- Medical Devices

- Mucosal Atomization Device Market

Mucosal Atomization Device Market Size, Share, Trends, Growth, Regional Forecasts, 2026 to 2033

Mucosal Atomization Device Market by Product Type (Nasal Atomization Device, Fiber Optic Atomization Device, Laryngo Tracheal Atomization Device, Bottle Atomizers), End-User (Hospitals, Ambulatory Surgical Centers (ASCs), Specialized Clinics), Technology (Gas-Propelled Atomization Device, Electrical Atomization Device), and Regional Analysis for 2026-2033

Mucosal Atomization Device Market Share and Trends Analysis

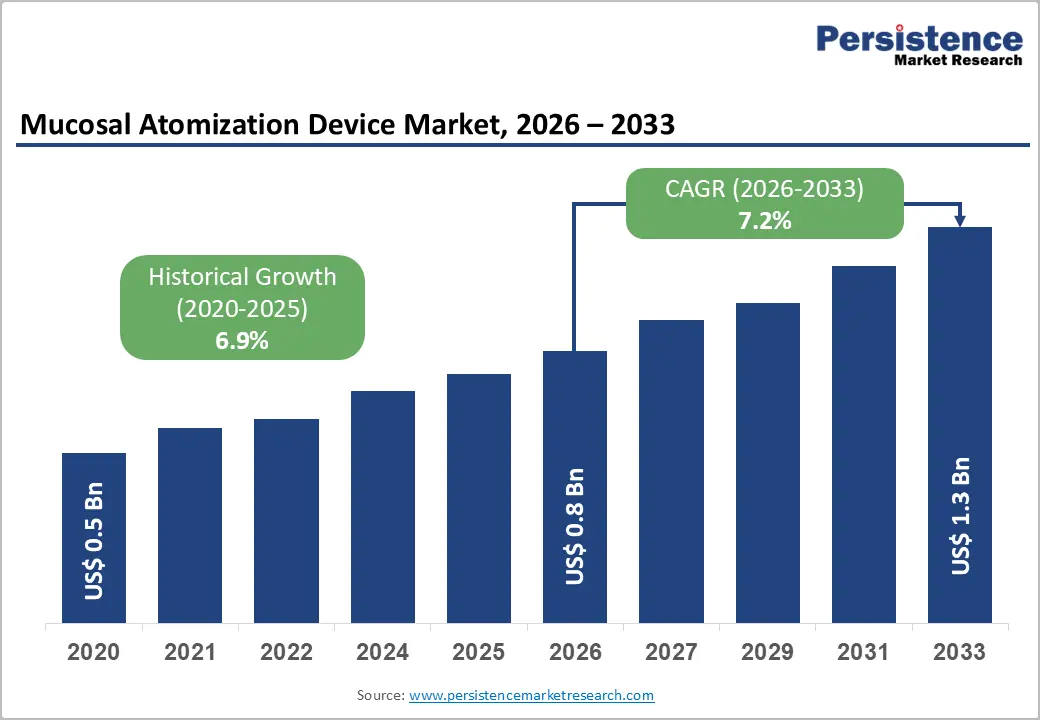

The global mucosal atomization device market size is likely to be valued at US$ 0.8 billion in 2026, and is projected to reach US$ 1.3 billion by 2033, growing at a CAGR of 7.2% during the forecast period 2026−2033. This robust expansion reflects increasing consumer adoption of functional foods and plant-based nutrition solutions. The market's growth trajectory is underpinned by rising health consciousness, regulatory clarity around novel food applications, and expanding distribution channels across both developed and emerging economies. This trend is further supported by the growing body of scientific evidence highlighting the numerous health benefits of chia seeds, including improved cardiovascular health, enhanced digestive function, and better weight management.

Key Industry Highlights

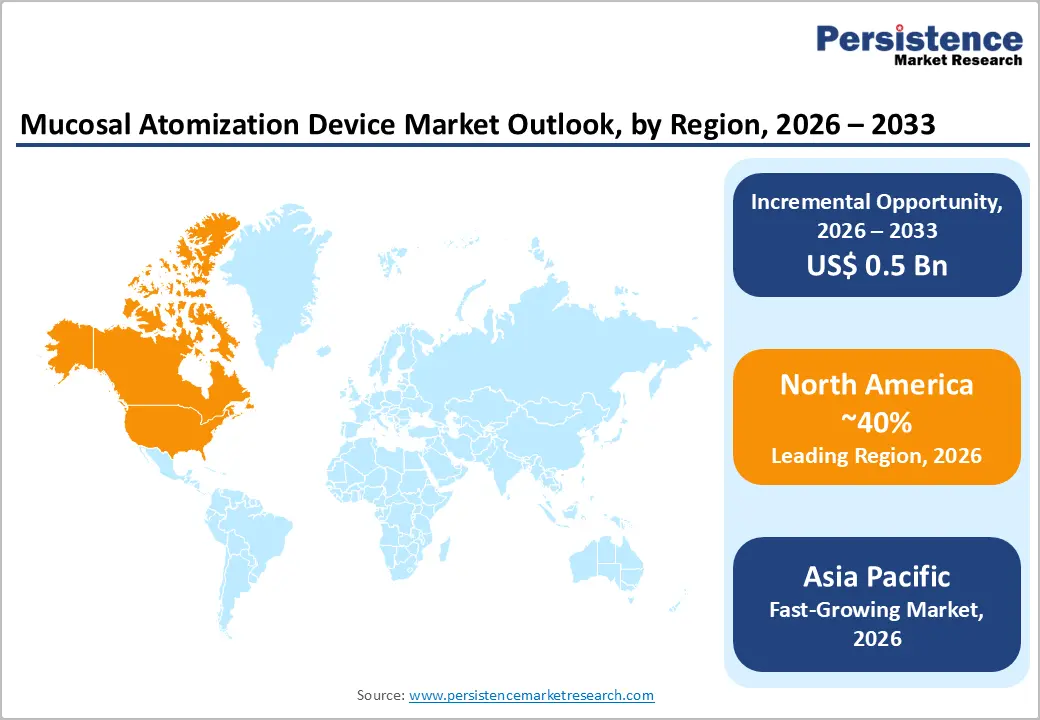

- Dominant Region: North America is expected to command about 40% market share in 2026, supported by substantial healthcare investments and sophisticated medical networks.

- Fastest-growing Market: The Asia Pacific market is set to be the fastest-growing during the forecast period, due to the rapid healthcare infrastructure development.

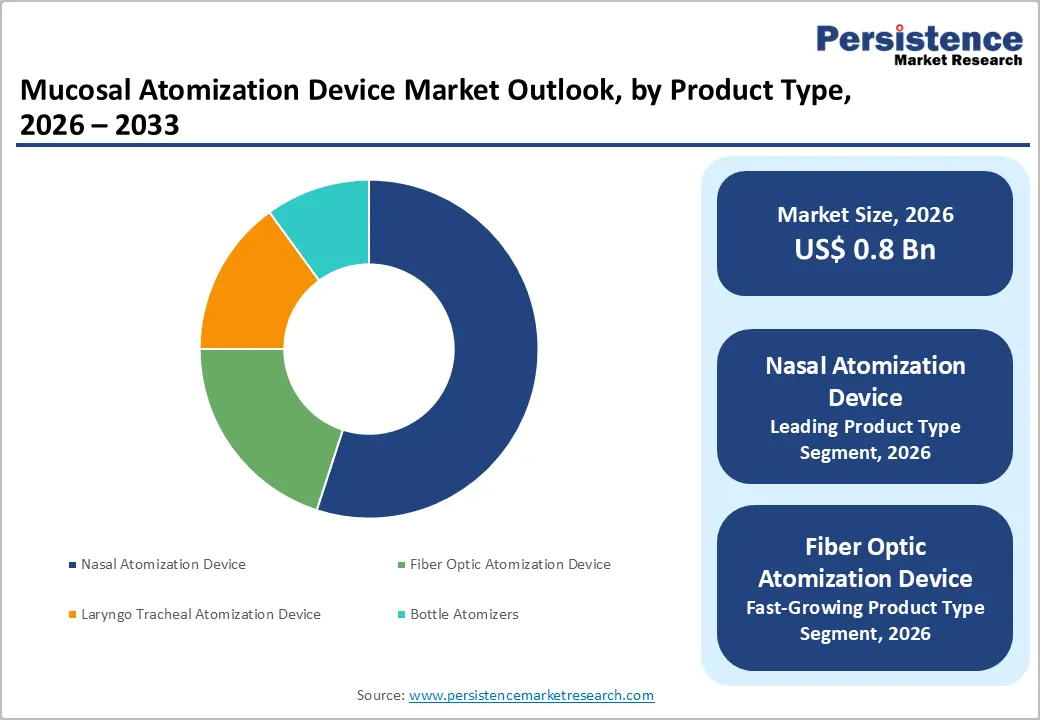

- Leading Product Type: Nasal atomization devices are set to lead with an estimated 55% market revenue share in 2026, boosted by their broad use in emergency medicine, anesthesia, and critical care.

- Fastest-growing Product Type: Fiber optic atomization devices are likely to be the fastest-growing during the 2026-2033 forecast period, fueled by precision requirements in advanced endoscopic and airway procedures.

- Leading & Fastest-growing End-User: Hospitals are expected to capture approximately 48% of the revenue share in 2026, while ambulatory surgical centers (ASCs) are expected to be the fastest-growing segment over the 2026-2033 forecast period.

| Key Insights | Details |

|---|---|

|

Mucosal Atomization Device Market Size (2026E) |

US$ 0.8 Bn |

|

Market Value Forecast (2033F) |

US$ 1.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.9% |

DRO Analysis

Rising Demand for Needle-Free Drug Delivery in Emergency & Acute Care

The global rise in opioid overdose emergencies continues to drive strong adoption of mucosal atomization devices (MADs). First responders and caregivers rely on these tools to deliver life-saving medications through the nasal route. This method bypasses the need for intravenous access, which often proves difficult in urgent situations. According to the U.S. Centers for Disease Control and Prevention (CDC), provisional data indicated that deaths involving opioids were approximately 83,100 in 12 months leading up to the reported drop in 2024. Governments and health agencies in numerous countries now incorporate MAD-compatible naloxone kits into their standard emergency protocols.

Healthcare providers value MADs for their simplicity and speed in real-world scenarios. Laypersons, such as family members, can administer treatments with minimal training, which broadens access beyond professional settings. National preparedness programs will have fully integrated these devices into public health strategies. Enhancing response capabilities worldwide. This shift strengthens institutional commitment and fosters sustained growth in the sector. Policymakers focus on equipping frontline workers with reliable tools, which reduces response times and improves survival rates. MADs gain prominence in emergency kits and training curricula. The trend positions these devices as essential components of future overdose prevention efforts, ensuring broader availability and acceptance among users at all levels.

Regulatory Approvals for Novel Intranasal Formulations

Pharmaceutical companies develop intranasal formulations that target emergency care and chronic conditions. The U.S. Food and Drug Administration (FDA) approved Neffy, a needle-free 2 mg epinephrine nasal spray by ARS Pharmaceuticals, for treating type I allergic reactions, including anaphylaxis in adults and children weighing 30 kg or more, marking the first major innovation in epinephrine delivery in over 35 years. These advancements open new treatment areas beyond traditional applications. Health providers adopt MADs to support these therapies in clinics and hospitals. The trend strengthens demand as providers integrate compatible devices into daily workflows. New intranasal drugs address urgent needs in areas such as allergies and mental health.

Regulatory clearances create clear reimbursement paths that encourage wider adoption. Healthcare systems will have embedded MADs into standard protocols for diverse indications. This evolution positions manufacturers to partner with drug developers for tailored delivery solutions. Payers recognize the value of efficient administration, which reduces costs and improves patient outcomes. In response, MADs gain traction across specialties, from emergency rooms to psychiatric units. The momentum fosters innovation in device design and supports long-term market expansion through reliable clinical partnerships.

High Cost of Advanced Atomization Systems and Reimbursement Gaps

Advanced mucosal atomization devices face challenges due to their higher upfront and per-use costs. Healthcare facilities in regions such as Asia Pacific and Latin America prioritize affordability in procurement decisions. Buyers often favor traditional intravenous systems that align with existing budgets and workflows. These preferences slow the uptake of innovative needle-free options in both community hospitals and larger medical centers. Providers weigh the benefits of rapid delivery against immediate financial pressures, which delay widespread integration. Reimbursement policies create additional hurdles for adoption. Payer systems across countries maintain inconsistent coverage for procedures involving these devices.

Insurers hesitate to establish dedicated billing codes, which leaves providers uncertain about cost recovery. Hospitals and clinics thus limit purchases to pilot programs or high-priority cases. Some markets will have standardized payments for such technologies, yet gaps persist in fragmented healthcare environments. Manufacturers respond by offering tiered pricing models and bundled kits to ease entry barriers. Policymakers could accelerate progress through unified guidelines that recognize efficiency gains from non-invasive methods. Until then, cost-conscious buyers continue to favor proven alternatives, constraining volume growth in emerging economies. This dynamic underscores the need for strategic localization and value-based selling to build long-term acceptance.

Limited Awareness and Training among Healthcare Professionals in Emerging Economies

Developing regions encounter significant obstacles to expanding the market for mucosal atomization devices due to limited training programs for nasal drug delivery methods. Healthcare workers in these areas often lack structured education on proper techniques. Emergency teams prioritize basic life support skills over specialized non-invasive administration. This gap hinders confident use of MADs during critical incidents. Local health authorities struggle to roll out comprehensive workshops, which slows device acceptance among frontline staff. Providers rely on familiar intravenous methods instead, as they require less preparation. Regulatory differences between national agencies and global standards further complicate market entry. Ministries delay approvals for imported devices, which extends timelines for hospital adoption.

Supply chains face disruptions from poor logistics and storage issues, making consistent availability a challenge. Improved coordination will have streamlined clearances in select countries, yet many areas lag behind. Manufacturers address these issues through partnerships with regional trainers and simplified device designs that need minimal instruction. Governments could boost progress by integrating MAD protocols into national curricula and fortifying distribution networks. Until such changes occur, potential users continue to overlook these tools in favor of established options. This situation highlights the value of tailored education campaigns and localized production to overcome entrenched barriers and unlock sustainable growth.

Integration with Smart Drug Delivery and IoT-Enabled Monitoring Platforms

The integration of mucosal atomization technology with smart healthcare systems opens a major growth path. Developers now build next-generation MAD platforms that connect to Internet of Things (IoT) sensors and digital monitoring tools. These features allow real-time tracking of doses and confirmation of patient adherence. Clinicians gain remote access to usage data, thereby improving decision-making during treatment. Hospitals adopt such connected devices to streamline workflows and enhance safety in busy environments. This shift creates demand for advanced solutions that go beyond basic delivery functions.

Healthcare networks will have widely deployed these smart MAD systems across specialties such as emergency care and chronic disease management. Manufacturers partner with technology firms to embed analytics and alerts into devices, which supports proactive interventions. Payers reward these innovations through favorable reimbursement for outcomes-based care. Providers value the ability to reduce errors and optimize therapy, which strengthens market pull for premium tiers. Companies differentiate their offerings with user-friendly apps and cloud integration, capturing higher profits from value-added features. The trend accelerates as digital health platforms mature, positioning MADs as key enablers of efficient, data-driven medicine.

Telemedicine and Remote Care Expansion

The expanding role of telemedicine and remote healthcare creates a strong opportunity for mucosal atomization device makers. Patients in distant or underserved areas now receive care through virtual platforms and home visits. Providers seek simple tools for medication delivery outside clinics. MADs meet this need with their needle-free design, which patients and caregivers use with ease. These devices support quick nasal administration during video consultations or remote check-ins. Healthcare teams guide users in real time, which improves treatment accuracy and confidence. This approach reduces travel burdens and expands access to therapies for chronic conditions or emergencies.

Health systems will have fully woven MADs into digital care networks worldwide. Developers integrate these tools with apps and monitoring systems for instant feedback on usage and results. Clinicians track adherence remotely, which allows timely adjustments to plans. Payers favor such solutions because they lower costs through fewer office visits. Families in rural zones gain independence with guided self-administration, bridging gaps in local services. Manufacturers respond by designing compact models with connectivity features, which appeal to telehealth partners. The shift empowers proactive care models and positions MADs as vital links between virtual oversight and effective delivery. Forward-looking companies seize this trend to build ecosystems that combine device simplicity with data insights, driving sustained adoption across diverse settings.

Category-wise Analysis

Product Type Insights

Nasal atomization devices are expected to dominate by commanding approximately 55% of the market revenue share in 2026, due to its broad use in emergency medicine, anesthesia, and critical care. Clinicians administer essential medications such as naloxone, midazolam, and ketamine through the nasal route in these settings. Numerous randomized controlled trials confirm their clinical effectiveness. Established emergency protocols further reinforce their dependability. This strong evidence base solidifies gas-propelled intranasal devices as the preferred standard for non-invasive drug delivery across high-volume care environments.

Fiber optic atomization devices are likely to be the fastest-growing segment during the 2026-2033 forecast period, fueled by precision requirements in advanced endoscopic and airway procedures. These devices integrate atomization capabilities with visualization technology, enabling targeted drug delivery during laryngoscopy, bronchoscopy, and intubation. Rising procedure volumes for minimally invasive ENT and respiratory interventions accelerate adoption in specialized hospitals and ambulatory centers. Their ability to combine therapeutic delivery with real-time anatomical guidance addresses unmet needs in complex cases.

End-User Insights

Hospitals are slated to hold an estimated 48% of the mucosal atomization device market revenue share in 2026. Their ability to manage diverse acute and chronic conditions that demand efficient drug delivery. High patient volumes require rapid, reliable administration methods, which these devices provide through non-invasive nasal or mucosal routes. Emergency departments, intensive care units, and anesthesia teams rely on them for time-critical medications during high-turnover scenarios. Additionally, hospitals function as primary sites for clinical trials and medical research, where providers test and validate new devices. This role accelerates technology adoption as evidence from controlled studies integrates into standard protocols. Procurement teams prioritize proven solutions with strong clinical backing, ensuring sustained demand across large-scale facilities.

ASCs are set to be the fastest-growing segment over the 2026-2033 forecast period. These facilities prioritize pain management and rapid patient recovery, which align perfectly with the quick absorption and needle-free administration of mucosal delivery systems. ASC staff value the straightforward design of these devices, which integrates easily into streamlined workflows without extensive training. As global demand rises for cost-effective outpatient procedures, ASC networks proliferate worldwide. This trend accelerates procurement of atomization devices to support sedation, analgesia, and anti-emetic protocols during same-day surgeries.

Regional Insights

North America Mucosal Atomization Device Market Trends

North America is set to command a significant portion of the mucosal atomization device market share at approximately 40% in 2026, driven by substantial healthcare investments and sophisticated medical networks. Providers in this region prioritize cutting-edge tools for emergency and critical care applications. The United States drives much of this momentum with its strong pharmaceutical sector and quick embrace of new technologies. Hospitals and clinics integrate these devices into standard protocols for rapid drug delivery. Research institutions test innovations that address local needs, such as overdose response and pain management. Regulatory bodies streamline approvals for safe, effective solutions, which encourages manufacturers to launch products first in this market. Payers support adoption through clear reimbursement paths that recognize clinical value.

The regional market will solidified its position with expanded innovation hubs and partnerships between device makers and drug developers. Companies base operations here to tap into skilled talent and distribution channels. Physicians adopt advanced atomizers for diverse indications, from anesthesia to neurology. Government programs promote emergency preparedness, embedding these tools in public health strategies. This environment fosters competition that drives quality improvements and cost efficiencies. Healthcare leaders focus on patient outcomes, which sustains demand across urban and rural facilities. The region's influence shapes global standards as best practices spread to other markets. Manufacturers gain strategic advantages through early feedback loops and robust trial networks, ensuring long-term leadership in device evolution.

Europe Mucosal Atomization Device Market Trends

Europe maintains steady growth in the mucosal atomization device market, fueled by an aging population and commitment to healthcare progress. Countries such as Germany, France, and the United Kingdom contribute significantly through mature medical networks. Providers adopt these tools for efficient drug administration in hospitals and clinics. National health systems emphasize non-invasive methods that improve patient comfort and speed recovery. Research centers develop enhanced designs tailored to local protocols, which support broader clinical use. Regulators enforce strict safety standards under the European Medicines Agency (EMA) framework, ensuring reliable performance across diverse settings. Payers reward solutions that reduce complications and hospital stays.

The deepened integration of these devices into routine care pathways worldwide. Manufacturers collaborate with regional innovators to refine atomization precision for respiratory and neurological treatments. Policymakers prioritize patient-centered innovations, which align with public health goals. Economic pressures prompt focus on cost-effective models without sacrificing quality. Healthcare teams train staff on standardized techniques, bridging gaps between urban centers and rural facilities. This approach strengthens outcomes in emergency response and chronic disease management. Companies gain a competitive edge through compliance with harmonized guidelines and partnerships with pharmaceutical firms. The continent's influence extends as best practices guide global adoption, positioning Europe as a hub for sustainable device advancement.

Asia Pacific Mucosal Atomization Device Market Trends

Asia Pacific is expected to become the fastest-growing market for mucosal atomization devices, due to rapid healthcare infrastructure development. Governments are investing heavily in hospitals and clinics to serve expanding urban populations. China and India lead this growth through national programs aimed at improving medical access and service quality. Providers are adopting non-invasive delivery tools to manage increasing cases of respiratory and neurological conditions. Local manufacturers are producing cost-effective models to meet diverse clinical needs. Rising healthcare budgets support the procurement of advanced devices for both emergency and routine care. Patients benefit from faster treatments that reduce hospital stays and complications.

The region will be transformed into a global manufacturing hub for these technologies. Policymakers prioritize domestic production, which lowers costs and ensures supply reliability. Physicians integrate atomization systems into protocols for pain control and sedation across specialties. Multinational firms establish partnerships with regional players to customize designs for local preferences. This collaboration accelerates innovation in portable and user-friendly formats. Healthcare networks train staff on efficient techniques, bridging urban-rural divides. The focus on preventive care strengthens demand as communities embrace needle-free options. Companies seize opportunities through localized distribution and regulatory alignment, driving sustained expansion amid demographic shifts.

Competitive Landscape

The global mucosal atomization device market structure is moderately consolidated, dominated by leading players such as Teleflex Incorporated, Aptar Group, Inc., Staccato Medical Ltd., and Aero Pump GmbH. These players collectively capture 55-60% of the market share. The market features a dynamic competitive landscape with established leaders and innovative newcomers. Major companies prioritize research and development investments to improve device performance and safety. They pursue strategic partnerships and product enhancements to address healthcare provider needs. These efforts help them retain market leadership amid evolving clinical demands. Smaller and medium-sized enterprises intensify competition by launching novel solutions that challenge dominant players. This blend of incumbents and agile challengers drives continuous innovation and raises industry standards across diverse care settings.

Key Industry Developments

- In January 2026, a review published by the U.S. National Institutes of Health (NIH) found that mucosal drug delivery, particularly intranasal routes, offers rapid, non-invasive administration with high bioavailability, making it highly effective for acute pain management and emergency care. This supports strong demand for mucosal atomization devices, which enable efficient drug dispersion across nasal surfaces, improving absorption, onset time, and overall therapeutic outcomes in critical care settings.

Companies Covered in Mucosal Atomization Device Market

- Teleflex Incorporated

- Aptar Group, Inc.

- Bespak

- Staccato Medical Ltd.

- Aero Pump GmbH

- BD (Becton, Dickinson and Company)

- Pfeiffer Vacuum

- Nemera SA

- Rexnord

- OptiNose AS

- Currax Pharmaceuticals LLC

- Shin-Etsu Polymer Co., Ltd.

- Sorrento Therapeutics

- ARS Pharmaceuticals

- Rhinostics Inc.

Frequently Asked Questions

The global mucosal atomization device market is projected to reach US$ 0.8 billion in 2026.

The market is driven by advanced healthcare infrastructure and clinical protocol standardization, which accelerates adoption across hospitals and emergency services.

The market is poised to witness a CAGR of 7.2% from 2026 to 2033.

Major opportunities lie in smart device integration with IoT and telemedicine platforms, creating premium growth segments.

Teleflex Incorporated, Aptar Group, Inc., Staccato Medical Ltd., and Aero Pump GmbH are some of the key players in the market.