- Agrochemicals

- Biopesticides Market

Biopesticides Market Size, Share, and Growth Forecast 2026 - 2033

Biopesticides Market by Product Type (Bioinsecticides, Bioherbicides, Biofungicides, Bionematicides), by Origin (Microbial, Biochemical), by Formulation (Liquid Formulation, Dry Formulation), Application (Foliar Spray, Seed Treatment, Soil Treatment, Post‑Harvest), Crop Type (Fruits & Vegetables, Grains & Cereals, Oilseeds & Pulses, Other Crops), and Regional Analysis, 2026 - 2033

Biopesticides Market Size and Trend Analysis

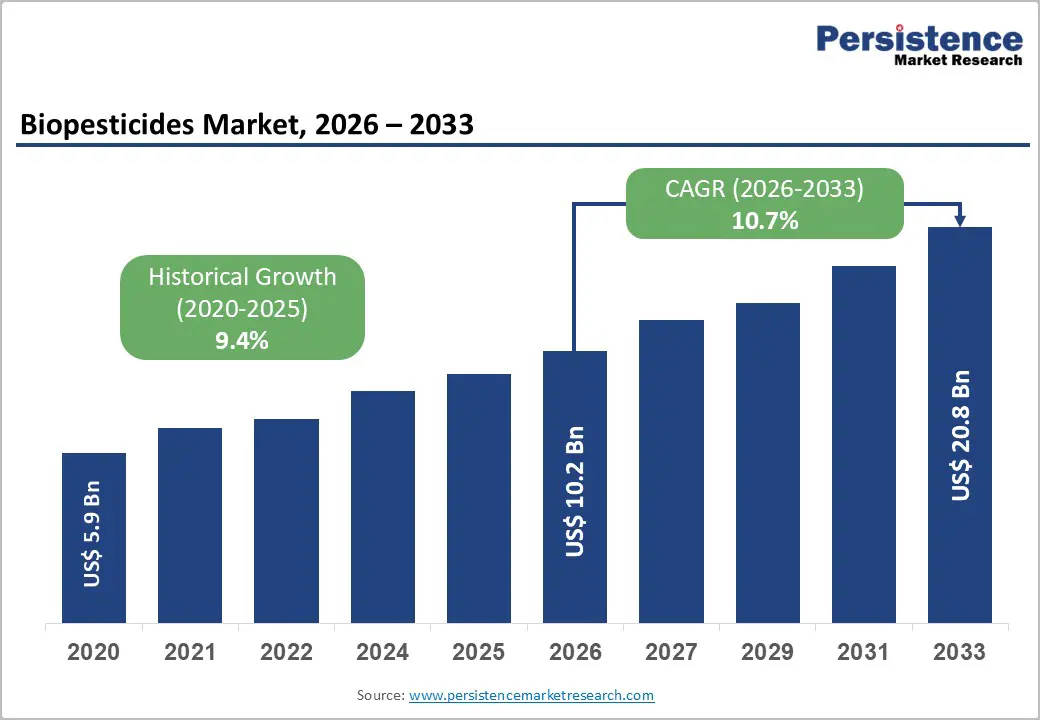

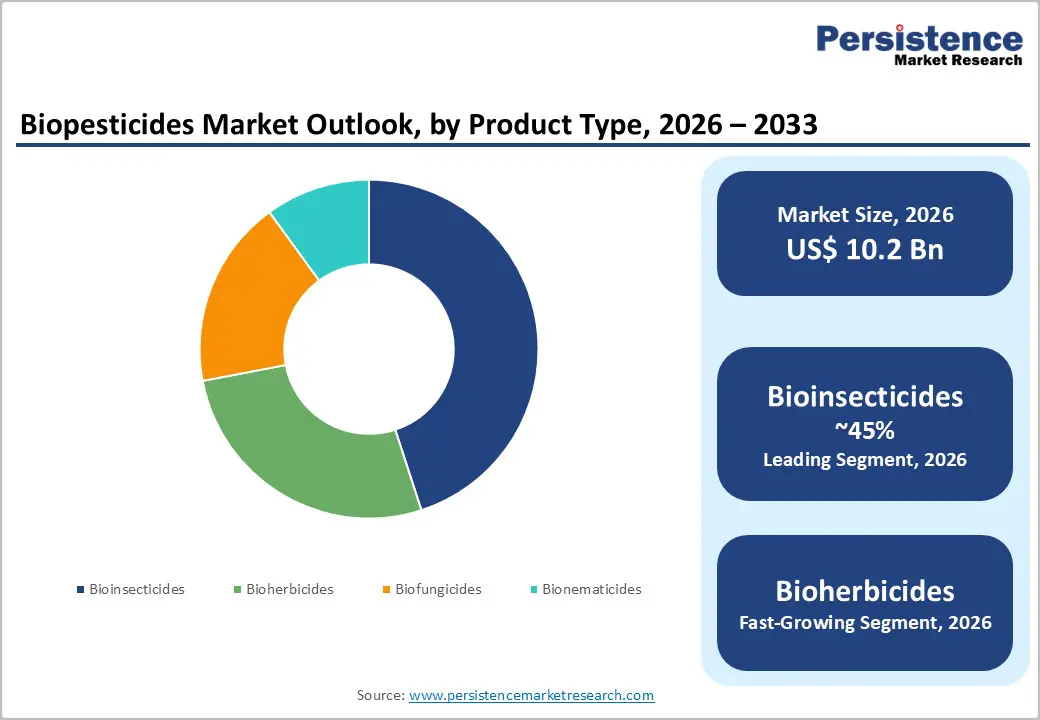

The global Biopesticides Market size is likely to be valued at US$ 10.2 billion in 2026 and is expected to reach US$ 20.8 billion by 2033, growing at a CAGR of 10.7% during the forecast period from 2026 to 2033.

This robust expansion is driven by rising demand for sustainable, eco-friendly crop-protection solutions in conventional, organic, and integrated pest management (IPM) systems.

Key Industry Highlights:

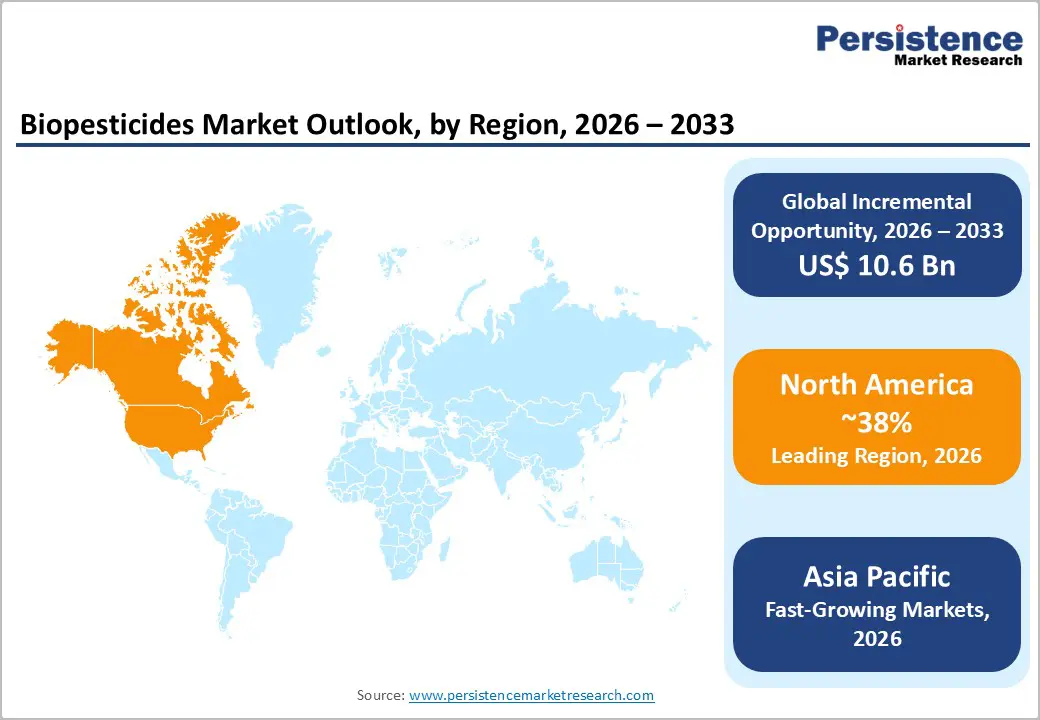

- Leading region: North America leads the Biopesticides Market holding 38% share, due to strong regulatory support, high adoption of organic farming, and advanced precision-ag technologies in the United States.

- Fastest-growing region: Asia Pacific is the fastest-growing region, driven by organic farming, horticulture, and specialty crops in China, Japan, India, and ASEAN countries.

- Dominant segment: Bioinsecticides are the dominant product type segment, capturing 40–45% of demand due to extensive use in row crops, horticulture, and specialty crops.

- Fastest-growing segment: Biofungicides are one of the fastest-growing segments, expanding at a higher CAGR than the overall market as disease-resistant crop varieties and IPM adoption intensify.

- Key market opportunity: The integration of biopesticides with precision agriculture technologies such as drones and AI-driven analytics represents a high-value growth opportunity, particularly in North America and Europe.

| Key Insights | Details |

|---|---|

|

Biopesticides Market Size (2026E) |

US$ 10.2 Billion |

|

Market Value Forecast (2033F) |

US$ 20.8 Billion |

|

Projected Growth CAGR (2026–2033) |

10.7% |

|

Historical Market Growth (2020–2025) |

9.4% CAGR |

Market Dynamics

Drivers - Global Transition Toward Organic Farming and IPM Systems is Rapidly Accelerating Biopesticide Adoption Across Sustainable Agriculture Worldwide

A major driver of the Biopesticides Market is the global transition toward sustainable agriculture, organic farming, and integrated pest management (IPM) practices. Rising consumer demand for chemical-free, residue-free, and environmentally safe food products is encouraging farmers to replace synthetic pesticides with natural alternatives. Biopesticides support soil health, reduce environmental damage, and align with sustainability goals, making them increasingly attractive across commercial farming systems.

Regulatory organizations such as the U.S. Environmental Protection Agency (EPA), European Food Safety Authority (EFSA), and Food and Agriculture Organization (FAO) are actively promoting biopesticide adoption through faster approvals, financial incentives, and restrictions on hazardous chemicals. These supportive policies are accelerating market penetration. Industry estimates indicate that biopesticides now represent more than 10% of global crop protection products, largely driven by organic farming growth and IPM integration. As sustainability becomes central to agricultural decision-making, demand for biopesticides is expected to continue rising steadily.

Stricter Environmental Regulations and Pesticide Reduction Policies Are Creating Strong Long-Term Demand for Eco-Friendly Biopesticides

Growing regulatory pressure and environmental awareness are strongly driving biopesticide adoption worldwide. Governments are tightening limits on chemical pesticide residues, banning high-risk substances, and promoting eco-friendly farming practices to protect soil health, water resources, and biodiversity. These policies are creating favorable conditions for biopesticides as safer crop protection alternatives.

The European Union’s Green Deal and Farm to Fork Strategy aim to reduce pesticide use by 50% by 2030, significantly accelerating demand for biological solutions. In India, initiatives such as the National Mission on Sustainable Agriculture and Pradhan Mantri Fasal Bima Yojana encourage farmers to adopt sustainable pest control methods. Environmental concerns related to pollution, resistance buildup, and declining soil fertility are also pushing growers toward natural solutions. Together, regulatory enforcement and sustainability goals are expanding biopesticide usage across row crops, horticulture, and specialty farming.

Restraints - Higher Operational Costs, Shorter Shelf Life, and Slower Action Continue to Limit Biopesticide Adoption in Price-Sensitive Markets

Despite growing interest, higher costs and performance limitations remain key challenges for the Biopesticides Market. Compared to synthetic pesticides, biopesticides often require more frequent applications, have shorter shelf life, and need specific storage conditions, which increase overall operating expenses. Many products also act more slowly and perform best under precise environmental conditions, making results less predictable for farmers seeking immediate pest control.

In cost-sensitive regions, especially in developing economies, growers may prefer cheaper chemical alternatives that offer faster visible impact. These economic barriers slow widespread adoption, particularly among smallholder farmers who operate on thin profit margins. Additionally, logistical challenges in distribution and storage further add to cost pressures. While technological improvements are enhancing product effectiveness, price competitiveness remains a major hurdle restraining rapid market expansion in the short to medium term.

Lack of Farmer Education, Training, and Technical Support Remains a Key Barrier to Widespread Biopesticide Implementation

Limited knowledge and technical understanding continue to restrict biopesticide adoption, especially in developing agricultural regions. Unlike conventional pesticides, biopesticides require accurate timing, correct dosage, and integration within IPM strategies to achieve optimal results. Many farmers lack access to training programs, extension services, and digital advisory platforms that explain proper application methods.

In rural areas with low literacy levels, awareness about the long-term benefits of biopesticides remains low, leading to hesitation in switching from traditional chemicals. Misuse or poor application can also result in disappointing outcomes, further discouraging adoption. Although governments and agribusiness companies are increasing outreach efforts through mobile platforms and demonstration farms, knowledge gaps still pose a short-term barrier. Expanding education initiatives and technical support will be critical to unlocking full market potential.

Opportunity - Rapid Expansion of Organic and Specialty Crop Production is Unlocking High-Value Growth Opportunities for Biopesticide Manufacturers

The rapid expansion of organic and specialty crop farming presents a significant growth opportunity for the biopesticides market. Organic agriculture depends heavily on biological pest control solutions due to strict restrictions on chemical pesticide use. Globally, organic farming is growing at an estimated CAGR of 15%, driven by rising health awareness, environmental concerns, and premium food demand. Specialty crops such as fruits, vegetables, nuts, and herbs face high pest pressure and quality standards, making biopesticides essential for yield protection and residue-free produce.

Industry estimates suggest that biopesticides account for over 20% of pesticide use in organic farming systems. As export markets increasingly require low chemical residues and sustainable certification, adoption is expected to accelerate further. This trend positions organic and specialty crop farming as one of the most profitable and fast-growing demand segments for biopesticide manufacturers.

Precision Agriculture Technologies are Enhancing Biopesticide Efficiency, Driving Adoption Through Targeted and Cost-Effective Crop Protection

The combination of biopesticides with precision agriculture technologies is emerging as a high-value growth opportunity. Advanced tools such as drones, GPS-guided sprayers, satellite imaging, and AI-based crop monitoring enable precise targeting of pests, reducing product waste and improving treatment effectiveness. Precision systems ensure optimal timing and dosage, which significantly improve the performance of biopesticides compared to traditional broad spraying methods.

Leading agribusiness firms, including Bayer AG, BASF SE, and Syngenta AG, are investing in digital farming platforms integrated with biological crop protection solutions. Industry data indicate that precision agriculture adoption is growing at 15–20% annually across major farming regions. As smart farming expands, biopesticides will benefit from improved efficiency, lower costs, and stronger yield outcomes. This technological alignment is expected to become a key growth driver for the market over the next decade.

Category wise Analysis

Product Type Insights

Bioinsecticides represent the largest product segment in the Biopesticides Market, accounting for approximately 45% of total market value. Their dominance reflects widespread usage across row crops, fruits, vegetables, and greenhouse farming, where insect damage directly impacts yields and crop quality. Products based on microbial organisms such as Bacillus thuringiensis (Bt) and natural compounds such as neem extracts are favored for their targeted action, low toxicity, and environmental safety.

These solutions help control pests while preserving beneficial insects and soil microorganisms. Major agribusiness players, including Bayer AG, BASF SE, and Syngenta AG have developed advanced bioinsecticide formulations suitable for large-scale farming operations. Their strong performance, regulatory acceptance, and compatibility with IPM systems reinforce their leadership position. As resistance to chemical insecticides increases, demand for bioinsecticides is expected to remain the primary growth engine of the biopesticides sector.

Origin Insights

Microbial biopesticides dominate the origin segment, representing approximately 60% of the total market value. This strong position is driven by their effectiveness in controlling insects, plant diseases, and nematodes while maintaining ecological balance. Bacteria, fungi, and viruses are widely used due to their high specificity and minimal impact on non-target organisms. These biological agents integrate seamlessly into IPM programs and organic farming systems.

Leading companies such as Novozymes, Marrone Bio Innovations, and Isagro SpA have developed advanced microbial formulations that enhance stability, shelf life, and performance under varying environmental conditions. Their continuous investment in strain improvement and delivery technologies further strengthens this segment. As sustainability regulations tighten and farmers seek safer alternatives, microbial biopesticides are expected to maintain their dominant role while expanding into new crop and regional markets.

Formulation Insights

Liquid formulations lead the biopesticides market, accounting for nearly 60% of global demand. Their popularity stems from ease of handling, quick absorption by plants, and compatibility with existing spraying equipment. Liquid biopesticides are widely applied through foliar spraying, seed treatment, and soil drenching, offering flexible usage across different crop stages. Farmers prefer liquid products due to uniform coverage and rapid action against pests and diseases.

Industry estimates indicate that more than 70% of biopesticide applications in major crops utilize liquid formats. Manufacturers are also investing in formulation improvements to enhance shelf life, stability, and effectiveness under field conditions. As modern farming equipment becomes more widespread and application precision improves, liquid formulations are expected to grow at a faster rate than dry or granular alternatives, further strengthening their leadership position in the market.

Application Insights

Foliar spray remains the most widely used application method, representing approximately 45% of biopesticide demand worldwide. This method enables rapid and direct treatment of pests and diseases affecting plant leaves, stems, and fruits. Farmers favor foliar spraying due to its simplicity, immediate effectiveness, and compatibility with standard agricultural equipment. It is extensively used across row crops, orchards, greenhouses, and vegetable farms.

Leading manufacturers have developed highly concentrated and fast-acting biopesticide sprays designed for large-scale and precision farming systems. Foliar application also allows better integration with pest monitoring technologies and targeted treatment programs. As growers increasingly adopt IPM strategies and smart farming tools, foliar spray usage is expected to remain the primary delivery method. Its efficiency and versatility will continue driving strong demand within the biopesticides market.

Crop Type Insights

Fruits and vegetables represent the largest crop segment for biopesticide consumption, accounting for nearly 35% of total market demand. These crops are highly susceptible to insect attacks, fungal infections, and post-harvest diseases, requiring intensive crop protection measures. Biopesticides are widely used to ensure high-quality, residue-free produce that meets strict domestic and export regulations.

Growers increasingly rely on biological solutions to maintain crop health while preserving soil fertility and ecosystem balance. Industry data indicate that more than 25% of pesticide usage in fruit and vegetable farming now involves biopesticides, driven by organic certification and IPM practices. Rising consumer preference for safe, chemical-free food is further strengthening this trend. As global consumption of fresh produce increases, fruits and vegetables will continue to be a core growth driver for the biopesticides market.

Regional Insights

North America Biopesticides Market Trends

North America remains a leading region in the biopesticides market, supported by advanced farming practices, strict regulations, and strong demand for organic food. The United States plays a central role, with regulatory bodies such as the EPA and USDA promoting eco-friendly crop protection solutions through favorable approval processes and sustainability programs. Organic farming in the region is expanding at an estimated CAGR of 10%, driven by health-conscious consumers and environmental initiatives.

Major agribusiness firms including Bayer AG, BASF SE, and Syngenta AG are actively investing in biological product development and precision agriculture integration. The region also benefits from a strong innovation ecosystem, with companies such as Marrone Bio Innovations and Novozymes launching advanced microbial solutions. Continued investments in digital farming and sustainability will keep North America a high-value and technology-driven market for biopesticides.

Europe Biopesticides Market Trends

Europe is a sustainability-focused and regulation-driven market for biopesticides, with strong demand across Germany, France, the United Kingdom, Spain, and Italy. The European Union’s Green Deal and Farm to Fork Strategy aim to significantly reduce chemical pesticide use by 2030, accelerating the transition toward biological alternatives. Strict enforcement by the European Food Safety Authority and European Chemicals Agency is further encouraging eco-friendly farming practices.

Organic agriculture is expanding rapidly, particularly in Germany and France, while Southern Europe remains a major hub for fruit and vegetable production. Governments across the region are supporting farmers through sustainability subsidies and innovation programs. ESG commitments by food producers and retailers are also boosting demand for residue-free crop protection. Together, these regulatory and consumer-driven forces position Europe as a stable, high-growth region for biopesticide adoption.

Asia Pacific Biopesticides Market Trends

Asia Pacific is the fastest-growing region in the biopesticides market, driven by large agricultural output, supportive government policies, and rising sustainability awareness. Countries such as China, India, Japan, and Southeast Asian nations are rapidly expanding biopesticide use across rice, vegetables, fruits, and plantation crops. China’s green agriculture initiatives and India’s National Mission on Sustainable Agriculture are promoting eco-friendly pest management solutions.

Organic farming is also gaining traction, supported by rising export demand and domestic health awareness. Japan’s advanced horticulture sector is increasingly adopting biological crop protection methods. ASEAN countries are emerging as major producers of specialty crops for global markets, driving further demand. Investments in precision agriculture, digital tools, and smart irrigation are strengthening biopesticide efficiency. These combined factors make Asia Pacific the most dynamic and high-potential region for future market growth.

Competitive Landscape

The global biopesticides market exhibits a moderately consolidated structure, with major global agribusiness firms dominating research, production, and distribution, alongside numerous regional players serving niche markets. Companies such as Bayer AG, BASF SE, Syngenta AG, Novozymes, and Marrone Bio Innovations hold significant market share through strong innovation capabilities and global supply networks. These firms invest heavily in microbial strain development, formulation technologies, and precision agriculture integration to enhance product performance and profitability.

Emerging business models include IPM solution platforms, customized biological blends, and subscription-based advisory services. Sustainability-focused differentiation, such as organic-certified and residue-free products, is becoming a major competitive advantage, especially in Europe and North America. Vertical integration, regulatory expertise, and technological innovation are increasingly defining market leadership. Overall, competition is shifting toward high-value, eco-friendly, and technology-driven solutions across global agriculture.

Key Developments:

- In June 2025: Bayer AG launched BICOTA, a new bioinsecticide designed to help farmers control stem borer pests in rice and other row crops with a single, IPM-compatible application. The product promotes plant health while offering safer pest control.

- In November 2024: BASF SE strengthened its biological crop protection capabilities by acquiring a startup focused on microbial seed and soil treatment solutions. This strategic move expands BASF’s R&D and portfolio reach in sustainable pest-control technologies.

- In January 2023: Syngenta AG entered a precision-agriculture partnership to leverage advanced drone and AI analytics technologies. This collaboration aims to enable more accurate, efficient biopesticide application and strengthen Syngenta’s offerings for large farms and progressive growers.

Companies Covered in Biopesticides Market

- Bayer AG

- DowDuPont

- BASF SE

- Syngenta AG

- Nufarm

- Novozymes

- Rolfes Agri

- Marrone Bio Innovations

- Isagro SpA

- Excel Crop Care Ltd.

- Sikko Industries Ltd.

- Certis USA L.L.C.

- Parry America, Inc.

- Andermatt Biocontrol AG

- Futureco Bioscience S.A.

- Valent BioSciences LLC

- Gujarat State Fertilizers and Chemicals Ltd.

- T.Stanes and Company Limited

- Bioceres Crop Solutions Corp.

- Corteva Agriscience

Frequently Asked Questions

The global Biopesticides Market is valued at US$ 10.2 Billion in 2026 and is projected to reach US$ 20.8 Billion by 2033, growing at a CAGR of 10.7% from 2026 to 2033, with a historical CAGR of 9.4% between 2020 and 2025.

Key demand drivers include shift toward sustainable and organic farming practices, regulatory support, and environmental concerns, which drive adoption of biopesticides in row crops, horticulture, and specialty crops.

The bioinsecticides segment is the leading product type category, capturing 45% of demand due to extensive use in row crops, horticulture, and specialty crops.

North America is the largest regional market for biopesticides, accounting for roughly 38% of global value, driven by strong regulatory support, high adoption of organic farming, and advanced precision‑ag technologies in the United States.

A key opportunity lies in the integration of biopesticides with precision agriculture technologies such as drones and AI‑driven analytics, particularly in North America and Europe, where digital‑transformation initiatives are accelerating.