- Bulk Chemicals

- Oxo Alcohol Market

Oxo Alcohol Market Size, Share, and Growth Forecast, 2026 - 2033

Oxo Alcohol Market by Product Type (N-Butanol, 2-Ethyl Hexanol, Isobutanol), Application (Acrylates, Glycol Ethers, Acetates, Resins, Plasticizers, Solvents), and Regional Analysis for 2026 - 2033

Oxo Alcohol Market Share and Trends Analysis

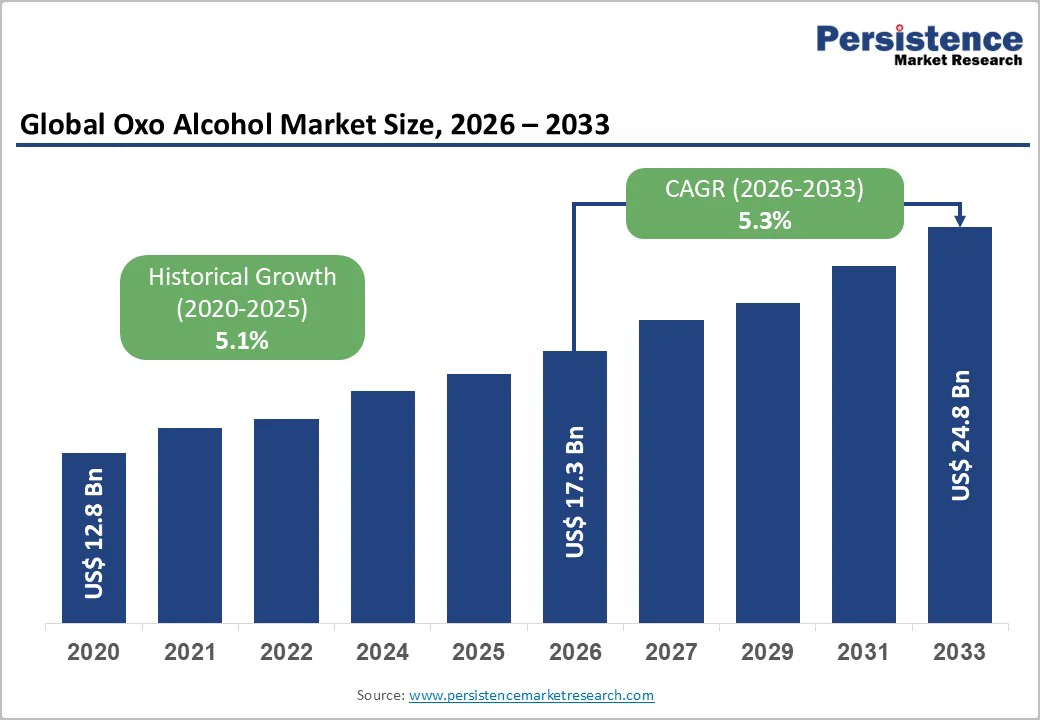

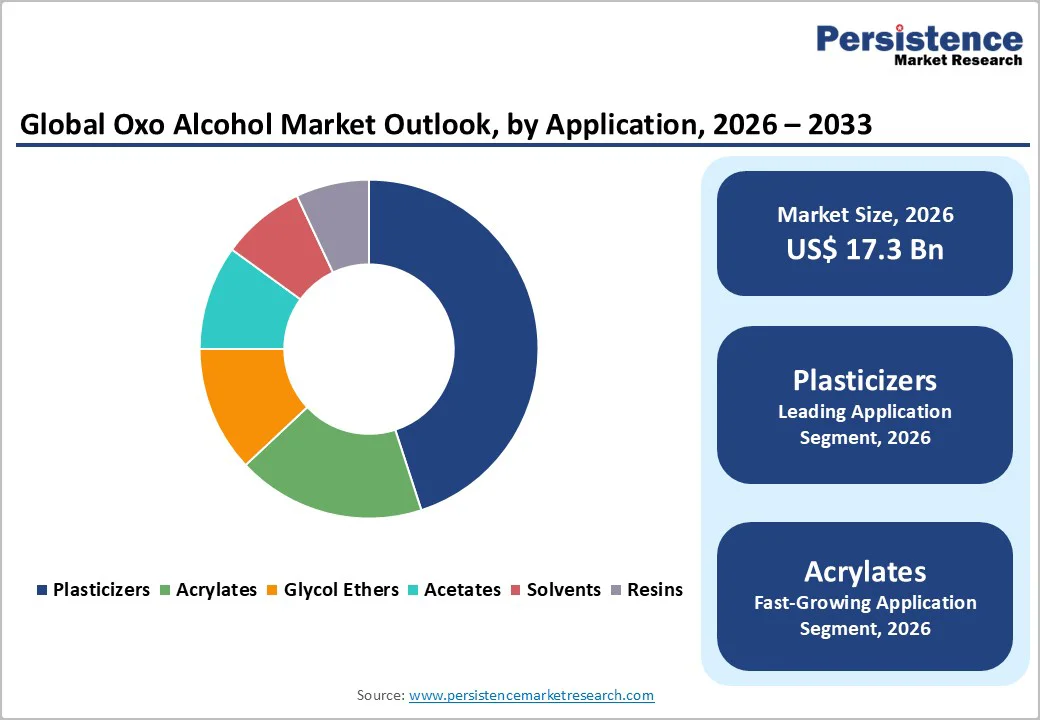

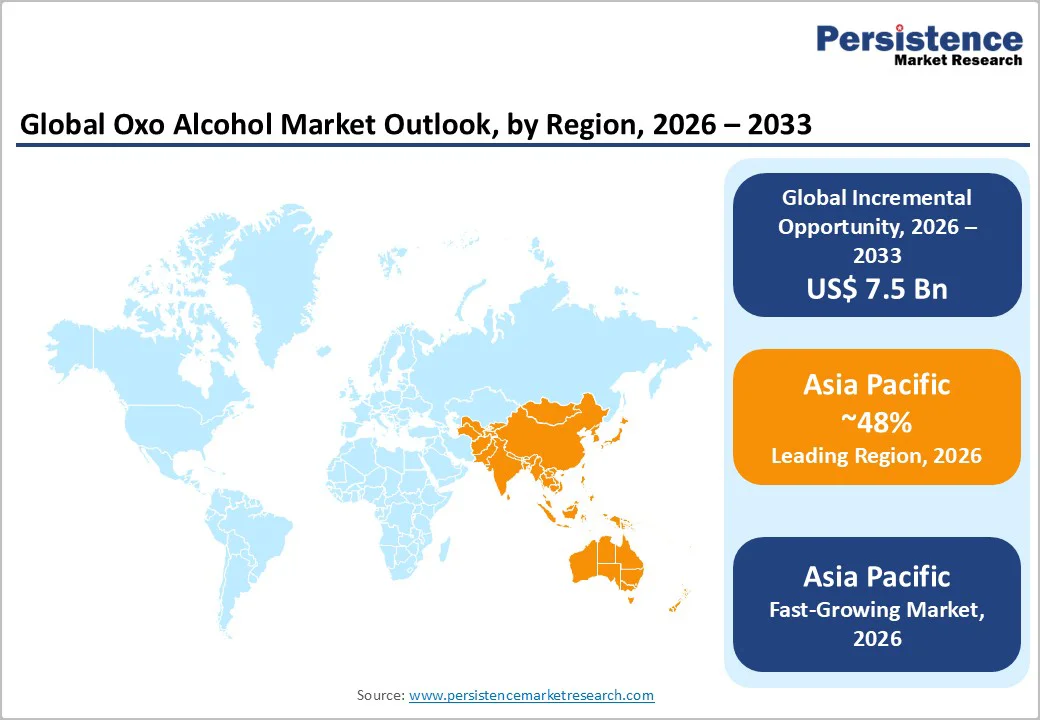

The global oxo alcohol market is estimated to be valued at US$17.3 billion in 2026 and is projected to reach US$24.8 billion by 2033, growing at a CAGR of 5.3% during the forecast period 2026 - 2033.

The growth of this market is fueled by consistent demand for downstream derivatives, such as plasticizers, acrylates, and glycol ethers, which remain essential across the construction, automotive, and packaging sectors. Rising industrial output in emerging economies and steady utilization in coatings and chemical formulations reinforce market stability. Regulatory shifts encouraging lower-VOC solvent systems also contribute to structural demand resilience.

Key Industry Highlights

- Dominant Region: Asia Pacific is expected to lead with about 48% share in 2026, driven by strong chemical infrastructure and downstream integration.

- Fastest-growing Regional Market: Asia Pacific is expected to be the fastest-growing market through 2033, aided by industrial expansion, high demand for sustainable chemicals, and smart plant integration.

- Leading Application: Plasticizers are expected to lead the oxo alcohol market in 2026, with a 45% share, driven by high demand in the flexible PVC, polymer, construction, packaging, and electrical industries.

- Fastest-growing Application: The acrylates segment is expected to grow fastest from 2026 to 2033, boosted by rising demand for eco-friendly, high-performance formulations across industries.

| Key Insights | Details |

|---|---|

| Oxo Alcohol Market Size (2026E) | US$17.3 Bn |

| Market Value Forecast (2033F) | US$24.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Plasticizers and Acrylates

Rising demand for plasticizers and acrylates acts as a key market driver due to their expanding role in performance-focused manufacturing. Plasticizer consumption is accelerating as industries move toward flexible PVC for wires, flooring, packaging films and automotive interiors, pushing suppliers to secure stable volumes of N-butanol and 2-ethylhexanol as core inputs.

Producers emphasize these Oxo-based alcohols for their efficiency in achieving consistent viscosity, durability and processing stability across high-volume applications. This deep integration into downstream value chains strengthens long-term purchasing commitments and elevates the need for reliable feedstock availability.

Acrylate-oriented growth is shaped by the accelerating need for high-performance coatings, adhesives and construction chemicals in urban development and industrial renovation activities. Oxo-derived alcohols function as essential building blocks in acrylic esters used to enhance drying speed, weather resistance and adhesion quality in advanced formulations.

Expanding infrastructure upgrades, protective coating applications and rising demand for specialty adhesives support wider adoption of acrylate systems, elevating the requirement for dependable alcohol inputs. This consistent pull from fast-evolving downstream segments positions oxo-based intermediates as critical enablers of innovation-driven manufacturing, strengthening their strategic relevance across diversified industrial environments.

Feedstock Price Volatility and Supply Chain Constraints

Feedstock price volatility is a key restraint, as production relies on petrochemical inputs whose prices fluctuate with movements in crude oil and gas. These fluctuations create margin compression, disrupt cost forecasting and reduce operational flexibility.

Sudden changes in raw material costs compel producers to adjust output plans, alter procurement cycles and revise pricing structures, which introduces instability across the value chain. Such unpredictability makes it difficult to maintain consistent operating performance and weakens short-term financial visibility for manufacturers.

Supply chain constraints reinforce this pressure by affecting access to feedstock, transport capacity and essential intermediates. Port congestion, geopolitical disruptions, and irregular cargo availability extend lead times and limit delivery reliability.

These challenges restrict producers from sustaining steady supply commitments and reduce customer confidence in long-term arrangements. The combined effect slows production efficiency, impacts working-capital discipline and creates barriers to strategic growth.

Technological Convergence and Process Innovation

Technological convergence and process innovation represent a key opportunity as integrated production systems create stronger control over catalysts, feedstock flows, and reaction pathways. Digital tools working alongside core chemical processes raise efficiency, stabilize product consistency, and support faster adjustments during continuous operations.

Smart monitoring and advanced purification methods strengthen operational reliability and reduce variability in large plants. These improvements reinforce margins and position producers to manage rising performance expectations across global supply networks.

Process innovation also enables flexible feedstock planning, higher throughput, and cleaner manufacturing routes that align with evolving customer requirements. Modern reactor designs, modular process units, and AI-supported decision environments deliver scalable advantages for product lines linked to plasticizers, coatings, and specialty intermediates.

Producers gain competitive strength as innovation elevates cost discipline, improves process visibility, and supports rapid adaptation to market shifts. The opportunity becomes strategic as technology-driven upgrades transform traditional production setups into efficient systems that support long-term commercial resilience and portfolio growth.

Category-wise Analysis

Product Type Insights

N-Butanol is likely to command overwhelming market dominance with an estimated 42% of the oxo alcohol market revenue share in 2026, with its position strengthened by its indispensability across high-volume, capital-intensive industries including construction, coatings, and packaging.

Its extensive integration into acrylates, acetates, and glycol ether production chains has created powerful network effects and supplier lock-in dynamics, while established manufacturing infrastructure and cost competitiveness provide durable competitive moats that insulate it from near-term displacement.

This incumbent advantage translates to predictable, stable cash flows for producers, though growth prospects remain constrained by market maturity and limited opportunities for disruptive application expansion in legacy end-markets.

2-Ethylhexanol is projected to achieve the highest CAGR from 2026 to 2033. This acceleration is driven by a structural market shift toward non-phthalate plasticizers, a regulatory-mandated transition that elevates demand for Dioctyl Terephthalate (DOTP) and alternative chemistries where 2-EH serves as a critical building block.

Rapid infrastructure development in emerging economies, coupled with accelerating automotive electrification and the expansion of the construction sector, creates a favorable demand tailwind that positions 2-EH as the most dynamic growth vector within the oxo alcohol ecosystem, offering early-mover producers premium valuations and market share capture opportunities in the fastest-growing segment through 2033.

Application Insights

Plasticizers are anticipated to maintain dominance in the oxo alcohol market revenues at an estimated 45% in 2026, serving as the foundational feedstock for flexible PVC and other high-volume polymer manufacturing processes.

Their mission-critical role in construction, especially for flooring and pipes, packaging films, and electrical cabling creates unmatched scale economies and supply chain entrenchment, reinforced by mature infrastructure and predictable demand from infrastructure megatrends.

This segment's stability provides producers with reliable revenue visibility, though pricing power remains constrained by commodity-like market dynamics and regulatory pressures toward non-phthalate alternatives.

Acrylates are expected to be the fastest-growing application area from 2026 to 2032, driven by surging demand for advanced coatings, adhesives, and textiles prioritizing performance, durability, and sustainability.

Construction sector expansion, automotive lightweighting, and the shift toward water-resistant, eco-friendly formulations create a perfect demand storm, positioning oxo-alcohol-derived acrylates as indispensable enablers of next-generation materials science.

This dynamic segment offers producers superior margin expansion through premium pricing, technological differentiation, and exposure to high-growth end-markets, fundamentally reshaping competitive positioning for those who invest ahead of the curve in capacity and innovation.

Regional Insights

North America Oxo Alcohol Market Trends

North America is slated to maintain commanding presence in 2026 in the oxo alcohol market landscape, anchored by world-class production hubs across the U.S. and Canada that benefit from unparalleled chemical infrastructure integration and proximity to massive downstream polymer, coating, and packaging ecosystems.

Robust demand from automotive, construction, and packaging sectors, coupled with reliable feedstock access and mature supply chains, creates predictable consumption patterns for N-butanol and 2-ethylhexanol derivatives, delivering producers stable margins through scale economies and regional self-sufficiency. This entrenched positioning insulates North American capacity from global volatility while supporting consistent capacity utilization rates.

The regional market is also expected to accelerate through the strategic adoption of alternative plasticizers, specialty chemicals, and eco-compliant formulations, propelled by aggressive investments in plant modernization, process optimization, and energy-efficient technologies.

Regulatory alignment with stringent environmental standards incentivizes high-performance oxo alcohols tailored for advanced coatings, adhesives, and industrial applications, opening premium pricing opportunities in a steadily growing market.

This dual-track evolution in the form of mature volume leadership and innovation-led expansion positions stakeholders in North America to capture disproportionate value as global sustainability mandates reshape chemical demand dynamics.

Europe Oxo Alcohol Market Trends

Europe is anticipated to command a substantial oxo alcohol market share in 2026, underpinned by world-class chemical facilities in Germany, France, and Italy that deliver unmatched production efficiency and seamless integration with sophisticated downstream coatings, adhesives, and plasticizer ecosystems.

Stringent quality standards, mature supply chains, and stable demand from automotive, construction, and packaging sectors ensure consistent consumption of critical derivatives, creating predictable revenue streams for incumbents despite global volatility.

Regulatory frameworks such as the European Union (EU) Green Deal have the potential to speed up market expansion by mandating eco-friendly, non-phthalate plasticizers and emission reductions, compelling manufacturers to pioneer energy-efficient processes, advanced catalysts, and bio-based alternatives that enhance yields while meeting compliance imperatives.

Surging demand for high-performance acrylates in specialty coatings and adhesives, driven by infrastructure renewal and automotive electrification, creates premium pricing opportunities, enabling agile producers to gain larger ground in the market.

Asia Pacific Oxo Alcohol Market Trends

Asia Pacific is forecasted to decisively dominate with an estimated 48% of the oxo alcohol market share in 2026, powered by the widespread presence of massive chemical production complexes in China, India, and Japan that deliver unmatched economies of scale.

Seamless vertical integration with high-volume flexible PVC, coatings, and plasticizer ecosystems, combined with structural cost advantages in labor and feedstock, creates formidable competitive barriers. At the same time, urbanization megatrends and infrastructure booms sustain relentless demand pull from proximate end-markets, achieving capacity utilization rates often exceeding 90%.

Being the fastest-expanding regional market with a projected CAGR of around 7% through 2033, Asia Pacific’s trajectory can get a boost via explosive investments in infrastructure, automotive, and packaging alongside regulatory pivots toward sustainable, non-phthalate intermediates and smart chemical plants.

Policy incentives, energy-efficient process upgrades, and specialty acrylate demand position manufacturers to capture premium margins in eco-compliant applications, transforming the region from volume leader to an innovation pioneer.

Competitive Landscape

The global oxo alcohol market structure exhibits moderate consolidation, where BASF, Dow, ExxonMobil, Eastman, LG Chem, and Evonik together command approximately 45% of the revenue share through integrated operations, proprietary hydroformylation technologies, and global distribution dominance.

Competition centers on pricing discipline, supply reliability amid feedstock volatility, and differentiation via superior performance specifications, regulatory compliance, and customized derivatives, creating high barriers to entry for new entrants while rewarding incumbents with predictable scale-driven margins and customer lock-in across petrochemical value chains.

Asia Pacific intensifies competitive pressure through aggressive capacity expansions by Chinese and Indian manufacturers capitalizing on cost advantages to capture surging regional demand, potentially eroding pricing power for commodity-grade oxo alcohols.

Players in North America and Europe prioritize technological differentiation to defend premium positioning, achieving higher margins amid stringent sustainability mandates. This bifurcated strategy landscape favors vertically integrated majors who balance volume growth in APAC with innovation-led profitability in mature markets.

Key Industry Developments

- In October 2025, BASF's announced that its SYNSPIRE G1-110 catalyst, installed at Nan Ya Plastics' 2-Ethyl Hexanol (2-EH) Mailiao plant in early 2024, has reduced annual steam consumption by 40,000 metric tons and avoided 38,000 metric tons of CO2 emissions through superior methane/CO2 reforming under dry conditions and carbon deactivation resistance.

- In September 2025, a new Rs 5,894 crore plant at IndianOil’s Gujarat Refinery in Vadodara was inaugurated to produce acrylics and oxo-alcohols, including n-butanol, converting refinery byproduct propylene into high-value chemicals.

- In May 2025, European oxo alcohols prices plunged to multi-month lows due to weak derivative demand from coatings and plasticizers, exacerbated by automotive and construction slowdowns, propylene price drops, and oversupply. The "coatings season" failed to materialize, Turkish exports lost to cheaper US/Asian material, and n-butanol held relatively stronger amid balanced supply.

Companies Covered in Oxo Alcohol Market

- BASF SE

- DowDuPont

- ExxonMobil Corporation

- Eastman Chemical Company

- Sasol

- LG Chem

- China Petrochemical Corporation

- Formosa Plastics Corporation

- Ineos

- Grupa Azoty ZAK SA

- Sinopec

- SABIC

Frequently Asked Questions

The global oxo alcohol market is projected to reach US$ 17.3 billion in 2026.

Rising demand for plasticizers, solvents, and acrylic derivatives across construction, automotive, and industrial manufacturing sectors is driving the market.

The market is poised to witness a CAGR of 5.3% from 2026 to 2033.

Industrial growth in Asia Pacific, increasing adoption of non-phthalate plasticizers, and technological advancements in catalyst efficiency and low-VOC production are key market opportunities.

Key players in the market include BASF SE, DowDuPont, ExxonMobil, Eastman Chemical, Sasol, and LG Chem, among others.