- Semiconductor Materials & Components

- Passive Components Market

Passive Components Market Size, Share, and Growth Forecast, 2026 - 2033

Passive Components Market by Product (Capacitors, Resistors, Inductors, Transformers, Crystals & Oscillators, Filters, Others), Industry (IT and Telecom, Consumer Electronics, Automotive, Industrial, Aerospace & Defense, Healthcare, Energy & Power, Others), and Regional Analysis for 2026 - 2033

Passive Components Market Size and Trends Analysis

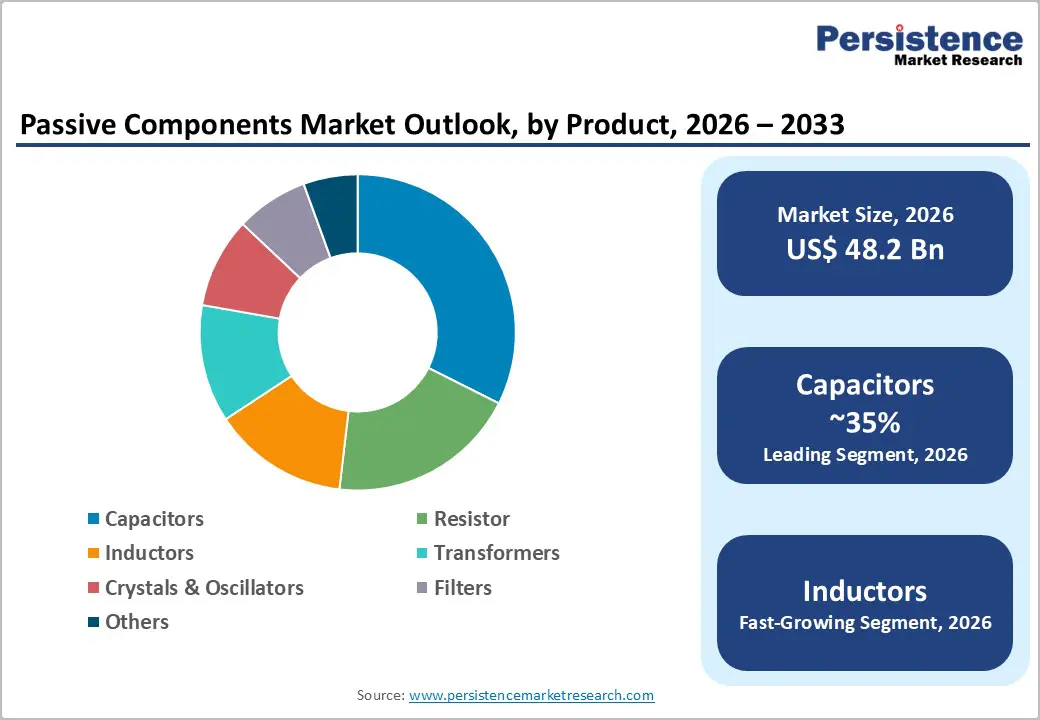

The global passive components market size is projected to rise from US$48.2 billion in 2026 to US$74.3 billion by 2033. It is anticipated to witness a CAGR of 6.4% during the forecast period from 2026 to 2033, driven by the increasing demand for smaller, more energy-efficient, and reliable electronic devices.

EV adoption has risen globally, with advanced electronics needing more capacitors and inductors per vehicle, while IoT and smart devices integrate denser circuits. The industry is experiencing price hikes due to metal price fluctuations, with Taiwanese manufacturers raising costs on tantalum capacitors, now extending to bead inductors, varistors, and NTC thermistors.

Key Industry Highlights:

- Leading Product: Capacitors dominate the market with over 35% share in 2026, valued at more than US$ 17 Bn, driven by their critical role in voltage stabilization, noise filtering, and energy management across consumer electronics, automotive, and industrial applications. Inductors are the fastest-growing segment, with a CAGR of 9.7%, supported by demand for efficient energy storage, electromagnetic interference suppression, and high-power density solutions in compact electronics and renewable energy systems.

- Leading Industry: Consumer Electronics holds the largest share at over 32% in 2026, valued at more than US$ 15.4 Bn, fueled by the proliferation of smartphones, tablets, wearables, and smart home devices requiring reliable, miniaturized passive components. Automotive is the fastest-growing industry, driven by rapid EV adoption and ADAS integration, which require higher quantities of capacitors, resistors, and inductors for power management, signal processing, and energy storage.

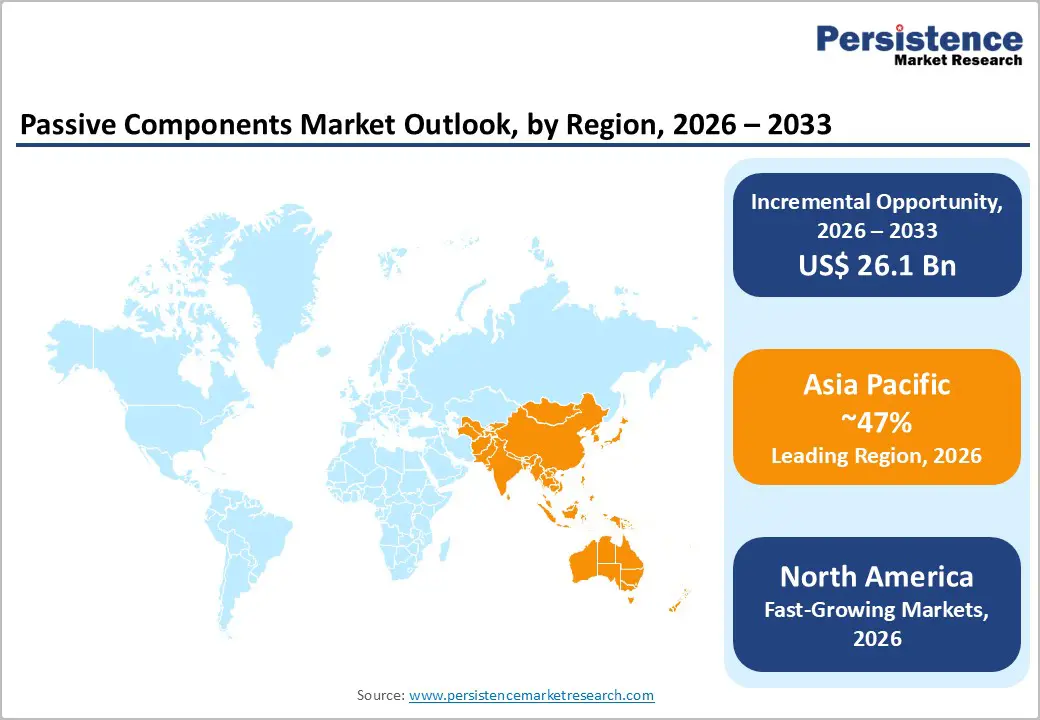

- Leading Region: Asia Pacific leads with over 47% share in 2026, valued at approximately US$ 22.7 Bn, supported by strong semiconductor ecosystems in China, Japan, South Korea, and Taiwan, combined with India’s electronics growth under Make in India and PLI schemes. North America is witnessing significant growth due to EV adoption, 5G rollout, AI infrastructure, and data center expansion, while Europe continues steady expansion driven by industrial and automotive demand, renewable energy integration, and compliance with EU RoHS and REACH directives.

- Key Opportunity: Integration of renewable energy and smart grid infrastructure, along with AI server and HPC expansion, presents strong growth potential for high-performance capacitors, inductors, and resistors capable of supporting high-frequency, high-temperature, and miniaturized applications.

| Key Insights | Details |

|---|---|

| Passive Components Market Size (2026E) | US$48.2 Bn |

| Market Value Forecast (2033F) | US$74.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Dynamics

Driver - IoT Device Proliferation and Miniaturization Demands

The rapid expansion of the global IoT market, projected to exceed 38.7 billion connections by 2030 according to GSMA Intelligence, is fueling demand for ultra-small, low-power, and highly reliable passive components. In 2025 alone, 240 million massive IoT connections were added worldwide as reported by the Ericsson Mobility Report, highlighting the accelerating adoption of connected devices. Applications in wearables, smart home devices, industrial sensors, and medical implants require miniaturized components that can deliver enhanced performance in compact form factors. Innovations such as Murata’s 006003-inch MLCC, measuring 0.16 mm by 0.08 mm and representing a 75 percent reduction in volume compared to previous smallest designs, enable manufacturers to integrate more functionality into smaller devices. This underscores the growing importance of miniaturized passive components as a key enabler for the evolving IoT ecosystem.

Automotive Electrification and Advanced Driver-Assistance Systems (ADAS)

The shift toward electric vehicles (EVs) and advanced driver-assistance systems (ADAS) is driving strong demand for passive components. Global EV sales surpassed 20 million units in 2025, according to a study. As vehicles electrify and integrate advanced electronics, the demand for passive electronic components has surged. For instance, while some of internal combustion engine (ICE) vehicles use around 3,000 MLCCs (multilayer ceramic capacitors), advanced battery electric vehicles use more than 10,000 MLCCs to support power electronics, battery-management systems, and ADAS modules. In Europe, new-car registrations grew modestly by 1.8% in 2025, highlighting continued adoption of electrified and electronically sophisticated vehicles.

Restraint - Raw Material Supply Chain Vulnerabilities and Price Volatility

Raw materials represent the highest variable cost in passive-component manufacturing, making the industry highly sensitive to supply-chain disruptions. Geopolitical tensions, mining or refining constraints, and stringent environmental regulations create significant price volatility and supply uncertainty. For example, before 2022, Ukraine supplied 45-54% of global semiconductor-grade neon gas, highlighting how regional conflicts can disrupt component production and escalate costs. In early 2026, rising silver and copper prices have led manufacturers to issue widespread price-increase notices. Tantalum supply remains structurally tight due to regulatory-sensitive mining in conflict-prone regions like the Democratic Republic of Congo, driving premiums for high-reliability capacitors demanded by AI hardware and defense applications. Such raw material volatility constrains production capacity and limits manufacturers’ ability to meet growing market demand.

Component Shortages and Manufacturing Capacity Constraints

Periodic component shortages and limited manufacturing capacities remain significant restraints in the passive components. Historical events, such as the 2018 global shortage of multilayer ceramic capacitors (MLCCs), saw lead times extend beyond six months, highlighting the vulnerability of supply chains. Rapid technological advancements and fluctuating consumer demand often lead to sudden spikes or drops in requirements, exposing OEMs and EMS providers to excess inventory, production delays, and increased costs. These constraints particularly impact the automotive, consumer electronics, and telecommunications sectors, slowing production schedules and driving component prices higher, which in turn affects overall market growth.

Opportunity - Renewable Energy Integration and Smart Grid Infrastructure

The global shift toward renewable energy and smart grid infrastructure presents significant growth opportunities for passive component manufacturers. Solar PV systems, wind turbines, energy storage solutions, and EV charging networks rely on advanced capacitors, inductors, and transformers for efficient energy conversion, voltage regulation, and power management. Additionally, smart grids demand robust components for sensors, automated switching, and electromagnetic interference suppression. According to the IEA, global renewable power capacity is projected to increase by almost 4,600 GW between 2025 and 2030, with growth in utility-scale and distributed solar PV more than doubling and accounting for nearly 80% of worldwide renewable electricity capacity expansion. This indicates a substantial rise in demand for high-performance passive components.

Artificial Intelligence and High-Performance Computing Expansion

The rapid expansion of AI, data centers, and high-performance computing (HPC) is creating strong demand for specialized passive components. AI servers and HPC systems require high-capacitance, high-reliability MLCCs, inductors, and resistors that operate at elevated temperatures (~105°C), support high-frequency workloads, and ensure stable power delivery with low noise. Miniaturized, high-density components are essential to optimize space and efficiency, particularly for edge AI devices and AI-enabled IoT applications. Samsung Electro-Mechanics reports that state-of-the-art AI servers use over ten times the MLCCs compared to general-purpose servers, highlighting the significant growth potential in this segment.

Category-wise Analysis

Product Insights

Capacitors dominate the market, capturing more than 35% market share in 2026 with a value exceeding US$ 17 Bn, due to their critical role in stabilizing voltage, filtering noise, and managing energy in electronic circuits. Modern devices increasingly rely on them to ensure stable operation and high-speed signal processing. The rise of 5G networks, high-performance computing, and compact IoT devices drives demand for capacitors with high reliability and miniaturized form factors, making them indispensable across industries.

Inductors are expected to grow at a CAGR of 9.7% due to the increasing need for efficient energy storage and filtering in compact electronic devices. They are essential in managing electromagnetic interference and ensuring stable current flow in high-frequency applications. The expansion of advanced electronics and renewable energy systems drives the need for inductors with higher power density and thermal stability, supporting more reliable and efficient device performance. The introduction of diverse inductor geometries and advanced materials enhances performance characteristics, supporting specialized applications.

Industry Insights

Consumer Electronics holds over 32% market share in 2026, with a value exceeding US$ 15.4 Bn, due to the growing demand for smaller, smarter, and more energy-efficient devices. Modern smartphones, tablets, wearables, and smart home appliances require reliable passive components to ensure stable performance, efficient power management, and signal integrity. Rising disposable incomes globally enable consumers to upgrade devices more frequently, sustaining robust demand for high-performance passive components with enhanced efficiency, reliability, and compact form factors.

Automotive is expected to grow at the highest rate due to the rapid adoption of electric vehicles (EVs) and advanced driver-assistance systems (ADAS), which require more capacitors, resistors, and inductors for energy storage, power management, and signal processing. Increasing vehicle electrification, including hybrid and fully electric platforms, drives demand for reliable and compact passive components. Modern cars are integrating infotainment, connectivity, and safety systems, all of which rely heavily on high-performance passive components to ensure stable operation under harsh automotive conditions.

Regional Insights

North America Passive Components Market Trends

North America is expected to grow at a significant rate. The United States leads regional growth supported by electric vehicle adoption, 5G rollout, AI infrastructure, and data center investments. Local production of capacitors and inductors for automotive powertrains and charging, along with military-grade resistors and capacitors for defense modernization, strengthens regional supply chains. Industry 4.0 practices and R&D centers drive technological innovation, while regional sourcing in the U.S. shortens lead times and boosts resilience. According to the U.S. Census Bureau, shipments of electrical equipment, appliances, and components reached $52.1 billion in unfilled orders in July 2025, reflecting sustained demand.

Asia Pacific Passive Components Market Trends

Asia Pacific holds over 47% share in 2026, reaching US$ 22.7 Bn value, driven by dense semiconductor ecosystems in China, Japan, South Korea, and Taiwan. China’s production strength, combined with India’s electronics growth under Make in India and PLI schemes of INR22,919 crore, drives demand across consumer electronics, automotive, and industrial sectors. The rollout of 5G networks and rising electric vehicle adoption intensify the need for compact, high-frequency components. Regional output underscores this leadership: in 2025, China produced 1.27 billion smartphones, 332 million microcomputers, and 484.3 billion integrated circuits, up 10.9% YoY, while Japan’s passive component imports reached ¥17,330 million in July 2025.

Europe Passive Components Market Trends

Europe is experiencing steady expansion, driven by strong demand from its advanced industrial and automotive sectors, with Germany, France, and the UK as major consumption hubs. Germany’s automotive OEMs and Tier 1 suppliers, including Volkswagen AG, BMW AG, Mercedes-Benz Group AG, and Robert Bosch GmbH, create robust demand, especially for electric mobility components under the EU’s 2035 ICE phase-out mandate. The European Chips Act is boosting semiconductor fabrication and associated component ecosystems, while France and Spain are expanding photovoltaics, nuclear, and renewable energy infrastructure, raising the need for high-reliability components. Compliance with EU RoHS and REACH directives further favors certified suppliers, shaping market dynamics and entry barriers.

Competitive Landscape

The global passive components market exhibits a moderately consolidated structure at the premium technology tier, with a handful of Japanese and South Korean manufacturers, along with Taiwanese firms, commanding significant shares in high-value segments such as MLCCs, precision resistors, and high-frequency inductors. Leading players are pursuing vertical integration, geographic manufacturing diversification, and targeted M&A to strengthen competitive moats. Numerous Chinese and other regional Tier 2 and Tier 3 suppliers compete aggressively in commodity segments, sustaining price pressure. R&D investment is increasingly focused on miniaturization, high-temperature performance, and embedded passive integration to address next-generation semiconductor packaging requirements.

Key Industry Developments:

- In July 2025, TDK Corporation expanded its TFM201612BLEA series of thin-film power inductors for automotive circuits, offering higher currents up to 5.6 A and improved efficiency with 31% lower DC resistance. Mass production began in July 2025, supporting compact, high-reliability applications in EVs and ADAS under high-temperature conditions.

- In June 2025, Murata launched the world’s first 0805-inch (2.0 × 1.25 mm) automotive MLCC offering 10µF at 50V, designed for ADAS and autonomous driving systems. The compact capacitor provides 2.1× higher capacitance than Murata’s previous 4.7µF/50V 0805 MLCC and saves ~53% PCB space compared to the 1206-inch 10µF/50V version.

Companies Covered in Passive Components Market

- KEMET Corp.

- KYOCERA AVX Components Corp

- Murata Manufacturing Co. Ltd.

- NICHICON Corp

- Nippon Chemi Con Corp

- Panasonic Corp

- Ryosan Co

- Samsung Electro Mechanics Co. Ltd

- TAIYO YUDEN CO. LTD.

- Yageo Corporation

- TDK Corporation

- AVX Corporation

- Others

Frequently Asked Questions

The global market is projected to be valued at US$48.2 Bn in 2026.

Growing demand for miniaturized, energy-efficient, and high-reliability devices that require stable power management, signal integrity, and thermal performance is a key driver of the market.

The passive components market is expected to witness a CAGR of 6.4% from 2026 to 2033.

The rapid adoption of electric vehicles, AI, and high-performance computing, which require advanced, high-reliability components, is creating strong growth opportunities.

KEMET Corp., KYOCERA AVX Components Corp, Murata Manufacturing Co. Ltd., NICHICON Corp, Nippon Chemi Con Corp, Panasonic Corp, Ryosan Co are among the leading key players.