- Technology

- MiFi Market

MiFi Market Size, Share, and Growth Forecast, 2025 - 2032

MiFi Market By Product Type (Portable Consumer MiFi, Rugged/Industrial MiFi, Others), Cellular Technology (4G LTE, 4G+, Others), End-user, Distribution Channel, and Regional Analysis for 2025 - 2032

MiFi Market Size and Trends Analysis

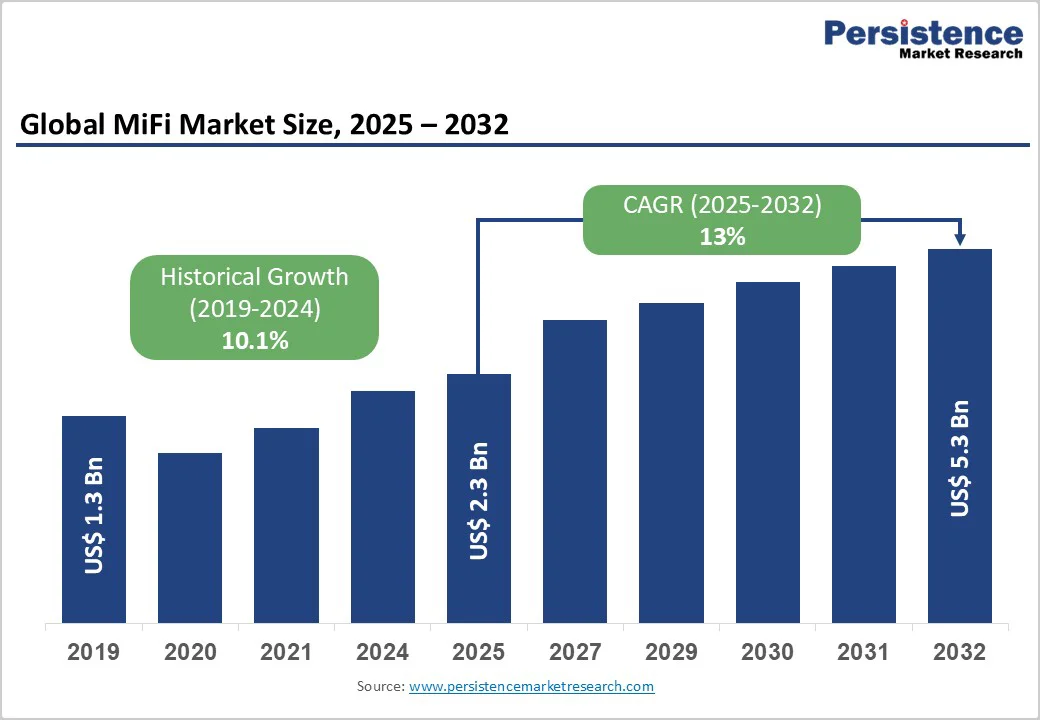

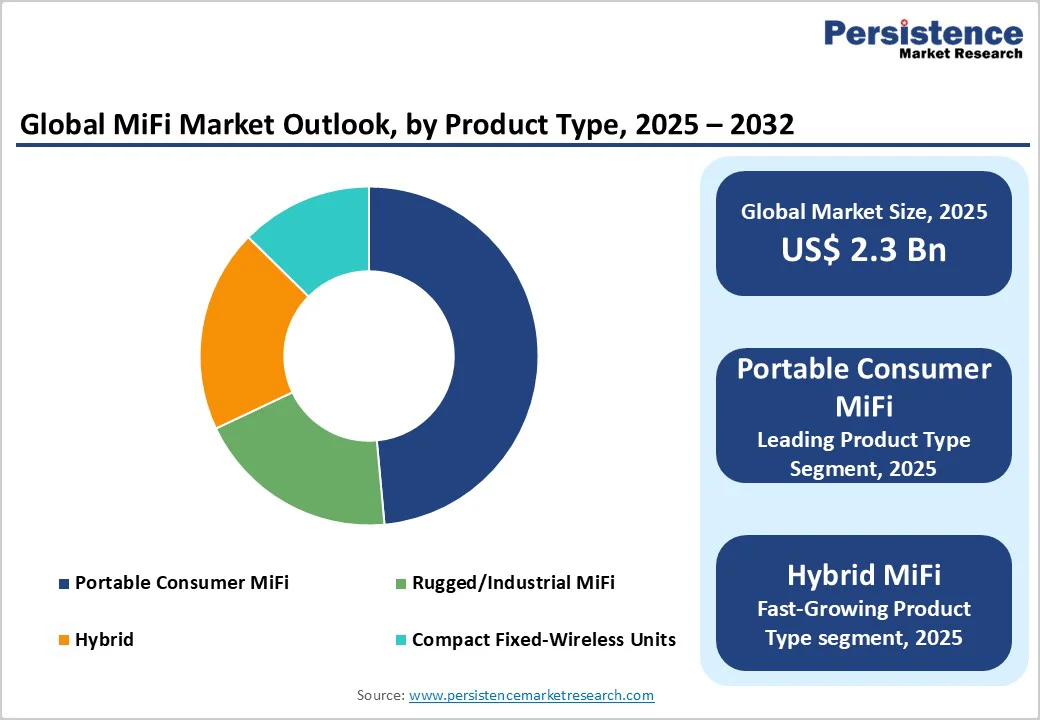

The global MiFi market size is likely to be valued at US$2.3 Billion in 2025 and is expected to reach US$5.3 Billion by 2032, growing at a CAGR of 13% during the forecast period from 2025 to 2032, driven by accelerated 5G rollouts, increasing remote and hybrid work adoption, and a larger installed base of mobile broadband users who demand secure, portable Wi-Fi solutions.

Enterprises use MiFi for temporary sites and field operations, while consumers prefer travel-friendly, multi-device hotspots with built-in batteries. Normalized supply chains and lower chipset costs have boosted shipments since 2022. Wi-Fi 6/6E, eSIMs, and hybrid power-bank designs are enhancing functionality and accelerating replacement cycles.

Key Industry Highlights

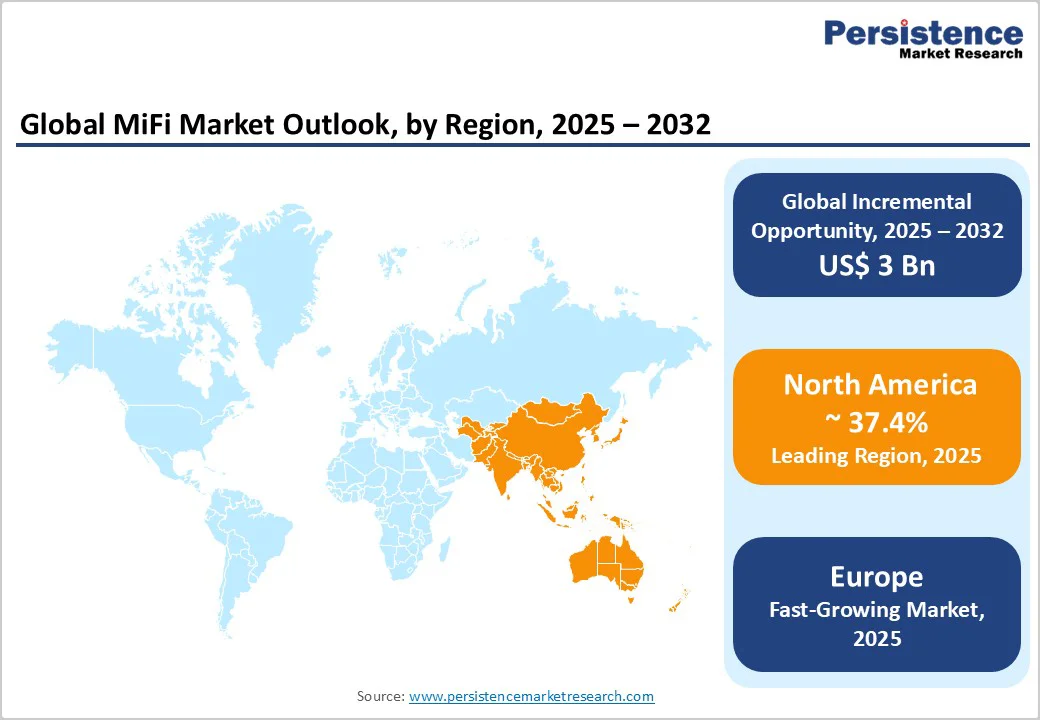

- Leading Region: North America dominates the global MiFi market, accounting for approximately 37.4% of total revenue in 2025, driven by high 5G adoption rates and advanced telecom infrastructure across the U.S. and Canada.

- Fastest-growing Region: Asia Pacific is projected to expand at the fastest pace, fueled by rising mobile internet penetration, increasing demand for affordable connectivity, and government-backed digital infrastructure programs in India, China, and Southeast Asia.

- Investment Plans: Leading manufacturers such as Inseego, Huawei, and ZTE are channeling investments exceeding US$450 Million (2024 - 2026) toward 5G-enabled MiFi development, cloud-management platforms, and AI-driven connectivity optimization to capture enterprise and consumer segments.

- Dominant Product Type: Portable consumer MiFi is expected to account for approximately 50% of unit shipments in 2025, making it the volume leader, supported primarily by carrier bundles and travel/retail channels.

- Leading Cellular Technology: 5G MiFi is projected to represent around 52% of market value in 2025, serving as the premium revenue driver.

| Key Insights | Details |

|---|---|

| MiFi Market Size (2025E) | US$2.3 Bn |

| Market Value Forecast (2032F) | US$5.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 13% |

| Historical Market Growth (CAGR 2019 to 2024) | 10.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - 5G Migration and Higher Throughput Demand

The global shift from 4G to 5G networks is a key revenue catalyst for MiFi vendors. 5G-enabled hotspots deliver significantly higher throughput and lower latency, supporting advanced use cases such as multi-user video conferencing, AR/VR testing, and field-based business continuity.

Industry forecasts link MiFi revenue growth directly to national 5G deployment timelines, with 5G hotspot shipments projected to rise at double-digit rates. As operators bundle MiFi devices with enterprise and consumer plans, average selling prices (ASPs) increase, and vendors benefit from supplementary revenue through device management and security service subscriptions.

Rise of Remote and Hybrid Work Connectivity

The post-pandemic shift toward remote and hybrid working has permanently altered connectivity needs. Enterprises now procure dedicated MiFi fleets for traveling employees, pop-up retail operations, construction sites, and disaster recovery zones.

These managed MiFi solutions offer centralized control, built-in security, and flexible SIM/eSIM management. Although enterprise unit volumes are smaller than consumer shipments, their higher per-device revenue and value-added service bundles make them disproportionately important to total market value.

Product Convergence and Evolving Form Factors

Innovation in design, integrating power banks, compact Wi-Fi 6 routers, embedded eSIMs, and global roaming features, has created new demand niches. The introduction of hybrid devices, combining power backup and hotspot functions, exemplifies this convergence trend.

These multi-use products attract both travelers and professionals who need portable connectivity with minimal friction. Product convergence enhances per-device profitability and extends retail reach into new categories such as travel accessories and outdoor gear, while giving operators opportunities to offer new subscription and roaming bundles.

Barrier Analysis - Competition from Embedded Connectivity in Smart Devices

The integration of tethering and eSIM functionality in modern smartphones and laptops has eroded the entry-level MiFi market. Users often rely on built-in mobile hotspots for occasional use, reducing demand for low-cost standalone devices.

Simultaneously, the increasing prevalence of fixed-wireless routers and 4G/5G-enabled tablets has constrained the consumer MiFi segment. This shift pressures manufacturers to focus on advanced features and enterprise-grade services rather than competing purely on price.

Regulatory Complexity and Roaming-Cost Fragmentation

Cross-border connectivity presents cost and compliance challenges. Variations in roaming fees, import duties, and radio-frequency certifications increase operational costs and extend time-to-market. In countries with roaming caps or complex regulatory frameworks, profit margins narrow by 5-10% compared to markets with harmonized standards. Such constraints limit uniform global rollouts and discourage smaller vendors from entering multi-country distribution agreements.

Opportunity Analysis - Managed MiFi Fleets and Enterprise Service Bundles

Managed MiFi fleets represent a major growth opportunity in the enterprise segment. Vendors offering device leasing, centralized management, and security integration can capture recurring revenue beyond hardware sales. Managed-service contracts typically yield 20-40% higher lifetime value per device compared with standalone hardware transactions. Expanding these offerings into mid-market enterprises and government organizations is expected to significantly enhance profitability.

Expansion in Emerging Markets and Travel Segments

Regions such as Asia Pacific, Latin America, and parts of Africa show immense growth potential where fixed broadband infrastructure remains limited. Portable Wi-Fi rental services at airports, hotels, and tourist destinations are expanding rapidly. These emerging and travel-driven markets could contribute as much as one-third of global incremental shipments through 2032, particularly when supported by local manufacturing and operator distribution partnerships.

Vertical Solutions for Industrial IoT and Public Safety

Ruggedized MiFi devices designed for utilities, emergency response, and industrial IoT deployments command premium pricing. Devices equipped with extended battery life, specialized certifications, and priority-access networking enable deployment in critical environments. Custom solutions for public safety or utility field crews can triple per-unit revenue when bundled with data plans, service-level agreements, and remote-management platforms.

Category-wise Analysis

Product Type Insights

Portable consumer MiFi devices account for roughly 50% of global shipments, driven by their compact design, affordability, and ease of use. Popular among travelers, students, and remote workers, they offer secure mobile connectivity and are often bundled with prepaid or postpaid data plans by telecom operators, enhancing accessibility in both mature and emerging markets.

Devices such as the NETGEAR Nighthawk M1, TP-Link M7350, and Huawei E5785 highlight their widespread adoption. Although their average selling price is lower than enterprise models, high-volume sales sustain market leadership. In Asia-Pacific and Latin America, affordable 4G connectivity continues to fuel consumer MiFi growth.

Hybrid MiFi devices, combining power bank functionality, SIM-based connectivity, and multi-device sharing, are experiencing the fastest growth, alongside ruggedized models designed for industrial and outdoor use. These specialized devices support emergency response, live event broadcasting, remote construction management, and off-grid operations in logistics and energy sectors.

Manufacturers such as Inseego, ZTE, and Alcatel Mobile are expanding portfolios featuring IP-rated enclosures, extended battery life, and 4G/5G support. The rising demand for reliable portable backup connectivity and outdoor digital operations is fueling adoption. With double-digit CAGRs, hybrid and rugged MiFi units represent a premium segment, offering higher ASPs, longer replacement cycles, and attractive margins for vendors and distributors.

Cellular Technology Insights

4G LTE remains the dominant cellular technology in the MiFi market, sustaining a majority share of the installed base as of 2025. Its strength lies in broad geographic coverage, device affordability, and mature infrastructure, making it the go-to connectivity option in emerging economies across India, Africa, and Southeast Asia.

Millions of users continue to rely on LTE hotspots for personal, educational, and micro-business applications, such as distance learning or rural e-commerce support. Devices such as the ZTE MF920U and JioFi 4G hotspots exemplify the category’s mass-market reach. Even as 5G expands, LTE hotspots benefit from network backward compatibility and widespread spectrum availability.

5G MiFi devices are the fastest growing, driven by the rapid deployment of mid-band and millimeter-wave networks and a surge in enterprise-grade mobility applications. These hotspots deliver gigabit-class throughput, low-latency performance, and enhanced multi-user support through Wi-Fi 6/6E integration.

Models such as the NETGEAR Nighthawk M6 Pro and Inseego MiFi X PRO 5G have become popular among remote professionals, content creators, and small enterprises requiring fiber-like wireless broadband. Telecom operators in North America, Japan, and Western Europe are leveraging 5G MiFi devices to promote premium data plans, fixed wireless access (FWA) bundles, and managed connectivity services.

Regional Market Insights

North America MiFi Market Trends - Enterprise-Driven 5G Leadership and Secure Connectivity

North America remains the largest revenue contributor with a market share of 37.4% market, supported by early 5G rollout, strong enterprise demand, and high average revenue per user (ARPU). The United States dominates regional sales, accounting for over 70% of total revenue, followed by Canada, which benefits from rising cross-border data use and remote-work adoption.

The region’s rapid migration from 4G to 5G MiFi devices, coupled with extensive operator partnerships and strong enterprise procurement, underpins its leadership position. Major telecom operators such as Verizon, AT&T, and T-Mobile actively promote MiFi-enabled mobile broadband plans for hybrid workers and SMBs. The market’s expansion is driven by robust 5G coverage across metropolitan areas, increasing demand for secure remote connectivity, and continued innovation in device management and cybersecurity.

In the U.S., for instance, Inseego and NETGEAR have launched advanced 5G MiFi models featuring integrated VPN and Wi-Fi 6E capabilities for enterprise clients. Regulatory standards, including FCC certifications and federal cybersecurity compliance, shape vendor qualification, particularly for government and critical infrastructure projects.

The competitive environment is moderately concentrated, with investment directed toward software-based management solutions and AI-driven endpoint protection. In 2025, Cradlepoint (Ericsson) expanded its enterprise device portfolio to support SD-WAN integration, strengthening its foothold in managed network services.

Europe MiFi Market Trends - SME Adoption and Tourism-Driven 4G/5G Diversity

Europe displays a diverse market structure, with Western Europe leading in 5G MiFi adoption while Central and Southern Europe remain dominated by cost-efficient 4G LTE models. High tourism rates and mobile workforces sustain consistent demand across major economies such as Germany, the U.K., France, and Spain.

Germany and the U.K. focus on enterprise-grade devices with enhanced security, while France relies on operator-bundled consumer plans. Spain and Italy experience seasonal demand peaks linked to tourism, rental connectivity, and short-term travel solutions.

Growth in the European market is supported by rising SME adoption of managed MiFi services, tourism-driven hotspot rentals, and integration of eSIM and multi-carrier connectivity technologies. Regulatory frameworks under the EU CE certification streamline cross-border trade, while data protection laws such as GDPR drive vendors to implement encrypted device management portals.

Leading telecoms, including Vodafone, Orange, and Deutsche Telekom, collaborate with OEMs such as ZTE and Huawei to offer region-specific MiFi bundles. Investment focus is shifting toward roaming optimization and advanced eSIM infrastructure. In 2024, Vodafone Germany introduced a business-grade 5G hotspot targeting remote workforce applications, marking a notable step in enterprise connectivity enhancement.

Asia Pacific MiFi Market Trends - High-Volume Production and Rapid 4G/5G Adoption

Asia Pacific is the largest MiFi market in terms of unit shipments, driven by a vast mobile broadband base, low-cost manufacturing, and a growing preference for portable connectivity. China and India collectively account for the majority of production and consumption, while Japan leads innovation in 5G hotspot technology.

China’s OEM ecosystem, including Huawei, ZTE, and TCL, supports global exports, and government-backed manufacturing initiatives enhance cost competitiveness. India’s expanding digital ecosystem, supported by Reliance Jio and Airtel, fuels the rapid adoption of affordable 4G hotspots for education, travel, and small business use.

The region’s growth is fueled by widespread 4G/5G user expansion, substitution of fixed broadband with wireless, and rising travel connectivity demand. Local manufacturing and favorable policies under programs such as India’s Make in India and China’s Smart Device Manufacturing Plan reduce import dependency and improve price accessibility.

Japan and South Korea are investing heavily in 5G mobile routers for high-speed enterprise and consumer use. In 2025, NEC Corporation and NTT Docomo jointly introduced a Wi-Fi 6E-enabled 5G MiFi solution targeting professional users, underscoring the region’s technological edge.

Competitive dynamics are diverse, with both global brands and domestic OEMs competing across premium and mass-market segments, while investments emphasize production scale-up and integration into IoT ecosystems.

Competitive Landscape

The global MiFi market features a dual structure: fragmented competition among low-cost consumer OEMs and a more concentrated segment of enterprise-focused vendors. Market leaders dominate premium 5G and managed-service categories, while a broad base of Asian manufacturers serves budget consumer demand. The shift toward service integration and fleet management is consolidating value among top-tier providers, who increasingly pursue recurring revenue models.

Dominant market themes include expansion of managed-service offerings, 5G device differentiation, and regional growth through operator alliances. Leading vendors focus on recurring revenue through device-plus-service models, while challengers compete through aggressive pricing and local distribution partnerships.

Key Industry Developments

- In April 2025, Inseego Corp. announced that four of its 5G-capable router and MiFi products had earned the “Verizon Frontline-Verified” designation, targeting mission-critical and public-safety connectivity markets.

- In April 2025, Inseego also hired wireless-industry veteran Ryan Sullivan as Senior VP of Carrier Product Management, signalling its push into carrier-channel MiFi and fixed wireless access (FWA) business.

Companies Covered in MiFi Market

- Inseego Corp.

- NETGEAR Inc.

- Huawei Technologies Co. Ltd.

- ZTE Corporation

- TP-Link Technologies Co. Ltd.

- Alcatel Mobile (TCL Communication)

- Cradlepoint (Ericsson)

- Peplink

- Sierra Wireless (Semtech Corporation)

- D-Link Corporation

- GlocalMe (uCloudlink Group Inc.)

- Franklin Wireless Corp.

- Novatel Wireless

- Skyroam Inc.

- Zyxel Communications Corp.

- Tenda Technology Inc.

- AsusTek Computer Inc.

- Samsung Electronics Co. Ltd.

- Nokia Corporation

- NEC Corporation

Frequently Asked Questions

The global MiFi market size is estimated at US$2.3 Billion in 2025, supported by rising 5G deployments, growing mobile workforce demand, and expanding IoT connectivity solutions.

By 2032, the MiFi market is projected to reach US$5.3 Billion, reflecting robust adoption of advanced 5G and enterprise-grade hotspot solutions across all major regions.

Key trends include the shift toward 5G MiFi devices, integration of eSIM and multi-carrier connectivity, AI-based device management, and increased enterprise procurement for remote and hybrid work models.

The 5G MiFi devices segment leads the market in 2025, contributing to more than 48% of total sales, driven by superior data speeds, low latency, and strong network compatibility with emerging IoT ecosystems.

The market is anticipated to grow at a CAGR of 13% between 2025 and 2032.

Major companies include Inseego Corp., Huawei Technologies Co., Ltd., ZTE Corporation, Netgear, Inc., and TP-Link Technologies Co., Ltd.