- Beverages

- Prebiotic Soda Market

Prebiotic Soda Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Prebiotic Soda Market by Soda Type (Dairy-Based Prebiotic Soda and Plant-Based Prebiotic Soda), by Packaging (Bottles, Tetra Packs, Cans, and Others), by Flavor (Fruit, Cola Flavors, and Others) by Distribution Channel (Hypermarkets, Convenience Stores, Independent Departmental Stores, Online Retailers, and Wholesalers & Distributors), and Regional Analysis from 2026 - 2033

Prebiotic Soda Market Share and Trend Analysis

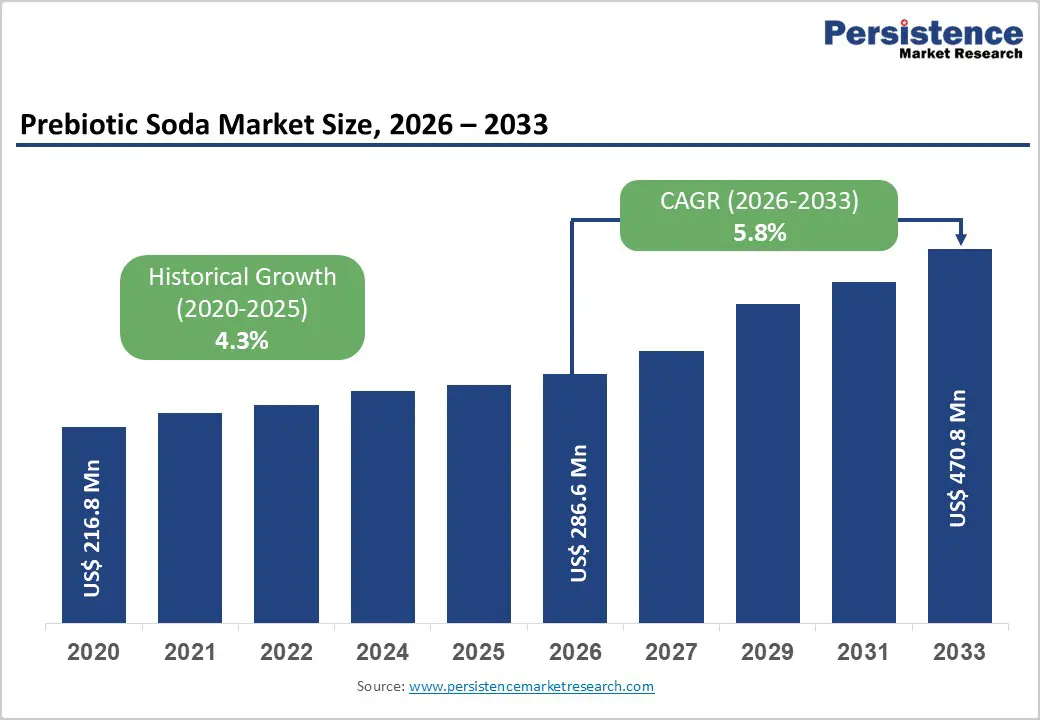

The global prebiotic soda market size is estimated to grow from US$ 286.6 million in 2026 to US$ 470.8 Mn by 2033. The market is projected to grow at a CAGR of 5.8% from 2026 to 2033. Global demand for prebiotic soda is rising steadily, driven by increasing consumer focus on digestive wellness, growing awareness of preventive health through everyday nutrition, and declining preference for high-sugar traditional carbonated drinks. Consumers are actively incorporating prebiotic sodas into daily routines to support gut balance, metabolic health, and overall well-being without sacrificing taste or convenience.

Expanding availability across supermarkets, convenience stores, online platforms, and foodservice outlets is supporting sustained market growth. Higher incidence of digestive discomfort linked to modern diets, increasing understanding of the gut–immune connection, and rising preference for low-calorie, functional beverages are further accelerating adoption. In addition, increasing consumer spending on premium wellness beverages and broader access to clean-label products are enabling wider uptake across both developed and emerging markets. Continuous innovation in prebiotic fiber selection, formulation stability, flavor optimization, and carbonation techniques is improving taste perception, efficacy, and repeat consumption. The growing emphasis on preventive health, lifestyle-oriented nutrition, and digitally enabled direct-to-consumer distribution models is further propelling global demand for prebiotic soda.

Key Industry Highlights:

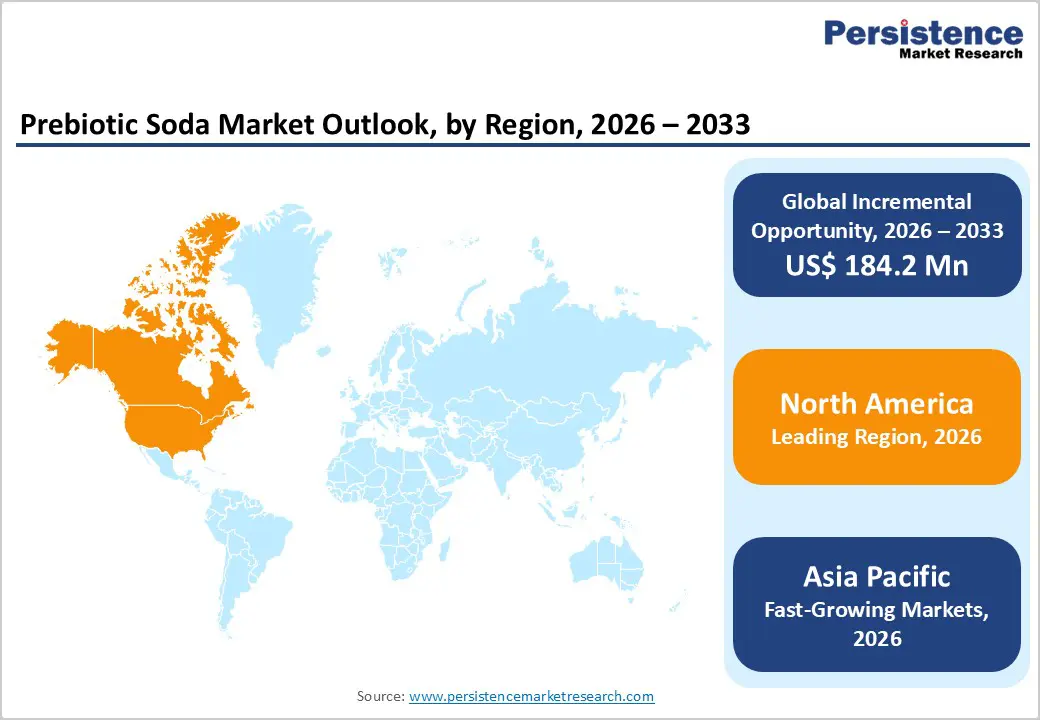

- Leading Region: North America holds the largest share at 46.7%, supported by high awareness of gut health, strong demand for functional beverages, mature retail and e-commerce infrastructure, widespread adoption of premium soda alternatives, and the presence of leading functional beverage brands.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rapid urbanization, rising disposable incomes, growing health consciousness, increasing demand for low-sugar beverages, and expanding access to modern retail and online channels.

- Leading Type Segment: Dairy-based prebiotic soda dominates the market due to familiar taste profiles, smooth mouthfeel, strong consumer acceptance, and suitability for regular consumption.

- Fastest-Growing Type Segment: Plant-based prebiotic soda is expanding rapidly as demand grows for vegan, lactose-free, and clean-label beverage options.

- Leading Flavor Segment: Fruit flavors remain the top segment, driven by broad consumer appeal, refreshing taste profiles, and strong association with natural and health-oriented positioning.

- Fastest-Growing Flavor Segment: Cola flavors are scaling quickly as brands successfully blend familiar soda taste with functional gut-health benefits, attracting mainstream soda consumers seeking healthier alternatives.

| Key Insights | Details |

|---|---|

|

Prebiotic Soda Market Size (2026E) |

US$ 286.6 Mn |

|

Market Value Forecast (2033F) |

US$ 470.8 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

5.8 % |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.3 % |

Market Dynamics

Driver - Shift toward Digestive Wellness and Healthier Soda Alternatives

Changing consumer attitudes toward nutrition and daily wellness are strongly accelerating demand for prebiotic sodas. Growing awareness of the role of gut health in digestion, immunity, metabolism, and mental well-being is encouraging consumers to proactively manage health through everyday food and beverage choices. Traditional carbonated soft drinks are increasingly perceived as high in sugar and low in nutritional value, prompting a shift toward functional alternatives that deliver added benefits without sacrificing taste. Prebiotic sodas appeal to this mindset by offering digestive fiber, low-calorie profiles, and clean-label positioning in familiar soda formats. Rising prevalence of digestive discomfort, irregular bowel habits, and lifestyle-related gut imbalance especially among urban populations further supports regular consumption.

Health-conscious millennials and Gen Z consumers are driving demand, viewing prebiotic beverages as part of preventive self-care routines rather than occasional remedies. The influence of nutritionists, wellness influencers, and functional beverage marketing has amplified consumer education around the gut–brain and gut–immune connection. Additionally, growing availability of prebiotic sodas across supermarkets, convenience stores, and online platforms has improved accessibility. As functional hydration becomes integrated into daily consumption habits, prebiotic sodas are increasingly positioned as a practical and enjoyable solution for long-term digestive wellness.

Restraints - Formulation Complexity, Taste Challenges, and Consumer Skepticism

Despite rising interest, several constraints continue to limit broader adoption of prebiotic sodas. One of the primary challenges lies in formulation complexity, as incorporating effective prebiotic fibers while maintaining carbonation stability, clarity, and shelf life requires advanced technical expertise. Certain prebiotic ingredients can negatively impact mouthfeel or cause off-flavors, making taste optimization critical yet difficult. Consumer expectations for soda-like sensory appeal leave little tolerance for bitterness or excessive viscosity. In addition, inconsistent understanding of prebiotics among mainstream consumers can create skepticism regarding efficacy, particularly when health claims are perceived as vague or insufficiently substantiated.

Price sensitivity also plays a role, as prebiotic sodas are often positioned at a premium compared to conventional soft drinks, limiting penetration among cost-conscious buyers. Regulatory scrutiny around functional claims varies across regions, restricting how benefits can be communicated on labels and marketing materials. This can reduce consumer clarity and slow trial rates. Furthermore, high competition within the broader functional beverage category including kombucha, probiotic drinks, and fiber-enhanced waters intensifies shelf competition. These factors collectively challenge brand differentiation and require sustained investment in education, formulation refinement, and value communication.

Opportunity - Product Innovation, Lifestyle Positioning, and Emerging Consumer Bases

Evolving consumer preferences are opening significant growth opportunities for prebiotic soda manufacturers. Innovation is moving beyond basic digestive positioning toward multifunctional formulations that support immunity, metabolic health, energy balance, and mental wellness. Blending prebiotics with botanicals, vitamins, adaptogens, or natural sweeteners enables brands to create differentiated offerings aligned with specific lifestyle needs. Flavor innovation presents another major opportunity, as consumers increasingly seek familiar soda profiles such as cola, citrus, and berry with a healthier twist. Expansion into emerging markets offers strong upside, supported by rising disposable incomes, westernization of diets, and growing awareness of functional nutrition.

E-commerce and direct-to-consumer models allow brands to educate consumers, offer subscriptions, and collect behavioral insights, strengthening engagement and repeat purchases. Clean-label transparency, low-sugar claims, and sustainable packaging resonate strongly with younger demographics, supporting premiumization. Advances in ingredient processing and fiber solubility are improving product stability and taste consistency. As functional beverages become embedded into daily routines rather than niche consumption occasions, prebiotic sodas are well positioned to capture long-term growth through innovation, accessibility, and lifestyle-driven branding.

Category-wise Analysis

By Soda Type, Dairy-Based Prebiotic Soda Leads Due to Familiar Taste Profile and Established Consumer Acceptance

The dairy-based prebiotic soda segment is projected to dominate the global prebiotic soda market in 2026, capturing a revenue share of 59.3%. This leadership is primarily driven by consumer familiarity with dairy-derived functional beverages and their association with digestive health benefits. Dairy-based formulations enable smoother mouthfeel, enhanced flavor masking of prebiotic fibers, and improved overall palatability compared to some plant-based alternatives. These products often leverage ingredients such as lactose-derived fibers and milk-based carriers that support effective prebiotic delivery while maintaining taste consistency.

Consumers seeking functional benefits without compromising on traditional soda-like sensory attributes show strong preference for dairy-based variants. Additionally, established cold-chain infrastructure and long-standing dairy beverage consumption habits in North America and Europe support wider retail penetration. Manufacturers also favor dairy-based platforms for integrating complementary functional ingredients without affecting carbonation stability. Continuous innovation in low-fat, reduced-lactose, and clean-label dairy formulations further strengthens the segment’s leadership globally.

By Packaging, Bottles Lead Due to Convenience, Portion Control, and Shelf Stability

The bottles segment is expected to lead the global prebiotic soda market in 2026, accounting for a 38.5% revenue share. Bottled packaging dominates due to its convenience, portability, and suitability for single-serve and multi-serve consumption. Bottles allow better carbonation retention and flavor preservation, which is critical for functional sodas containing sensitive prebiotic ingredients. Consumers increasingly prefer resealable bottles for on-the-go consumption, supporting repeat intake without adding any other challenges.

From a manufacturer’s perspective, bottles provide flexibility in branding, labeling, and transparency, which helps communicate functional claims and ingredient benefits clearly. Glass bottles are often associated with premium positioning, while PET bottles support mass-market affordability. Strong compatibility with cold storage, vending machines, and retail refrigeration further boosts adoption. As functional beverage consumption becomes part of daily routines, bottled prebiotic sodas continue to outperform other packaging formats due to their balance of convenience, product integrity, and consumer trust.

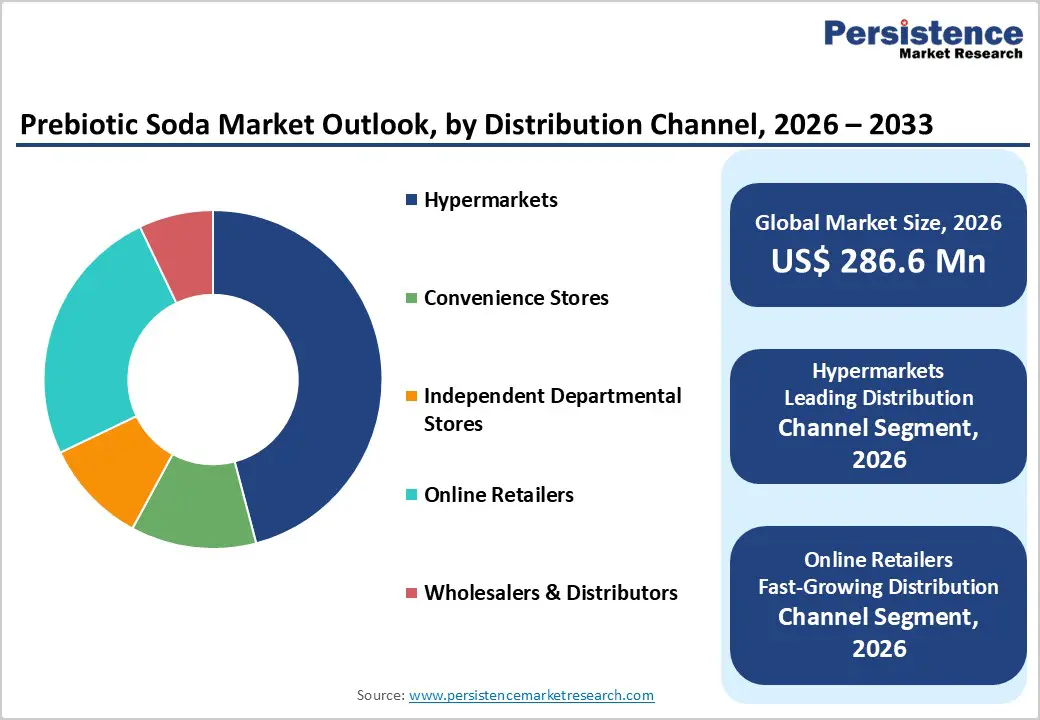

By Distribution Channel, Hypermarkets Lead Due to High Visibility and Bulk Consumer Reach

Hypermarkets are projected to dominate the global prebiotic soda market in 2026, capturing a 45.9% revenue share. The channel’s dominance is driven by extensive shelf space, high foot traffic, and strong visibility for functional beverage brands. Hypermarkets enable consumers to compare multiple brands, flavors, and formulations in a single location, supporting informed purchase decisions. These stores play a critical role in trial purchases, particularly for new and emerging prebiotic soda brands.

Promotional pricing, bundled offers, and in-store sampling further accelerate adoption. For manufacturers, hypermarkets provide scale advantages and consistent volume sales across urban and suburban markets. While online retail is growing rapidly, hypermarkets remain the primary channel for impulse and routine beverage purchases. Their ability to stock both premium and mainstream offerings ensures broad consumer reach. As functional sodas transition from niche to mainstream consumption, hypermarkets continue to serve as the cornerstone distribution channel globally.

Regional Insights

North America Prebiotic Soda Market Trends

North America is expected to dominate the global prebiotic soda market in 2026, accounting for a 46.7% value share, led primarily by the United States. The region benefits from high awareness of gut health, strong demand for functional beverages, and a well-established culture of consuming health-oriented sodas as alternatives to traditional carbonated drinks. Consumers in North America actively seek low-sugar, clean-label, and fiber-enriched beverages, driving sustained demand for prebiotic sodas.

The presence of leading brands, advanced product innovation capabilities, and robust cold-chain logistics supports rapid product launches and wide retail availability. E-commerce and subscription-based beverage platforms are highly developed, further strengthening sales momentum. Favorable spending capacity enables premium pricing for functional beverages with clinical positioning. Regulatory clarity around functional ingredient usage also supports market confidence. Additionally, increasing focus on preventive health, weight management, and digestive wellness continues to reinforce long-term market leadership across the region.

Europe Prebiotic Soda Market Trends

Europe’s prebiotic soda market is expected to grow steadily in 2026, supported by rising health consciousness, strong preference for natural ingredients, and increasing demand for sustainable beverage options. Countries such as Germany, the U.K., France, Italy, and the Nordic region demonstrate robust consumption of functional drinks integrated into daily lifestyles. European consumers show high interest in digestive wellness and fiber intake, driving adoption of prebiotic sodas as alternatives to sugary carbonated beverages.

Strict regulatory standards around ingredient transparency and health claims promote high-quality formulations, enhancing consumer trust. Sustainability plays a critical role, with growing emphasis on recyclable packaging and responsibly sourced ingredients. Specialty beverage retailers, supermarkets, and online platforms are key distribution channels, while cafes and wellness-focused outlets contribute to brand visibility. Innovation in botanical flavors and reduced-sugar formulations aligns well with regional preferences. These factors collectively support stable and consistent growth across the European prebiotic soda market.

Asia Pacific Prebiotic Soda Market Trends

Asia Pacific prebiotic soda market is projected to register a higher CAGR of around 7.9% between 2026 and 2033, driven by rapid urbanization, rising disposable incomes, and evolving dietary habits across China, India, Japan, and South Korea. Increasing awareness of digestive health and functional nutrition is gradually shaping beverage consumption patterns, particularly among younger, urban populations. Traditional familiarity with fermented and gut-friendly foods creates a favorable foundation for prebiotic soda adoption. Expansion of modern retail formats, convenience stores, and e-commerce platforms is improving product accessibility across major cities.

Global brands are entering the region through partnerships and localized production to adapt flavors to regional taste preferences. Social media influence, digital marketing, and health-focused education campaigns are accelerating consumer awareness. Government support for food and beverage innovation in several countries further strengthens supply capabilities. These dynamics position Asia Pacific as the fastest-growing regional market globally.

Competitive Landscape

The global prebiotic soda market is highly competitive, with strong participation from GT's Living Foods, Health-Ade LLC, Kevita, Brew Dr., Humm Kombucha, and Revive Drinks. These players leverage broad retail and e-commerce distribution networks, strong brand recognition, and continuous innovation in prebiotic ingredient selection, formulation stability, taste optimization, sugar reduction, and carbonation profiles to address growing consumer demand for digestive health and functional refreshment.

Rising health consciousness, increasing awareness of gut health, and a shift away from traditional high-sugar carbonated beverages are driving innovation in the market. Manufacturers are focusing on clinically supported prebiotic fibers, clean-label and low-calorie formulations, plant-based ingredients, and familiar soda-inspired flavors, while expanding online retail presence, entering emerging markets, and sustaining R&D investments to deliver functional, palatable, and lifestyle-aligned prebiotic soda offerings.

Key Industry Developments:

- In September 2025, Prodalim unveiled new fruit-based prebiotic soda concepts, highlighting its expansion into functional beverages that combine natural fruit ingredients with digestive health benefits. This initiative reflects the company’s focus on clean-label innovation and its strategy to address rising global demand for healthier, low-sugar soda alternatives.

- In July 2025, PepsiCo Inc. revealed plans to launch a prebiotic cola under its flagship soda brand, marking a strategic move into the functional carbonated beverage segment. The planned introduction signals PepsiCo’s intent to modernize its core soda portfolio by aligning classic cola flavors with growing consumer demand for digestive health and wellness-focused beverages.

- In February 2025, The Coca-Cola Company expanded into the prebiotic soda segment with the launch of Simply Pop, aiming to tap into the fast-growing demand for health-focused and functional beverage alternatives. The launch underscores Coca-Cola’s strategic shift toward low-sugar, wellness-oriented beverages that align with evolving consumer preferences for digestive health and functional nutrition.

Companies Covered in Prebiotic Soda Market

- GT's Living Foods

- Health-Ade LLC

- Kevita

- Brew Dr.

- Humm Kombucha

- Revive Drinks

- Remedy Drinks

- BetterBooch

- Clearly Kombucha

- Suja Life, LLC.

- Farmhouse Culture

- WILD TONIC®

- Lifeway Foods, Inc.

- The Bu

- Others

Frequently Asked Questions

The global prebiotic soda market is projected to be valued at US$ 286.6 Mn in 2026.

Rising consumer awareness of gut health and functional benefits drives demand, supported by a broader shift toward healthier, low-sugar and clean-label beverages; product innovation and flavor diversification also expand consumption and repeat purchases.

The global prebiotic soda market is poised to witness a CAGR of 5.8%between 2026 and 2033.

Expansion into emerging markets with tailored flavors and distribution strategies presents significant growth opportunity.

GT's Living Foods, Health-Ade LLC, Kevita, Brew Dr., Humm Kombucha, and Revive Drinks are some of the key players in the prebiotic soda market.