- Pharmaceuticals

- Parkinson's Disease Drugs Market

Parkinson's Disease Drugs Market Size, Share, and Growth Forecast 2026 - 2033

Parkinson's Disease Drugs Market by Drug Class (Levodopa-based Formulations, Dopamine Agonists, MAO-B Inhibitors, COMT Inhibitors, Anticholinergics, Adenosine A2A Receptor Antagonists, Others), Route of Administration (Oral, Transdermal (Patches), Inhalation, Others), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Others), and Regional Analysis, 2026 - 2033

Parkinson's Disease Drugs Market Size and Trend Analysis

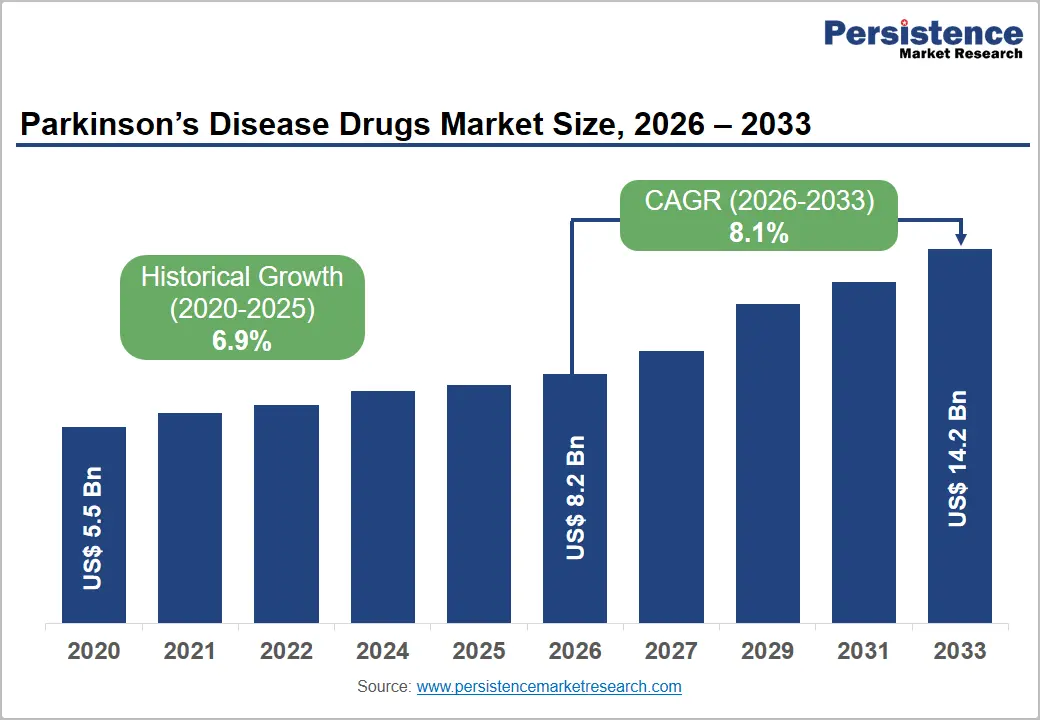

The global parkinson's disease drugs market size is expected to be valued at US$ 8.2 billion in 2026 and projected to reach US$ 14.2 billion by 2033, growing at a CAGR of 8.1% between 2026 and 2033. This robust growth trajectory is underpinned by the rapidly expanding global Parkinson's disease patient population, driven by aging demographics worldwide.

The World Health Organization (WHO) estimates that over 8.5 million individuals were living with Parkinson's disease globally in 2019, a figure projected to more than double by 2040 as populations age. Escalating disease awareness, expanding access to specialist neurology care across emerging economies, and a prolific pipeline of novel disease-modifying and symptomatic therapies, including adenosine A2A receptor antagonists and advanced levodopa delivery formulations, are collectively accelerating drug adoption and sustaining above-average revenue growth rates throughout the forecast period.

Key Industry Highlights:

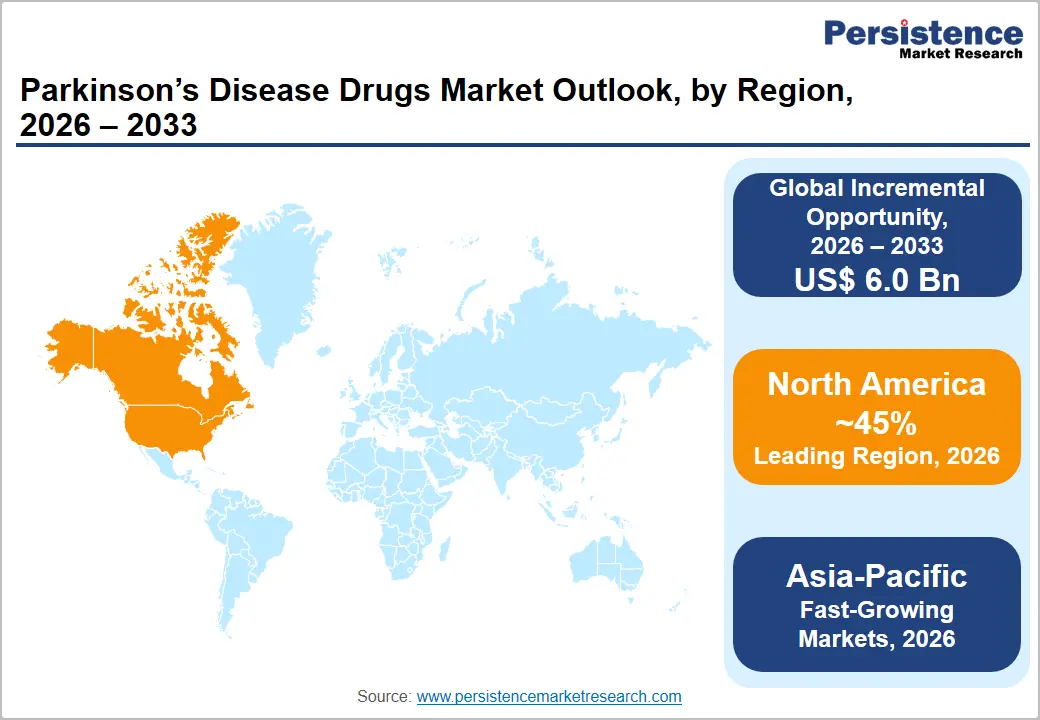

- Leading Region: North America dominates the global Parkinson's Disease Drugs market with approximately 45% revenue share in 2025, driven by U.S. Medicare Part D reimbursement, Parkinson's prevalence projected to exceed 1.2 million by 2030 per the Parkinson's Foundation, and early commercial access to premium branded formulations.

- Fast-growing Market: Asia Pacific is the fast-growing regional market, propelled by China's 3 million+ Parkinson's patients, rapidly aging populations across Japan, South Korea, and India, and expanding specialist neurology infrastructure enabling earlier diagnosis and pharmacological treatment initiation.

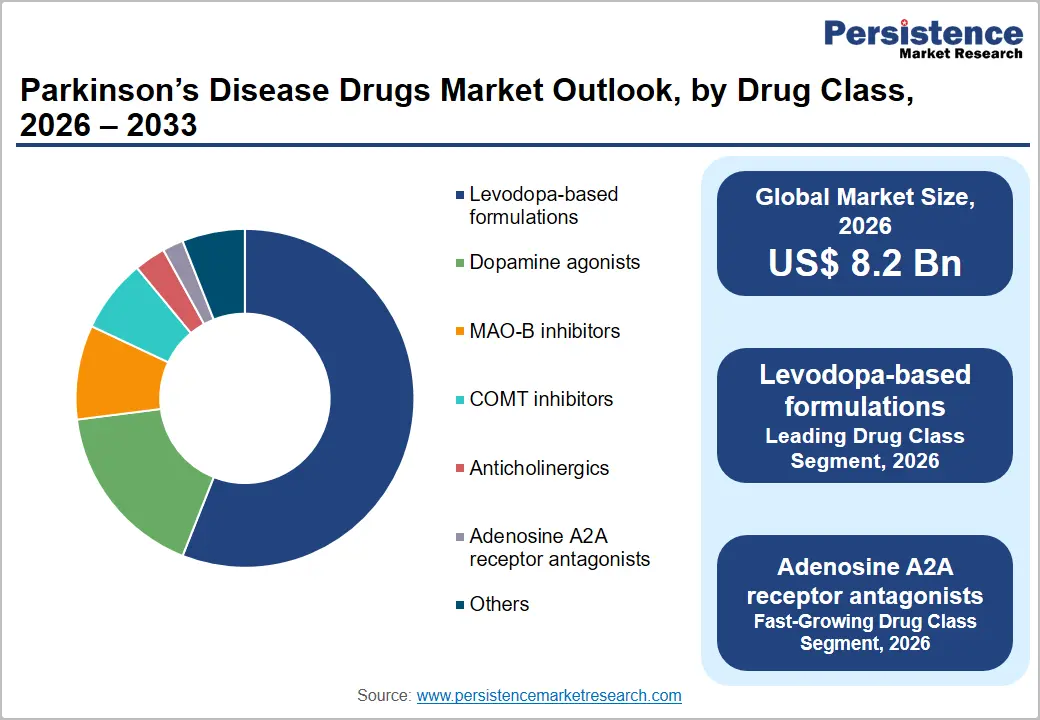

- Dominant Drug Class: Levodopa-based formulations dominate the drug class category with approximately 56% global market share in 2025, anchored by five decades of clinical gold-standard status, AAN and MDS guideline-driven prescribing mandates, and premium revenue from proprietary extended-release and advanced delivery platform formulations.

- Fast-growing Drug Class: Adenosine A2A receptor antagonists represent the fastest-growing drug class through 2033, led by FDA-approved istradefylline (Nourianz), offering a novel non-dopaminergic mechanism for OFF-episode reduction that addresses key limitations of existing adjunct dopaminergic therapies in advanced Parkinson's management.

- Opportunity: Advanced delivery technologies including inhaled levodopa (Inbrija) and transdermal rotigotine (Neupro) represent the highest-value commercial opportunity, addressing the 40%+ of chronic levodopa patients experiencing disabling OFF episodes and commanding substantial price premiums over genericized oral formulations.

Market Dynamics

Drivers - Rapidly Aging Global Population Expanding the Parkinson's Disease Patient Base

The single most powerful structural driver of Parkinson's disease drugs market growth is the accelerating aging of the global population. Age is the most significant non-genetic risk factor for Parkinson's disease, with incidence rising sharply after age 60. The United Nations Department of Economic and Social Affairs projects that the global population aged 60 years and over will reach 2.1 billion by 2050, up from 1 billion in 2020.

The Parkinson's Foundation estimates that approximately 90,000 Americans are newly diagnosed each year, with the overall U.S. prevalence expected to exceed 1.2 million by 2030. In Europe, the European Parkinson's Disease Association (EPDA) estimates that over 1.2 million Europeans currently live with Parkinson's, a figure that will expand substantially as the continent's population ages, creating an ever-widening addressable market for pharmacological therapies.

Restraints - Generic Drug Competition Eroding Brand Revenues for Established Therapies

The widespread genericization of core Parkinson's pharmacotherapies including levodopa/carbidopa, pramipexole, ropinirole, and rasagiline has significantly compressed average selling prices across the largest-volume drug segments. A 2023 analysis by the IQVIA Institute for Human Data Science documented that generic penetration rates in established neurology drug categories routinely exceed 85-90% within 24 months of patent expiry. This price erosion reduces revenue per prescription for major pharmaceutical incumbents and creates sustained downward pressure on market revenue growth rates within mature drug classes, requiring manufacturers to increasingly depend on differentiated extended-release formulations, novel delivery systems, and pipeline-stage compounds to sustain portfolio revenue growth.

Opportunities - Adenosine A2A Receptor Antagonists: Fastest-Growing Drug Class with Substantial Untapped Potential

Adenosine A2A receptor antagonists represent the fastest-growing drug class in the Parkinson's disease drugs market, positioned at the intersection of unmet clinical need and novel mechanism-of-action differentiation. Istradefylline, marketed as Nourianz by Eisai in the United States following FDA approval in 2019, demonstrated clinically meaningful reductions in daily OFF-time in pivotal Phase III trials without worsening dyskinesia, addressing a critical limitation of dopaminergic add-on therapies.

Post-approval prescribing uptake has been accelerating as neurologists gain experience with the class, and multiple next-generation A2A antagonists are in mid-to-late stage clinical development globally. The European Medicines Agency (EMA) review of istradefylline and the class's potential expansion into earlier treatment lines represent significant near-term commercial catalysts that could materially expand the A2A antagonist revenue base through the 2033 forecast horizon.

Category-wise Analysis

Drug Class Insights

Levodopa-based formulations dominate the Parkinson's Disease Drugs market by drug class, likely toi command approximately 56% of global revenue in 2026. This entrenched leadership reflects levodopa's unmatched efficacy as the gold-standard symptomatic therapy for Parkinson's disease, a clinical position it has maintained for over five decades since its original introduction.

The American Academy of Neurology (AAN) and Movement Disorder Society (MDS) guidelines universally recommend levodopa/carbidopa as the cornerstone of pharmacological management for most Parkinson's patients at all disease stages. Despite extensive genericization of standard immediate-release formulations, manufacturers continue to generate significant revenues from proprietary extended-release platforms (e.g., Rytary by AbbVie Inc.), intestinal gel delivery systems (Duopa/Duodopa), and novel carbidopa/levodopa combination formulations that command premium pricing by addressing motor fluctuations in advanced disease.

Route of Administration Insights

The oral route of administration leads the Parkinson's Disease Drugs market with approximately 72% revenue share in 2026, reflecting the overwhelming prevalence of oral tablet and capsule formulations across all major Parkinson's drug classes. The oral route's dominance is supported by the availability of virtually all first-line and adjunct Parkinson's therapies including levodopa/carbidopa, dopamine agonists, MAO-B inhibitors, and COMT inhibitors in oral forms with well-established clinical protocols.

Patient familiarity, ease of self-administration, and the availability of generic oral formulations at low cost reinforce oral administration as the standard prescribing default across primary and specialist neurology practice globally. Oral extended-release formulations such as Rytary (carbidopa/levodopa ER) and Mirapex ER (pramipexole ER) sustain premium revenue contribution within the oral segment by offering differentiated pharmacokinetic profiles over immediate-release generics.

Regional Insights

North America Parkinson's Disease Drugs Market Trends and Insights

North America dominates the Parkinson’s Disease Drugs market due to high diagnosis rates, advanced neurology infrastructure, and strong insurance-driven drug access. The region benefits from high specialist density and early adoption of advanced dopaminergic and infusion-based therapies. Aging demographics are a major driver, with the U.S. Census Bureau projecting rapid growth in the 65+ population, directly increasing Parkinson’s prevalence.

U.S. Parkinson's Disease Drugs Market Trends and Insights

The United States is the leading country in the region and is expected to reach US$ 3.4 Bn by 2026. According to CDC estimates, nearly 90,000 new Parkinson’s cases are diagnosed annually, with prevalence significantly increasing among individuals above 60 years. Strong Medicare reimbursement, NIH-funded research programs, and widespread availability of advanced therapies such as levodopa-carbidopa intestinal gel and inhalation rescue treatments support market growth. High neurologist density, strong patient advocacy networks, and robust clinical trial participation further accelerate adoption of MAO-B inhibitors and dopamine agonists.

Canada Parkinson's Disease Drugs Market Trends and Insights

Canada is the fastest growing country in the region, expected to grow at ~8.6% CAGR, supported by Public Health Agency of Canada data indicating a rising neurodegenerative disease burden and a rapidly aging population projected to reach nearly 25% seniors by 2030. Expansion of tele-neurology, improved access to dopamine agonists and MAO-B inhibitors, and growing rural healthcare penetration are strengthening treatment adoption. Mexico shows steady growth supported by expanding public neurology services, increasing use of generic Levodopa-based therapies, and gradual improvements in early diagnosis and hospital infrastructure.

Europe Parkinson's Disease Drugs Market Trends and Insights

Europe is a key region due to strong public healthcare systems, universal coverage, and structured neurological disease management programs. EU-wide aging trends significantly increase Parkinson’s prevalence, supported by Eurostat data showing one of the oldest population structures globally. Clinical guideline adherence ensures high uptake of both Levodopa and adjunct therapies.

Germany Parkinson's Disease Drugs Market Trends and Insights

Germany is the leading country in Europe and is expected to reach US$ 1.8 Bn by 2026. Federal Statistical Office data indicates that over 22% of the population will be aged 65+ by 2030, significantly increasing Parkinson’s burden. The country benefits from strong hospital infrastructure, high neurologist density, and comprehensive reimbursement under statutory health insurance. Widespread adoption of COMT inhibitors, MAO-B inhibitors, and combination therapies is supported by advanced movement disorder centers, strong clinical research participation, and high healthcare expenditure.

UK Parkinson's Disease Drugs Market Trends and Insights

The United Kingdom is expected to achieve a fast-growth in Europe at ~8.4% CAGR, driven by NHS-led early diagnosis initiatives and increasing neurological consultations. Rising adoption of MAO-B inhibitors in early-stage therapy, expansion of tele-neurology services, strong patient registry systems, and improved access to rescue therapies are accelerating growth. France contributes stable growth supported by universal healthcare coverage, high Levodopa penetration, structured geriatric care systems, and expanding chronic disease reimbursement programs.

Asia Pacific Parkinson's Disease Drugs Market Trends and Insights

Asia Pacific is the fast-growing market due to rapidly aging population, increasing disease awareness, and expanding healthcare infrastructure. WHO regional data indicates significant growth in neurological disorders in countries like China, Japan, and India, driven by longer life expectancy and improved diagnosis rates.

China Parkinson's Disease Drugs Market Trends and Insights

China is the leading country in the region and is expected to reach US$ 2.1 Bn by 2026. According to China’s National Health Commission, over 2.5 million Parkinson’s patients are estimated, with rising prevalence driven by aging demographics. Expansion of tier-2 and tier-3 hospital networks, increasing insurance reimbursement coverage, and strong domestic pharmaceutical manufacturing are improving access to Levodopa-based and dopamine agonist therapies. Government initiatives focused on chronic neurological disease management are further supporting demand growth.

India Parkinson's Disease Drugs Market Trends and Insights

India is the fast-growing market in Asia-Pacific, expected to reach at ~9.2% CAGR, driven by rising diagnosis rates, increasing geriatric population, and improving access to neurology care. ICMR reports growing neurological disease burden, although underdiagnosis remains high. Expansion of private neurology hospitals, rapid growth in generic Parkinson’s drug usage, increasing awareness campaigns, and urban healthcare infrastructure development are accelerating market penetration.

Japan represents a mature high-value market with over 29% of the population aged above 65, supported by high healthcare expenditure, advanced rehabilitation systems, and strong adoption of transdermal and infusion-based therapies.

Competitive Landscape

The global Parkinson's disease drugs market exhibits a moderately consolidated competitive structure, with AbbVie Inc., UCB S.A., Supernus Pharmaceuticals, and Teva Pharmaceutical Industries among the prominent commercial leaders in branded Parkinson's drug portfolios. Key differentiators include proprietary extended-release formulations, advanced delivery technologies (transdermal, inhalation, intestinal infusion), and clinical pipeline depth in non-dopaminergic mechanisms. Major generic pharmaceutical manufacturers including Teva and Mylan compete intensively on established oral formulations.

Emerging competitive strategies encompass disease-modifying therapy development, digital therapeutics integration for motor symptom tracking, and direct-to-neurologist education programs. R&D investment is increasingly focused on alpha-synuclein, LRRK2, and GLP-1 pathways targeting disease modification rather than symptomatic management alone.

Key Developments

- In July 2025: Scientists from the University of South Australia developed a long-acting injectable formulation that delivers two key Parkinson’s medications for an entire week. They tested an injectable gel implant that combines an FDA-approved biodegradable substance with a pH-sensitive substance. The team found that the gel gradually released the key Parkinson's medications over one week.

- In July 2025: Neuraxpharm joined hands with Dizlin Pharmaceuticals to accelerate Dizlin’s Infudopa SubC drug-device combination therapy. It enables continuous levodopa-carbidopa delivery in people with advanced Parkinson’s disease.

Companies Covered in Parkinson's Disease Drugs Market

- AbbVie Inc.

- Boehringer Ingelheim Intl. GmbH

- F. Hoffmann-La Roche Ltd.

- Novartis AG

- Pfizer Inc.

- Teva Pharmaceutical Industries Ltd.

- UCB S.A.

- Supernus Pharmaceuticals, Inc.

- Lundbeck A/S

- Others

Frequently Asked Questions

The global Parkinson's disease drugs market is estimated to be valued at US$ 8.2 billion in 2026.

Aging population, rising Parkinson’s prevalence, improved diagnosis, expanding therapy access, and advancing dopaminergic drug development.

North America is the leading region with approximately 45% global revenue share in 2025.

Disease-modifying therapies, gene therapy advances, personalized medicine, and novel non-dopaminergic treatment development expansion.

AbbVie Inc., Boehringer Ingelheim Intl. GmbH, F. Hoffmann-La Roche Ltd., Novartis AG, Pfizer Inc.