- Media & Entertainment

- Motion Graphics Market

Motion Graphics Market Size, Share, and Growth Forecast, 2026 - 2033

Motion Graphics Market by Application (Advertising & Marketing, Film & Television Production, Education & E-learning, Healthcare & Medical), Technology (2D Animation, 3D Animation, Real-Time Rendering), Deployment Type (Cloud, Hybrid), and Regional Analysis for 2026-2033

Motion Graphics Market Share and Trends Analysis

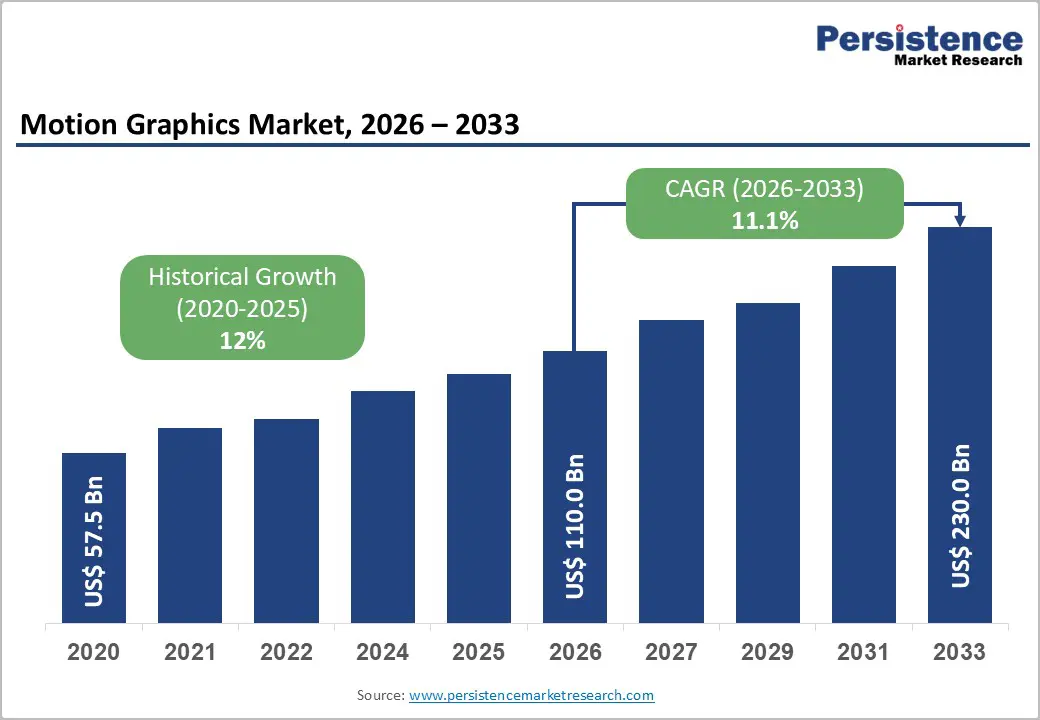

The global motion graphics market size is likely to be valued at US$ 110.0 billion in 2026, and is projected to reach US$ 230.0 billion by 2033, growing at a CAGR of 11.1% during the forecast period 2026−2033. This robust growth is primarily following the accelerating digital transformation across the media and entertainment sectors. Content creators are presently increasing their use of immersive visuals in advertising and corporate communications to capture the attention of digital audiences. The proliferation of streaming platforms and social media channels is currently creating unprecedented opportunities for sophisticated motion graphics applications.

Technological advancements in artificial intelligence (AI) and real-time rendering capabilities are presently lowering production barriers for smaller studios. These smart tools automate repetitive tasks, such as keyframe generation and color grading, allowing designers to focus on higher-level creative concepts. The integration of these intelligent systems has significantly enhanced the speed and quality of visual content across all mobile and web-based platforms. This ongoing innovation is ensuring that motion graphics continue to evolve as an essential component of interactive user experiences and modern digital marketing strategies.

Key Industry Highlights

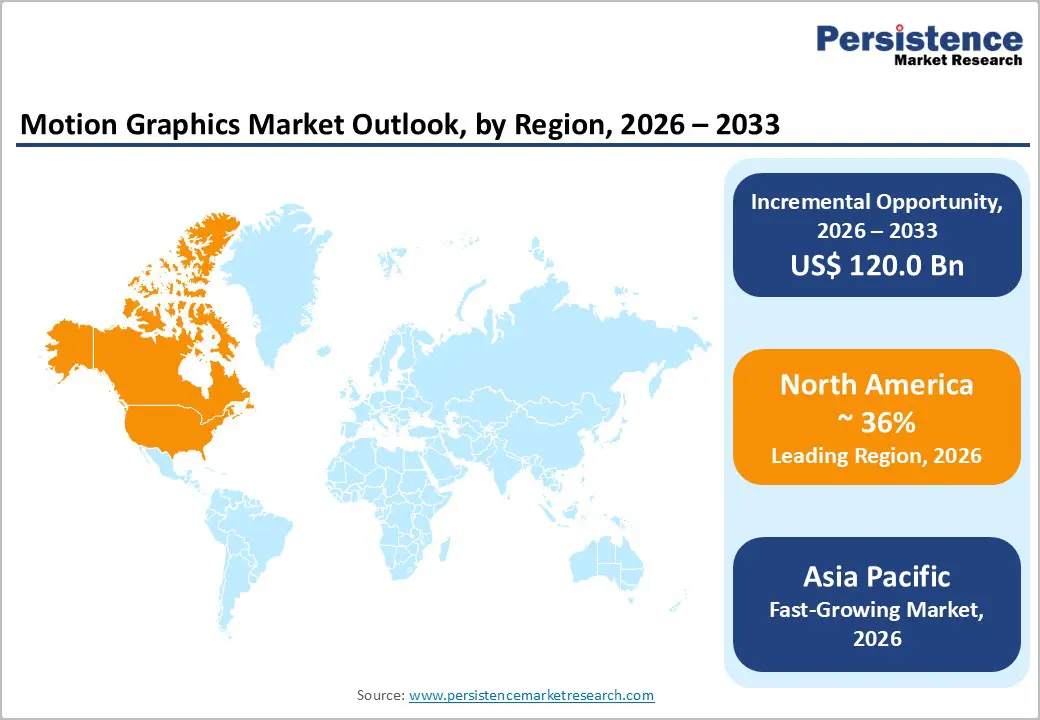

- Dominant Region: North America is set to command around 36% of the market share in 2026, driven by the combined strength of its entertainment, technology, and advertising ecosystems.

- Fastest-growing Regional Market: Asia Pacific is anticipated to emerge as the fastest-growing market, owing to massive digital advertising industries and surging entertainment production.

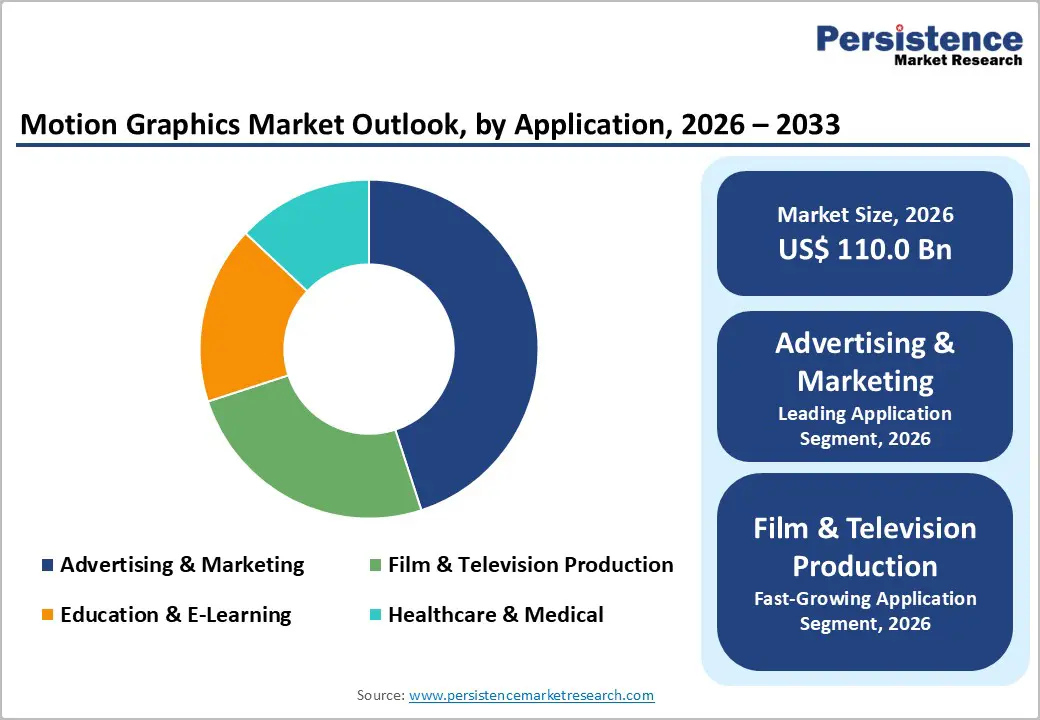

- Leading & Fastest-growing Application: Advertising and marketing are slated to lead with an estimated 38% share in 2026, whereas film and television production is likely to be the fastest-growing segment during the 2026-2033 forecast period.

- Market Driver: The global pivot toward digital media consumption is now a structural growth engine for the motion graphics market.

- Market Opportunities: Generative AI is reshaping how organizations plan, produce, and scale motion graphics across the content lifecycle.

- September 2025: Adobe released more than 90 new built-in effects, transitions, and animations in Premiere Pro 25.5, enhancing motion capabilities and workflow without the need for separate plugins.

| Key Insights | Details |

|---|---|

| Motion Graphics Market Size (2026E) | US$ 110.0 Bn |

| Market Value Forecast (2033F) | US$ 230.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 11.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 12% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Exponential Growth in Digital Content Consumption

The global pivot toward digital media consumption is now a structural growth engine for the motion graphics market. As users spend more time in digital ecosystems such as streaming platforms, social networks, and e-learning environments, their expectations for visually rich, narrative-driven content continue to rise. Enterprises increasingly recognize that static formats struggle to capture attention in crowded digital channels. Marketing, product, and communications teams now treat motion graphics as a core capability rather than a discretionary creative add-on. This shift is reshaping budget allocations, technology roadmaps, and content strategies across industries.

Organizations use motion graphics to differentiate their brand presence, simplify complex messages, and build stronger customer engagement across touch points. Senior leaders increasingly evaluate motion design investments against measurable outcomes such as conversion uplift, audience retention, and training effectiveness. This outcome-based mindset is driving demand for scalable workflows, integrated tool chains, and closer collaboration among creative, data, and marketing teams. Companies that develop strong internal or partner capabilities in motion graphics are better positioned to communicate clearly, respond quickly to market changes, and remain relevant in an environment where attention is one of the scarcest business resources.

Content Saturation and Declining Attention Metrics

Rising audience fatigue and declining engagement quality are beginning to limit the effectiveness of motion graphics as a marketing and communication tool. As users encounter a constant stream of animated content across social media, streaming platforms, and corporate websites, they become more selective about what they watch. Viewers increasingly skip or ignore content that feels repetitive, overly promotional, or misaligned with their interests, which reduces the impact of standard motion graphics executions. This environment places pressure on brands that continue to rely on volume and frequency rather than relevance, narrative clarity, and user-centric design.

These headwinds require organizations to shift from a production-focused mindset to an outcome-focused approach. Teams need to position motion graphics within a broader experience strategy that prioritizes audience insights, clear messaging, and channel-specific optimization. This approach includes testing creative variations, aligning content with specific stages of the customer journey, and integrating motion assets with data-driven targeting and personalization efforts. Companies that reframe motion graphics as a tool for clarity and value creation, rather than as a purely aesthetic asset, are more likely to protect margins, sustain engagement, and maintain credible performance with stakeholders.

Integration with Generative AI and Automated Content Production

Generative AI is reshaping how organizations plan, produce, and scale motion graphics across the content lifecycle. Creative teams no longer rely solely on manual workflows and can use AI systems to automate repetitive tasks, surface design options, and accelerate early-stage concept development. This change allows designers to focus more on storytelling, brand alignment, and visual quality, while the tools manage activities such as asset generation, layout adaptation, and basic animation passes. As text-to-video engines mature, they increasingly serve as rapid-prototyping environments, allowing teams to test narrative ideas, tone, and visual direction before committing resources to high-fidelity production.

These capabilities change how leaders think about investment, capability building, and governance in motion design. Decision-makers can view AI-assisted motion graphics as a lever to increase creative throughput, diversify content portfolios, and support more granular audience segmentation without linearly increasing headcount. Real-time personalization and dynamic rendering also open the door to experiences that adapt to context, intent, and user history, which strengthens the role of motion graphics within broader customer journey design. Executives need to balance speed and scale with controls on brand consistency, the ethical use of AI, and workforce upskilling, so that human talent and automated systems reinforce rather than undermine each other.

Category-wise Analysis

Application Insights

Advertising and marketing are slated to maintain a dominant position in the market, with an estimated 2026 share exceeding 38%. This leadership position reflects the central role of motion graphics in digital advertising campaigns, social media marketing, and brand storytelling initiatives. Brands use animated visuals to quickly capture attention, clearly communicate propositions, and maintain consistency across channels such as display, mobile, and connected television. Marketing teams increasingly integrate motion graphics into always-on content strategies for product launches, seasonal promotions, and ongoing engagement programs. The segment also benefits from ongoing innovation in programmatic advertising, personalized video experiences, and interactive formats that support deeper audience participation and more actionable insight generation.

Film and television production is likely to be the fastest-growing segment during the 2026-2033 forecast period. Streaming platform proliferation continues to drive sustained demand for motion graphics in title sequences, visual effects integration, and informational overlays that support navigation and context. Content owners rely on animated typography, logo treatments, and transitions to reinforce brand identity and create distinctive viewing experiences across genres such as drama, sports, and factual programming. Accessible motion graphics software has lowered creative and technical barriers for independent producers, allowing smaller teams to achieve professional visual standards. This democratization broadens the supplier base for streaming platforms and significantly expands the addressable market beyond traditional studio ecosystems.

Technology Insights

2D animation is expected to account for approximately 45% of the motion graphics market revenue share in 2026. This dominance stems from the broad applicability of the technology across social media content, explainer videos, and user interface animations, where concise and clear communication is critical. Teams use two-dimensional motion graphics to create consistent visual narratives that adapt easily to formats such as short-form posts, product demonstrations, and in-app experiences. The relatively low production complexity and fast turnaround make this approach well-suited to high-volume content pipelines, where marketers and agencies must respond quickly to campaign requirements while maintaining quality and platform compatibility.

3D animation is projected to be the fastest-growing segment over the 2026-2033 forecast period. Advancements in real-time rendering engines, particularly the adaptation of game engines for motion graphics workflows, have significantly improved the economics of 3D production. Studios and in-house teams can now iterate more quickly, visualize changes instantly, and shorten approval cycles, making 3D motion graphics more accessible across a broader range of projects. Adoption in areas such as product visualization, architectural presentations, and medical communications is creating diversified revenue streams that extend beyond entertainment and advertising. Because 3D work often delivers higher perceived value and impact than two-dimensional alternatives, providers can position these services at premium price points, supporting revenue growth even when project volumes remain relatively limited.

Deployment Type Insights

The cloud-based deployment is poised to lead with an approximate 52% of the motion graphics market share in 2026. Cloud-based platforms enable real-time collaboration, centralized asset management, and streamlined review cycles, which reduces friction in coordination among clients, creatives, and technical specialists. Flexible subscription models also lower upfront investment requirements, making professional-grade infrastructure accessible to smaller studios and independent creators. As more organizations adopt cloud-first production strategies, they gain greater scalability, faster turnaround times, and a stronger ability to align capacity with project demand.

Hybrid deployment is expected to be the fastest-growing segment during the 2026-2033 forecast period. This approach addresses data security concerns in sectors that handle sensitive content, including defense, healthcare, and financial services. Enterprise clients increasingly adopt hybrid architectures to balance high-performance rendering for complex projects with cloud scalability for collaborative editing and asset sharing. As these models mature, organizations gain more control over where data resides and how workloads run, while still benefiting from flexible capacity and modern workflow tools that support larger, more strategic engagements with technology providers.

Regional Insights

North America Motion Graphics Market Trends

North America is set to command a sizable portion of the market share, standing at approximately 36% in 2026, driven by underpinned by the combined strength of its entertainment, technology, and advertising ecosystems. The United States drives most of this activity, with major film and television hubs in states such as California and New York creating sustained demand for sophisticated title sequences, visual effects, and broadcast packages. Technology companies in leading innovation centers use motion graphics for user experience design, product storytelling, and platform branding, which reinforces their role as a core capability rather than a niche creative service. Large enterprises treat motion graphics as a strategic lever to differentiate digital experiences, support premium brand positioning, and translate complex product value propositions into clear, accessible visual narratives.

The regional regulatory and funding environment further supports this leadership position through strong intellectual property protection and targeted incentives for creative industries. Production credits and support schemes encourage motion graphics and visual effects projects to remain onshore, while also attracting international productions that require advanced talent and infrastructure. The competitive landscape comprises established studios, in-house enterprise teams, and a growing cohort of startups developing specialized tools and automation for design, rendering, and collaboration. Canada adds further depth to the region by offering cost-effective production capacity and policy support for creative technology development, which helps position North America as an integrated hub for both premium content creation and scalable service delivery.

Europe Motion Graphics Market Trends

Europe represents a structurally important pillar of the motion graphics market, supported by the region’s diversified industrial base and strong creative heritage. Germany anchors demand through its automotive and industrial sectors, where technical visualization, product animation, and process simulations support engineering, marketing, and training needs. The United Kingdom builds on London’s role as an advertising and media hub, combining agency networks, broadcasters, and streaming platforms that rely on motion graphics for brand identity, campaign execution, and broadcast packages. France contributes through a mature animation ecosystem and long-standing public support for cultural production, while Spain and Southern Europe add momentum through rapid digital marketing adoption and increasing investment in online video content.

Regulation and policy act as important accelerators rather than simple constraints in this landscape. European Union digital accessibility rules and web standards encourage the use of motion graphics in public information, citizen services, and commercial interfaces, provided the content remains inclusive and compliant. The General Data Protection Regulation (GDPR) has also increased the need for clear, visually supported explanations of privacy practices, consent flows, and data rights, prompting organizations to invest in structured, easy-to-understand animated communication.

Asia Pacific Motion Graphics Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing market for motion graphics from 2026 to 2033, driven by massive digital advertising markets, government digitalization initiatives, and expanding entertainment production. China’s policy focus on cultural and creative industries positions motion graphics within a broader agenda to expand digital content exports and raise the quality of domestic media. Japan builds on its established animation and design traditions to serve both entertainment and enterprise needs, using motion graphics for technical visualization, product storytelling, and corporate communication. India’s growth reflects the convergence of film, streaming platforms, startups, and national digital programs, creating a large, price-sensitive, and innovation-oriented client base for motion graphics services.

Cost advantages and supportive policy frameworks further strengthen Asia-Pacific’s appeal for regional and global clients. Lower labor and operating costs enable competitive outsourcing models, allowing international studios and brands to scale production while keeping budgets under control. Within the ASEAN bloc, markets such as Singapore, Malaysia, and Thailand are developing specialized production clusters backed by creative economy incentives and skills development programs. Multinational studios and platforms are increasingly establishing regional facilities and partnerships, using the Asia-Pacific as both a cost-efficient delivery base and a source of culturally relevant content for local and global audiences.

Competitive Landscape

The global motion graphics market is moderately fragmented, with leading players including Adobe Inc., Autodesk Inc., Maxon Computer GmbH, Blackmagic Design Pty Ltd., and Corel Corporation. Market fragmentation is increasing as larger investors and industry players consolidate capabilities through targeted acquisitions, with private equity firms often buying mid-sized studios to build greater production scale and geographic reach. These roll-up strategies aim to create integrated networks that can handle complex, multi-market briefs and offer clients more predictable delivery, pricing, and capacity.

Competitive positioning is becoming more defined between technology providers that supply software platforms and service providers that deliver creative production, resulting in distinct roles within the broader ecosystem. Software vendors compete on workflow efficiency, automation, and integration with other enterprise systems, while production companies differentiate through creative quality, sector expertise, and the ability to translate client objectives into effective motion graphics assets.

Key Industry Developments

- In October 2025, YouTube introduced a major visual refresh across its mobile, web, and TV apps, featuring a cleaner video player, smoother navigation, and improved motion design for actions like double-tap to skip. The update also introduces playful custom-like animations tied to video content, streamlined Watch Later and playlist saving, and threaded comments that make conversations easier to follow.

- In September 2025, Maxon rolled out a new Maxon One “Design” update that introduces a refreshed, modular visual identity across its ecosystem of 3D, motion graphics, and VFX tools. The Fall release focuses on stronger brand cohesion and a cleaner, more flexible interface design while continuing to deliver workflow and feature improvements for artists using Cinema 4D, Redshift, ZBrush, Red Giant, and related products.

- In March 2025, Rodeo FX acquired Mikros Animation from Technicolor Group, taking over all its operations and equipment while allowing the studio to continue functioning under its own brand and leadership team. The deal combines Mikros’ strong track record in feature and episodic animation with Rodeo FX’s VFX expertise and global expansion strategy, aiming to create a larger creative hub without diluting Mikros’ distinct style.

Companies Covered in Motion Graphics Market

- Adobe Inc.

- Autodesk Inc.

- Maxon Computer GmbH

- The Foundry Visionmongers Ltd.

- Blackmagic Design Pty Ltd.

- SideFX Software

- Blender Foundation

- Corel Corporation

- Nemetschek Group

- Runway ML Inc.

- Boris FX Inc.

- Red Giant LLC

- Toon Boom Animation Inc.

- NewTek Inc.

- Cavalry.scenegroup

Frequently Asked Questions

The global motion graphics market is projected to reach US$ 110.0 billion in 2026.

The market is driven by growing digital media consumption, enterprise demand for video-based communication, and advances in creative technologies such as AI and real-time rendering.

The market is poised to witness a CAGR of 11.1% from 2026 to 2033.

Integration with extended reality (XR) and text-to-video automation and the rise of template-based and software-as-a-service (SaaS) tools that democratize motion graphics for smaller businesses are unlocking high-value opportunities.

Adobe Inc., Autodesk Inc., Maxon Computer GmbH, Blackmagic Design Pty Ltd., and Corel Corporation are some of the key players in the market.