

- Astellas Pharma Inc.

- Pfizer Inc.

- Johnson & Johnson Services, Inc.

- Bayer AG

- Sanofi

- Myovant Sciences

- Tolmar Pharmaceuticals

- Foresee Pharmaceuticals Co., Ltd.

- AbbVie Inc.

- Endo International plc

- Clovis Oncology

- Exelixis, Inc.

- NantKwest (ImmunityBio)

- Bristol Myers Squibb

- Others

Frequently Asked Questions

The global market is projected to be valued at US$ 23.5 billion in 2026.

The primary demand driver is the rising global prevalence of prostate cancer among aging men, alongside increasing adoption of AR inhibitors and GnRH-based therapies.

North America leads the prostate cancer hormone therapy market due to high disease prevalence, favorable reimbursement policies, early drug approvals, and strong branded therapy adoption.

Key opportunities include expanding combination hormone therapy usage, increasing PSA screening programs, improving healthcare infrastructure, and broader reimbursement access across emerging Asia-Pacific and Latin America markets.

Major players with strong portfolios include Astellas Pharma Inc., Pfizer Inc., Johnson & Johnson Services, Inc., Bayer AG, and Sanofi.