- Pharmaceuticals

- Nicotine Replacement Therapy (NRT) Market

Nicotine Replacement Therapy (NRT) Market Size, Share, and Growth Forecast, 2025 - 2032

Nicotine Replacement Therapy (NRT) Market By Product Type (Nicotine Patches, Gums, Lozenges, Inhalers), Therapy Type (Monotherapy, Combination), Route of Administration, Distribution Channel, and Regional Analysis for 2025 - 2032

Nicotine Replacement Therapy (NRT) Market Size and Trends Analysis

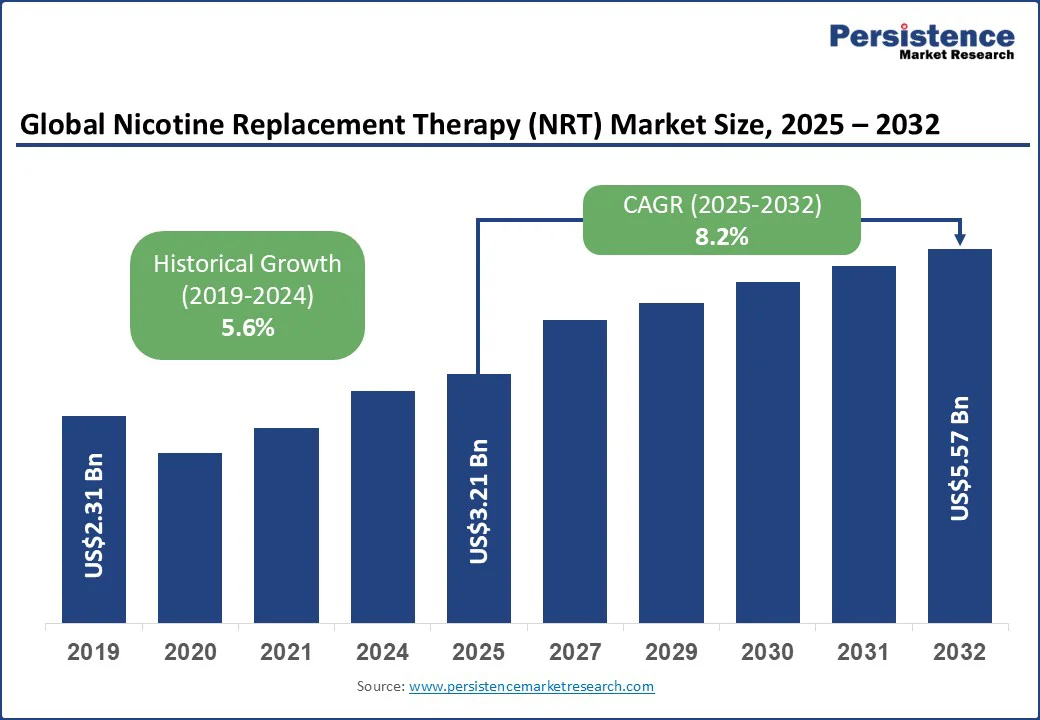

The global nicotine replacement therapy (NRT) market size is likely to be valued at US$3.21 Bn in 2025 and is expected to reach US$5.57 Bn by 2032, growing at a CAGR of 8.2% during the forecast period from 2025 to 2032.

Key Industry Highlights

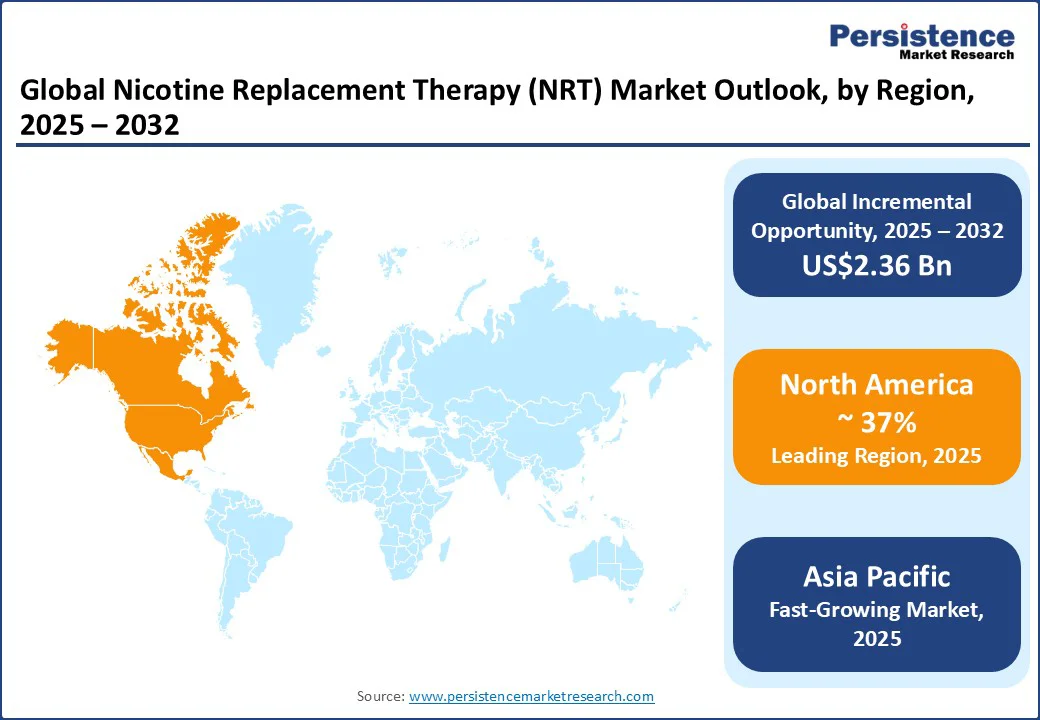

- Leading Region: North America is anticipated to dominate the NRT market with a 37% share in 2025, supported by strong retail penetration, clinical endorsements, and the FDA’s recent PMTA approvals for nicotine pouches.

- Fastest-growing Region: Asia Pacific is expected to be the fastest-growing market, driven by rising government cessation initiatives in countries including India and China, and growing retail availability of oral NRT formats.

- Investment Plans: Key players are investing in oral nicotine innovations and telehealth-enabled cessation platforms, with launches such as ZYN’s PMTA-approved pouches in the U.S. and localized flavor portfolios for Europe and Asia.

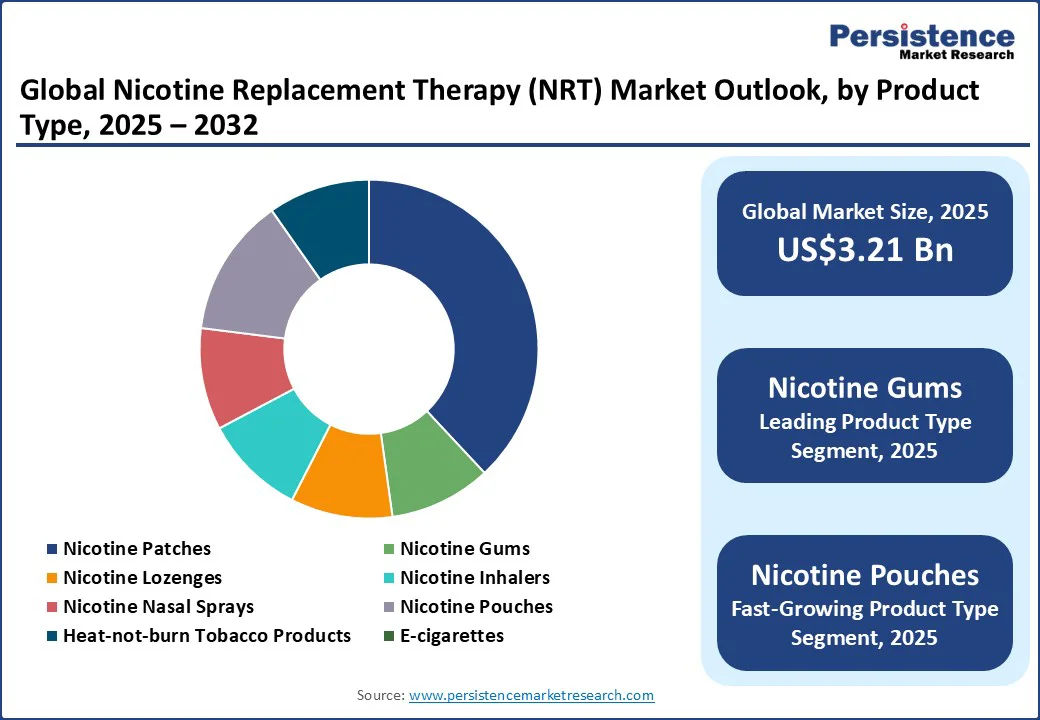

- Dominant Product Type: Nicotine gums are projected to hold the largest share at 43% in 2025, benefiting from consumer familiarity, OTC access, and flexible dosing options.

- Fastest-growing Route of Administration: Inhalation & nasal NRT is the fastest-growing category, expanding due to discreet usage, rapid nicotine delivery, and adoption in emerging markets where oral formats face cultural constraints.

| Global Market Attribute | Key Insights |

|---|---|

| Nicotine Replacement Therapy (NRT) Market Size (2025E) | US$3.21 Bn |

| Market Value Forecast (2032F) | US$5.57 Bn |

| Projected Growth (CAGR 2025 tos 2032) | 8.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.6% |

The nicotine replacement therapy (NRT) market, comprising medically approved products such as nicotine gums, patches, lozenges, inhalers, and mouth sprays, plays a pivotal role in helping individuals overcome tobacco dependence.

The rise in public health initiatives, favorable regulatory frameworks, and growing awareness of smoking-related health risks drives a steady adoption through prescription and over-the-counter channels. The market growth is further fueled by product innovations, expanding distribution via e-commerce and pharmacies, and increasing insurance coverage, positioning NRT as a key component of smoking cessation strategies worldwide.

Market Dynamics

Driver - Regulatory Shifts and Digital Integration

Regulatory developments are reshaping the nicotine replacement therapy market by expanding its definition to include certain pharmacist-supervised nicotine pouches, improving clinical acceptance, and enhancing retail visibility. Strong evidence supporting combination nicotine replacement therapy is influencing clinical guidelines, encouraging manufacturers to launch bundled products that combine fast-acting formats such as lozenges with longer-acting patches.

Expanded Medicaid and private payer coverage are reducing out-of-pocket costs, increasing adoption among price-sensitive and high-risk populations. At the same time, flavor restrictions and behind-the-counter rules are creating opportunities for premium, pharmacist-supervised product positioning in pharmacies.

Digital health integration is also driving growth, with telehealth platforms now routinely offering NRT prescriptions and linking patients directly to e-commerce fulfillment for rapid home delivery. This model expands access to rural populations and younger demographics while increasing subscription-based and repeat purchases through online pharmacies and direct-to-consumer channels.

Manufacturers are leveraging real-world adherence data to address behavioral and information gaps by introducing adherence aids, flavor innovations, and digital reminders. These combined efforts are fostering a market shift toward niche offerings and bundled digital cessation programs that integrate counseling, delivery, and NRT products into a seamless patient experience.

Restraint - Product Limitations and Emerging Alternatives Impact Adherence in NRT Categories

In the transdermal and oral NRT categories, product-specific limitations are increasingly affecting adherence. Patch-induced contact dermatitis and localized skin irritation often lead to early discontinuation, while denture adhesion issues and incorrect chewing techniques with nicotine gum cause inconsistent dosing and gastrointestinal discomfort.

Nicotine lozenges can trigger mucosal irritation, hiccups, and heartburn when used improperly, resulting in higher dropout rates. Early clinical findings also point to gum recession and oral ulcers linked to nicotine pouch use, which discourage adoption among patients concerned about dental health.

Short-acting NRT formats present a different set of challenges. Inhalers often cause throat irritation, and nasal sprays can be uncomfortable, discouraging long-term use despite their quick relief from cravings. The need for precise dosing across these formats often results in underdosing or misuse in real-world conditions, limiting quit success rates compared to controlled clinical trials.

The growing shift toward e-cigarettes and more sensory-satisfying nicotine alternatives is reducing the addressable market for traditional NRT products, particularly among younger consumers. In some regions, inconsistent pharmacy stocking and limited frontline counseling create further gaps in accessibility, reducing trial-to-repeat purchase conversion.

Opportunity - Telehealth and E-Commerce Drive Growth in Nicotine Replacement Therapy Market

Telehealth and mail-order distribution are creating strong growth avenues for the nicotine replacement therapy (NRT) market. Telehealth-prescribed NRT e-commerce fulfillment enables clinicians to send starter kits and schedule automated refills directly to patients’ homes. Pharmacist-led counseling aligns with a pharmacist-supervised nicotine pouch behind-the-counter model, increasing clinical engagement and promoting upselling of combination regimens.

Robust clinical evidence supporting combination nicotine replacement therapy with fast-acting lozenges is driving the launch of bundled SKUs and clinician-endorsed starter packs. These evolving channels reduce access barriers for rural and underserved populations while supporting subscription-based and recurring revenue models for manufacturers.

Partnerships between NRT providers and digital health platforms are opening opportunities for integrated care packages. A digital smoking cessation plus NRT subscription model can merge app-based cognitive behavioral therapy, personalized coaching, adherence reminders, and scheduled product deliveries into a single solution. With clinical and real-world studies showing that digital therapeutics boost adherence and quit success rates, bundling them with NRT strengthens customer lifetime value.

There is also an emerging product gap for dental-conscious users, creating scope for innovation in dental-friendly, low-irritation nicotine pouch formulations. Pilot programs in pharmacies that provide mailed starter packs followed by automated subscription refills demonstrate that this approach can be scaled effectively, particularly for payer-subsidized patient segments.

Category-wise Analysis

Product Type Insights

Nicotine gums are collectively anticipated to account for estimated 43% share in 2025. Their dominance is driven by broad over-the-counter access, affordability, and strong consumer familiarity, making them the preferred option for initial quit attempts.

Flexible dosing allows users to control cravings on demand, and these formats are often paired with nicotine patches as part of combination therapy, a strategy increasingly supported by clinical guidelines. The high penetration of private-label options in supermarkets, chain pharmacies, and e-commerce platforms further boosts their accessibility and sales volume.

Nicotine pouches are the fastest-growing product type. They offer discreet use, a variety of flavors, and a tobacco-free format, appealing strongly to adult smokers seeking modern, convenient alternatives. Investment and distribution expansion by major tobacco and nicotine companies has accelerated their availability in both retail and online channels. In some regions, regulatory acceptance of certain pouch products as NRT has also opened the door to clinical recommendations and pharmacy placement, further driving uptake.

Route of Administration Insights

Oral NRT, including gums, lozenges, and approved nicotine pouches, is likely to hold an estimated 55% market share in 2025. Their leadership stems from convenience, portability, and the quick relief they offer for breakthrough cravings. Widely available over the counter, these products require minimal user training and are often used alongside patches in combination therapy. The addition of nicotine pouches to this category has amplified its share, as these products cater to modern preferences for discreet, flavored, and smoke-free nicotine options.

Inhalation and nasal formats, which include nicotine inhalers and migraine nasal sprays, are the fastest-growing route of administration. Their appeal lies in rapid nicotine absorption, which closely mimics the speed of cigarette nicotine delivery and provides immediate craving relief.

These formats are gaining traction among heavy or long-term smokers who struggle with cravings during high-stress situations. Recent improvements in inhaler ergonomics and spray formulations have addressed earlier tolerability issues, while telehealth prescriptions and targeted patient education are expanding adoption in both clinical and home-use settings.

Regional Insights

North America Nicotine Replacement Therapy (NRT) Market Trends - Strong Retail Penetration and Clinical Endorsements Driving Cessation Product Uptake

North America is anticipated to be the leading region, accounting for an estimated 37% of the market share in 2025. The nicotine replacement therapy (NRT) is being shaped by rapid channel diversification and the strong emergence of nicotine pouches in both retail and pharmacy settings. In the U.S., the FDA’s 2024 authorization of multiple ZYN nicotine pouch products under the PMTA pathway marked a significant milestone, legitimizing certain pouch formats and accelerating their distribution in mainstream retail.

At the same time, state Medicaid programs and quitline initiatives are expanding starter-kit models that combine patches with fast-acting oral formats, removing cost barriers and improving adherence rates. This combination of regulatory acceptance for some smoke-free alternatives and expanded clinical distribution for evidence-based NRT is creating a more competitive but also more dynamic marketplace.

In Canada, Health Canada has approved selected nicotine pouch products for sale but imposed strict controls such as flavor limits, pharmacist supervision, and behind-the-counter placement. These measures limit youth appeal while positioning approved pouch SKUs within a more clinical, pharmacy-driven channel, an environment that favors pharmacist engagement and evidence-based counseling for patients.

Asia Pacific Nicotine Replacement Therapy (NRT) Market Trends - Government-Led Cessation Programs and Rising Adoption of Oral NRT Formats

Asia Pacific is projected to be the fastest-growing nicotine replacement therapy (NRT) market through 2032. The market presents a dual scenario, with mature regions such as Japan and Australia shaping premium, clinically regulated nicotine categories, while emerging markets drive NRT expansion through public health initiatives. Japan continues to lead globally in the adoption of heat-not-burn products, with devices such as IQOS dominating nicotine consumption. This entrenched use of reduced-risk products shifts the competitive landscape, requiring traditional NRT players to focus on differentiation through clinical efficacy, combination therapy bundles, and targeted medical channels.

In Australia, regulatory restrictions remain tight for nicotine pouches and vapes, which are permitted only by prescription, while the Pharmaceutical Benefits Scheme subsidizes certain NRT patch courses. State quitlines further support access by mailing free starter packs to eligible smokers. This model favors manufacturers that partner with national cessation services, supply subsidized NRT, and ensure compliance with strict import and retail laws, while also contending with the challenge of illicit product availability.

Europe Nicotine Replacement Therapy Market Trends - Flavor Innovation and Regulatory Shifts Reshaping Cessation Product Landscape

Europe’s NRT landscape is defined by regulatory diversity, with national rules creating both risks and opportunities. In the U.K., NHS stop-smoking services have broadened pharmacotherapy access by reintroducing cytisine and expanding varenicline supply, while continuing to provide NRT products as part of comprehensive cessation support. This integrated approach creates a favorable environment for manufacturers who collaborate closely with healthcare providers to supply starter kits aligned with behavioral support programs.

Germany, meanwhile, is experiencing rapid growth in nicotine pouch sales, despite a fragmented regulatory environment where classification rules vary by state and periodic restrictions disrupt distribution. While this growth highlights strong consumer demand, it also highlights the need for agile market-access strategies that adapt to shifting legal frameworks. Across Europe, evolving national rules on flavors, taxation, and product placement mean that market entry strategies must be tailored for each jurisdiction, balancing compliance with opportunities in both retail and clinical channels.

Competitive Landscape

The global nicotine replacement therapy (NRT) market is moderately consolidated, with a mix of pharmaceutical giants, consumer health companies, and tobacco-alternative manufacturers competing across multiple product categories.

Established players such as Johnson & Johnson, GlaxoSmithKline, and Perrigo, maintain strong positions through extensive OTC portfolios, broad retail penetration, and consistent product innovation, such as improved flavor profiles and extended-release formulations. Their long-standing partnerships with healthcare providers and public health organizations also strengthen brand trust and clinical credibility.

Key Industry Developments

- In January 2025, the U.S FDA approved the marketing of 20 ZYN nicotine pouch products under PMTA, legitimizing the brand for mainstream retail and pharmacy sales. This expands the competitive field for smoke-free alternatives and prompts reassessment of pouch versus classic NRT strategies.

- In July 2024, the WHO released its first global clinical guideline for tobacco cessation, endorsing NRT alongside varenicline, bupropion, and cytisine. The move boosts reimbursement potential and public program adoption, especially in low- and middle-income countries.

Companies Covered in Nicotine Replacement Therapy (NRT) Market

- Johnson & Johnson

- GlaxoSmithKline plc

- Perrigo Company plc

- Pfizer Inc.

- Philip Morris International Inc.

- Altria Group, Inc.

- British American Tobacco plc

- Japan Tobacco Inc.

- Imperial Brands plc

- Fertin Pharma A/S

- Cambrex Corporation

- Dr. Reddy’s Laboratories Ltd.

- Cipla Ltd.

- ITC Limited

- KT&G Corporation

- Reynolds American Inc. (RAI)

- NJOY LLC

- Nicorette

- Halewood International Ltd.

- Alchem International Pvt. Ltd.