- Pharmaceuticals

- Nocturia Market

Nocturia Market Size, Trends, Share, Growth, and Regional Forecast, 2025 to 2032

Nocturia Market by Drug Type (Anticholinergic Drugs, Desmopressin, Antibiotics, Antispasmodic, and Others), Indication (Mixed Nocturia, Low Nocturnal Bladder Capacity, Nocturnal Polyuria, and Global Polyuria), Distribution Channel, and Regional Analysis from 2025 to 2032

Nocturia Market Share and Trends Analysis

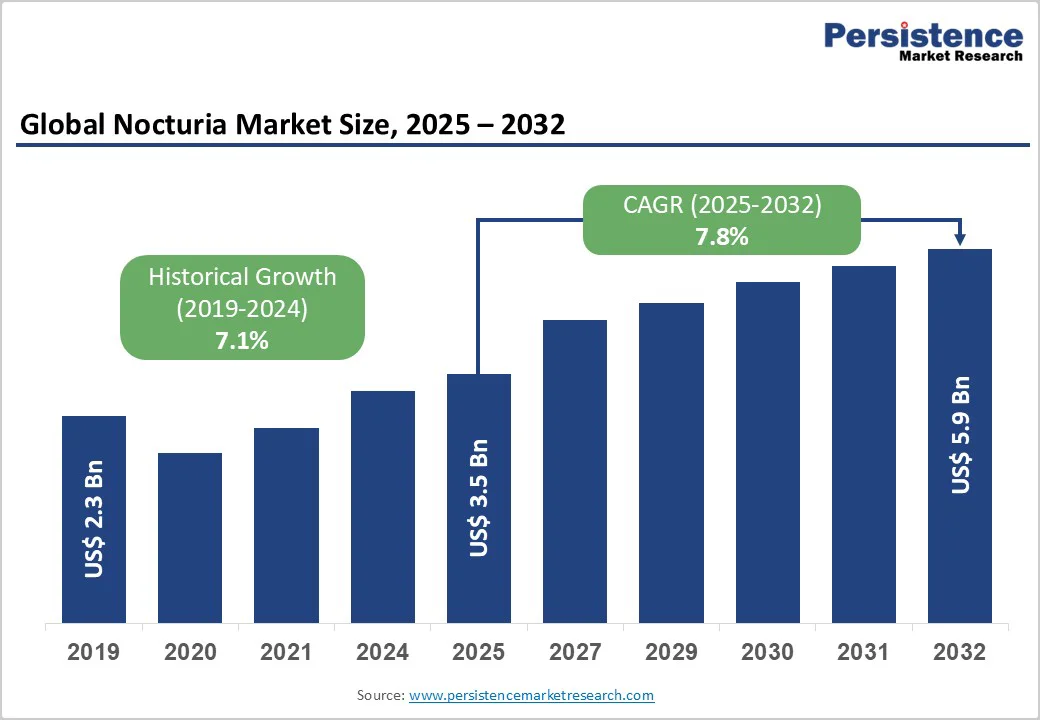

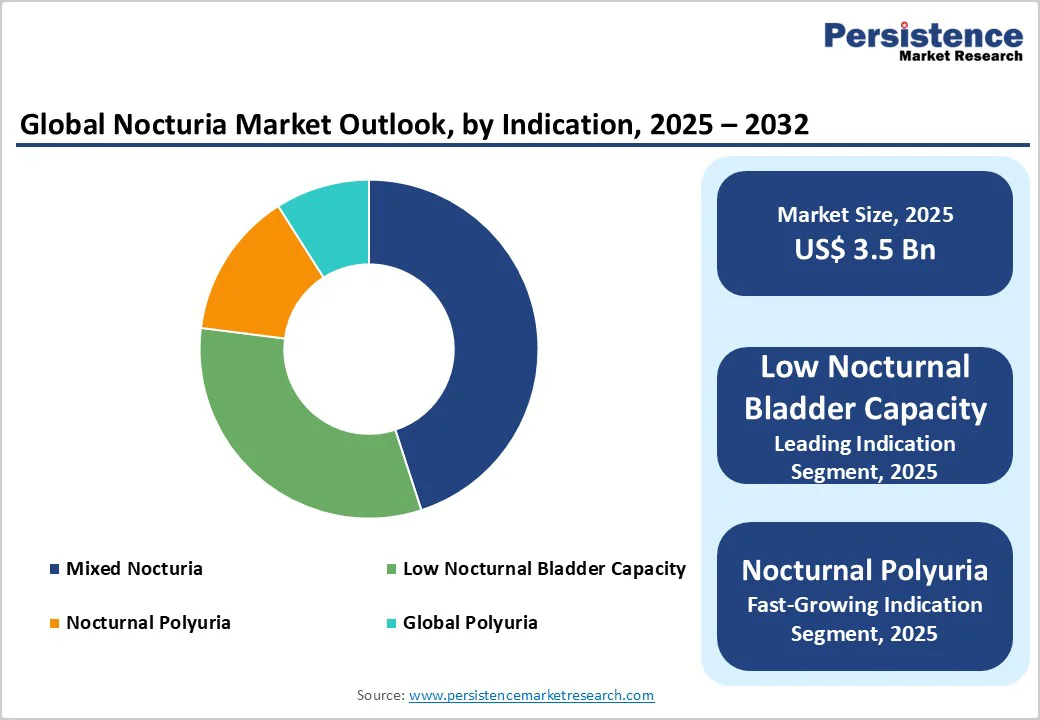

The global nocturia market size is likely to achieve US$ 3.5 billion in 2025 and is projected to reach US$ 5.9 billion at a CAGR of 7.8% during the forecast period from 2025 to 2032.

The primary objective of the report is to offer insights into developments in the Nocturia market that are significantly transforming global businesses and enterprises. Rise in prevalence of cancer, diabetes, and cardiovascular disease globally are important factors that are responsible for the growth in revenue of the nocturia market. A significant percentage of population is affected by diseases.

Greater access to manufacturing infrastructure, increased access to Contract Manufacturing Organizations (CMOs) and advancement in drug delivery systems are the factors expected to drive revenue growth of the nocturia market globally. Furthermore, high operational costs and discontinuation of product manufacturing due to competition from low-cost manufacturers are hampering growth in this market.

Key Industry Highlights:

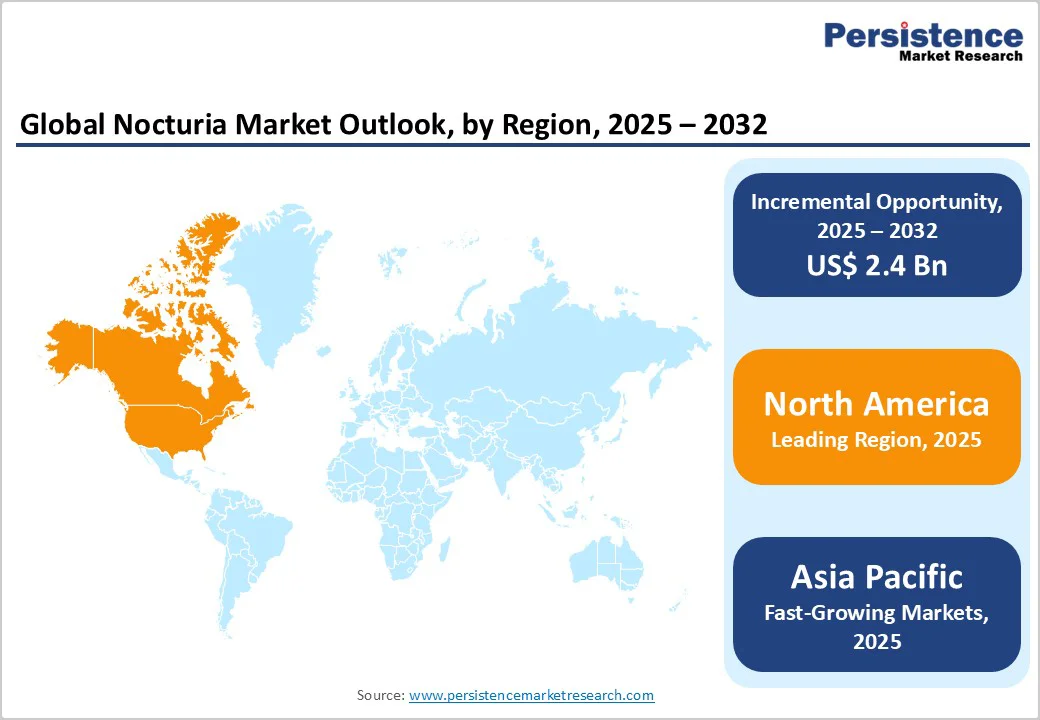

- Leading Region: North America leads the market, driven by advanced healthcare systems, innovation pipelines, and broad insurance access supporting both diagnosis and therapy.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region owing to rising awareness, investment in digital health, and a focus on addressing the needs of the aging population.

- Dominant Segment: Desmopressin remains the dominant drug type supported by robust clinical evidence and regulatory success in managing nocturnal polyuria.

- Fastest Growing Segment: Anticholinergic drugs, driven by increasing diagnosis of overactive bladder-related nocturia and broader clinical use in elderly populations.

| Global Market Attributes | Key Insights |

|---|---|

| Nocturia Market Size (2025E) | US$ 3.5 Bn |

| Market Value Forecast (2032F) | US$ 5.9 Bn |

| Projected Growth (CAGR 2025 to 2032) | 7.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 7.1% |

Market Dynamics

Driver - Aging Population and Disease Prevalence Drives Global Demand for Advanced Nocturia Solutions

The global population is aging at an unprecedented rate, serving as a key catalyst for the expansion of the nocturia market. According to estimates from the World Health Organization, the number of people aged 60 years and above is projected to double, reaching nearly 2.1 billion by 2050.

This demographic transition is directly associated with a rising prevalence of nocturia, as the frequency of nighttime urination increases significantly with advancing age. Epidemiological studies reveal that approximately 56% of community-dwelling older men in Korea experience nocturia, while nearly half of men aged 70 to 79 years report two or more nightly voids.

The condition is further compounded by age-related comorbidities such as benign prostatic hyperplasia (BPH), overactive bladder (OAB), and diabetes mellitus, all of which contribute to the onset and severity of nocturnal symptoms. These interconnected health factors are intensifying the need for effective diagnostic tools, pharmacological therapies, and long-term disease management strategies.

As the elderly population continues to expand across both developed and emerging economies, the burden of nocturia is expected to rise proportionately, creating sustained demand for innovative treatment options and supporting the overall growth trajectory of the nocturia therapeutics market.

Restraints - Drug Side-Effect Profile and Compliance Issues

Although pharmacological innovations have improved nocturia management, patient adherence continues to pose a major challenge due to adverse drug reactions. Medications such as desmopressin, while effective in reducing nocturnal urine output, carry a risk of hyponatremia, particularly in elderly patients and those with renal impairment.

Similarly, anticholinergic drugs, commonly prescribed for bladder overactivity, often cause side effects like dry mouth, constipation, and blurred vision, leading many patients to discontinue therapy prematurely. These tolerability concerns directly impact long-term treatment success and limit the overall effectiveness of pharmacotherapy.

Regulatory agencies, including the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA), have implemented stringent safety protocols and monitoring guidelines for electrolyte balance and renal function. Such precautions, though necessary for patient safety, can also slow down prescription rates and restrict broader market penetration for certain nocturia medications, highlighting the ongoing balance between efficacy and tolerability.

Opportunity - Growing Adoption of Digital Health Technologies and Artificial Intelligence

The growing adoption of digital health technologies and artificial intelligence presents a significant opportunity for advancing nocturia management. Smart diagnostic tools such as digital voiding diaries, wearable bladder sensors, and connected health applications are transforming how symptoms are tracked and interpreted.

These technologies allow for continuous, real-time monitoring of urinary patterns, sleep quality, and fluid intake, providing physicians with accurate data for diagnosis and treatment optimization. AI-driven analytics can identify patient-specific trends, helping tailor therapies based on individual physiology and lifestyle factors. This personalized approach not only improves treatment adherence but also enhances clinical outcomes.

Furthermore, the integration of telemedicine platforms facilitates remote consultations, ensuring greater access to care for elderly and mobility-restricted patients. Regulatory support for digital healthcare innovation is encouraging investment in software-driven diagnostics and mobile health tools.

As these technologies become mainstream, they are expected to significantly improve disease management efficiency, reduce healthcare costs, and strengthen patient engagement in nocturia care.

Category-wise Analysis

By Drug Type, Desmopressin Drugs Dominate the Market, Anticholinergic Drugs Emerges as the Fastest-Growing Category

In 2024, Desmopressin emerged as the leading drug type in the global nocturia market, commanding approximately 34% of total revenue. Its dominance is supported by proven clinical efficacy in decreasing nighttime urine output and improving sleep quality, particularly among patients with nocturnal polyuria and low nocturnal bladder capacity.

The drug’s wide therapeutic application across adult and pediatric groups, coupled with strong physician familiarity and multiple dosage formulations such as orally disintegrating tablets (ODT) and nasal sprays, reinforce its market leadership. Ongoing regulatory approvals and label expansions continue to strengthen Desmopressin’s competitive edge.

Anticholinergic drugs represent the fastest-growing segment, driven by increasing diagnosis of overactive bladder-related nocturia and broader clinical use in elderly populations. These agents such as oxybutynin, tolterodine, and solifenacin are gaining traction due to their ability to improve bladder storage capacity and reduce urinary urgency. The combination of Desmopressin’s established dominance and the rapid growth of anticholinergics underscore a diversified therapeutic landscape within the nocturia drug market.

By Indication, Low Nocturnal Bladder Capacity is Leading

The Low Nocturnal Bladder Capacity (LNBC) segment accounted for the largest market share of approximately 45% in 2024, establishing itself as the leading indication within the global nocturia landscape.

This dominance stems primarily from the rising prevalence of bladder dysfunctions, particularly among aging populations, where reduced bladder compliance and detrusor overactivity are common. Growing clinical focus on identifying and managing lower urinary tract symptoms (LUTS) has led to earlier diagnosis and more targeted therapeutic approaches for LNBC-related nocturia.

Advancements in urodynamic assessment tools and diagnostic imaging have enabled precise evaluation of bladder storage capacity, promoting the adoption of pharmacological treatments such as antimuscarinic agents, β3-adrenoceptor agonists, and alpha-blockers.

Additionally, increased awareness among healthcare professionals regarding behavioral and combination therapies has further enhanced patient outcomes. The segment continues to benefit from ongoing research aimed at understanding bladder physiology and improving treatment personalization, solidifying its position as the central driver of growth in the nocturia therapeutics market.

Region-wise Insights

North America Nocturia Market Trends

North America continues to dominate the global nocturia market, driven by a combination of high disease awareness, advanced healthcare infrastructure, and significant investment in research and development. The U.S. leads the region with a strong presence of key pharmaceutical players focusing on innovative formulations such as Desmopressin ODT and other vasopressin analogues designed for nocturnal polyuria management.

Supportive regulatory frameworks by the U.S. Food and Drug Administration (FDA), including priority review and accelerated approval programs, have facilitated faster product launches and market expansion. In addition, high healthcare spending, insurance coverage for prescription drugs, and a well-established distribution network enhance patient access to treatment.

Clinical guidelines in the U.S. increasingly emphasize screening and early management of nocturia, particularly among elderly and high-risk groups. Canada contributes through growing urology-focused clinical research and technology integration.

Collaborations between academic institutions and pharmaceutical companies are advancing personalized medicine and digital health approaches, including mobile-based monitoring of urinary symptoms. The increasing incorporation of artificial intelligence for diagnostic precision and patient adherence programs further strengthens the region’s leadership position, ensuring steady growth and innovation across the nocturia therapeutic landscape in North America.

Asia and Pacific Nocturia Market Trends

The Asia Pacific region represents the fastest-growing market for nocturia treatments, supported by demographic shifts, lifestyle changes, and healthcare modernization across key countries such as China, Japan, India, and South Korea.

The rapidly aging population and rising incidence of chronic urological conditions, including overactive bladder and benign prostatic hyperplasia, are creating strong therapeutic demand. Japan remains a key contributor, given its advanced healthcare systems and higher prevalence of nocturia among elderly individuals.

In China, government-led initiatives under the “Healthy China 2030” framework are improving awareness, diagnostics, and access to urological care. India is witnessing growing healthcare investment and expansion of urology clinics in both urban and semi-urban settings. Pharmaceutical manufacturers are forming local partnerships to enhance production and distribution, while also engaging in educational campaigns to reduce underdiagnosis.

Increased reimbursement for urological drugs in several Asia Pacific markets has further encouraged treatment uptake. The adoption of telemedicine, digital platforms, and AI-based diagnostic solutions is also transforming patient management.

Continuous R&D efforts, combined with supportive policy frameworks and international collaborations, are expected to make Asia Pacific a major growth hub for nocturia therapies, attracting both global and regional players over the forecast period.

Market Competitive Landscape

The global nocturia market is highly competitive, featuring a mix of multinational and specialty pharmaceutical firms focusing on urinary and renal disorders. Key players such as Allergan, Ferring Pharmaceuticals, Teva, and Glenmark emphasize portfolio expansion through innovative therapies and lifecycle management of urological drugs.

Companies are adopting both short-term strategies like product launches and partnerships, and long-term goals including R&D investment in desmopressin analogues and combination therapies to strengthen their position in the growing nocturia treatment landscape.

Key Industry Developments:

- In September 2025, Cipla introduced Huena, marking India’s first non-antibiotic medication developed to combat urinary tract infections (UTIs).

- In May 2024, Sumitomo Pharma announced that the U.S. FDA had accepted its supplemental New Drug Application (sNDA) for Vibegron, aimed at treating men with overactive bladder (OAB) symptoms who are already receiving pharmacological therapy for benign prostatic hyperplasia (BPH).

Companies Covered in Nocturia Market

- Allergan, Inc.

- Urigen Pharmaceuticals

- Vantia Therapeutics

- Ferring Pharmaceuticals

- Glenmark Pharmaceuticals Inc.

- Teva Pharmaceutical Industries Ltd.

- AA Pharma Inc.

- Avadel Pharmaceuticals plc

- Elder Pharmaceuticals Ltd

- Fourrts India Laboratories Pvt Ltd

- Others

Frequently Asked Questions

The global market is projected to be valued at US$ 3.5 Bn in 2025.

The growing elderly population, combined with rising awareness of urological health and new drug approvals, is the major demand driver worldwide.

The global market is poised to witness a CAGR of 7.8% between 2025 and 2032.

Digital health integration for personalized nocturia management and remote monitoring platforms will be the primary growth opportunity.

Leading players include Allergan, Inc., Urigen Pharmaceuticals, Ferring Pharmaceuticals, Glenmark Pharmaceuticals Inc., Teva Pharmaceutical Industries Ltd., are some of the major players operating in the market.