- Construction & Engineering

- Modular & Prefabricated Construction Market

Modular & Prefabricated Construction Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Modular & Prefabricated Construction Market Size, Share, and Growth Forecast 2026 - 2033 Product Type (Permanent, Relocatable), Material (Steel, Wood, Concrete, Others), End-user (Real Estate & Developers, Government & Public Sector, Healthcare, Education, Hospitality, Industrial), and Regional Analysis 2026 - 2033

Modular & Prefabricated Construction Market Size and Trend Analysis

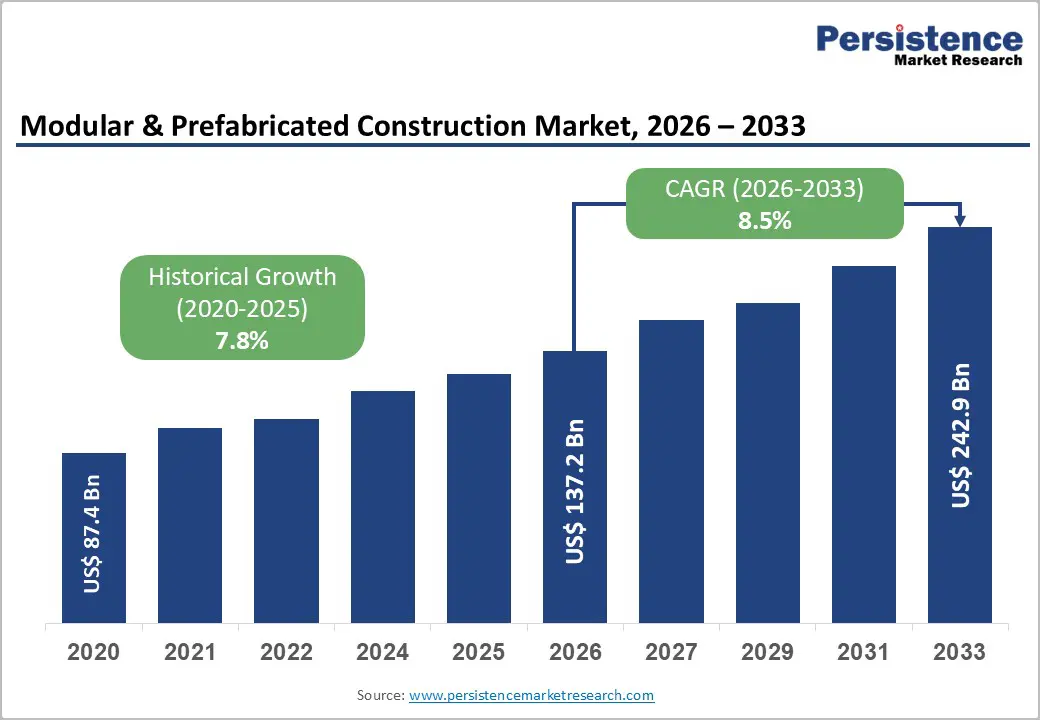

The global modular & prefabricated construction market is projected to reach US$137.2 billion in 2026 and US$242.9 billion by 2033, growing at a CAGR of 8.5% over the forecast period.

This expansion is driven by rising demand for faster project delivery, labor-shortage mitigation, and cost-efficient, high-quality building solutions across residential, commercial, and infrastructure sectors.

Key Industry Highlights:

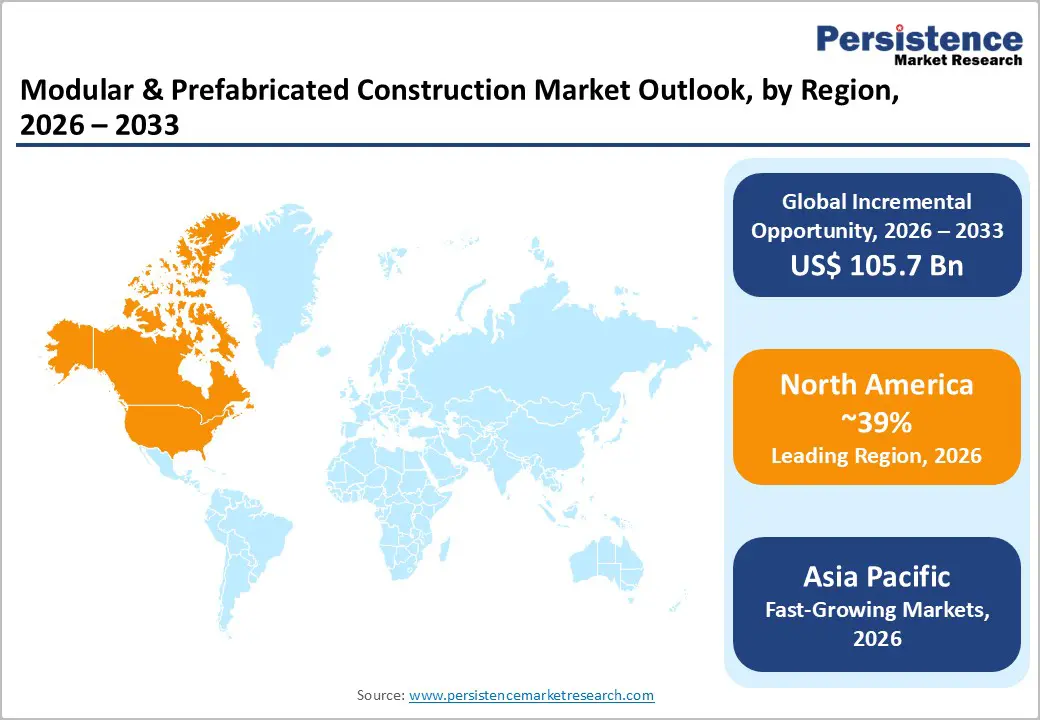

- Leading region: North America leads the Modular & Prefabricated Construction Market with a 49% share, driven by mature regulations, high technology adoption, and large-scale affordable housing and infrastructure programs.

- Fastest-growing region: Asia Pacific is the fastest-growing region with a rising CAGR of 10.2%, driven by rapid urbanization, population growth, and government-backed infrastructure and housing-for-all initiatives in China, India, and ASEAN countries.

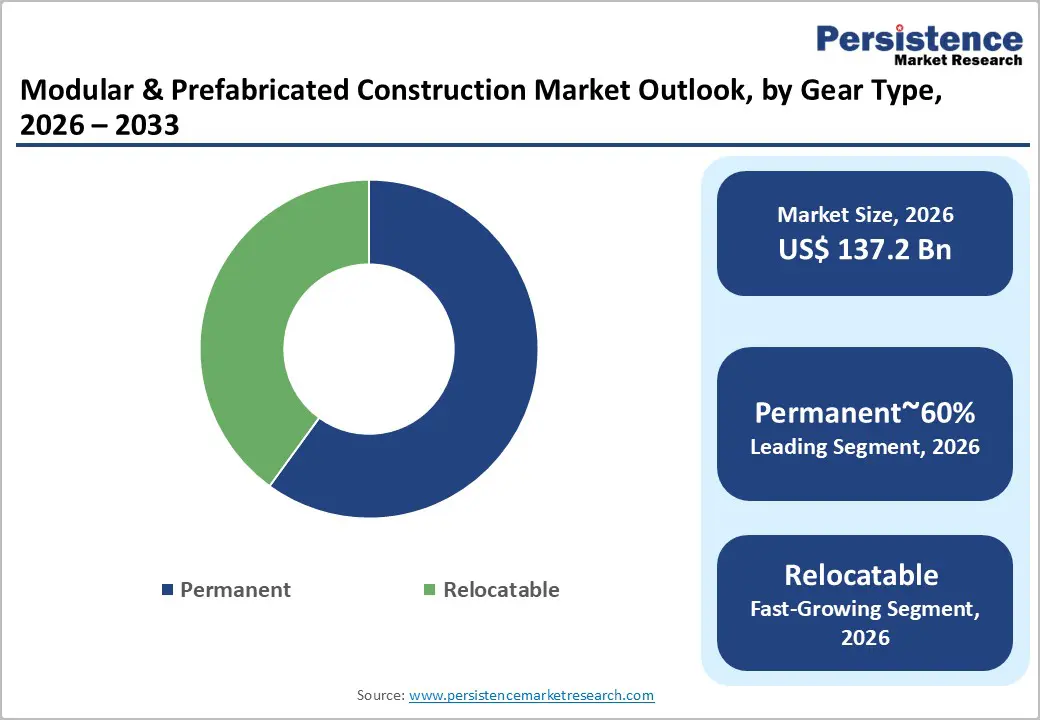

- Dominant segment from any category: The permanent product-type segment dominates, capturing around 60% of the market by providing long-term, structurally robust buildings for multi-family residential, healthcare, and institutional projects.

- Fastest-growing segment across any category: The relocatable product-type segment is the fastest-growing, with share expanding to approximately 20% as temporary housing, disaster-relief shelters, and event-based infrastructure drive demand.

- Key Opportunity: The expansion of permanent modular construction in multi-family and institutional projects presents a major opportunity, particularly in real estate, healthcare, and education sectors seeking faster, high-quality, and sustainable building solutions.

| Key Insights | Details |

|---|---|

| Modular & Prefabricated Construction Market Size (2026E) | US$ 137.2 Billion |

| Market Value Forecast (2033F) | US$ 242.9 Billion |

| Projected Growth CAGR (2026 - 2033) | 8.5% |

| Historical Market Growth (2020 - 2025) | 7.8% |

Market Dynamics

Drivers - Labor shortages are accelerating the adoption of modular construction for faster, efficient, and manpower-optimized project delivery

The global construction industry is facing persistent labor shortages, driven by aging workers and declining interest in skilled trades, as highlighted by organizations such as the International Labour Organization (ILO) and national construction bodies. In North America and Europe, contractors struggle to fill on-site positions, increasing labor costs and project delays. As a result, developers are shifting toward modular and prefabricated construction methods that significantly reduce on-site labor requirements.

Factory-based production enables greater workflow control, faster assembly, and higher quality standards. Industry studies indicate that modular construction can shorten project timelines by 30-50% compared with traditional building methods, while reducing material waste and rework. These productivity gains are especially attractive for residential, commercial, and infrastructure projects with strict deadlines, making modular construction a practical solution to workforce challenges and efficiency pressures across global markets.

Government housing programs and urban infrastructure initiatives are driving large-scale modular construction adoption worldwide

Rapid urbanization across the Asia Pacific and Africa is increasing demand for affordable housing, social housing, and large-scale residential developments. Modular and prefabricated construction offers a fast, scalable, and cost-efficient solution to meet this growing need. Governments in countries such as India, China, and across the European Union are actively promoting off-site construction through housing-for-all programs and public-private partnership initiatives.

India’s Pradhan Mantri Awas Yojana (PMAY) and China’s urban redevelopment projects encourage the use of prefabricated concrete and steel modules to accelerate housing delivery. In addition to residential demand, infrastructure development in healthcare, education, and transportation is increasing the adoption of modular construction. These supportive policies reduce project timelines, control costs, and improve build quality, significantly expanding the market potential for modular and prefabricated construction worldwide.

Restraints - High factory setup costs and limited production capacity restrict rapid modular construction market expansion

Setting up modular and prefabricated manufacturing facilities requires a large upfront investment in factory infrastructure, advanced machinery, automation systems, and specialized logistics networks. These high capital requirements create entry barriers, particularly for small and mid-sized construction firms. Production facilities require large land areas, heavy-lifting equipment, and transport solutions for oversized modules, which are not readily available in many regions.

In emerging markets, weak supply chains, inconsistent power supply, and limited access to high-quality raw materials further constrain factory expansion. As demand rises, limited manufacturing capacity can lead to production bottlenecks, longer lead times, and increased costs. These challenges impede rapid scaling during peak construction periods, slowing overall market growth and reducing modular providers' ability to meet large-volume project requirements efficiently.

Complex regulatory frameworks and inconsistent building codes are slowing modular construction approvals and project execution

Modular buildings must comply with a wide range of building regulations, including fire safety, seismic standards, zoning regulations, and transportation permits, which vary significantly across countries and municipalities. Although many regions are working to align modular standards with traditional construction codes, inconsistencies in inspection procedures and approval processes remain common. Developers often encounter delays due to ambiguous certification requirements and inconsistent interpretations by local authorities.

For international projects, differences in load restrictions, module dimensions, and material testing rules add further complexity to logistics and planning. These regulatory uncertainties increase project costs and risk, particularly for first-time adopters of modular construction. As a result, some developers hesitate to transition from conventional methods, limiting the faster adoption of modular and prefabricated building solutions.

Opportunities - Rising use of permanent modular buildings across residential, healthcare, and institutional sectors is boosting long-term market growth

Permanent modular construction (PMC) represents a major growth opportunity as developers increasingly use it for long-term residential, healthcare, and educational facilities. PMC offers the durability and design flexibility of traditional buildings while delivering faster completion and higher quality control through factory production. Multi-family housing, student accommodations, hospitals, and office complexes are adopting modular systems to meet growing demand and regulatory timelines.

Modern modular designs allow architectural customization, advanced mechanical systems, and high-end finishes, making them suitable for large-scale developments. In North America and Europe, many institutional projects are now delivered using modular methods integrated with BIM and lean construction processes. Additionally, green building certifications such as LEED and BREEAM recognize modular construction for reducing waste and lowering carbon emissions, thereby strengthening its appeal among sustainability-focused developers.

Increasing demand for relocatable modular units in disaster response, healthcare emergencies, and temporary infrastructure projects

Relocatable modular buildings offer strong growth potential in temporary housing, disaster relief, construction-site facilities, and event infrastructure. Organizations such as the United Nations and national disaster response agencies increasingly rely on modular units for the rapid deployment of shelters, field hospitals, and mobile classrooms. These structures can be transported, installed quickly, and reused across multiple locations, making them cost-effective and flexible.

In healthcare, modular clinics and emergency treatment centers have proven essential during pandemics and natural disasters, providing rapid access to medical care that traditional construction would be too slow to provide. Industrial projects also use relocatable modular units for workforce accommodation, site offices, and storage facilities. Their reusability improves asset utilization and lowers long-term investment costs, positioning relocatable modular solutions as a valuable infrastructure option across industries.

Category-wise Analysis

Product Type Insights

The permanent product-type segment holds nearly 60% of the overall market, reflecting strong demand for durable, long-term modular buildings. Permanent modular construction is widely used in residential complexes, hospitals, student housing, and commercial buildings where structural strength and design quality are essential. These buildings are treated similarly to traditional structures in financing and regulatory systems, making them attractive to developers. Permanent modules support multi-story designs, advanced electrical and plumbing systems, and modern architectural finishes. They can also be integrated into existing structures for renovations and expansions. Developers prefer permanent modular solutions because they reduce construction timelines while maintaining high quality and compliance standards. The ability to deliver turnkey projects more quickly improves cash flow, reduces risk, and supports large-scale urban development needs, making this segment the market leader.

Material Insights

Steel dominates the materials segment, accounting for approximately 55% of the market due to its strength, durability, and compatibility with automated manufacturing processes. Steel-frame modular units are commonly used in high-rise residential buildings, commercial spaces, and industrial facilities where structural performance and long spans are required. High-strength steel grades allow lighter structures that meet transport weight limits while maintaining safety standards.

Automated welding and robotic assembly improve precision, reduce labor costs, and increase production speed. Steel also offers excellent resistance to earthquakes, fire, and harsh environments, making it ideal for urban and industrial applications. While concrete and timber modules serve specific markets such as low-rise housing or eco-friendly buildings, steel remains the preferred material for large-scale, high-value modular construction projects worldwide.

End-user Insights

Real estate developers represent the largest end-use segment, accounting for approximately 40% of market demand. Developers increasingly use modular construction for multifamily housing, mixed-use projects, and affordable housing to meet the needs of a growing urban population. Modular methods allow faster project completion, helping developers reduce financing costs and accelerate revenue generation. Studies show project timelines can be reduced by up to 50%, while maintaining high quality standards.

In countries such as China and India, government-supported housing programs have driven large-scale adoption of prefabricated modules for apartment complexes. Developers benefit from predictable construction schedules, improved cost control, and reduced on-site risks. These advantages make modular construction a strategic tool for real estate firms seeking efficient, scalable, and profitable development solutions.

Regional Insights

North America Modular & Prefabricated Construction Trends

North America leads the market in technological adoption and regulatory support, with the United States holding the largest share. The region benefits from advanced manufacturing facilities, standardized building codes, and strong financing systems that support permanent modular construction. Government programs focused on affordable housing and infrastructure modernization actively encourage off-site construction methods.

Modular solutions are increasingly used in residential developments, healthcare expansions, and educational facilities. Major construction firms integrate BIM, automation, and lean construction techniques to improve project efficiency and quality. The region’s strong supply chain, skilled workforce, and regulatory alignment continue to drive widespread adoption, positioning North America as a mature and innovation-driven modular construction market.

Europe Modular & Prefabricated Construction Trends

Europe shows strong demand for sustainable and regulation-compliant modular buildings, particularly in Germany, the UK, France, and Spain. European Union policies promoting carbon reduction and circular economy practices favor factory-based construction due to lower waste and improved resource efficiency.

Countries such as Germany and the UK lead in the use of steel and cross-laminated timber modular systems for residential and institutional projects. France and Spain are expanding modular social housing and student accommodation programs. Harmonization of building standards across the region is improving cross-border project development. Sustainability goals, labor shortages, and urban housing pressures continue to drive growth in modular construction across Europe.

Asia Pacific Modular & Prefabricated Construction Trends

Asia Pacific is the fastest-growing region, driven by urban expansion, population growth, and government-funded infrastructure projects. China and India are rapidly adopting modular construction for residential housing, hospitals, and industrial facilities under national development programs. Japan uses prefabricated modules for earthquake-resistant buildings and efficient urban housing solutions.

Southeast Asian countries such as Singapore, Malaysia, and Indonesia are expanding the use of modular construction for affordable housing and logistics infrastructure. The region benefits from strong manufacturing capabilities, improved transportation networks, and cost-competitive production. These factors position Asia Pacific as the primary growth engine for the global modular and prefabricated construction market.

Competitive Landscape

The modular & prefabricated construction market is moderately consolidated, featuring a mix of global construction firms, specialized modular manufacturers, and regional contractors. Major players such as ACS Group, Bouygues Construction, Larsen & Toubro, Lendlease, Kiewit Corporation, Laing O’Rourke, and Red Sea International dominate through large project portfolios and integrated design-build capabilities.

These companies invest heavily in automation, digital construction platforms, and factory production facilities to improve efficiency and scale. Smaller firms compete by offering niche solutions, regional compliance expertise, and cost-effective project delivery. Strategic partnerships with material suppliers, technology providers, and logistics firms are common. Ongoing mergers and acquisitions are driving consolidation, strengthening market presence, and expanding production capacity across regions.

Key Developments:

- In September 2025, Larsen & Toubro Limited inaugurated a dedicated modular-construction hub in India focused on affordable housing and infrastructure, using steel-frame and prefabricated concrete modules to accelerate project delivery by about 40% while enhancing quality standards.

- In June 2024, Lendlease Corporation formalized a strategic partnership with Berkeley Modular to deliver permanent modular residential and student-housing solutions across Australia and Europe, integrating BIM and lean-construction practices to boost project efficiency and sustainability outcomes.

- In March 2024, ACS Group expanded its modular-construction capacity in Spain by investing in automated production lines for steel-frame modules deployed in residential and healthcare projects, aligning with EU policies on green buildings and circular economy practices.

Companies Covered in Modular & Prefabricated Construction Market

- ACS Group

- Algeco

- Berkeley Modular Limited

- Bouygues Construction

- DUB0X

- Guerdon, LLC

- Hickory Group

- Kiewit Corporation

- Kleusberg GmbH

- Laing O’Rourke

- Larsen & Toubro Limited

- Lendlease Corporation

- Red Sea International

- Riko Group

- Satellite Shelters

Frequently Asked Questions

The Modular & Prefabricated Construction Market is projected to reach US$ 242.9 Billion by 2033, growing at a CAGR of 8.5% from 2026, driven by labor-shortage mitigation, urbanization, and government-backed housing and infrastructure programs.

Key demand drivers include labor shortages, productivity pressures, urbanization, housing-affordability challenges, and government-backed infrastructure and social-housing programs, which push developers toward faster, cost-efficient, and high-quality building solutions.

The Permanent product-type segment dominates, capturing around 60% of the market by providing long-term, structurally robust buildings for multi-family residential, healthcare, and institutional projects.

North America leads the global Modular & Prefabricated Construction Market, supported by mature regulations, high technology adoption, and large-scale affordable-housing and infrastructure programs.

A key opportunity lies in permanent modular construction for multi-family and institutional projects, particularly in real estate, healthcare, and education sectors seeking faster, high-quality, and sustainable building solutions.

Major players include ACS Group, Algeco, Berkeley Modular Limited, Bouygues Construction, DUB0X, Guerdon, LLC, Hickory Group, Kiewit Corporation, Kleusberg GmbH, Laing O’Rourke, Larsen & Toubro Limited, Lendlease Corporation, Red Sea International, Riko Group, and Satellite Shelters, among others.