- Pharmaceuticals

- Uncomplicated Urinary Tract Infection (UTI) Treatment Market

Uncomplicated Urinary Tract Infection (UTI) Treatment Market Size, Share, and Growth Forecast 2026 - 2033

Uncomplicated Urinary Tract Infection (UTI) Treatment Market by Drug Class (Gepotidacin, Probenecid, Sulfonamide, Tetracycline, Nitrofuran), by Route of Administration (Oral, Injectable), by Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), by Regional Analysis, 2026 - 2033

Uncomplicated Urinary Tract Infection (UTI) Treatment Market Share and Trends Analysis

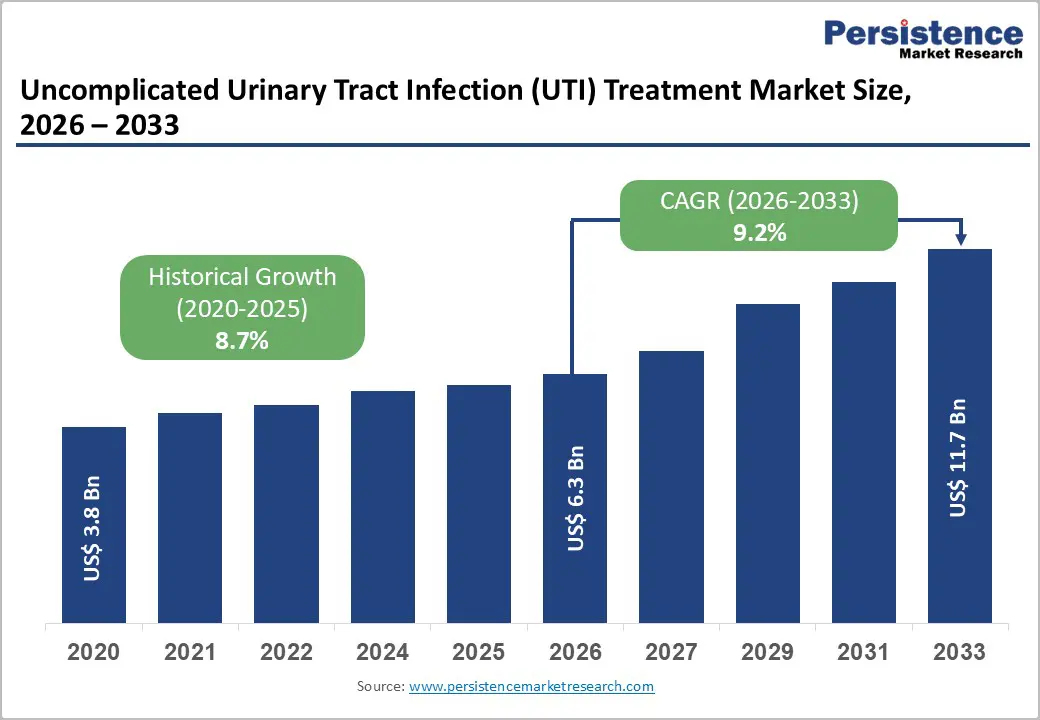

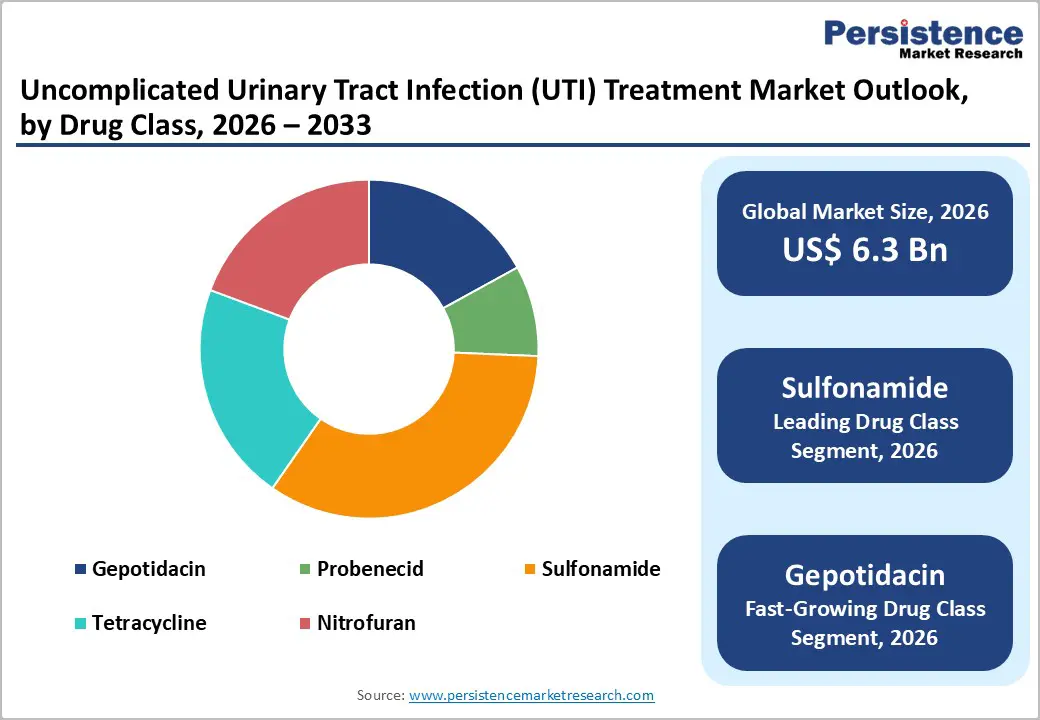

The global uncomplicated urinary tract infection (UTI) treatment market size is expected to be valued at US$ 6.3 billion in 2026 and projected to reach US$ 11.7 billion by 2033, growing at a CAGR of 9.2% between 2026 and 2033.

Strong growth is underpinned by the very high lifetime incidence of uncomplicated UTI in women, rising antimicrobial resistance that necessitates newer agents, and expanding access to outpatient and e-pharmacy channels for oral antibiotics. UTIs are among the most common community infections: between 40-60% of adult women will experience at least one UTI in their lifetime, and around 10% report an episode every year, generating substantial recurring demand for short-course oral therapies and driving sustained prescription volumes globally.

Key Industry Highlights:

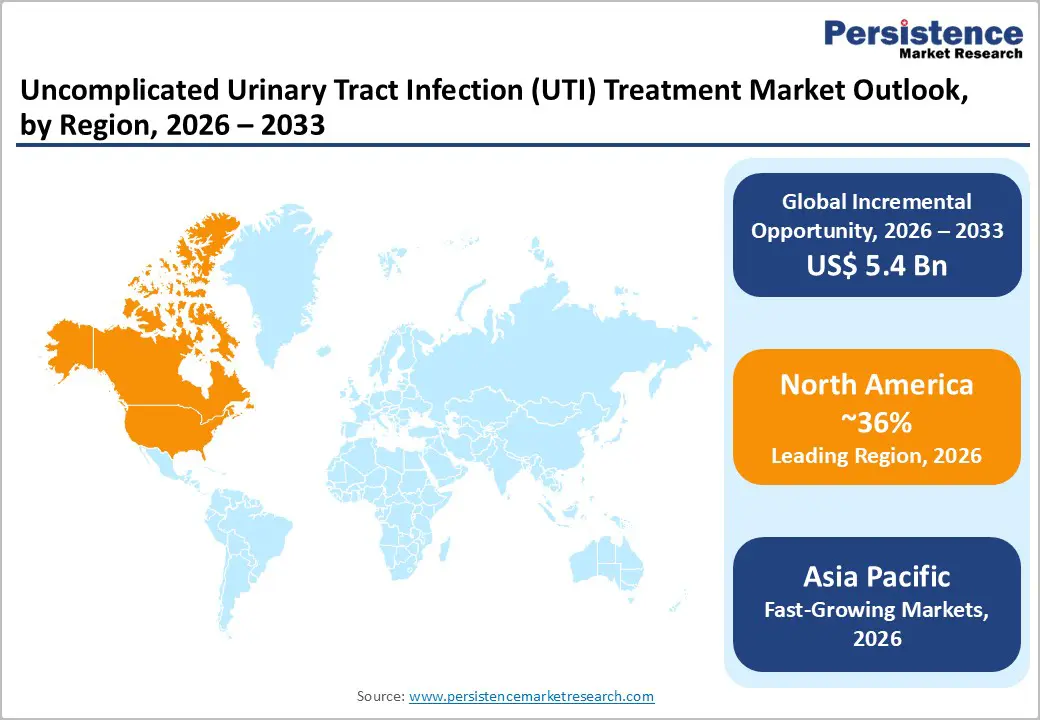

- Leading region: North America remains the largest uncomplicated UTI treatment market, supported by high diagnosis and treatment rates, robust insurance coverage, strong antimicrobial stewardship frameworks, and rapid uptake of novel agents and digital health-enabled prescribing and dispensing pathways.

- Fastest-growing region: Asia Pacific is poised for the fastest growth, driven by expanding primary-care access, large and aging populations, rising awareness of UTI symptoms, and investments to address high levels of antimicrobial resistance

- through more appropriate empirical therapy and surveillance.

- Dominant segment: The Sulfonamide drug class, particularly trimethoprim-sulfamethoxazole, holds an estimated 34% share due to long-standing inclusion in guidelines as a first-line oral therapy when local resistance thresholds permit, strong familiarity among prescribers, and widespread generic availability.

- Fastest growing segment: Gepotidacin, a first-in-class oral antibiotic from GlaxoSmithKline plc, is expected to be the fastest-growing drug class segment once approved, leveraging phase III data showing non-inferiority or superiority to nitrofurantoin and addressing unmet needs in resistant or recurrent uncomplicated UTI.

- Key market opportunity: Companies that pair innovative oral agents and optimized regimens with telehealth triage, antimicrobial stewardship tools, and integrated online pharmacy distribution can capture incremental demand from recurrent uncomplicated UTI patients while aligning with global efforts to combat antimicrobial resistance.

| Key Insights | Details |

|---|---|

| Uncomplicated UTI Treatment Market Size (2026E) | US$ 6.3 billion |

| Market Value Forecast (2033F) | US$ 11.7 billion |

| Projected Growth CAGR (2026 - 2033) | 9.2% |

| Historical Market Growth (2020 - 2025) | 8.7% |

Market Dynamics

Drivers - High incidence and recurrence of uncomplicated UTI in women and older adults

A primary growth driver is the very high incidence and recurrence of uncomplicated UTI, particularly among women of reproductive age and older adults. Narrative reviews and clinical resources report that 50-60% of adult women will experience at least one UTI in their lifetime, with an annual incidence around 10% and recurrence within six months in roughly 25-30% of cases. Population-based studies in primary care settings in Europe similarly highlight high community incidence and frequent help-seeking for dysuria and lower urinary symptoms, confirming a large, recurrent treatment pool. As populations age and comorbidities such as diabetes increase, the number of patients at risk of recurrent uncomplicated cystitis continues to rise, sustaining prescription volumes for established oral antibiotics and creating headroom for newer agents targeting patients who have failed first-line therapies.

Guideline-backed preference for oral first-line antibiotics in uncomplicated UTI

Another powerful driver is the continued guideline endorsement of oral antibiotics such as nitrofurantoin, trimethoprim-sulfamethoxazole and fosfomycin as first-line treatments for uncomplicated cystitis. The Infectious Diseases Society of America (IDSA) recommends nitrofurantoin 100 mg twice daily for 5 days, or a 3-day course of trimethoprim-sulfamethoxazole when local resistance to Escherichia coli is below 20%, while reserving fluoroquinolones to limit collateral damage. Real-world analyses of over 57,000 episodes of uncomplicated UTI show that first-line agents achieve lower revisit and complication rates compared with fluoroquinolones or beta-lactams, reinforcing their frontline role. Evidence from randomized trials and Cochrane reviews also shows that many patients, including children and those with more severe presentations, can be effectively managed with oral rather than intravenous antibiotics, bolstering demand for oral formulations.

Restraints - Rise in antimicrobial resistance in uropathogenic bacteria

The rapid rise of antimicrobial resistance (AMR) in uropathogenic E. coli and other Gram-negative pathogens poses a structural restraint on the uncomplicated UTI treatment market. Surveillance studies show resistance of uropathogenic E. coli to trimethoprim-sulfamethoxazole ranging from 14.6% to 60% across European countries, while resistance to fluoroquinolones often exceeds 50% in many developing regions. The World Health Organization (WHO) estimates that in 2023, about 1 in 6 laboratory-confirmed bacterial infections causing common community diseases, including UTIs, were resistant to key antibiotics, with resistance particularly high in South-East Asia and Eastern Mediterranean regions. Rising resistance undermines the effectiveness of staple drug classes such as sulfonamides and tetracyclines, complicates empirical therapy, and can force shifts to broader-spectrum or more expensive agents, increasing treatment costs and constraining predictable volume growth for older molecules.

Stewardship pressures and restrictions on inappropriate antibiotic use

Another restraint comes from antimicrobial stewardship initiatives and payer policies aimed at curbing unnecessary antibiotic prescriptions for self-limiting urinary symptoms and asymptomatic bacteriuria. Clinical guidelines emphasize that a proportion of uncomplicated UTIs may resolve spontaneously, around 20% of healthy non-pregnant women improve without antibiotics and strongly discourage treatment of asymptomatic bacteriuria outside specific groups such as pregnant women or patients undergoing urological procedures. Stewardship programs in primary care encourage delayed prescribing, narrow-spectrum choices, and shorter durations, while national and regional campaigns aim to reduce antibiotic use overall in human health. These efforts, while essential to preserving drug effectiveness, can temper growth in total prescription volumes for uncomplicated UTI, particularly in high-income markets with mature stewardship frameworks.

Opportunity - Launch of novel agents such as gepotidacin for resistant uncomplicated UTI

A major opportunity lies in the emergence of new oral agents, particularly gepotidacin, an investigational first-in-class triazaacenaphthylene antibiotic being developed by GlaxoSmithKline plc (GSK) for uncomplicated UTI. The pivotal EAGLE-2 and EAGLE-3 phase III trials enrolling more than 3,000 women demonstrated that oral gepotidacin was non-inferior and, in one trial, statistically superior to nitrofurantoin for therapeutic success, defined as combined clinical resolution and microbiological eradication. Across the trials, 94% of patients receiving gepotidacin did not require additional antibiotics during follow-up, with a safety profile consistent with earlier studies. If approved, gepotidacin would be the first new class of oral antibiotic for uncomplicated UTI in over 20 years, offering a differentiated option for patients at high risk of resistance or recurrence and creating a premium sub-segment within the market.

Category-wise Analysis

Drug Class Insights

Within drug classes, Sulfonamide combinations, most notably trimethoprim-sulfamethoxazole, are estimated to account for about 34% of the uncomplicated UTI treatment market in 2025, making them the leading segment. Historically, trimethoprim-sulfamethoxazole has been the standard empiric therapy for uncomplicated cystitis, supported by large randomized trials showing efficacy comparable to fluoroquinolones over three-day regimens. Even as resistance has risen, sulfonamides remain widely used where local resistance levels are acceptable, because they are orally administered, inexpensive, and well integrated into primary care prescribing habits. Clinical guidelines continue to recommend trimethoprim-sulfamethoxazole as a first-line option when E. coli resistance rates are below 20%, ensuring continued demand, especially in regions with structured surveillance and stewardship programs that enable targeted use.

Distribution Channel Insights

Among distribution channels, Retail Pharmacies are expected to be the leading segment, with an estimated share of around 58% in 2025. Uncomplicated UTIs are predominantly managed in outpatient settings by general practitioners, gynecologists, and urgent-care physicians, who prescribe short-course oral antibiotics, typically filled at community pharmacies. Retail pharmacies provide broad geographic coverage, extended opening hours, and access to over-the-counter adjuncts such as urinary alkalinizers and analgesics, making them the default point of care for most non-hospitalized patients. At the same time, the rapid expansion of online pharmacies-a global market already nearing US$ 100 billion in 2024 and expected to more than double over the next decade- supports a growing but still smaller share for e-pharmacy channels, particularly in digitally mature markets. Hospital pharmacies remain important for complicated UTIs and inpatient transitions, but account for a minority of antibiotic volumes for uncomplicated UTIs.

Regional Insights

North America Uncomplicated UTI Treatment Market Trends and Insights

North America continues to be the leading region in the uncomplicated UTI treatment market due to its well-established healthcare infrastructure, high healthcare spending, and strong disease awareness among patients and clinicians. The United States accounts for a substantial share of the regional market, with frequent outpatient cases of UTIs driving demand for effective antibiotic therapies and newer treatment options. Broad adoption of modern diagnostic tools, telehealth services, and antibiotic stewardship programs supports timely diagnosis and optimal prescribing practices, which further bolsters market growth. Canada also contributes through universal healthcare access and preventive care initiatives that promote early treatment. North America’s leadership is reinforced by extensive research and development activities focused on novel therapeutics and improved treatment protocols, including recent approvals of next-generation antibiotics. Retail and hospital pharmacies remain key distribution channels, while digital platforms and e-pharmacy growth improve patient access. Overall, advanced care pathways, ongoing innovation, and robust regulatory support are central to North America’s dominance in the uncomplicated UTI treatment market.

Asia Pacific Uncomplicated UTI Treatment Market Trends and Insights

The Asia Pacific uncomplicated UTI treatment market is emerging as the fastest-growing regional segment globally, driven by several structural and demographic trends. The region’s large and increasingly urban population, especially in China, India, Japan, and Southeast Asia has heightened the overall incidence of UTIs, particularly among women and the aging population, making early diagnosis and treatment more common. Growth in healthcare infrastructure, expanding access to clinical services, and rising healthcare expenditure are broadening the reach of effective treatment options across both urban and rural areas. Telemedicine and e-pharmacy adoption are improving care access and convenience, while increasing public awareness through health campaigns is encouraging timely medical consultation and antibiotic use. Additionally, government investments and policy support aimed at improving diagnostic capabilities and infectious disease care are reinforcing this expansion. However, antibiotic resistance and variability in healthcare quality remain challenges, prompting demand for innovative therapies and stewardship initiatives. Overall, these dynamics position Asia Pacific as a high-potential and rapidly evolving market for uncomplicated UTI treatments.

Competitive Landscape

The uncomplicated UTI treatment market is highly competitive, driven by a mix of innovative pharmaceutical companies and generic drug manufacturers. Competition centers on antibiotic efficacy, safety profile, dosing convenience, and resistance management. Companies are investing in research and development of novel antibiotics, as well as expanding their distribution channels through hospitals, retail pharmacies, and online platforms to capture a wider patient base. Price competitiveness and regional market penetration are also key strategies, particularly in emerging markets.

Key Developments:

- In August 2025, Iterum Therapeutics launched ORLYNVAH™, the first oral penem antibiotic for uncomplicated urinary tract infections (uUTIs) in the United States. The drug, approved by the U.S. Food and Drug Administration for adult women with limited or no alternative oral antibacterial options, was the first new branded uUTI treatment introduced in over 25 years and the first oral penem antibiotic to become commercially available in the U.S. This launch provided a new treatment option for clinicians and patients facing rising antibiotic resistance and was positioned to reduce emergency department visits and hospital admissions.

Companies Covered in Uncomplicated Urinary Tract Infection (UTI) Treatment Market

- Pfizer Inc.

- Merck & Co., Inc.

- GlaxoSmithKline plc

- Bayer AG

- Johnson & Johnson

- AbbVie Inc.

- F. Hoffmann-La Roche Ltd

- Dr. Reddy’s Laboratories Ltd.

- Cipla Ltd.

- Lupin Limited, Aurobindo Pharma Ltd.

- Novartis AG

- Teva Pharmaceutical Industries Ltd.

- Sun Pharmaceutical Industries Ltd.

- Glenmark Pharmaceuticals Ltd.

Frequently Asked Questions

The global Uncomplicated Urinary Tract Infection (UTI) Treatment market size is expected to be around US$ 6.3 billion in 2026, reflecting strong underlying incidence, high treatment rates, and continued reliance on short-course oral antibiotics worldwide.

Key demand drivers include the very high lifetime incidence and recurrence of uncomplicated UTI in women, guideline preference for oral first-line antibiotics such as nitrofurantoin and trimethoprim sulfamethoxazole, and growing access to primary care, urgent care, and telehealth services that facilitate timely diagnosis and prescription.

North America is the leading region, supported by high diagnosis and treatment rates, advanced antimicrobial stewardship and surveillance systems, strong reimbursement coverage, and rapid adoption of innovative oral agents and digital prescribing and dispensing platforms.

A major opportunity lies in the commercialization of novel agents such as gepotidacin and in expanding integrated care models that couple optimized oral regimens with telemedicine triage and online pharmacy fulfillment, especially in regions with high antimicrobial resistance and rising demand for convenient care.

Key market players include Pfizer Inc., Merck & Co., Inc., GlaxoSmithKline plc, Bayer AG, Johnson & Johnson, AbbVie Inc., F. Hoffmann-La Roche Ltd, Dr. Reddy’s Laboratories Ltd., Cipla Ltd., Lupin Limited, Aurobindo Pharma Ltd., and Novartis AG, along with several other multinational and regional generic manufacturers.