- Medical Devices

- Menstrual Cups Market

Menstrual Cups Market Size, Share, and Growth Forecast, 2025 - 2032

Menstrual Cups Market By Product Type (Disposable, Reusable), Material Type (Medical-Grade Silicone, Thermoplastic Elastomer), Design (Bell-Shaped, Round-Shaped), Distribution Channel (Online Sales, Offline Sales), and Regional Analysis for 2025 - 2032

Menstrual Cups Market Size and Trends Analysis

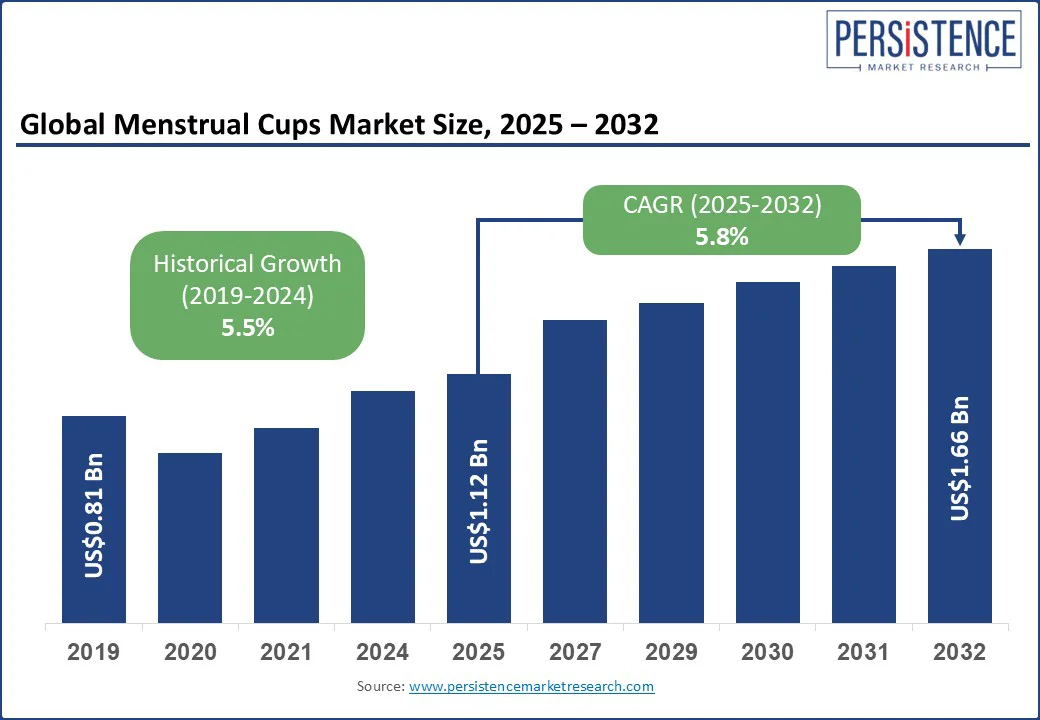

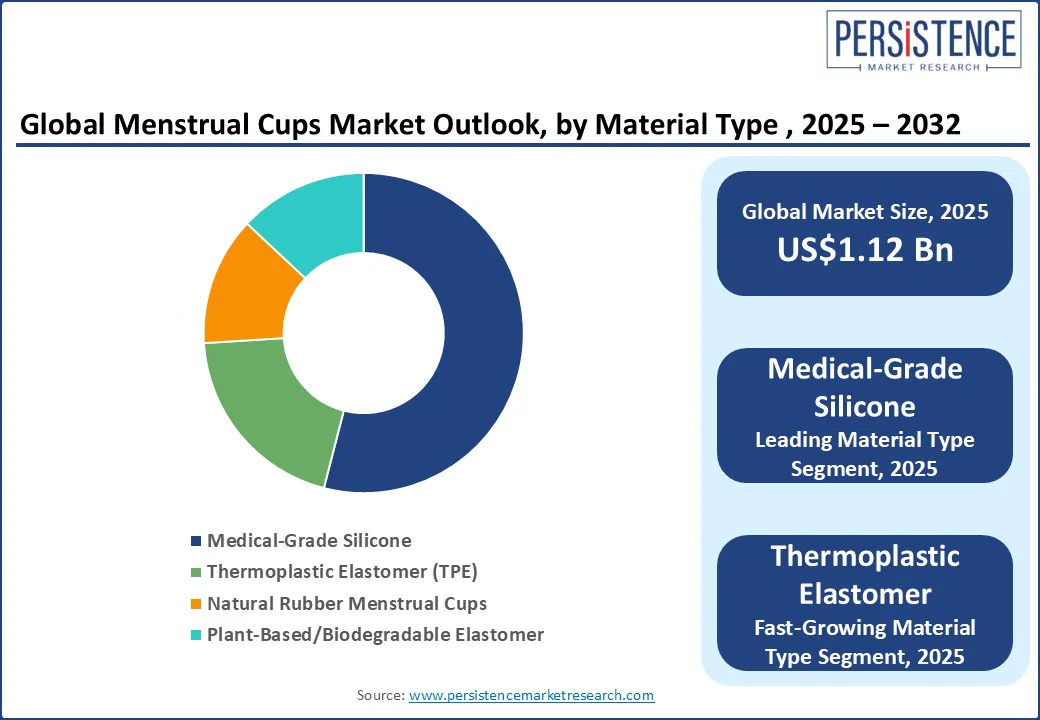

The global menstrual cups market size is projected to rise from US$1.12 Bn in 2025 to US$1.66 Bn by 2032. It is anticipated to witness a CAGR of 5.8% during the forecast period from 2025 to 2032.

The menstrual cups industry is gaining momentum as consumers increasingly shift toward sustainable, cost-effective, and eco-friendly menstrual hygiene solutions. Rising awareness about the environmental impact of disposable sanitary products, coupled with growing advocacy for women’s health and menstrual equity, is driving adoption across both developed and emerging economies.

Key Industry Highlights

- Leading Region: North America is projected to hold a 38% market share in 2025, supported by strong retail penetration, well-established menstrual health education programs, and high consumer willingness to adopt sustainable hygiene products.

- Fastest-growing Region: Asia Pacific is anticipated to grow at the highest CAGR due to rapid urban adoption, government-backed awareness campaigns, and rising e-commerce accessibility in countries including India and China.

- Dominant Product Type: Reusable menstrual cups are anticipated to account for over 82% share in 2025, driven by durability, cost-effectiveness, and sustainability benefits.

- Leading Material Type: Medical-grade silicone menstrual cups are expected to lead, with a 54% market share in 2025, owing to their hypoallergenic properties, durability, and compliance with health safety standards.

|

Global Market Attribute |

Key Insights |

|

Menstrual Cups Market Size (2025E) |

US$1.12 Bn |

|

Market Value Forecast (2032F) |

US$1.66 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.5% |

Market Dynamics

Driver - Targeted Distribution, Product Innovation, and Sustainable Design Boost Adoption

Public procurement and NGO campaigns are increasingly introducing menstrual cups into communities in the emerging economies, including India. Kerala’s Thinkal rollout stands out as a leading example of government-funded distribution programs in India.

This initiative pairs the free provision of medical-grade silicone menstrual cups with hands-on training, significantly improving the adoption rates. Recent systematic reviews and field trials consistently report high safety and user satisfaction following proper training, reinforcing the acceptability of menstrual cups in low- and middle-income countries.

Manufacturing at scale, combined with automation, reduces unit costs. OEM listings and molding machine data demonstrate how automation in menstrual cup production drives down per-unit costs, making a wholesale price of US$1 achievable.

Contract manufacturers offer menstrual cups for a fraction of a dollar, enabling cost-effective private-label market entry. Brands use a direct-to-consumer menstrual cup subscription model and starter kits to cut adoption friction. Brands such as DivaCup offer starter kits that include different cup sizes and accessories to help users find the right fit, addressing a key concern for first-time users. Easy online ‘how-to’ content, returns, and trial bundles speed purchase decisions and broaden mainstream reach.

The rise of biodegradable menstrual cups, made from plant-based elastomers, is creating a niche for eco-conscious consumers seeking zero-waste menstrual care. Brands Heyday and Carmesi are leveraging compostable packaging and certified sustainable materials to appeal to green product enthusiasts, while aligning with tightening regulations on single-use plastics in hygiene products.

Restraint - Absence of standardization, Cultural Barriers, and Infrastructure Gaps Limit Uptake

The absence of standardized firmness classification for menstrual cups leads to frequent complaints of mismatch, as brands vary significantly in diameter, capacity, and stiffness. This inconsistency leads to significant brand-to-brand variation in menstrual cup diameter, often causing poor fit, leakage issues, and higher return rates. Clinical observations and cohort studies have also linked improper removal techniques to the menstrual cup-related and IUD expulsion risk, prompting some healthcare providers to be cautious in their recommendations. In addition, preliminary research has noted potential pelvic floor discomfort or urinary symptoms in sensitive users after prolonged use, further influencing product acceptance.

Cleaning and reuse remain heavily dependent on access to clean water and private facilities, which creates significant menstrual cup cleaning barriers in low-resource settings. The lack of discreet washing areas, especially in public toilets, limits user confidence and long-term adoption. Cultural norms in certain regions reinforce virginity-associated internal device stigma, particularly among adolescents, leading to resistance to trying the product. Moreover, inadequate training and limited awareness among healthcare workers reduce clinic-level advocacy, slowing the overall scale-up of menstrual cup adoption in underserved markets.

Opportunity-Targeted Distribution, Product Innovation, and Sustainable Design Boost Adoption

School-based and community distribution programs present a strong growth opportunity when combined with proper training and follow-up support. Randomized and cluster trials demonstrate that providing cups alongside hands-on sessions significantly increases acceptability, reduces trial abandonment, and can even improve school attendance among adolescent girls.

Initiatives that integrate menstrual cup adoption into school-based menstrual health programs and use local peer champions have proven effective in converting trial users into consistent, long-term users. Field evidence also shows that trained community promoters can normalize internal menstrual products and help shorten the learning curve for first-time users.

The expansion of e-commerce and strategic product bundling is streamlining the purchasing process for new consumers. Offering starter kits, detailed how-to guides, and a menstrual cup starter kit subscription model have increased first-time conversions while reducing product returns.

Growing interest in the plant-based rubber biodegradable menstrual cup is fueling a premium, eco-friendly segment, supported by compostable packaging and sustainability certifications. At the same time, advancements in LSR injection molding and automated production lines are driving down per-unit costs, creating attractive private-label opportunities for NGOs, healthcare distributors, and major retailers.

Category-wise Analysis

Product Type Insights

Reusable menstrual cups hold the dominant position in the market with an estimated market share of around 82% in 2025. Their popularity stems from a combination of cost savings, durability, and environmental benefits, as a single cup can last up to 10 years. Consumers are increasingly seeking waste-reducing alternatives to disposable sanitary products, and reusable cups fit this shift perfectly.

Education campaigns by NGOs and healthcare providers have further boosted confidence in their safety and ease of use. The long replacement cycle also makes them more appealing to price-conscious buyers, strengthening their lead in both developed and emerging markets. For example, DivaCup is one of the most widely recognized and globally distributed reusable menstrual cups, popular in North America and Europe.

Disposable menstrual cups account for roughly 15% of the market and are the fastest-growing product type. Their appeal stems from single-use convenience, which resonates with first-time users who may be hesitant about cleaning and reusing cups. They are especially favored for travel, emergencies, and situations with limited access to washing facilities.

The development of biodegradable disposable models is further enhancing their acceptance among eco-conscious consumers who want both convenience and sustainability. Flex Softcup line includes disposable or limited-use menstrual cups made from thin, flexible material designed to be used once or a few times. These are often sold as single-use alternatives for situations such as travel.

Material Type Insights

Medical-grade silicone menstrual cups are anticipated to dominate the material segment, with a market share of 54% in 2025. Their leadership is rooted in superior safety, as silicone is hypoallergenic, non-porous, and compliant with global medical standards.

This material offers a comfortable fit, flexibility, and resilience, making it a trusted choice for both healthcare professionals and end-users. Its longevity also contributes to strong consumer loyalty, as cups made from medical-grade silicone can last for years without degrading in performance.

Thermoplastic elastomer (TPE) menstrual cups are witnessing the fastest growth in the material category, with a high CAGR through 2032. TPE offers a softer, more flexible structure, making it comfortable for first-time users and suitable for customization.

Its recyclability and lower production costs allow brands to target price-sensitive markets while still offering a safe and reliable product. The adaptability of TPE to varied manufacturing processes also enables innovative product designs, fueling its rapid adoption in both mid-range and entry-level product lines.

Regional Insights

North America Menstrual Cups Market Trends - Widespread Retail Availability and Health Education Growth

North America is projected to dominate the menstrual cups market, holding nearly 38% of global sales in 2025, driven by high disposable incomes, a strong brand presence, and extensive retail distribution. In the U.S., major retailers such as Walmart and Target, alongside pharmacy chains, have played a pivotal role in positioning menstrual cups as a mainstream hygiene option. Companies, including The Flex Company, have broadened their offerings with biodegradable variants and compact single-use cups aimed at first-time users who may be hesitant about reusable products.

Canada is experiencing growth through innovative designs such as the Bfree Cup, which incorporates antimicrobial technology and eliminates the need for boiling, an advantage for rural communities and individuals with limited access to private washing facilities. Retail expansion, coupled with sustained consumer education efforts, continues to strengthen North America’s leadership in the global market.

Asia Pacific Menstrual Cups Market Trends - Rapid Urban Adoption and Growing Awareness through Grassroots Programs

Asia Pacific remains the fastest-growing region with a projected high CAGR, benefiting from large population bases, rising menstrual health awareness, and rapid adoption of e-commerce channels. In India, the Sirona Hygiene Foundation launched a menstrual cup campaign across 25 villages in Uttarakhand, partnering with DivIn Pro. The effort included menstrual hygiene education, hands-on training sessions, distribution of 3,100 free menstrual cups, and the establishment of a dedicated helpline for user support.

Urban markets are experiencing strong growth from direct-to-consumer brands leveraging social media and influencer partnerships to target younger demographics. China is leveraging its private-label manufacturing strengths to produce both affordable TPE cups and high-end silicone products. Sales on platforms such as Tmall and JD.com are amplified through livestream shopping events and influencer-driven campaigns, helping normalize menstrual cup use. Rapid manufacturing capabilities also allow for continuous product innovation tailored to the diverse needs of regional consumers.

Europe Menstrual Cups Market Trends - Eco Trends and Evolving Hygiene Regulations

Europe represents a mature and regulation-driven menstrual cups market. Medical-grade silicone products dominate due to strict health standards and consumer trust in certified materials. The U.K. benefits from strong retail penetration through pharmacy chains such as Boots and Lloyds, complemented by active direct-to-consumer engagement from established brands.

Educational initiatives in schools and collaborations with healthcare professionals are proving effective in increasing adoption among younger users. Germany stands out as one of the fastest-growing European markets, with consumers showing a preference for technically advanced designs, such as adjustable stems and multiple firmness levels, produced by domestic innovators like Me Luna and Merula. The country’s widespread pharmacy network and willingness to invest in premium, safety-certified products have positioned it as a high-value hub within Europe’s menstrual cup sector.

Competitive Landscape

The global menstrual cups market is moderately consolidated, with a mix of global brands and region-specific players competing through product innovation, material quality, and targeted marketing. Leading companies such as Diva International, Lunette, Mooncup Ltd., and The Flex Company focus on expanding product portfolios with medical-grade silicone designs, biodegradable variants, and collapsible travel cups. Strategic partnerships with retail chains, health organizations, and NGOs have helped these brands strengthen market penetration, particularly in North America and Europe, where brand trust and certification standards drive consumer preference.

Emerging regional players in Asia Pacific and Latin America are increasingly disrupting the market by offering affordable, high-quality alternatives through e-commerce platforms. Many leverage localized marketing strategies, community workshops, and culturally adapted product designs to overcome adoption barriers.

Manufacturers in China and India, such as Sirona Hygiene Private Limited, in particular, are gaining ground by combining low-cost production with rapid product customization, allowing them to supply both domestic markets and international private-label contracts. This dynamic competition is pushing established brands to innovate faster while expanding into untapped demographic segments.

Key Industry Developments

- In February 2024, Diva International introduced a softer menstrual cup specifically designed for first-time users and individuals with sensitive pelvic muscles, leading to a 15% sales boost within six months.

- In February 2024, Saalt launched a plant-derived biodegradable menstrual cup. The launch was accompanied by a digital awareness campaign targeting environmentally conscious millennials and Gen Z consumers, leveraging social media influencers and educational content to emphasize the product’s benefits and its role in reducing environmental impact.

Companies Covered in Menstrual Cups Market

- Diva International Inc.

- Saalt LLC

- Lunette Menstrual Cup

- Mooncup Ltd

- AllMatters

- MeLuna GmbH

- Ruby Cup

- FLEX Company

- Intimina

- Sirona Hygiene Private Limited

- Cora

- Hey Girls CIC

- FemmyCycle

- Kind Cup

- Mahina Cup

- Tupperware Brands

- SckoonCup

- BeYou Cup

- IrisCup

- Pixie Cup

Frequently Asked Questions

The menstrual cups market is projected to reach US$ 1.12 Bn in 2025.

By 2032, the menstrual cups market is expected to grow to US$ 1.66 Bn.

Key trends include the rise of biodegradable menstrual cups, increasing adoption among urban millennials through e-commerce channels, and growing integration of menstrual health education in schools.

The reusable menstrual cups segment leads the market with over 82% share in 2025, driven by sustainability concerns, long-term cost savings, and broad product availability.

The menstrual cups market is anticipated to grow at a CAGR of 5.8% from 2025 to 2032, supported by increased awareness and eco-conscious consumer choices.

Major players with strong product portfolios include Diva International Inc., Saalt LLC, Lunette, Mooncup Ltd, and The Flex Company.