- Pharmaceuticals

- Preventive Medicine Market

Preventive Medicine Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Preventive Medicine Market by Service Type (Screening & Early Detection, Vaccination & Immunization, Preventive Drug Therapies, Wellness & Lifestyle Interventions, and Digital Health & Remote Monitoring Services), Age Group (Pediatric, Adult, and Geriatric), Application (Cardiovascular Diseases, Cancer, Diabetes, Infectious Diseases, Respiratory Diseases, Mental Health, Neurological Disorders, and Others) End-user, and Regional Analysis from 2026 to 2033

Preventive Medicine Market Share and Trend Analysis

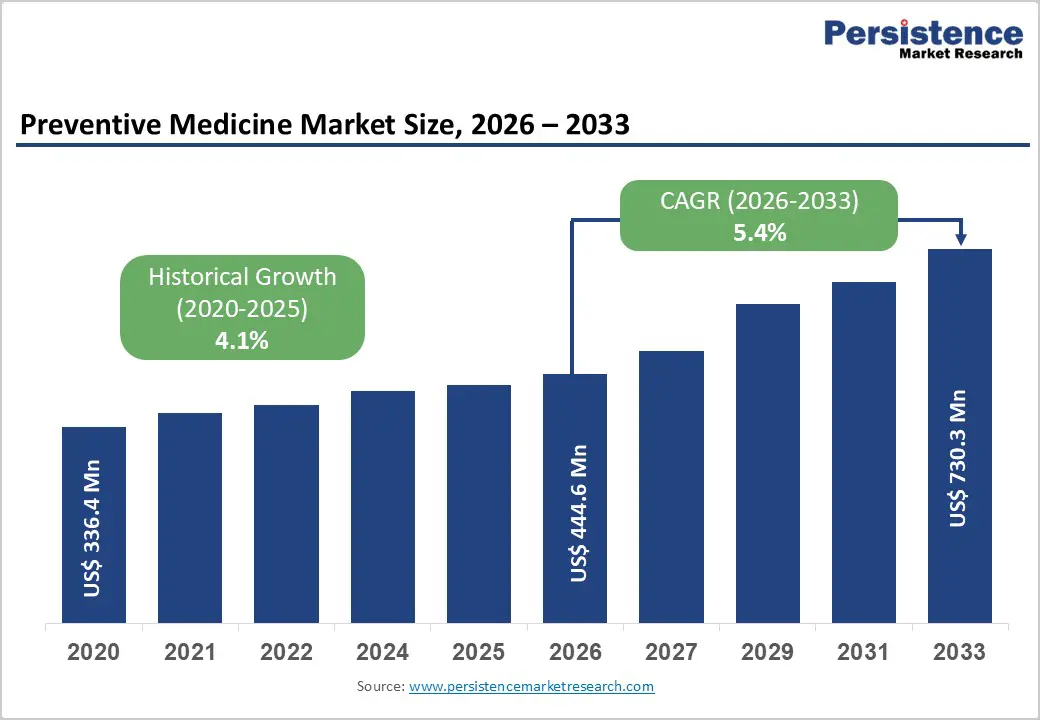

The global preventive medicine market size is estimated to grow from US$ 444.6 million in 2026 to US$ 730.3 million by 2033. The market is projected to grow at a CAGR of 5.4% from 2026 to 2033.

Global demand for preventive medicine solutions is increasing steadily, driven by the rising prevalence of chronic and lifestyle-related conditions such as cardiovascular diseases, cancer, diabetes, respiratory disorders, and mental health conditions, along with a growing shift toward proactive, early-stage healthcare delivery.

Expanding adoption of preventive services across hospitals, specialty clinics, diagnostic centers, and ambulatory care settings is supporting sustained market growth. Higher volumes of population-based screening programs, improved clinician and patient awareness regarding early risk identification, and growing preference for non-invasive preventive interventions are further accelerating uptake. In addition, rising healthcare expenditure and broader access to advanced diagnostics, digital health platforms, and preventive therapeutics are enabling wider deployment across both developed and emerging markets.

Continuous innovation in screening technologies, risk assessment tools, wearable devices, and digital health integration is improving clinical accuracy, patient engagement, and care efficiency. The increasing focus on outpatient-based preventive services, home monitoring, and digitally connected care pathways is further propelling global demand for preventive medicine solutions.

Key Industry Highlights

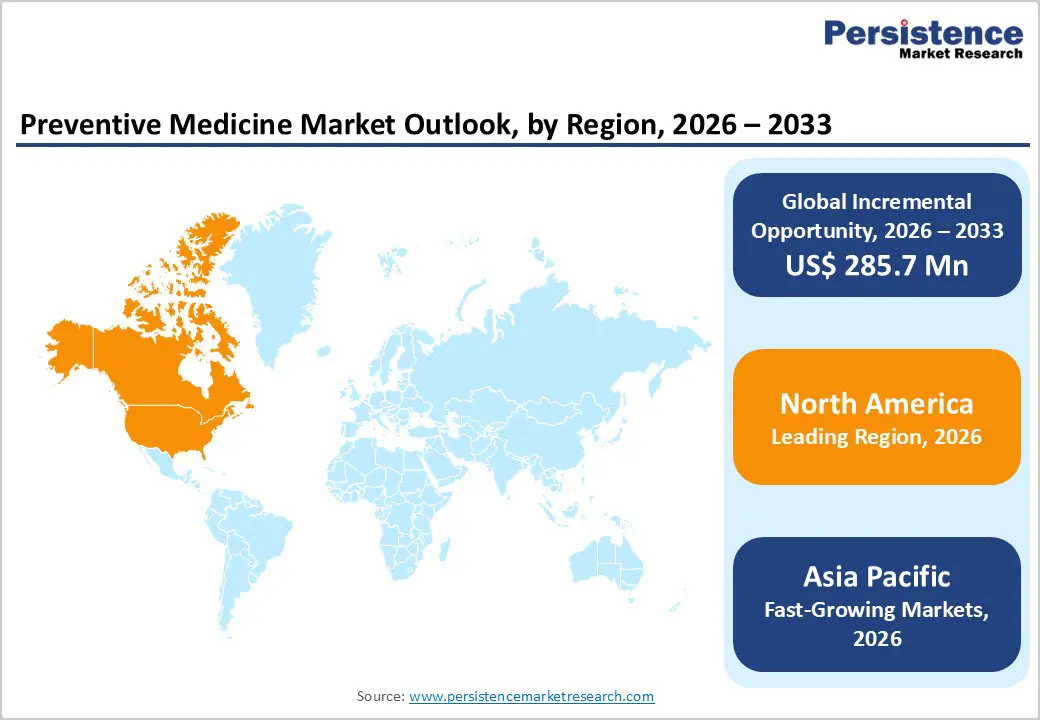

- Leading Region: North America holds the largest share at 46.7%, supported by advanced healthcare infrastructure, strong emphasis on preventive care, early adoption of digital health and screening technologies, and the presence of major pharmaceutical, diagnostic, and healthcare companies.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to large at-risk populations, rapid growth in healthcare and diagnostic facilities, improved access to preventive services, and increased investments in early disease detection and population health programs.

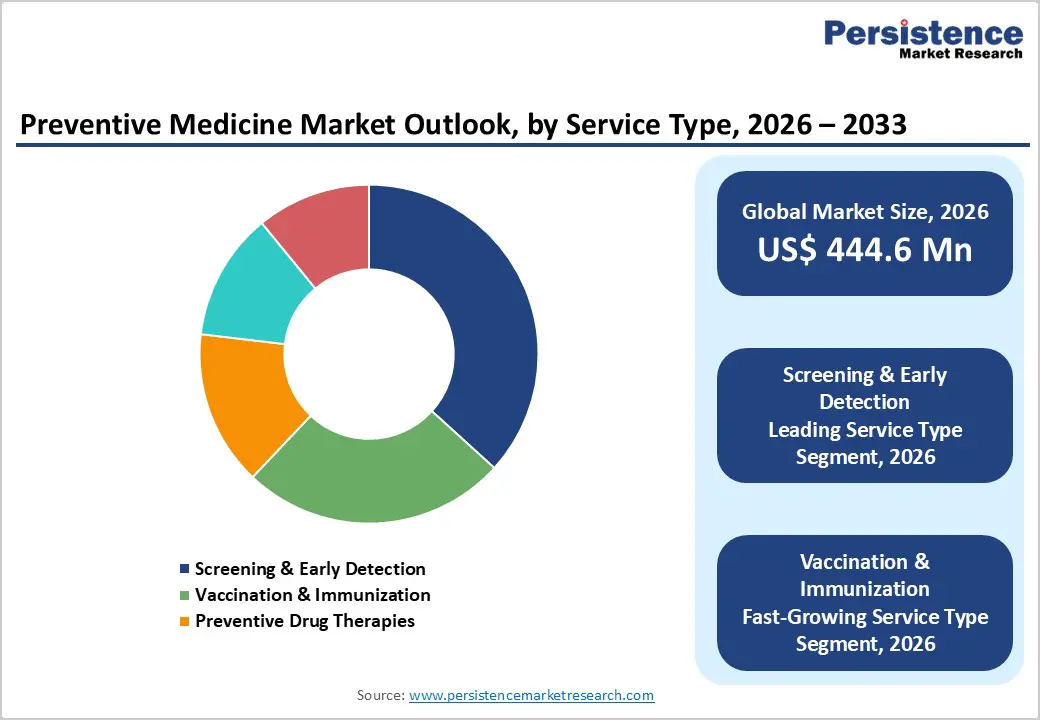

- Leading Service Type Segment: Screening & early detection dominate the market due to their central role in identifying diseases at asymptomatic stages and their widespread integration into routine preventive care pathways.

- Fastest-Growing Service Type Segment: Vaccination & immunization are expanding rapidly as governments and healthcare providers intensify efforts to prevent infectious diseases and reduce long-term healthcare burdens.

- Leading Application Segment: Cardiovascular diseases remain the top application area, driven by high global disease prevalence and a strong emphasis on early risk assessment and long-term prevention.

- Fastest-Growing Application Segment: Cancer is scaling quickly as screening initiatives expand and preventive strategies increasingly focus on early detection and risk reduction.

| Key Insights | Details |

|---|---|

| Preventive Medicine Market Size (2026E) | US$ 444.6 Mn |

| Market Value Forecast (2033F) | US$ 730.3 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Driver - Rising Chronic Disease Burden and Shift Toward Proactive, Early-Stage Healthcare

Escalating prevalence of chronic and lifestyle-related diseases is a core driver accelerating the adoption of preventive medicine globally. Cardiovascular diseases, diabetes, cancer, respiratory disorders, and mental health conditions are increasingly diagnosed due to aging populations, sedentary lifestyles, urbanization, and dietary changes. Healthcare systems are under mounting pressure to move upstream, intervening before disease progression leads to costly hospitalizations and long-term complications. Preventive medicine addresses this need by emphasizing early risk identification, routine screening, immunization, and behavioral interventions.

Advancements in diagnostic technologies, including biomarker-based testing, imaging-based screening, and digital risk assessment tools, have improved the accuracy and accessibility of early detection. Growing awareness among patients and clinicians of the clinical and economic benefits of prevention further supports its adoption. Governments and payers are increasingly prioritizing preventive care as a cost-containment strategy, integrating screening programs and wellness initiatives into national healthcare frameworks. The shift toward value-based care models, which reward improved outcomes rather than treatment volume, further reinforces demand. As healthcare delivery increasingly focuses on long-term population health management rather than episodic treatment, preventive medicine continues to gain strategic importance across both public and private healthcare systems.

Restraints - Cost Constraints, Uneven Access, and Limited Preventive Care Adoption in Some Regions

The adoption of preventive medicine faces several economic, structural, and behavioral barriers. Upfront costs associated with screening programs, diagnostic testing, vaccination campaigns, and digital preventive platforms can be significant, particularly for healthcare systems operating under constrained budgets. In low- and middle-income regions, limited healthcare funding often prioritizes acute care over preventive services, delaying widespread implementation. Access disparities also restrict market expansion. Preventive services are less accessible in rural and underserved areas due to shortages of healthcare professionals, diagnostic infrastructure, and digital connectivity.

Additionally, inconsistent reimbursement policies across countries and payer systems reduce provider incentives to invest in preventive solutions. In some markets, a lack of standardized preventive care guidelines leads to fragmented implementation and variability in service quality. Behavioral and awareness challenges further limit uptake. Preventive medicine relies heavily on patient engagement, adherence, and long-term lifestyle modification, which can be difficult to sustain. Cultural attitudes, low health literacy, and skepticism toward preventive interventions may reduce participation in screening and wellness programs. These financial, infrastructural, and behavioral constraints collectively moderate the pace of preventive medicine market expansion.

Opportunity - Expansion of Digital Health, Personalized Prevention, and Population-Level Care Models

Shifting healthcare priorities are creating substantial growth opportunities for preventive medicine. Digital health platforms, including mobile health applications, wearable monitoring devices, and remote patient engagement tools, are transforming preventive care delivery by enabling continuous risk monitoring and early intervention. These technologies improve accessibility, especially in outpatient and home-based settings, while supporting scalable population health strategies. Personalized preventive medicine represents another major opportunity. Integration of genomics, predictive analytics, and AI-driven risk stratification allows prevention strategies to be tailored to individual risk profiles, improving effectiveness and patient adherence. Employers and insurers are increasingly investing in workplace wellness and preventive programs to reduce long-term healthcare costs and improve productivity.

Emerging economies offer significant untapped potential as healthcare infrastructure expands and governments prioritize preventive care to manage the rising prevalence of chronic diseases. Public health initiatives focused on vaccination, early screening, and lifestyle modification are gaining momentum, supported by digital outreach and telehealth models. Ongoing innovation in diagnostics, data integration, and care coordination is enhancing preventive outcomes while reducing delivery costs. As healthcare systems increasingly shift toward proactive, data-driven, and outcome-focused models, preventive medicine is well-positioned for sustained, long-term growth.

Category-wise Analysis

By Service Type Insights

The screening & early detection segment is projected to dominate the global preventive medicine market in 2026, accounting for 36.7% of revenue. This leadership is driven by the critical role of early diagnosis in reducing disease progression, treatment costs, and mortality across chronic and lifestyle-related conditions. Preventive screening programs for cardiovascular diseases, cancer, diabetes, and infectious diseases are increasingly embedded into routine clinical practice across hospitals, specialty clinics, and diagnostic centers.

Advanced diagnostic technologies, including imaging-based screening, laboratory diagnostics, and risk assessment tools, support accurate identification of disease at pre-symptomatic stages. Widespread government-supported screening initiatives and employer-led wellness programs further strengthen adoption. The shift toward value-based care models, where early detection directly improves outcomes and cost efficiency, continues to accelerate demand. Continuous advancements in diagnostic accuracy, workflow automation, and digital integration reinforce this segment's sustained leadership in global preventive medicine delivery.

By Application Insights

The cardiovascular diseases segment is expected to lead the global preventive medicine market in 2026, accounting for 32.5% of revenue. This dominance reflects the widespread prevalence of cardiovascular conditions globally and the strong clinical emphasis on early risk identification and long-term disease prevention. Preventive interventions, such as blood pressure monitoring, cholesterol screening, lifestyle risk assessment, and digital heart health tracking, are routinely implemented across primary and secondary care settings.

Large-scale screening initiatives targeting high-risk populations, including aging individuals and patients with metabolic disorders, have significantly increased preventive service utilization.

Advancements in wearable monitoring devices, AI-enabled risk stratification, and integrated digital health platforms have enhanced early intervention capabilities. Additionally, growing awareness among patients and providers regarding the benefits of proactive cardiovascular management supports sustained demand. Integration of preventive cardiology programs within hospitals and outpatient care networks further reinforces this segment’s position as the largest application area in preventive medicine.

By End-user, Hospitals Lead Due to Integrated Preventive Care Delivery and High Patient Reach

The hospitals segment is projected to dominate the global preventive medicine market in 2026, accounting for 44.1% of revenue. Hospitals serve as central hubs for preventive healthcare delivery due to their advanced infrastructure, multidisciplinary clinical expertise, and access to comprehensive diagnostic and therapeutic services. Preventive services, including screening programs, vaccination initiatives, chronic disease risk assessments, and preventive drug therapies, are increasingly embedded within hospital-based care pathways.

High patient volumes, particularly for chronic disease management and routine health evaluations, support consistent utilization of preventive medicine solutions. Hospitals also benefit from long-term procurement contracts, integrated electronic health records, and established clinical protocols that support the adoption of preventive care. Their ability to coordinate care across specialties, manage high-risk populations, and deliver population-level prevention strategies further strengthens demand. Ongoing investments in digital health integration, outpatient preventive clinics, and value-based care models ensure that hospitals maintain a dominant role in the global adoption of preventive medicine.

Region-wise Insights

North America Preventive Medicine Market Trends

North America is expected to dominate the global preventive medicine market in 2026, accounting for 46.7% of the value, driven largely by the United States. The region benefits from a highly developed healthcare infrastructure, strong emphasis on preventive care, and widespread adoption of advanced diagnostic and digital health technologies. Preventive screening programs for cardiovascular diseases, cancer, diabetes, and infectious diseases are well established and widely reimbursed, thereby supporting high utilization rates.

Strong payer support, including insurance coverage for preventive services, encourages early intervention and routine health monitoring across diverse populations. Hospitals, diagnostic centers, and specialty clinics actively integrate preventive medicine into standard care pathways.

The presence of leading pharmaceutical, diagnostic, and digital health companies accelerates innovation and commercialization of preventive solutions. Early adoption of wearable health devices, AI-enabled risk assessment tools, and remote monitoring platforms enhances patient engagement and long-term disease prevention. Additionally, strong public health initiatives, clinician awareness, and patient education programs reinforce the adoption of preventive care. Continued investments in digital infrastructure and value-based healthcare models sustain North America’s leadership in the preventive medicine market.

Europe Preventive Medicine Market Trends

Europe’s preventive medicine market is expected to grow steadily in 2026, supported by aging populations, rising prevalence of chronic diseases, and increased policy focus on early diagnosis and prevention. Countries such as Germany, the U.K., France, Italy, and the Nordic region demonstrate strong adoption due to universal healthcare coverage and structured preventive care frameworks. Government-backed screening programs for cardiovascular diseases, cancer, and metabolic disorders play a central role in driving demand. Hospitals and primary care networks routinely implement preventive diagnostics, vaccination programs, and lifestyle intervention initiatives.

Regulatory emphasis on population health management and cost containment encourages healthcare systems to prioritize prevention over treatment. Europe is also witnessing increasing adoption of digital preventive solutions, including remote monitoring, electronic health records, and AI-based risk stratification tools. Standardized clinical guidelines and supportive reimbursement policies further facilitate adoption across care settings. Ongoing investments in digital health infrastructure, clinician training, and public awareness campaigns strengthen long-term market growth and ensure sustained utilization of preventive medicine across the region.

Asia Pacific Preventive Medicine Market Trends

Asia Pacific preventive medicine market is projected to register a higher CAGR of around 7.3% between 2026 and 2033, driven by rapid healthcare expansion and increasing focus on early disease prevention. Large populations in China, India, Japan, and South Korea, combined with rising incidence of cardiovascular diseases, diabetes, cancer, and respiratory disorders, are significantly boosting demand for preventive services. Expanding access to healthcare facilities, the growth of private hospitals, and improvements in diagnostic infrastructure support increased adoption.

Government-led initiatives to strengthen preventive healthcare, expand insurance coverage, and improve population health outcomes are key drivers of growth. Cost-sensitive markets are accelerating demand for affordable, scalable, and digitally enabled preventive solutions, including mobile health platforms and wearable monitoring devices. Global players are expanding regional presence through partnerships, localized manufacturing, and clinician education programs. Continuous improvements in diagnostic accuracy, digital integration, and preventive care delivery models further enhance adoption, positioning the Asia-Pacific region as the fastest-growing in the global preventive medicine market.

Competitive Landscape

The global preventive medicine market is highly competitive, with strong participation from Johnson & Johnson, Pfizer Inc., Novartis AG, Quest Diagnostics, Omron Healthcare, and F. Hoffmann-La Roche Ltd. These players leverage extensive global distribution networks, strong brand equity, and continuous innovation in preventive therapeutics, diagnostics, vaccination platforms, digital health tools, and remote monitoring technologies to address a broad spectrum of preventive healthcare needs.

Rising prevalence of chronic diseases, growing emphasis on early disease detection, increasing healthcare cost containment pressures, and supportive public health initiatives are driving innovation. Manufacturers are focusing on advanced screening technologies, personalized preventive therapies, AI-enabled risk assessment, wearable and remote monitoring solutions, and integrated digital care pathways, while strengthening partnerships with healthcare providers, expanding presence in emerging markets, and sustaining R&D investments to deliver scalable, accessible, and outcome-driven preventive healthcare solutions.

Key Industry Developments:

- In July 2025, Plum committed INR 200 crore toward expanding preventive healthcare initiatives and introduced an at-home health screening solution. The investment aims to strengthen early disease detection, improve accessibility to preventive services, and support scalable, consumer-centric healthcare delivery models across India.

- In February 2026, Pfizer Inc. announced the launch of its TrumpRx program to improve the affordability and accessibility of innovative medicines for millions of Americans. Under the program, patients gain access to a portfolio of more than 30 medicines offered at substantial discounts to list prices. This initiative forms part of Pfizer’s broader landmark Most Favored Nation (MFN) agreement with the U.S. government, designed to lower out-of-pocket prescription costs while reinforcing the United States’ leadership in pharmaceutical innovation.

Companies Covered in Preventive Medicine Market

- Johnson & Johnson

- Pfizer Inc.

- Novartis AG

- Quest Diagnostics

- Omron Healthcare

- F. Hoffmann-La Roche Ltd.

- Siemens Healthineers

- Abbott Laboratories

- Teladoc Health

- Sanofi

- BD

- Novartis

- GSK plc.

- Danaher Corporation

- Others

Frequently Asked Questions

The global preventive medicine market is projected to be valued at US$ 444.6 Mn in 2026.

Rising global burden of chronic diseases, aging populations, and growing emphasis on early diagnosis and cost-effective healthcare are driving demand for preventive medicine.

The global preventive medicine market is poised to witness a CAGR of 5.4%between 2026 and 2033.

Rapid expansion of digital health, remote monitoring, and personalized preventive care solutions presents significant growth opportunities in the global preventive medicine market.

Johnson & Johnson, Pfizer Inc., Novartis AG, Quest Diagnostics, Omron Healthcare, and F. Hoffmann-La Roche Ltd. are some of the key players in the preventive medicine market.