- Technology

- 4G (LTE) Devices Market

4G (LTE) Devices Market Size, Share, and Growth Forecast 2026 - 2033

4G (LTE) Devices Market by Device Type (Smartphones, Tablets, CPE / Fixed Wireless Routers, Mobile Hotspots & USB Dongles, Automotive LTE Devices, Industrial & Enterprise LTE Devices, Cellular IoT / M2M Modules), by Application, by End User, and by Regional Analysis, 2026 - 2033

4G (LTE) Devices Market Size and Trend Analysis

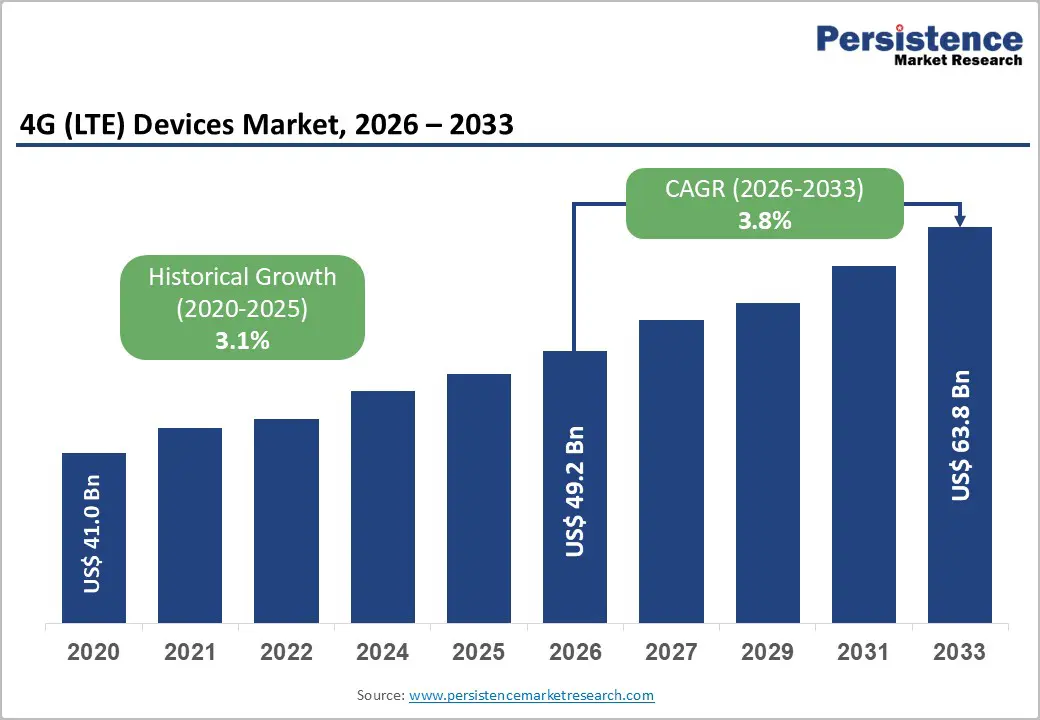

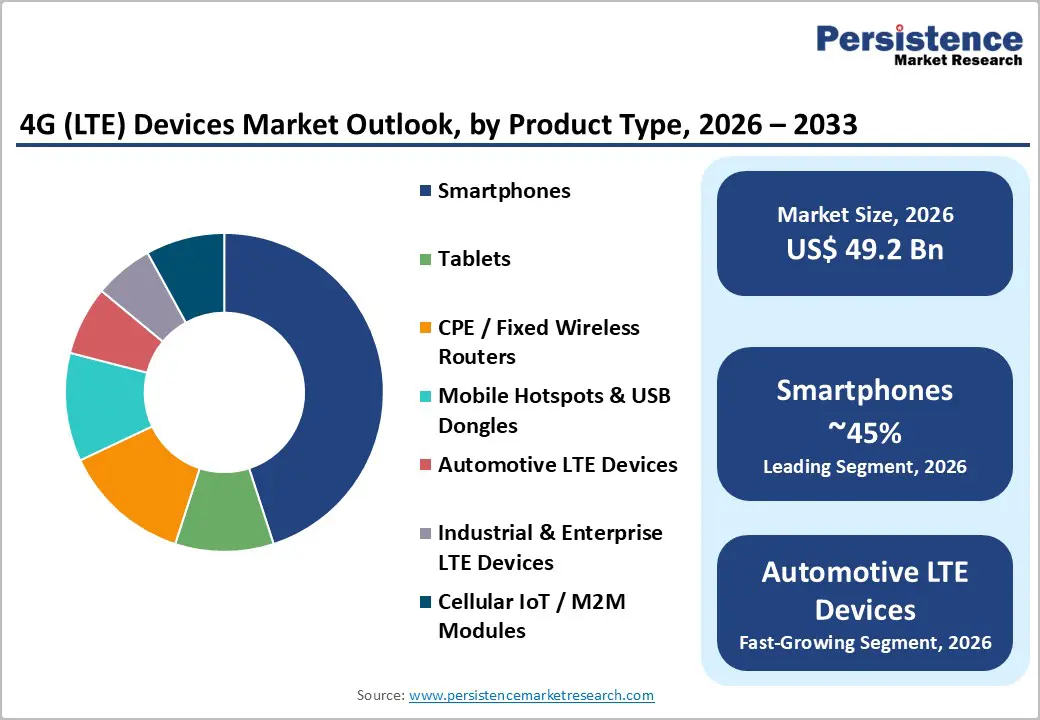

The global 4G (LTE) devices market size is likely to be valued at US$ 49.2 Billion in 2026 and is expected to reach US$ 63.9 Billion by 2033, growing at a CAGR of 3.8% during the forecast period from 2026 and 2033.

The market continues to expand due to the sustained reliance on Long-Term Evolution (LTE) networks as the primary connectivity backbone in emerging economies and industrial applications. While 5G adoption is accelerating in premium segments, 4G LTE devices remain critical for cost-sensitive markets, rural connectivity, and massive IoT deployments where low power consumption and widespread coverage are paramount.

Key Market highlights

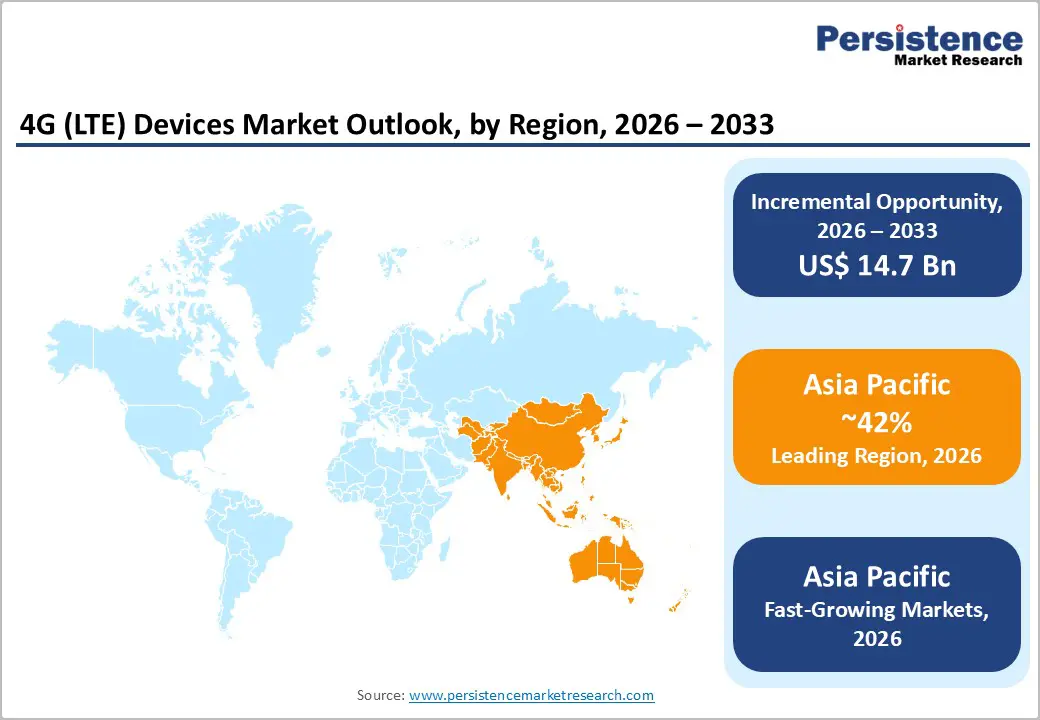

- Leading Region: Asia Pacific leads the 4G (LTE) devices market with 42% share, driven by massive consumer volumes, low-cost manufacturing, and large-scale IoT deployments.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with rising CAGR of 5.7%, supported by strong demand for affordable smartphones, industrial LTE adoption, and rapid IoT expansion.

- Dominant Segment: Smartphones remain the leading segment, holding 45% market share, accounting for the largest market share due to high volumes in entry-level and mid-range price categories.

- Fastest-Growing Segment: Cellular IoT and M2M modules are the fastest-growing segment, driven

- by smart metering, asset tracking, and industrial automation applications.

- Key Market Opportunity: Private LTE Networks for industrial and critical infrastructure offer significant revenue potential outside of the consumer market.

| Key Insights | Details |

|---|---|

| 4G (LTE) Devices Market Size (2026E) | US$ 49.2 Billion |

| Market Value Forecast (2033F) | US$ 63.9 Billion |

| Projected Growth CAGR (2026 - 2033) | 3.8% |

| Historical Market Growth (2020 - 2025) | 3.1% |

Market Dynamics

Market Growth Drivers

4G LTE Remains the Backbone for Industrial IoT, Private Networks, and Mission-Critical Infrastructure Connectivity

The rapid expansion of the Internet of Things (IoT) is strongly driving demand for 4G (LTE) devices, particularly across industrial and infrastructure applications. While consumer smartphones are rapidly transitioning to 5G, industrial users continue to rely on 4G LTE because it is proven, reliable, cost-effective, and widely deployed. Technologies such as LTE-M and NB-IoT play a central role in Industry 4.0 by enabling millions of connected sensors, smart meters, and asset-tracking devices to operate efficiently with low power consumption and long lifecycles. Manufacturing plants, utilities, transportation networks, and smart cities are increasingly deploying private LTE networks to ensure secure, stable, and wide-area connectivity.

In 2025, Huawei Technology Company Limited reinforced this trend by highlighting large-scale LTE-M and NB-IoT deployments supporting utilities and smart city infrastructure. Nationwide rollouts, such as China Telecom’s NB-IoT networks, demonstrate how mature 4G-based IoT technologies continue to serve as the backbone for mission-critical industrial systems, sustaining long-term demand for LTE modules, routers, and gateways.

Affordable 4G Devices Drive Digital Inclusion and Mass Connectivity Across Price-Sensitive Emerging Economies

In many emerging regions, including Sub-Saharan Africa, Latin America, and parts of Southeast Asia, 4G LTE remains the foundation of mobile connectivity. The high cost of deploying 5G infrastructure and the premium pricing of 5G-compatible devices make 4G the most practical and affordable solution for a large portion of the population. For billions of users, 4G smartphones act as the primary gateway to the digital economy, enabling access to mobile banking, online education, entertainment, and social platforms.

As legacy 2G and 3G networks are gradually phased out, 4G remains the most natural upgrade path, offering faster speeds at a manageable cost. This transition supports a large and stable installed base of users, sustaining demand for affordable 4G smartphones, feature phones, and mobile hotspots. Reflecting this trend, Samsung Electronics launched the Galaxy A16 LTE in South Africa in January 2025, targeting price-sensitive consumers in markets where 4G infrastructure is already widespread and economically efficient.

Market Restraints

Rapid 5G Adoption and Spectrum Re-farming Reduce Long-Term Growth Potential for Consumer 4G Devices

The rapid commercialization of 5G networks is a major restraint on the 4G (LTE) Devices Market, particularly in consumer electronics. Mobile operators in North America, Europe, and China are prioritizing investments in 5G and actively refarming spectrum previously allocated to 4G to support new 5G services. This shift reduces the long-term efficiency of 4G-only devices and encourages consumers to migrate toward 5G-capable handsets.

5G handset shipments have already surpassed 4G shipments in several key markets, including India, where 5G devices accounted for approximately 79% of total smartphone sales. This rapid transition places pressure on original equipment manufacturers to scale back production of pure 4G devices. As a result, market value growth in premium and mid-range 4G segments is constrained, limiting the overall expansion potential of the LTE device ecosystem in developed markets.

Chipset Manufacturers’ Focus on 5G Accelerates Supply Constraints and Obsolescence of Standalone 4G Devices

Semiconductor manufacturers are increasingly prioritizing high-margin 5G chipsets over legacy 4G components, creating supply-side challenges for the LTE device market. Leading chipset vendors such as Qualcomm and MediaTek are allocating advanced manufacturing nodes, including 3nm and 4nm processes, primarily to 5G System-on-Chips. In contrast, 4G chipsets are largely produced on older nodes, limiting innovation and efficiency improvements. This strategic shift reduces economies of scale for 4G components and contributes to tighter supply conditions.

As a result, the price gap between entry-level 5G smartphones and high-end 4G devices continues to narrow. Consumers seeking longer device lifecycles increasingly favor 5G-enabled products, even in price-sensitive segments. This supply chain prioritization accelerates the obsolescence of standalone 4G devices and reduces their competitiveness, driving a faster market transition than demand-side factors alone would otherwise produce.

Market Opportunities

Rising Private LTE Adoption Fuels Demand for Rugged, Secure Connectivity Across Critical Infrastructure Sectors

Private LTE is emerging as a significant growth opportunity across critical infrastructure sectors such as utilities, mining, oil and gas, ports, transportation, and public safety. These industries often operate in remote or harsh environments where public mobile networks are unreliable or unavailable. Private LTE provides secure, dedicated, and high-performance connectivity that is more practical and cost-effective than deploying full private 5G networks. As a result, utilities and energy companies are modernizing their communication systems using LTE-based solutions that deliver wide-area coverage, strong signal penetration, and consistent performance.

This shift is generating strong demand for rugged, industrial-grade LTE devices, including intrinsically safe smartphones, routers, and mobile computing platforms. In 2025, Panasonic Corporation reinforced this trend by positioning its fully rugged TOUGHBOOK 40 laptop for mission-critical use across utilities, policing, and field services. With support for private LTE networks such as CBRS and FirstNet, the device highlights the growing importance of rugged LTE endpoints within private network ecosystems.

4G LTE Continues to Power Cost-Effective Telematics and Connected Vehicle Services in Mass-Market Automotive

The automotive sector continues to present a strong opportunity for 4G LTE devices through telematics and connected vehicle services. While autonomous driving and advanced driver assistance systems are driving long-term interest in 5G, most currently deployed connected vehicle features operate efficiently on mature LTE networks. Services such as fleet management, emergency eCall systems, infotainment, remote diagnostics, and over-the-air software updates do not require ultra-low latency or high data rates. As a result, 4G LTE remains a cost-effective and reliable solution for mass-market vehicles.

Automakers continue to integrate LTE-based telematics control units to meet regulatory requirements and customer expectations without significantly increasing vehicle costs. HARMAN, a subsidiary of Samsung Electronics, showcased its Ready Connect telematics platform, designed to operate on 4G LTE today and support future upgrades to 5G. This modular approach enables scalable deployment and reinforces the long-term relevance of LTE in automotive connectivity beyond 2025.

Category-wise Insights

Device Type Analysis

Smartphones are the leading subsegment within the Device Type category, accounting for approximately 45% of the total 4G (LTE) devices market share. This dominance is driven by extremely high shipment volumes, particularly in emerging markets where affordability and wide LTE coverage remain critical. While premium consumers are shifting toward 5G, entry-level and mid-range 4G smartphones continue to sell at scale in regions such as India, Africa, Southeast Asia, and Latin America. These devices serve as the primary gateway to digital services including communication, payments, entertainment, and education. Continuous replacement of feature phones with smartphones further supports volume growth, ensuring that LTE smartphones remain the largest contributor to overall device demand.

Application Analysis

Consumer Communication and Data is the leading application subsegment, representing approximately 60% of total market demand. This leadership is driven by the everyday use of 4G LTE devices for voice calls, messaging, video streaming, social media, and mobile internet access. A massive global user base continues to rely on LTE networks due to their affordability, reliability, and extensive coverage. In emerging markets, 4G remains the primary mobile broadband technology, while in advanced markets it functions as the fallback and coverage layer. High data consumption frequency, recurring usage patterns, and a large installed base of LTE smartphones make consumer communication the most dominant and stable application area within the 4G LTE ecosystem.

End User Analysis

Consumers are the leading end-user subsegment, accounting for approximately 65% of total 4G LTE device demand worldwide. This dominance stems from widespread ownership of LTE smartphones, tablets, and personal mobile hotspots used for communication, entertainment, and internet access. In developing regions, consumers depend heavily on 4G devices as their primary digital interface for banking, education, e-commerce, and social engagement. The affordability of LTE devices compared to 5G alternatives continues to support strong adoption. Additionally, the ongoing phase-out of 2G and 3G networks sustains demand for replacements. Although enterprise and industrial usage are growing, the sheer volume of consumer-owned devices ensures consumers remain the largest end-user segment.

Regional Insights

North America 4G (LTE) Devices Market Trends

The North American market is defined by a mature telecommunications ecosystem where 4G LTE has evolved into a critical coverage layer rather than the primary network. A key trend is the shutdown of legacy 2G and 3G networks, which has firmly established 4G as the baseline for voice and data services. While consumer smartphone sales are heavily skewed toward 5G, strong demand persists for LTE devices in industrial and enterprise applications.

Private LTE deployments using CBRS spectrum are gaining traction in sectors such as energy, logistics, and manufacturing. Major carriers like Verizon and AT&T continue to maintain robust LTE networks to support millions of existing IoT devices that are not expected to migrate to 5G in the near term. This ensures sustained procurement of 4G modules, routers, and industrial endpoints across the region.

Europe 4G (LTE) Devices Market Trends

In Europe, the 4G LTE Devices Market is shaped by strict regulatory frameworks and coordinated digital infrastructure development. Countries such as Germany, the U.K., and France use LTE as a reliable solution for rural broadband initiatives where fiber deployment faces delays. The automotive sector plays a significant role, supported by Europe’s strong manufacturing base.

Automakers continue to embed 4G telematics units to enable predictive maintenance, vehicle diagnostics, and connected services. Additionally, the widespread shutdown of 3G networks across the region is driving a large-scale replacement cycle for legacy M2M hardware. Utilities and industrial operators are upgrading to 4G-enabled routers and smart meters to ensure service continuity. These factors collectively sustain demand for LTE devices despite the parallel expansion of 5G networks.

Asia Pacific 4G (LTE) Devices Market Trends

Asia Pacific remains the largest volume market for 4G LTE devices, driven by population scale and diverse economic conditions across China, India, and ASEAN countries. In India, 4G smartphones continue to dominate the sub-US$150 segment, which represents a substantial portion of total device shipments despite rapid 5G rollout.

The region also serves as a global manufacturing hub, supporting strong adoption of industrial LTE solutions for factory automation and logistics. China leads global cellular IoT deployments, with millions of NB-IoT and LTE-M modules used in smart city applications. The availability of low-cost components from regional suppliers enables manufacturers to maintain competitive pricing. As a result, Asia Pacific continues to generate high LTE device volumes even as advanced markets gradually plateau.

Competitive Landscape

Market Structure Analysis

The 4G (LTE) Devices Market is moderately consolidated, with a few global technology giants dominating the high-volume smartphone and tablet categories, while the industrial and IoT segments remain more fragmented with specialized players. Leading companies like Samsung Electronics and Apple Inc. command the consumer space but are aggressively pivoting to 5G, leaving the long-tail 4G market to value-focused brands like Xiaomi Inc. and Lenovo Group Limited. In the industrial domain, competition centers on module reliability and longevity. Market leaders are differentiating themselves by offering "ruggedized" devices and enterprise-grade security features (such as Samsung's Knox or Panasonic's Toughbook line). Emerging business models include "Device-as-a-Service" for enterprise IoT, allowing companies to bundle hardware with connectivity and management software.

Key Market Developments

- In February, 2024: Samsung Electronics, through its subsidiary HARMAN, unveiled the "Ready Connect 5G TCU" but confirmed continued support and production of advanced LTE-based Telematics Control Units to support mass-market vehicle tiers that do not yet require 5G bandwidths.

- In October, 2024: Huawei Technology Company Limited announced the integration of AI-driven optimization tools for its existing 4G LTE core networks, ensuring that industrial clients using Private LTE can achieve 5G-like latency and reliability without immediate hardware overhauls.

- In November, 2024: Panasonic Corporation updated its Toughbook 40 series to feature modular connectivity packs that support dedicated 4G LTE bands (including Band 14 for FirstNet), catering specifically to public safety agencies that rely on LTE for mission-critical communications.

Companies Covered in 4G (LTE) Devices Market

- Apple Inc.

- Samsung Electronics

- ZTE Corporation

- Huawei Technology Company Limited

- Lenovo Group Limited

- ASUSTek Computer, Inc.

- Xiaomi Inc.

- LG Electronics Inc.

- Panasonic Corporation

- Nokia Corporation

- Sony Group Corporation

- HTC Corporation

Frequently Asked Questions

The global market is projected to reach US$ 63.9 Billion by 2033, growing at a CAGR of 3.8% from 2026 to 2033.

Key drivers include the expansion of the Internet of Things (IoT), the deployment of Private LTE networks in industrial sectors, and the affordability of 4G devices in emerging markets.

The Smartphones segment currently dominates the market, accounting for the largest share of revenue due to widespread global adoption and replacement cycles.

Asia Pacific is expected to lead the market, driven by high manufacturing output, large population bases in India and China, and continued infrastructure investments.

A significant opportunity lies in the Private LTE sector for industries such as mining, utilities, and manufacturing, which require secure and reliable dedicated networks.

Key players include Samsung Electronics, Apple Inc., Huawei Technology Company Limited, Xiaomi Inc., and ZTE Corporation, among others.