- Plastics, Polymers & Resins

- Non-Chlorinated Polyolefins Market

Non-Chlorinated Polyolefins Market Size, Share, and Growth Forecast 2026 - 2033

Non-Chlorinated Polyolefins Market by Polymer Type (Polyethylene, Polypropylene, Polystyrene, Other), Application (Plastics, Paints & Coatings, Adhesives, Rubber, Other), End-use Industry (Automotive, Packaging, Electrical & Electronics, Building & Construction, Other), and Regional Analysis for 2026-2033

Non-Chlorinated Polyolefins Market Size and Trend Analysis

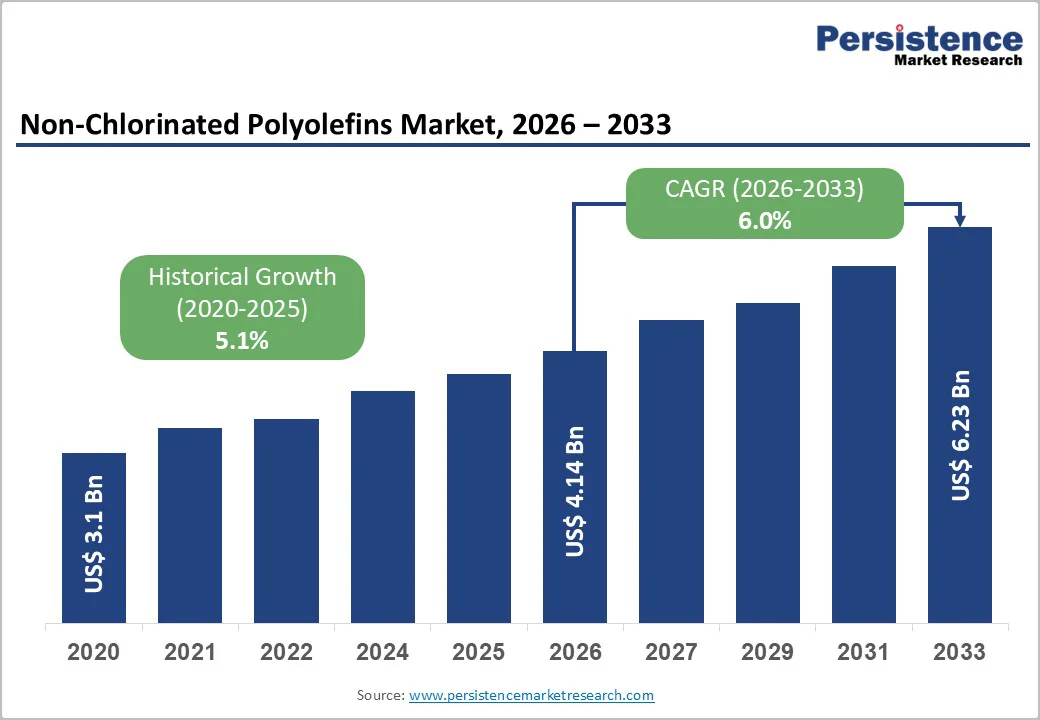

The global Non-Chlorinated Polyolefins market size is supposed to be valued at US$ 4.1 Bn in 2026 and is projected to reach US$ 6.2 Bn by 2033, growing at a CAGR of 6.0% between 2026 and 2033.

The market trajectory is primarily driven by the escalating demand for environmentally sustainable adhesion promoters in the automotive and packaging industries. As regulatory bodies across North America and Europe tighten restrictions on volatile organic compounds (VOCs) and halogenated materials, manufacturers are rapidly shifting from traditional chlorinated polyolefins (CPOs) to non-chlorinated alternatives. This transition is further accelerated by the "lightweighting" trend in the automotive sector, where non-chlorinated primers are essential for bonding paints to thermoplastic olefin (TPO) bumpers and exterior parts without hazardous pretreatments. Consequently, the convergence of regulatory pressure and performance requirements for hard-to-bond substrates is establishing a robust foundation for market expansion.

| Key Insights | Details |

|---|---|

| Non-Chlorinated Polyolefins Size (2026E) | US$ 4.1 Bn |

| Market Value Forecast (2033F) | US$ 6.2 Bn |

| Projected Growth CAGR (2026-2033) | 6.0% |

| Historical Market Growth (2020-2025) | 5.1% |

Market Dynamics

Market Growth Drivers

Expanding Automotive Applications and Lightweighting Initiatives

The automotive sector represents a primary growth driver for non-chlorinated polyolefins, as manufacturers increasingly adopt lightweight materials to enhance fuel efficiency and reduce vehicular emissions. Modern automotive design strategies emphasize the replacement of conventional materials, such as metals and rubber, with high-performance polymeric solutions. Non-chlorinated polyolefins serve as adhesion promoters in primers and basecoat systems for plastic components. A 10% reduction in vehicle weight can result in a 6%-8% improvement in fuel economy, prompting automotive original equipment manufacturers (OEMs), including Ford, General Motors, and Stellantis, to integrate advanced polyolefin formulations into both interior and exterior applications.

The growing production of electric vehicles (EVs) further accelerates this trend, as lightweight construction becomes critical to extending driving range without compromising safety or aesthetic appeal. Regulatory frameworks such as vehicle fuel economy standards and corporate average fuel economy (CAFE) requirements in North America have established binding targets that necessitate material innovation, making non-chlorinated polyolefins increasingly indispensable in bumpers, trims, dashboards, and door panels.

Rising Demand from Flexible Packaging and E-commerce Growth

The expansion of the e-commerce sector and the corresponding surge in flexible packaging demand create significant opportunities for non-chlorinated polyolefins, particularly in applications requiring adhesion and coating properties. Polyethylene and polypropylene films, which dominate flexible packaging for food, pharmaceuticals, and personal care products, require advanced adhesion promoters to ensure robust ink and coating bonding without compromising recyclability. Global e-commerce sales continue to accelerate, with retailers seeking cost-effective packaging solutions that simultaneously meet food safety standards and environmental sustainability objectives.

The paints and coatings market, valued at hundreds of billions globally, increasingly incorporates non-chlorinated polyolefin formulations to replace traditional chlorinated primers, driven by consumer awareness and brand commitment to reduced-VOC (volatile organic compound) products. Emerging markets in the Asia Pacific, particularly India and Southeast Asia, are experiencing rapid growth in organized retail and e-commerce infrastructure, creating sustained demand for premium packaging materials. The global shift toward lighter, more durable, and recyclable packaging solutions positions non-chlorinated polyolefins as essential components in industrial and consumer applications.

Market Restraints

High Manufacturing Costs and Production Complexity

Non-chlorinated polyolefin production involves more complex processing methods than traditional chlorinated alternatives, resulting in higher manufacturing costs that constrain market competitiveness. The synthesis of halogen-free polymeric structures requires specialized catalyst systems, precise temperature control, and multi-stage purification processes, all of which increase capital expenditure and operational expenses. This cost differential creates particular challenges in price-sensitive segments such as commodity coatings and general-purpose adhesives, where end-users may remain reluctant to transition from established chlorinated formulations despite environmental incentives.

Smaller and mid-sized converter companies operating in developing regions often lack the financial resources to invest in compatible production infrastructure, thereby limiting market adoption rates. Additionally, supply chain fragmentation and the limited number of qualified suppliers globally can lead to extended lead times and pricing volatility, particularly during periods of high demand or supply disruptions.

Substrate-Specific Compatibility Limitations and Alternative Solutions

Non-chlorinated polyolefins exhibit performance inconsistencies across substrate types, with limited universal applicability, which can limit market penetration in specialized applications. While these compounds exhibit excellent adhesion properties on low-energy surfaces such as polypropylene and polyethylene, their performance on high-energy substrates may require additional formulation modifications or surface pre-treatment, increasing overall processing complexity.

The emergence of alternative adhesion promotion technologies, including advanced silane-based primers and novel polymer chemistries, provides end-users with multiple options for achieving comparable performance at potentially lower costs. Established manufacturing workflows in mature industrial sectors continue to rely on proven chlorinated formulations, where retrofitting production lines to accommodate non-chlorinated alternatives represents both technical and financial challenges. This entrenched competitive landscape has slowed the transition rate in certain application sectors, particularly in legacy industrial coatings and specialty adhesive formulations.

Market Opportunities

Growing Flame Retardant Market Integration with Non-halogenated Formulations

The flame retardant market, which encompasses both halogenated and non-halogenated solutions, presents substantial opportunities for integrating non-chlorinated polyolefins, particularly as regulatory frameworks progressively eliminate halogenated flame retardants. Non-halogenated flame retardants, including phosphorus-based and mineral-based formulations, represent the fastest-growing segment in fire protection chemistry, with the global flame retardant market expected to expand substantially through 2033.

Applications in building and construction materials, electrical and electronics housings, and automotive components increasingly mandate halogen-free compliance, directly stimulating demand for non-chlorinated polyolefins as compatible base materials. The polyolefin segment led the flame retardant application market with over 25% market share, indicating substantial volume opportunities for specialty non-chlorinated formulations. Government investment in smart city infrastructure and energy-efficient building designs in Asia Pacific, Europe, and North America creates ongoing demand for fire-safe materials incorporating advanced adhesion promoters and coating technologies. Companies developing integrated flame-retardant polyolefin solutions stand to capture significant market value as regulatory mandates accelerate across geographies.

Circular Economy Initiatives and Recycled Polyolefin Integration

The global plastic waste crisis and commitment to circular economy principles have catalyzed substantial investment in polyolefin recycling technologies and infrastructure, creating opportunities for non-chlorinated polyolefin producers to develop formulations compatible with applications that use recycled content. Recent initiatives in India, particularly the Plastics Circularity Initiative launched by Re Sustainability and Sharrp Ventures, aim to produce high-quality recycled polymers for the FMCG and packaging sectors, with an expected annual production of 9,000 tonnes of superior recycled polymers.

Advanced molecular recycling facilities, exemplified by Eastman's commercial-scale operation with capacity to process 110,000 metric tons of polyester waste annually, demonstrate the technical feasibility of large-scale polymer transformation. Non-chlorinated polyolefin-based coating and adhesion systems facilitate the processing and application of recycled materials while maintaining performance characteristics required for demanding applications. The expansion of extended producer responsibility (EPR) schemes across Europe and emerging markets mandates manufacturer accountability for end-of-life material management, driving investment in circular-compatible material formulations. Companies pioneering non-chlorinated polyolefin solutions for recycled material streams stand to benefit from premium pricing and long-term supply agreements with sustainability-focused converters and brand-owning companies.

Category-wise Insights

Polymer Type Analysis

Polypropylene (PP) serves as the leading segment within the polymer type category, accounting for a dominant share of approximately 60% of the total market. This dominance is attributed to the extensive use of modified polypropylene as the primary feedstock for manufacturing adhesion promoters. Polypropylene-based non-chlorinated polyolefins offer the best chemical affinity for bonding to PP and TPO substrates, which are the most common plastics used in automotive bumpers and instrument panels. Their molecular structure can be readily modified with functional groups such as maleic anhydride to create robust chemical bridges between the nonpolar substrate and the polar coatings. The material's balance of cost-effectiveness, chemical resistance, and mechanical flexibility makes it the preferred choice for formulators seeking to replace chlorinated variants without sacrificing performance in demanding exterior applications.

Application Analysis

Paints & Coatings represents the leading application segment, holding a market share of roughly 45%. The segment's leadership is underpinned by the critical role Non-Chlorinated Polyolefins play as primers and tie-layers in the finishing of plastic components. In the automotive OEM and refinish sectors, these materials are indispensable for ensuring that basecoats and clearcoats adhere to plastic bumpers, ensuring the paint does not peel or flake under stress or weathering. The shift towards monochromatic vehicle designs, where plastic parts match the metal body color, has intensified the need for reliable adhesion promoters. Furthermore, the rising popularity of soft-touch coatings in automotive interiors and consumer electronics handles relies heavily on these primers to bond polyurethane or acrylic coatings to the underlying polyolefin structure, cementing this segment's market supremacy.

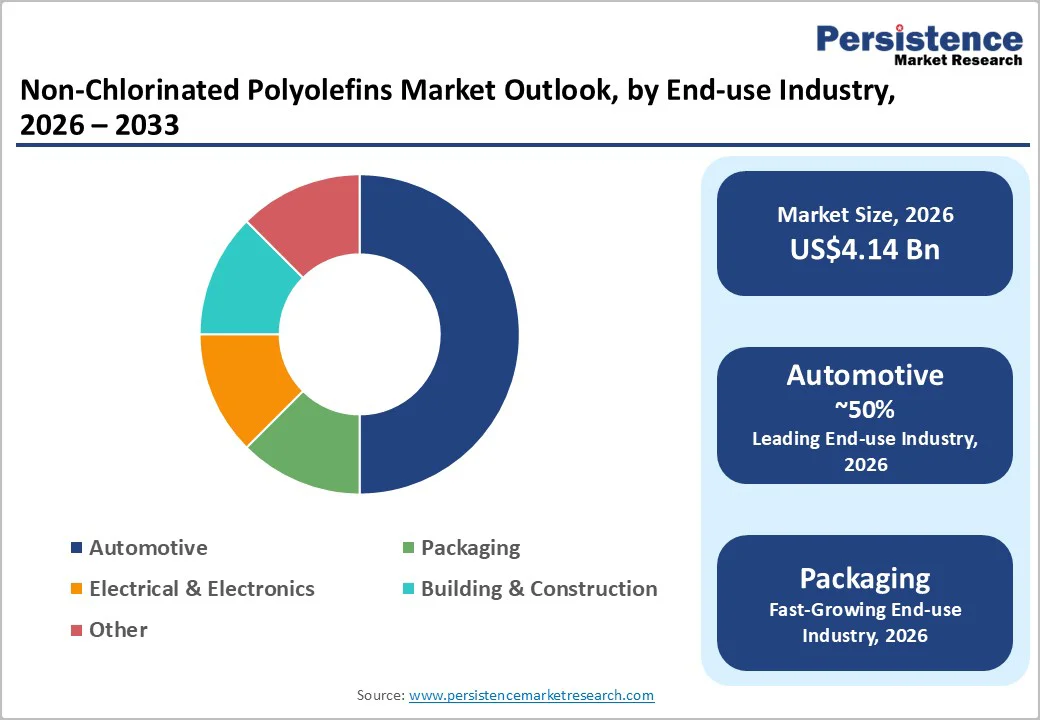

End-use Industry Analysis

Automotive is the undisputed leader in the end-use industry category, commanding over 50% of the market share. This hegemony is driven by the massive volume of polyolefin plastics employed in modern vehicle manufacturing to achieve weight reduction and fuel economy targets. Virtually every exterior plastic component, from bumper fascias to rocker panels and side moldings, requires surface treatment to accept paint or adhesives. As global automakers like Toyota, Volkswagen, and GM enforce stricter environmental standards for their supply chains, the transition to non-chlorinated primers has accelerated. The segment is further bolstered by the increasing use of adhesives for structural bonding of plastic tailgates and front-end modules, where Non-Chlorinated Polyolefins act as the enabling technology for joining dissimilar materials, ensuring structural integrity and crashworthiness.

Regional Insights

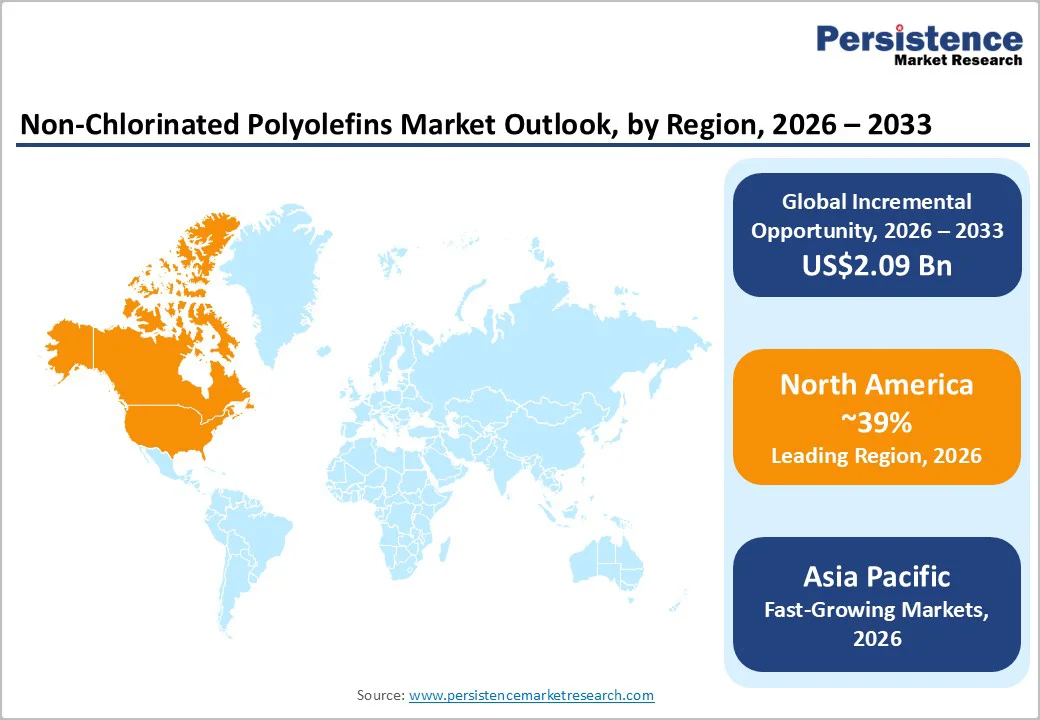

North America Non-Chlorinated Polyolefins Trends

North America currently dominates the global market, with 39% of the market share, driven by a mature automotive manufacturing ecosystem and stringent environmental enforcement. The United States leads in demand, with major OEMs investing heavily in lightweight materials to meet Corporate Average Fuel Economy (CAFE) standards. The region is characterized by a high adoption rate of advanced materials technologies, with companies such as Eastman Chemical Company and Dow Inc. pioneering the development of next-generation halogen-free adhesion promoters.

Furthermore, a robust Paints and Coatings Market infrastructure supports the rapid commercialization of water-borne non-chlorinated dispersions. Regulatory pressure from the EPA regarding hazardous air pollutants continues to be a catalyst, forcing regional formulators to phase out legacy chlorinated systems faster than in other parts of the world.

Europe Non-Chlorinated Polyolefins Trends

Europe represents a highly influential market characterized by rigorous sustainability mandates and a focus on circular economy principles. Countries such as Germany, France, and Italy are at the forefront of this shift, driven by the European Union's REACH regulations which severely restrict the use of chlorinated chemicals. This regulatory environment has spurred significant innovation among regional players such as BASF SE and LyondellBasell Industries N.V., which are developing bio-based and non-chlorinated alternatives to align with the growing "Green Deal" initiatives.

The region's strong luxury automotive sector also demands high-performance coating solutions that offer flawless aesthetics and durability, further propelling the uptake of premium non-chlorinated adhesion promoters. Additionally, the region is seeing increasing application in the packaging sector, where sustainable, chlorine-free inks are becoming standard requirements for recyclable films.

Asia Pacific Non-Chlorinated Polyolefins Trends

Asia Pacific is recognized as the fastest-growing region, driven by rapid industrialization and the expansion of automotive production hubs in China, India, and Japan. China, the world's largest automotive market, is experiencing a surge in demand for Non-Chlorinated Polyolefins as domestic manufacturers upgrade their coating lines to meet international quality and environmental standards. The region's growth is also supported by a booming packaging industry, where the demand for high-quality printing on flexible polyolefin films is rising.

Japanese companies such as Mitsui Chemicals Inc. and Sumitomo Chemical Co., Ltd. are key contributors to technology, exporting high-grade functionalized polyolefins across the region. As environmental regulations in China and India tighten to combat pollution, the shift from conventional chlorinated primers to eco-friendly non-chlorinated alternatives is expected to accelerate, offering immense volume growth potential.

Competitive Landscape

Market Structure Analysis

The global Non-Chlorinated Polyolefins market is moderately consolidated, with a few multinational chemical giants controlling the majority of the production capacity for high-performance grades. Key players compete primarily on product differentiation, focusing on compatibility with diverse substrates and solubility in eco-friendly solvents. The market structure is defined by significant barriers to entry, including high R&D costs and the need for specialized polymerization technologies to graft functional groups onto polyolefin backbones. Leading companies are adopting strategies of vertical integration, securing their supply of base resins while developing proprietary grafting processes. There is also a notable trend towards collaboration with coating formulators to develop tailored solutions for specific automotive OEMs. Innovation is currently centered on lowering the baking temperature of these primers to save energy and enabling adhesion to recycled plastics, reflecting the broader industry push towards sustainability and circularity.

Key Market Developments

- December 2025: Mitsui Chemicals, Idemitsu Kosan, and Sumitomo Chemical concluded definitive agreements to integrate Sumitomo Chemical's polypropylene and linear low-density polyethylene businesses into Prime Polymer, positioning the combined entity to achieve annual cost savings exceeding 8 billion yen while strengthening competitive positioning against imported polyolefins in the Japanese market.

- July 2023: Eastman Chemical Company collaborated with a major automotive coating supplier to introduce a new water-borne adhesion promoter system based on its non-chlorinated technology, aimed at reducing VOC emissions in automotive paint shops in Europe.

- March 2024: Dow Inc. commissioned a new production unit for its specialty polyolefin elastomers, which serve as key base materials for non-chlorinated adhesion promoters, ensuring a stable supply for the growing Asian market.

Top Companies in Non-Chlorinated Polyolefins

Eastman Chemical Company (USA) is a global leader in adhesion promoter technology, offering one of the broadest portfolios of non-chlorinated polyolefins under its Advantis and Eastman brands. The company leverages its deep expertise in chemical modification to provide solutions that bond to difficult substrates like TPO and polypropylene. Eastman is aggressively pivoting towards sustainable solutions, focusing on water-dispersible and halogen-free products that help customers meet strict regulatory compliance.

Mitsui Chemicals Inc. (Japan) is renowned for its ADMER and UNISTOLE product lines, which are industry benchmarks for modified polyolefins. The company’s non-chlorinated adhesion promoters are widely used in automotive, packaging, and industrial applications. Mitsui distinguishes itself through advanced polymerization technologies that allow for precise control over the polymer architecture, resulting in superior adhesion performance and chemical resistance, particularly in the demanding Asian automotive sector.

Dow Inc. (USA) commands a significant position in the market through its vast capabilities in polyolefin material science. While a major supplier of base resins, Dow also produces functionalized polymers and dispersions such as AFFINITY and PRIMACOR that serve as critical ingredients in non-chlorinated primer formulations. The company’s strategy focuses on large-scale efficiency and the development of collaborative solutions with downstream coating manufacturers to address sustainability challenges across the global value chain.

Key Market Highlights

- Leading Region: North America leads the global market, accounting for a significant revenue share due to strict environmental regulations and high adoption of advanced automotive coating technologies by major OEMs in the United States.

- Fastest Growing Region: Asia Pacific is projected to witness the highest growth rate, driven by booming automotive production in China and India and increasing regulatory pressure to replace chlorinated chemicals in industrial applications.

- Dominant Segment: Polypropylene (PP) remains the dominant polymer type segment, serving as the primary feedstock for adhesion promoters due to its chemical compatibility with automotive bumpers and superior mechanical properties.

- Fastest Growing Segment: Water-borne Adhesion Promoters within the application category are expanding rapidly as industries shift away from solvent-based systems to comply with low-VOC regulations in packaging and automotive sectors.

- Key Market Opportunity: The development of Bio-based Non-Chlorinated Polyolefins offers a lucrative opportunity, allowing manufacturers to cater to the rising demand for renewable materials in the consumer electronics and sustainable packaging markets.

Companies Covered in Non-Chlorinated Polyolefins Market

- ExxonMobil Corporation

- Dow Inc.

- LyondellBasell Industries N.V.

- BASF SE

- SABIC

- Mitsui Chemicals Inc.

- LG Chem Ltd.

- Eastman Chemical Company

- INEOS Group Holding S.A.

- Formosa Plastic Corporation

- Sumitomo Chemical Co., Ltd.

Frequently Asked Questions

The global market is projected to reach a value of US$ 6.2 Bn by 2033, growing at a CAGR of 6.0% from 2026 to 2033, driven by increasing demand for sustainable adhesion promoters.

The primary drivers include strict environmental regulations limiting VOC emissions, the shift towards halogen-free materials, and the increasing use of lightweight plastics like TPO in the automotive industry that require specialized adhesion promoters.

Polypropylene is the leading polymer type segment, accounting for the majority of the market share. It is the preferred base material for manufacturing adhesion promoters due to its excellent compatibility with automotive plastic substrates.

North America currently dominates the market, supported by a technologically advanced automotive sector and stringent EPA regulations that encourage the adoption of eco-friendly, non-chlorinated coating systems.

A significant opportunity lies in developing water-borne non-chlorinated dispersions. This caters to the growing trend of sustainable, water-based coatings and inks in the packaging and textile industries, offering a compliant alternative to solvent-based systems.

Key players in the market include Eastman Chemical Company, Mitsui Chemicals Inc., Dow Inc., Toyobo Co., Ltd., and LyondellBasell Industries N.V., who are leading the development of high-performance non-chlorinated adhesion solutions.