- Agrochemicals

- Pesticide Inert Ingredients Market

Pesticide Inert Ingredients Market Size, Share, and Growth Forecast 2025 - 2032

Pesticide Inert Ingredients Market by Source (Bio-based, Synthetic), Ingredient Type (Solvents, Emulsifiers, Surfactants, Propellants, Others), Form (Solid, Liquid), End-user (Herbicides, Insecticides, Fungicides, Other), and Regional Analysis for 2025 - 2032

Pesticide Inert Ingredients Market Size and Trend Analysis

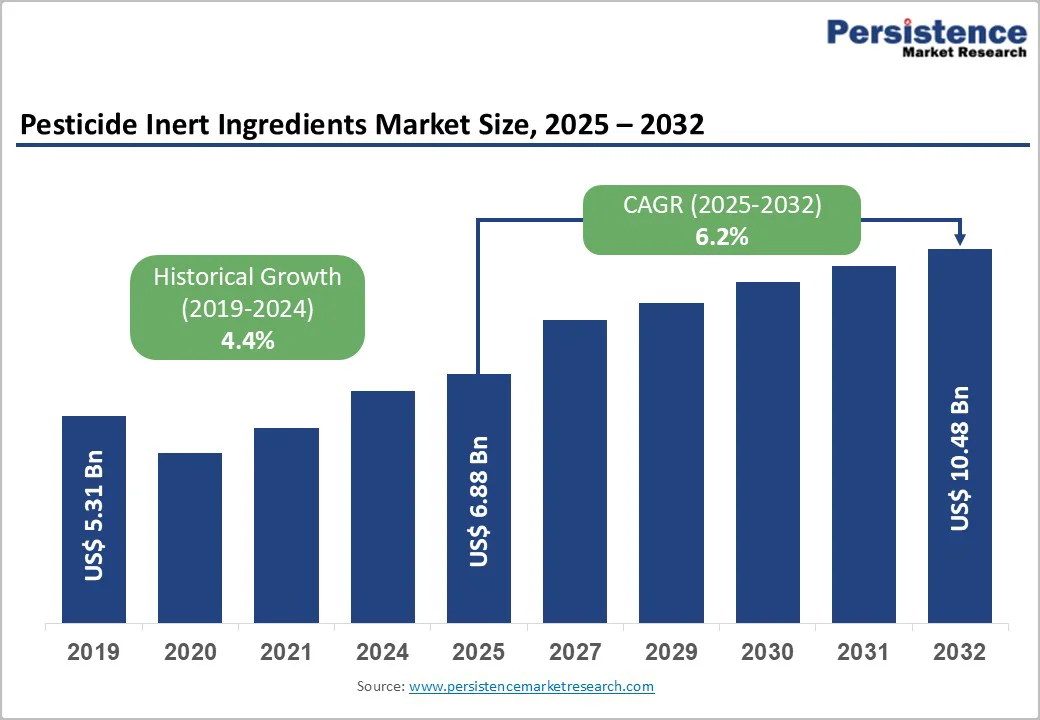

The global Pesticide Inert Ingredients Market size is supposed to be valued at US$6.9 Bn in 2025 and is projected to reach US$10.5 Bn by 2032, growing at a CAGR of 6.2% between 2025 and 2032.

The primary driver of this growth is the escalating global demand for effective crop protection solutions amid rising food security challenges. With the world's population projected to reach 9.7 billion by 2050 according to the United Nations Food and Agriculture Organization (FAO), agricultural productivity must increase by 60%, necessitating advanced pesticide formulations where inert ingredients play a crucial role in enhancing efficacy and application. The regulatory pushes for sustainable agriculture, such as the European Union's Farm to Fork Strategy, encourage innovation in low-toxicity inerts, fostering market expansion through greener formulations.

Key Market Highlights

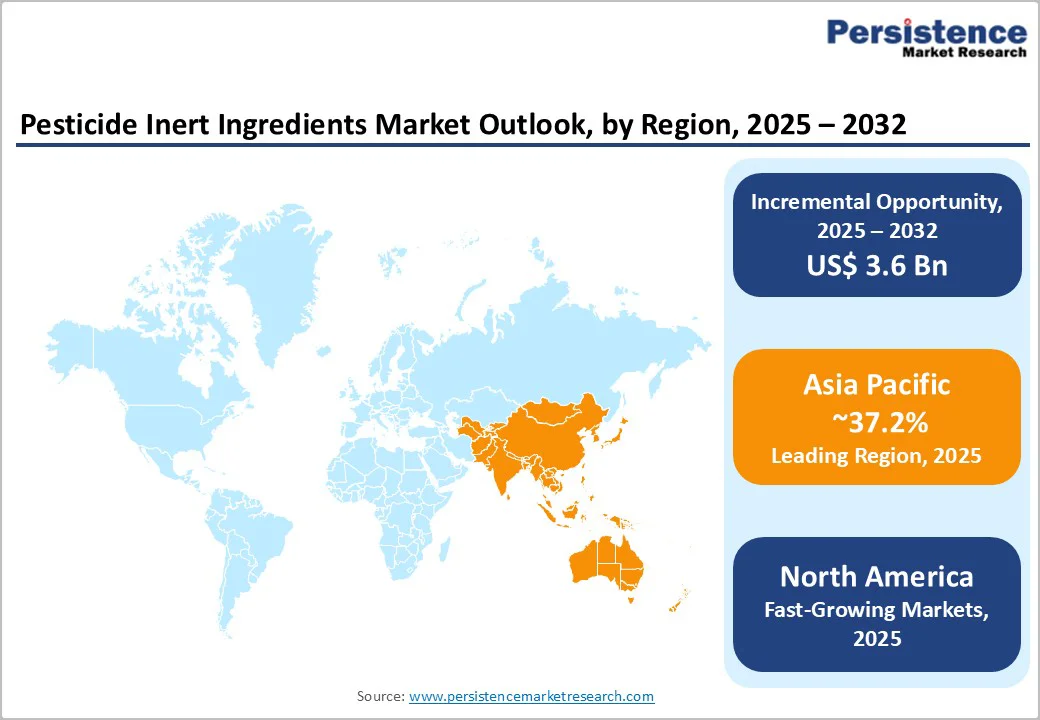

- Regional Leader: Asia Pacific dominates the global pesticide inert ingredients market with a 37.2% share in 2024, driven by intensive agriculture in China and India.

- Fastest Growing Region: North America emerges as the fastest growing region due to advanced regulatory support from the EPA and high adoption of precision farming, ensuring stable demand for innovative inerts.

- Leading Segment: Synthetic sources claim dominance in the category, with 65% of the market share, offering cost-effective stability for conventional pesticides amid global food security needs.

- Fastest Growing Segment: Bio-based ingredients represent the fastest-growing segment, driven by sustainability policies like the EU Green Deal and rising biopesticide integration.

- Growth Opportunity: Bio-based development offers key opportunities, enabling compliance with eco-regulations and capturing premium organic markets for long-term revenue growth.

| Key Insights | Details |

|---|---|

|

Pesticide Inert Ingredients Market Size (2025E) |

US$6.9 Bn |

|

Market Value Forecast (2032F) |

US$10.5 Bn |

|

Projected Growth CAGR (2025-2032) |

6.2% |

|

Historical Market Growth (2019-2024) |

4.4% |

Market Dynamics

Drivers - Rising Demand for Enhanced Pesticide Efficacy

The increasing demand for pesticides with enhanced performance is a key driver for the Pesticide Inert Ingredients Market, as inerts ensure better dispersion, adhesion, and stability of the active components. According to the United States Environmental Protection Agency (EPA), over 80% of registered pesticides rely on solvents and emulsifiers to optimize application, thereby reducing drift and enhancing contact with the target pest. This is particularly evident in row crop farming, where uniform coverage can boost yields by up to 15%, as reported by the USDA National Agricultural Statistics Service.

The parallel growth in the broader Pesticides Market, valued at US$3.8 Bn in 2025 and expanding at 7.5% CAGR through 2032, underscores how inert innovations directly support higher agricultural output. Farmers adopting integrated pest management (IPM) benefit from these inerts, which minimize overuse and resistance development, ultimately driving sustained market demand through proven efficiency gains and cost savings in formulation.

Shift Toward Sustainable Agriculture Practices

Sustainability initiatives worldwide are propelling demand for eco-friendly inert ingredients, aligning with global efforts to reduce chemical residues in food chains. The FAO highlights that sustainable intensification could cut pesticide dependency by 20-30% while maintaining yields, with bio-based inerts like natural surfactants enabling this transition. For instance, the adoption of such inerts in organic farming has grown by 25% annually, as per International Federation of Organic Agriculture Movements (IFOAM) data, due to their biodegradability and lower toxicity profiles.

Stringent regulatory pressures from agencies, including the U.S. Environmental Protection Agency (EPA) and the European Chemicals Agency (ECHA) under REACH regulations, have accelerated manufacturer investment in biodegradable formulations. Over 150 new formulations featuring non-toxic inert ingredients were introduced during 2023-2024, with bio-based alternatives demonstrating superior compatibility with biopesticides and biological control agents. Biosurfactants produced from renewable sources exhibit top-notch biocompatibility while reducing surface tension effectively, making them preferred choices for integrated pest management strategies across North America and Europe.

Market Restraints - Stringent Regulatory Frameworks

Regulatory hurdles imposed by bodies like the EPA and European Food Safety Authority (EFSA) significantly restrain market growth by limiting the approval of new inert ingredients due to toxicity and environmental concerns. The EPA's inert ingredient list under FIFRA requires extensive testing, with only about 1,500 substances approved out of thousands evaluated, leading to delays of up to 2 years in commercialization.

The European Commission adopted Regulation (EU) 2024/1487 in May 2024, introducing uniform data requirements for synergists and safeners with compliance deadlines extending to June 2028. These regulatory burdens increase development costs and extend time-to-market periods, particularly affecting small and medium enterprises attempting to introduce innovative bio-based inert ingredients. These barriers discourage innovation in traditional synthetics, forcing reformulations that raise production expenses and slow market entry, ultimately impacting availability and affordability for end-users in agriculture.

Competition from Generic Manufacturers and Cost Pressures

Established inert ingredient suppliers are experiencing margin compression due to intensifying competition from generic manufacturers, particularly in emerging markets where production costs are substantially lower. BASF discontinued glufosinate-ammonium production at Knapsack and Frankfurt facilities in 2024-2025, citing economic pressures from generic competition and elevated energy costs.

The proliferation of 40 smart formulation units in China has automated over 65% of emulsifiable concentrate production, creating pricing pressures across global supply chains. Rising raw material costs for petroleum-derived solvents and propellants, coupled with fluctuating feedstock availability, have constrained profitability for conventional synthetic inert ingredient manufacturers.

Opportunity - Expansion in Bio-Based Inert Development

Biological pesticide registrations climbed 34% in 2024 as the EPA implemented fast-track approval processes responding to retailer sustainability mandates and consumer demand for residue-free produce. Companies like Evonik Industries AG introduced silica-fluid systems in July 2024 that stabilize microbial actives in liquid formulations for 18 months, addressing critical shelf-life challenges in the Biopesticides Market.

Recent advancements, like fermentation-derived surfactants, offer 65% lower emissions than synthetics, enabling compliance with policies such as the US Farm Bill's bio-preferred mandates. Bio-based surfactants incorporating enzyme-catalyzed synthesis demonstrate superior emulsification properties while meeting EU REACH standards and supporting regenerative agriculture initiatives

Integration with Precision Agriculture Technologies

Precision agriculture technologies, including drone applications, variable-rate spraying systems, and real-time field analytics, are fundamentally transforming pesticide application methodologies and creating significant demand for specialized inert ingredients. The U.S. Environmental Protection Agency 2024 herbicide strategy mandates drift-reduction technologies across approximately 900 protection zones, driving formulation thresholds for drift indices below 10%.

Market participants developing innovative adjuvants and surfactants specifically engineered for precision delivery systems are capturing premium market valuations and establishing technology differentiation advantages. Manufacturers such as Stepan Company have launched novel tank-mix adjuvants, including STEPGROW CT, formulated through intensive laboratory and field trial development to enhance wetting performance, reduce foam, and improve efficacy with modern application equipment across diverse pesticide categories, including herbicides, insecticides, and fungicides.

Category-wise Analysis

Source Insights

The Synthetic segment leads the source category with approximately 65% market share, owing to its cost-effectiveness, scalability, and superior compatibility in large-scale pesticide production. Petroleum-derived solvents, emulsifiers, and surfactants offer cost advantages and technical performance characteristics that remain essential for conventional chemical pesticide applications, particularly in large-scale commodity crop protection.

However, bio-based inert ingredients represent the fastest-growing segment, experiencing adoption rates exceeding 22% annually as manufacturers respond to sustainability imperatives and regulatory incentives favoring renewable feedstocks. The Potassium Dihydrogen Phosphate Market is increasingly incorporating bio-based adjuvants that enhance nutrient uptake efficiency while reducing environmental footprints. Companies, including Clariant AG and Evonik Industries AG, have launched biosurfactant product lines featuring ADJUWEX™ and BREAK-THRU® MSO MAX 522 that demonstrate equivalent or superior performance compared to synthetic alternatives while meeting biodegradability requirements established under EPA List 4 guidelines.

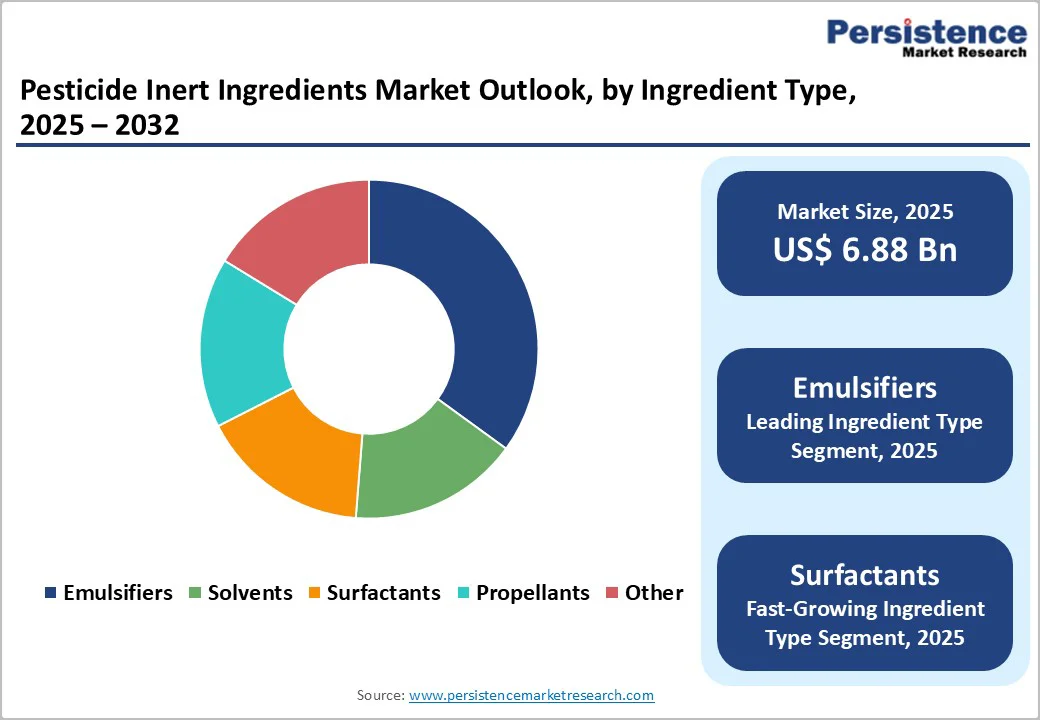

Ingredient Type Insights

Emulsifiers dominate the Ingredient Type category with around 35% share, as they are essential for creating stable pesticide mixtures that prevent separation and ensure even distribution. According to Purdue University Extension research, emulsifiers like alcohol ethoxylates enhance wetting and spreading, improving pesticide uptake on leaf surfaces compared to non-emulsified forms. Their leadership stems from widespread use in herbicide and insecticide formulations, where immiscible oil-water blends are common, supported by EFSA assessments confirming their role in over 60% of EU-approved products. This segment's prevalence is further bolstered by innovations in low-foam variants, catering to spray equipment needs and minimizing application losses.

Form Insights

Liquid formulations dominate the pesticide inert ingredients market with approximately 72% share, driven by superior compatibility with modern high-pressure boom sprayers, autonomous drones, and center-pivot irrigation systems. Liquid inert ingredients, including emulsifiable concentrates, suspension concentrates, and water-dispersible liquids, offer ease of mixing, uniform distribution, and flexibility in tank-mix applications that solid formulations cannot match.

University of Florida IFAS Extension studies indicate that liquid inerts facilitate quicker dissolution and uniform application, reducing clogging in nozzles by 40% versus solids, which is critical for large-acreage operations. This dominance is supported by industry adoption in foliar sprays, where liquids enable precise dosing aligned with IPM protocols, as per FAO guidelines. Their versatility across crop types further solidifies leadership, despite solids' niche in granular products.

End-user Analysis

Herbicides lead the end-user category with roughly 45% share, reflecting their extensive application in weed control for major crops like corn and soybeans. The USDA reports that herbicides account for over 50% of US pesticide usage, with inerts enhancing their translocation and rainfastness to combat resistance, affecting over 100 million acres globally per the Weed Science Society of America.

North America demonstrates particularly high herbicide-inert ingredient utilization, with glyphosate-tolerant soybean adoption rates exceeding 95% and corn adoption reaching 89% across principal production regions, necessitating sophisticated formulation chemistries to address emerging herbicide-resistant weed populations, including Palmer amaranth and waterhemp. This supremacy is justified by economic pressures on farmers, where effective weed management boosts yields by 10-15%, making inert-optimized formulations a staple in broadleaf and grass control programs.

Regional Insights

North America Pesticide Inert Ingredients Market Trends

The U.S. maintains market leadership in the North America pesticide inert ingredients sector, underpinned by robust regulatory frameworks administered by the EPA and USDA that ensure product safety while fostering innovation in sustainable formulation technologies. Recent EPA updates in 2025 streamlined registrations for low-risk bio-inerts, spurring developments like bio-surfactants that reduce residues by 20% in crop protection. This fosters an innovation hub, with USDA investments in precision ag tech integrating advanced inerts for targeted applications, enhancing efficacy in high-value corn belts.

The region's trends emphasize sustainability, with the North America Crop Protection Chemicals Market seeing 4.2% CAGR growth per industry analyses, driven by IPM adoption covering 30% of farmland. Farmer cooperatives and ag-tech firms collaborate on inert formulations compliant with FQPA tolerances, minimizing pollinator risks amid rising organic acreage.

Europe Pesticide Inert Ingredients Market Trends

European markets exhibit stringent regulatory harmonization under REACH and the Plant Protection Products Regulation (PPPR), with the European Commission implementing Regulation (EU) 2024/1487 in May 2024, establishing uniform data requirements for pesticide components, including synergists and safeners. Agrochemical companies operating across Germany, France, the U.K., and Spain must navigate comprehensive approval processes requiring Chemical Safety Reports for substances exceeding 10 tonnes annual production.

In Germany, inert innovations have cut emissions by 15%, as per ECHA data, supporting sustainable viticulture and horticulture. The U.K. post-Brexit alignments with EFSA ensure seamless trade, while Spain's olive sector benefits from water-soluble inerts amid drought challenges. Performance varies, with France leading in bio-based trials that boost formulation stability by 25%, per INRAE studies.

Asia Pacific Pesticide Inert Ingredients Market Trends

Asia Pacific constitutes the largest regional market, accounting for 37.2% of global agrochemical consumption in 2024. China and India collectively generate approximately 60% of regional pesticide inert ingredient demand, reflecting the agricultural scale of these economically significant nations and intensifying crop protection chemistry adoption. Government support, including agricultural modernization initiatives, subsidy programs, and technology adoption incentives, stimulates continued pesticide consumption growth and corresponding inert ingredient demand acceleration.

ASEAN nations like Vietnam leverage low-cost production for exports, with 10% annual growth in inert formulations per ASEAN Secretariat reports. Japan's tech-driven sector focuses on nano-inerts for precision spraying, reducing usage by 15%, while regional dynamics favor bio-shifts amid ASEAN sustainability pacts.

Competitive Landscape

The pesticide inert ingredients market exhibits a consolidated structure, dominated by multinational chemical giants controlling over 60% of supply through vertical integration and R&D investments. Leaders pursue expansion via mergers, like joint ventures for bio-based production, and allocate 5-7% of revenues to innovation in green surfactants. Key differentiators include proprietary low-toxicity formulas and supply chain resilience, while emerging models emphasize circular economy approaches, such as recycled solvents, to meet ESG standards and capture sustainable segments.

Key Market Developments

- March 2025: BASF and Agmatix unveiled an artificial intelligence tool detecting soybean cyst nematode stress through aerial imagery, guiding targeted adjuvant-supported nematicide sprays that optimize inert ingredient utilization.

- October 2025: Croda International Plc released a comprehensive white paper exploring regenerative agriculture innovations and specialty ingredient roles in transforming agricultural sustainability practices.

- July 2024: Evonik Industries AG introduced a silica-fluid stabilization system enabling microbial actives to maintain viability in liquid formulations for 18 months, addressing critical biopesticide commercialization challenges.

Top Companies in the Pesticide Inert Ingredients Market

BASF SE (Ludwigshafen, Germany) leads with a diverse portfolio of synthetic and bio-based inerts, generating significant revenue from agricultural solutions and investing heavily in R&D for low-residue technologies, holding a strong influence through global patents.

DowDuPont (Midland, USA) excels in emulsifiers and solvents, leveraging its chemical expertise for IPM-compatible products; its maturity and scale ensure portfolio breadth, with key expansions in sustainable formulations driving market share.

Clariant AG (Muttenz, Switzerland) focuses on specialty surfactants, noted for innovation in bio-inerts; its influence stems from ESG-aligned offerings, bolstered by strategic partnerships enhancing presence in Europe and Asia.

Companies Covered in Pesticide Inert Ingredients Market

- Clariant AG

- Eastman Chemical Company

- Evonik Industries AG

- Solvay SA

- BASF SE

- Huntsman International LLC.

- DowDuPont

- Royal Dutch Shell Plc

- Stepan Company

- Croda International Plc.

- LyondellBasell Industries N.V.

- Akzo Nobel N.V.

Frequently Asked Questions

The market is valued at US$6.9 Bn in 2025 and expected to reach US$10.5 Bn by 2032, reflecting a 6.2% CAGR driven by sustainable formulation demands.

Key drivers include rising food security needs, boosting pesticide use, and sustainability shifts favoring bio-based inerts, supported by FAO projections for a 60% agricultural output increase by 2050.

Emulsifiers lead with a 35% share, essential for stabilizing pesticide mixtures and improving application efficiency in herbicides and insecticides.

Asia Pacific dominates the market with a 37.2% share in 2024, led by robust growth in the agriculture industry in China and India.

Bio-based inerts offer significant potential, aligning with the Biopesticides Market growth and policies like the EU Green Deal for eco-friendly formulations.